Download as pptx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- NCP Acute PainDocument3 pagesNCP Acute PainAlex MarieNo ratings yet

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument55 pagesAuditing and Assurance Services: Seventeenth Edition, Global EditionCharlotte Chan100% (1)

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument46 pagesAuditing and Assurance Services: Seventeenth Edition, Global EditionCharlotte ChanNo ratings yet

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument29 pagesAuditing and Assurance Services: Seventeenth Edition, Global EditionCharlotte ChanNo ratings yet

- Subsequent Cash Receipt Test: Close Family Close Family MemberDocument3 pagesSubsequent Cash Receipt Test: Close Family Close Family MemberCharlotte ChanNo ratings yet

- Week 2 Diagonal Diversification Strategies For Financial FirmsDocument26 pagesWeek 2 Diagonal Diversification Strategies For Financial FirmsCharlotte ChanNo ratings yet

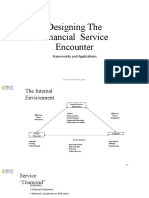

- Week 3 Designing The Financial Service EncounterDocument19 pagesWeek 3 Designing The Financial Service EncounterCharlotte ChanNo ratings yet

- Week 6 Benchmarking and Comparing Performance of Financial FirmsDocument16 pagesWeek 6 Benchmarking and Comparing Performance of Financial FirmsCharlotte ChanNo ratings yet

- Lec 9Document19 pagesLec 9Aqsa gulNo ratings yet

- JaneEyre ExtendedEssayOutlineDocument3 pagesJaneEyre ExtendedEssayOutlineAnonymous w3Gji93No ratings yet

- Stonhard Color Sheet Stonclad Fnlrev-1Document1 pageStonhard Color Sheet Stonclad Fnlrev-1Anonymous aii1ilNo ratings yet

- Science: Quarter 1 - Module 1: Scientific Ways of Acquiring Knowledge and Solving ProblemsDocument22 pagesScience: Quarter 1 - Module 1: Scientific Ways of Acquiring Knowledge and Solving Problemsnoahzaec100% (2)

- Ode and NameDocument670 pagesOde and Namenavneetkpatil8409No ratings yet

- BasterLord - Network Manual v2.0Document24 pagesBasterLord - Network Manual v2.0xuxujiashuoNo ratings yet

- Sexual Orientation Sexuality Wiki Fandom PDFDocument1 pageSexual Orientation Sexuality Wiki Fandom PDFAngus FieldingNo ratings yet

- Design and Construction of Diaphragm Walls Embedded in Rock For A Metro ProjectDocument27 pagesDesign and Construction of Diaphragm Walls Embedded in Rock For A Metro ProjectCEG BangladeshNo ratings yet

- 2010 Drama For Life Festival - ProgrammeDocument13 pages2010 Drama For Life Festival - ProgrammeSA BooksNo ratings yet

- Effects of Covid-19 To Students in The Medical FieldDocument2 pagesEffects of Covid-19 To Students in The Medical FieldAnne RonquilloNo ratings yet

- AsiDocument30 pagesAsikholifahnwNo ratings yet

- United States v. Gerard Valmore Brown, A/K/A Blackie, A/K/A Gerald Kennedy, United States of America v. Melvin Sanders, A/K/A Pops, United States of America v. Andre Simpson, 76 F.3d 376, 4th Cir. (1996)Document5 pagesUnited States v. Gerard Valmore Brown, A/K/A Blackie, A/K/A Gerald Kennedy, United States of America v. Melvin Sanders, A/K/A Pops, United States of America v. Andre Simpson, 76 F.3d 376, 4th Cir. (1996)Scribd Government DocsNo ratings yet

- Porn Addiction - The Non Sexual Reasons - Pornography AddictionDocument1 pagePorn Addiction - The Non Sexual Reasons - Pornography Addictiona_berger6684No ratings yet

- A Corpus-Based Contrastive Study of Adverb + Verb Collocations in Chinese Learner English and Native Speaker EnglishDocument28 pagesA Corpus-Based Contrastive Study of Adverb + Verb Collocations in Chinese Learner English and Native Speaker EnglishMehwish AwanNo ratings yet

- Foreign Technology DivisionDocument467 pagesForeign Technology DivisionArashNo ratings yet

- Jay Abraham - The 10 Biggest Marketing Mistakes Everyone Is Making and How To Avoid ThemDocument12 pagesJay Abraham - The 10 Biggest Marketing Mistakes Everyone Is Making and How To Avoid Themisrael_zamora6389100% (1)

- Maybee, Julie E. - Hegel, Georg W. - Picturing Hegel - An Illustrated Guide To Hegel's Encyclopaedia Logic-Lexington Books (2009) PDFDocument668 pagesMaybee, Julie E. - Hegel, Georg W. - Picturing Hegel - An Illustrated Guide To Hegel's Encyclopaedia Logic-Lexington Books (2009) PDFArroyo de FuegoNo ratings yet

- Time Cost Trade OffDocument22 pagesTime Cost Trade Offtulsi pokhrelNo ratings yet

- 42 Items Q and ADocument2 pages42 Items Q and AJoy NavalesNo ratings yet

- Orthodontic Treatment in The Management of Cleft Lip and PalateDocument13 pagesOrthodontic Treatment in The Management of Cleft Lip and PalatecareNo ratings yet

- University of Engineering & Technology Lahore: Hassan RazaDocument1 pageUniversity of Engineering & Technology Lahore: Hassan RazaShumaila AshrafNo ratings yet

- Jepretan Layar 2023-08-16 Pada 3.51.45 PMDocument47 pagesJepretan Layar 2023-08-16 Pada 3.51.45 PMFenni PrisiliaNo ratings yet

- 01 The QuizDocument7 pages01 The QuizJabriellaSanMiguel100% (1)

- Emad 21522379 Type A KWH PDFDocument8 pagesEmad 21522379 Type A KWH PDFEMAD ABDULRAHMAN ABDULLAH HASAN MASHRAH -No ratings yet

- Why Is Omkar Called As Pranav MantraDocument6 pagesWhy Is Omkar Called As Pranav Mantraami1577No ratings yet

- Efm Cip UfDocument6 pagesEfm Cip UfDaneAoneNo ratings yet

- Notes in Criminal SociologyDocument8 pagesNotes in Criminal SociologyWevinneNo ratings yet

- Weight-Volume Relationships, Plasticity, and Structure of SoilDocument30 pagesWeight-Volume Relationships, Plasticity, and Structure of SoilHanafiahHamzahNo ratings yet

- Jurisprudence Research Paper TopicsDocument5 pagesJurisprudence Research Paper TopicsAmandeep MalikNo ratings yet