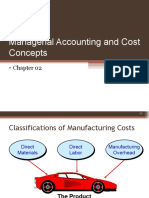

Act 202. Chap002

Act 202. Chap002

You might also like

- The Players Guide To Text Game Ebook PDFDocument69 pagesThe Players Guide To Text Game Ebook PDFMatt Smith100% (3)

- The Ultimate Guide To Texting GirlsDocument41 pagesThe Ultimate Guide To Texting Girlspocketmint79% (14)

- Unit 2 Standard Test ADocument2 pagesUnit 2 Standard Test Assaruskax50% (2)

- CH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisDocument84 pagesCH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisankonmahmudNo ratings yet

- 3.1.1.2 Lab - My Protocol RulesDocument2 pages3.1.1.2 Lab - My Protocol Rulessupiyandir100% (1)

- Sms Sending Job DetailsDocument2 pagesSms Sending Job DetailsLofojayNo ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost Concepts027 - Dyan Febita SariNo ratings yet

- Chap 002Document18 pagesChap 002Hafsa JawedNo ratings yet

- Chap002 - Manag AccDocument28 pagesChap002 - Manag AccSandra RohandiNo ratings yet

- Chap002 - Manag Acc & Cost ConceptDocument29 pagesChap002 - Manag Acc & Cost Conceptlilis astriyani sinagaNo ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsTouhid TomalNo ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost Conceptsginish12No ratings yet

- Design CostDocument21 pagesDesign CostDr. Ashish AggarwalNo ratings yet

- Cost ConceptsDocument18 pagesCost Conceptsmuttakin106No ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsrisaNo ratings yet

- Managerial Accounting Chapter 2Document61 pagesManagerial Accounting Chapter 2Wajeeh RehmanNo ratings yet

- Managerial Accounting Chap 2Document72 pagesManagerial Accounting Chap 2Sankary CarollNo ratings yet

- Managerial Accounting and Cost ConceptsDocument44 pagesManagerial Accounting and Cost ConceptsQUANG NGUYỄN VINHNo ratings yet

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost ConceptsBobbles D LittlelionNo ratings yet

- Basicconceptsofcostaccounting 141207032058 Conversion Gate02Document53 pagesBasicconceptsofcostaccounting 141207032058 Conversion Gate02sajjadNo ratings yet

- Basic Concepts of Cost AccountingDocument51 pagesBasic Concepts of Cost AccountingMary ANo ratings yet

- Managerial Accounting and Cost ConceptsDocument57 pagesManagerial Accounting and Cost ConceptsFrances Monique AlburoNo ratings yet

- Cost Terms, Concepts, and ClassificationsDocument22 pagesCost Terms, Concepts, and ClassificationsKi xxiNo ratings yet

- Basic Concepts of Cost AccountingDocument53 pagesBasic Concepts of Cost AccountinghasnainNo ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsadamNo ratings yet

- Managerial Accounting and Cost ConceptsDocument19 pagesManagerial Accounting and Cost ConceptsFarhan RabbehNo ratings yet

- Basic Concepts of Cost AccountingDocument51 pagesBasic Concepts of Cost AccountingImran KhanNo ratings yet

- Cost Term, Concept and ClassificationsDocument28 pagesCost Term, Concept and ClassificationskumarNo ratings yet

- Garrison Lecture Chapter 2Document61 pagesGarrison Lecture Chapter 2Ahmad Tawfiq Darabseh100% (2)

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost Conceptshaccp bkipmNo ratings yet

- Chapter 2 Managerial Accounting and Cost ConceptsDocument49 pagesChapter 2 Managerial Accounting and Cost ConceptsFarihaNo ratings yet

- SPPTChap 002Document19 pagesSPPTChap 002Ibrahim Elmorsy Maintenance - 3397No ratings yet

- Chapter - 2 - Managerial Accounting and Cost ConceptDocument61 pagesChapter - 2 - Managerial Accounting and Cost ConceptSoka PokaNo ratings yet

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost ConceptsAmer Wagdy GergesNo ratings yet

- SPPTChap 002Document16 pagesSPPTChap 002saharinshakib7505No ratings yet

- Dwnload Full Managerial Accounting 2nd Edition Garrison Solutions Manual PDFDocument35 pagesDwnload Full Managerial Accounting 2nd Edition Garrison Solutions Manual PDFwoollyprytheeuctw100% (11)

- Managerial Accounting 2nd Edition Garrison Solutions ManualDocument35 pagesManagerial Accounting 2nd Edition Garrison Solutions Manualiramitchellwnumr100% (28)

- Managerial Accounting 15th Edition Garrison Solutions ManualDocument35 pagesManagerial Accounting 15th Edition Garrison Solutions Manualreneestanleyf375h100% (27)

- Managerial Accounting 2nd Edition Garrison Solutions ManualDocument25 pagesManagerial Accounting 2nd Edition Garrison Solutions ManualMaryBalljswt100% (54)

- Introduction To Cost ManagementDocument31 pagesIntroduction To Cost ManagementVINCENT GAYRAMONNo ratings yet

- 1b - Cost Concepts and Terminology - 14sept06Document31 pages1b - Cost Concepts and Terminology - 14sept06Zaid AnsariNo ratings yet

- Managerial Accounting and Cost ConceptsDocument48 pagesManagerial Accounting and Cost ConceptsKirei MinaNo ratings yet

- Managerial Accounting 15th Edition Garrison Solutions ManualDocument25 pagesManagerial Accounting 15th Edition Garrison Solutions ManualKatherineJohnsonDVMinwp100% (60)

- Slide Chapter 2Document65 pagesSlide Chapter 2daoviethung29No ratings yet

- Managerial Accounting For Managers 3rd Edition Noreen Solutions ManualDocument35 pagesManagerial Accounting For Managers 3rd Edition Noreen Solutions Manualrenewerelamping1psm100% (29)

- Act 202 Chapter 2Document52 pagesAct 202 Chapter 2Shaon KhanNo ratings yet

- 02-Cost-Terms-Concepts-and-Behavior - Managerial AccountingDocument58 pages02-Cost-Terms-Concepts-and-Behavior - Managerial Accountingsabrina jane falconNo ratings yet

- An Introduction To Cost Terms and PurposesDocument33 pagesAn Introduction To Cost Terms and PurposesAi LatifahNo ratings yet

- Acct Cost ConceptsDocument52 pagesAcct Cost ConceptsLauNo ratings yet

- 4 Chapter20Document40 pages4 Chapter20154 ahmed ehabNo ratings yet

- Cost ConceptsDocument56 pagesCost ConceptsAngela De chavezNo ratings yet

- CH 5Document21 pagesCH 5hohrmpm2No ratings yet

- Managerial Accounting and Cost Concepts: Chapter TwoDocument63 pagesManagerial Accounting and Cost Concepts: Chapter TwoMd Hasibul Karim 1811766630No ratings yet

- 02 MAS - Cost ConceptDocument10 pages02 MAS - Cost ConceptKarlo D. ReclaNo ratings yet

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost ConceptsFederico SalernoNo ratings yet

- COST ESTIMATION A Class Lecture by Rashid Hussain 1657763473Document55 pagesCOST ESTIMATION A Class Lecture by Rashid Hussain 1657763473HiteshSandhalNo ratings yet

- Chapter 2Document10 pagesChapter 2Aklil TeganewNo ratings yet

- Cost Concept and ClassificationDocument45 pagesCost Concept and ClassificationMountaha0% (1)

- Managerial Accounting and Cost Concepts: Learning Objective 1Document15 pagesManagerial Accounting and Cost Concepts: Learning Objective 1Sinh TrầnNo ratings yet

- 2 - Cost Concepts and BehaviorsDocument4 pages2 - Cost Concepts and BehaviorsKaryl FailmaNo ratings yet

- MS03 - Cost Behavior and Cost Classification PDFDocument12 pagesMS03 - Cost Behavior and Cost Classification PDFTina PascualNo ratings yet

- Chapter 2 UpdatedDocument58 pagesChapter 2 Updatedbing bongNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Mobile Learning For TeachersDocument22 pagesMobile Learning For TeachersNeuber Silva FerreiraNo ratings yet

- Ishii Et Al-2019-Human Behavior and Emerging TechnologiesDocument8 pagesIshii Et Al-2019-Human Behavior and Emerging TechnologiesYuni Novianti Marin MarpaungNo ratings yet

- Mobile Phone and YouthDocument37 pagesMobile Phone and YouthVisruth K Ananad33% (3)

- Exercise READING SKILLSDocument3 pagesExercise READING SKILLSRirin DamayantiNo ratings yet

- Internet Slang and SMS (Texting) LanguageDocument7 pagesInternet Slang and SMS (Texting) LanguageHarley LausNo ratings yet

- Chapter 5 BehaviorDocument65 pagesChapter 5 BehaviorDavid ArtunduagaNo ratings yet

- Epr-T ANGLAIS - Copie-1 - CopieDocument22 pagesEpr-T ANGLAIS - Copie-1 - CopiePatrick NdayisabaNo ratings yet

- Case 3 AT&TDocument3 pagesCase 3 AT&TmaxNo ratings yet

- G7 English Lesson Exemplar 1st Quarter PDFDocument80 pagesG7 English Lesson Exemplar 1st Quarter PDFMark C. Gutierrez90% (30)

- Modul Bahasa Inggris 2 - Unit 6 - Rev 2019Document16 pagesModul Bahasa Inggris 2 - Unit 6 - Rev 2019Dhana ChompNo ratings yet

- The Relationship Between Smartphone Use & Academic Performance PDFDocument13 pagesThe Relationship Between Smartphone Use & Academic Performance PDFjeckNo ratings yet

- Michelle Carter Appellant Carter Reply BriefDocument12 pagesMichelle Carter Appellant Carter Reply BriefSyndicated NewsNo ratings yet

- Virgin Phone GuideDocument17 pagesVirgin Phone GuideMichael RuaneNo ratings yet

- The ProblemDocument40 pagesThe ProblemAllen Timtiman BisqueraNo ratings yet

- ProjectDocument18 pagesProjectDigvijay Singh100% (4)

- No Telkomsel Number Other Party Type DateDocument24 pagesNo Telkomsel Number Other Party Type DateHaryanto MarsakapNo ratings yet

- Discursive EssayDocument3 pagesDiscursive EssayLyubomira LyubenovaNo ratings yet

- Coronavirus (Covid 19) Prevention Measures: MARCH 2020Document19 pagesCoronavirus (Covid 19) Prevention Measures: MARCH 2020neha.banNo ratings yet

- TAM Questionnaire On SMS LearningDocument10 pagesTAM Questionnaire On SMS LearningNoor JasslinaNo ratings yet

- Text4baby: Development and Implementation of A National Text Messaging Health Information ServiceDocument7 pagesText4baby: Development and Implementation of A National Text Messaging Health Information ServiceSteveEpsteinNo ratings yet

- Vinit Kumar Gunjan, Vicente Garcia Diaz, Manuel Cardona, Vijender Kumar Solanki, K. V. N. Sunitha - ICICCT 2019 – System Reliability, Quality Control, Safety, Maintenance and Management_ Applications .pdfDocument894 pagesVinit Kumar Gunjan, Vicente Garcia Diaz, Manuel Cardona, Vijender Kumar Solanki, K. V. N. Sunitha - ICICCT 2019 – System Reliability, Quality Control, Safety, Maintenance and Management_ Applications .pdfepieNo ratings yet

- CCNA Exploration Chapter 1Document30 pagesCCNA Exploration Chapter 1xapadoNo ratings yet

- حل كتاب التمارين الإنجليزي Mega Goal 2.1 ثاني ثانوي مسارات ف1 1444Document50 pagesحل كتاب التمارين الإنجليزي Mega Goal 2.1 ثاني ثانوي مسارات ف1 1444Mjnhhb YviugNo ratings yet

- Sandy City Fluoride Overfeed Final ReportDocument103 pagesSandy City Fluoride Overfeed Final ReportAnonymous WCaY6rNo ratings yet

Download as pptx, pdf, or txt

You might also like

- The Players Guide To Text Game Ebook PDFDocument69 pagesThe Players Guide To Text Game Ebook PDFMatt Smith100% (3)

- The Ultimate Guide To Texting GirlsDocument41 pagesThe Ultimate Guide To Texting Girlspocketmint79% (14)

- Unit 2 Standard Test ADocument2 pagesUnit 2 Standard Test Assaruskax50% (2)

- CH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisDocument84 pagesCH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisankonmahmudNo ratings yet

- 3.1.1.2 Lab - My Protocol RulesDocument2 pages3.1.1.2 Lab - My Protocol Rulessupiyandir100% (1)

- Sms Sending Job DetailsDocument2 pagesSms Sending Job DetailsLofojayNo ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost Concepts027 - Dyan Febita SariNo ratings yet

- Chap 002Document18 pagesChap 002Hafsa JawedNo ratings yet

- Chap002 - Manag AccDocument28 pagesChap002 - Manag AccSandra RohandiNo ratings yet

- Chap002 - Manag Acc & Cost ConceptDocument29 pagesChap002 - Manag Acc & Cost Conceptlilis astriyani sinagaNo ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsTouhid TomalNo ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost Conceptsginish12No ratings yet

- Design CostDocument21 pagesDesign CostDr. Ashish AggarwalNo ratings yet

- Cost ConceptsDocument18 pagesCost Conceptsmuttakin106No ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsrisaNo ratings yet

- Managerial Accounting Chapter 2Document61 pagesManagerial Accounting Chapter 2Wajeeh RehmanNo ratings yet

- Managerial Accounting Chap 2Document72 pagesManagerial Accounting Chap 2Sankary CarollNo ratings yet

- Managerial Accounting and Cost ConceptsDocument44 pagesManagerial Accounting and Cost ConceptsQUANG NGUYỄN VINHNo ratings yet

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost ConceptsBobbles D LittlelionNo ratings yet

- Basicconceptsofcostaccounting 141207032058 Conversion Gate02Document53 pagesBasicconceptsofcostaccounting 141207032058 Conversion Gate02sajjadNo ratings yet

- Basic Concepts of Cost AccountingDocument51 pagesBasic Concepts of Cost AccountingMary ANo ratings yet

- Managerial Accounting and Cost ConceptsDocument57 pagesManagerial Accounting and Cost ConceptsFrances Monique AlburoNo ratings yet

- Cost Terms, Concepts, and ClassificationsDocument22 pagesCost Terms, Concepts, and ClassificationsKi xxiNo ratings yet

- Basic Concepts of Cost AccountingDocument53 pagesBasic Concepts of Cost AccountinghasnainNo ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsadamNo ratings yet

- Managerial Accounting and Cost ConceptsDocument19 pagesManagerial Accounting and Cost ConceptsFarhan RabbehNo ratings yet

- Basic Concepts of Cost AccountingDocument51 pagesBasic Concepts of Cost AccountingImran KhanNo ratings yet

- Cost Term, Concept and ClassificationsDocument28 pagesCost Term, Concept and ClassificationskumarNo ratings yet

- Garrison Lecture Chapter 2Document61 pagesGarrison Lecture Chapter 2Ahmad Tawfiq Darabseh100% (2)

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost Conceptshaccp bkipmNo ratings yet

- Chapter 2 Managerial Accounting and Cost ConceptsDocument49 pagesChapter 2 Managerial Accounting and Cost ConceptsFarihaNo ratings yet

- SPPTChap 002Document19 pagesSPPTChap 002Ibrahim Elmorsy Maintenance - 3397No ratings yet

- Chapter - 2 - Managerial Accounting and Cost ConceptDocument61 pagesChapter - 2 - Managerial Accounting and Cost ConceptSoka PokaNo ratings yet

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost ConceptsAmer Wagdy GergesNo ratings yet

- SPPTChap 002Document16 pagesSPPTChap 002saharinshakib7505No ratings yet

- Dwnload Full Managerial Accounting 2nd Edition Garrison Solutions Manual PDFDocument35 pagesDwnload Full Managerial Accounting 2nd Edition Garrison Solutions Manual PDFwoollyprytheeuctw100% (11)

- Managerial Accounting 2nd Edition Garrison Solutions ManualDocument35 pagesManagerial Accounting 2nd Edition Garrison Solutions Manualiramitchellwnumr100% (28)

- Managerial Accounting 15th Edition Garrison Solutions ManualDocument35 pagesManagerial Accounting 15th Edition Garrison Solutions Manualreneestanleyf375h100% (27)

- Managerial Accounting 2nd Edition Garrison Solutions ManualDocument25 pagesManagerial Accounting 2nd Edition Garrison Solutions ManualMaryBalljswt100% (54)

- Introduction To Cost ManagementDocument31 pagesIntroduction To Cost ManagementVINCENT GAYRAMONNo ratings yet

- 1b - Cost Concepts and Terminology - 14sept06Document31 pages1b - Cost Concepts and Terminology - 14sept06Zaid AnsariNo ratings yet

- Managerial Accounting and Cost ConceptsDocument48 pagesManagerial Accounting and Cost ConceptsKirei MinaNo ratings yet

- Managerial Accounting 15th Edition Garrison Solutions ManualDocument25 pagesManagerial Accounting 15th Edition Garrison Solutions ManualKatherineJohnsonDVMinwp100% (60)

- Slide Chapter 2Document65 pagesSlide Chapter 2daoviethung29No ratings yet

- Managerial Accounting For Managers 3rd Edition Noreen Solutions ManualDocument35 pagesManagerial Accounting For Managers 3rd Edition Noreen Solutions Manualrenewerelamping1psm100% (29)

- Act 202 Chapter 2Document52 pagesAct 202 Chapter 2Shaon KhanNo ratings yet

- 02-Cost-Terms-Concepts-and-Behavior - Managerial AccountingDocument58 pages02-Cost-Terms-Concepts-and-Behavior - Managerial Accountingsabrina jane falconNo ratings yet

- An Introduction To Cost Terms and PurposesDocument33 pagesAn Introduction To Cost Terms and PurposesAi LatifahNo ratings yet

- Acct Cost ConceptsDocument52 pagesAcct Cost ConceptsLauNo ratings yet

- 4 Chapter20Document40 pages4 Chapter20154 ahmed ehabNo ratings yet

- Cost ConceptsDocument56 pagesCost ConceptsAngela De chavezNo ratings yet

- CH 5Document21 pagesCH 5hohrmpm2No ratings yet

- Managerial Accounting and Cost Concepts: Chapter TwoDocument63 pagesManagerial Accounting and Cost Concepts: Chapter TwoMd Hasibul Karim 1811766630No ratings yet

- 02 MAS - Cost ConceptDocument10 pages02 MAS - Cost ConceptKarlo D. ReclaNo ratings yet

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost ConceptsFederico SalernoNo ratings yet

- COST ESTIMATION A Class Lecture by Rashid Hussain 1657763473Document55 pagesCOST ESTIMATION A Class Lecture by Rashid Hussain 1657763473HiteshSandhalNo ratings yet

- Chapter 2Document10 pagesChapter 2Aklil TeganewNo ratings yet

- Cost Concept and ClassificationDocument45 pagesCost Concept and ClassificationMountaha0% (1)

- Managerial Accounting and Cost Concepts: Learning Objective 1Document15 pagesManagerial Accounting and Cost Concepts: Learning Objective 1Sinh TrầnNo ratings yet

- 2 - Cost Concepts and BehaviorsDocument4 pages2 - Cost Concepts and BehaviorsKaryl FailmaNo ratings yet

- MS03 - Cost Behavior and Cost Classification PDFDocument12 pagesMS03 - Cost Behavior and Cost Classification PDFTina PascualNo ratings yet

- Chapter 2 UpdatedDocument58 pagesChapter 2 Updatedbing bongNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Mobile Learning For TeachersDocument22 pagesMobile Learning For TeachersNeuber Silva FerreiraNo ratings yet

- Ishii Et Al-2019-Human Behavior and Emerging TechnologiesDocument8 pagesIshii Et Al-2019-Human Behavior and Emerging TechnologiesYuni Novianti Marin MarpaungNo ratings yet

- Mobile Phone and YouthDocument37 pagesMobile Phone and YouthVisruth K Ananad33% (3)

- Exercise READING SKILLSDocument3 pagesExercise READING SKILLSRirin DamayantiNo ratings yet

- Internet Slang and SMS (Texting) LanguageDocument7 pagesInternet Slang and SMS (Texting) LanguageHarley LausNo ratings yet

- Chapter 5 BehaviorDocument65 pagesChapter 5 BehaviorDavid ArtunduagaNo ratings yet

- Epr-T ANGLAIS - Copie-1 - CopieDocument22 pagesEpr-T ANGLAIS - Copie-1 - CopiePatrick NdayisabaNo ratings yet

- Case 3 AT&TDocument3 pagesCase 3 AT&TmaxNo ratings yet

- G7 English Lesson Exemplar 1st Quarter PDFDocument80 pagesG7 English Lesson Exemplar 1st Quarter PDFMark C. Gutierrez90% (30)

- Modul Bahasa Inggris 2 - Unit 6 - Rev 2019Document16 pagesModul Bahasa Inggris 2 - Unit 6 - Rev 2019Dhana ChompNo ratings yet

- The Relationship Between Smartphone Use & Academic Performance PDFDocument13 pagesThe Relationship Between Smartphone Use & Academic Performance PDFjeckNo ratings yet

- Michelle Carter Appellant Carter Reply BriefDocument12 pagesMichelle Carter Appellant Carter Reply BriefSyndicated NewsNo ratings yet

- Virgin Phone GuideDocument17 pagesVirgin Phone GuideMichael RuaneNo ratings yet

- The ProblemDocument40 pagesThe ProblemAllen Timtiman BisqueraNo ratings yet

- ProjectDocument18 pagesProjectDigvijay Singh100% (4)

- No Telkomsel Number Other Party Type DateDocument24 pagesNo Telkomsel Number Other Party Type DateHaryanto MarsakapNo ratings yet

- Discursive EssayDocument3 pagesDiscursive EssayLyubomira LyubenovaNo ratings yet

- Coronavirus (Covid 19) Prevention Measures: MARCH 2020Document19 pagesCoronavirus (Covid 19) Prevention Measures: MARCH 2020neha.banNo ratings yet

- TAM Questionnaire On SMS LearningDocument10 pagesTAM Questionnaire On SMS LearningNoor JasslinaNo ratings yet

- Text4baby: Development and Implementation of A National Text Messaging Health Information ServiceDocument7 pagesText4baby: Development and Implementation of A National Text Messaging Health Information ServiceSteveEpsteinNo ratings yet

- Vinit Kumar Gunjan, Vicente Garcia Diaz, Manuel Cardona, Vijender Kumar Solanki, K. V. N. Sunitha - ICICCT 2019 – System Reliability, Quality Control, Safety, Maintenance and Management_ Applications .pdfDocument894 pagesVinit Kumar Gunjan, Vicente Garcia Diaz, Manuel Cardona, Vijender Kumar Solanki, K. V. N. Sunitha - ICICCT 2019 – System Reliability, Quality Control, Safety, Maintenance and Management_ Applications .pdfepieNo ratings yet

- CCNA Exploration Chapter 1Document30 pagesCCNA Exploration Chapter 1xapadoNo ratings yet

- حل كتاب التمارين الإنجليزي Mega Goal 2.1 ثاني ثانوي مسارات ف1 1444Document50 pagesحل كتاب التمارين الإنجليزي Mega Goal 2.1 ثاني ثانوي مسارات ف1 1444Mjnhhb YviugNo ratings yet

- Sandy City Fluoride Overfeed Final ReportDocument103 pagesSandy City Fluoride Overfeed Final ReportAnonymous WCaY6rNo ratings yet