Download as pptx, pdf, or txt

You might also like

- Fina5390 s2 Caselet Le Meridien Strategy Part Answers 2016Document2 pagesFina5390 s2 Caselet Le Meridien Strategy Part Answers 2016AvinashSinghNo ratings yet

- Solution BaldwinDocument9 pagesSolution BaldwinSweet AppleNo ratings yet

- Chapter 6 The Foreign Exchange MarketsDocument34 pagesChapter 6 The Foreign Exchange MarketsNyamandasimunyola100% (1)

- Econ 138: Financial and Behavioral Economics: Noise-Trader Risk in Financial Markets February 8 & 13, 2017Document35 pagesEcon 138: Financial and Behavioral Economics: Noise-Trader Risk in Financial Markets February 8 & 13, 2017econdocs0% (1)

- Securities Operations PDFDocument7 pagesSecurities Operations PDFVenu MadhavNo ratings yet

- Foreign Exchange MarketDocument41 pagesForeign Exchange MarketYousuf JamalNo ratings yet

- Exchange RateDocument32 pagesExchange RateCharlene Ann EbiteNo ratings yet

- IFM Notes 1Document90 pagesIFM Notes 1Tarini MohantyNo ratings yet

- Lecture 10-Foreign Exchange MarketDocument42 pagesLecture 10-Foreign Exchange MarketfarahNo ratings yet

- Manajemen Keuangan Internasional 9-10Document41 pagesManajemen Keuangan Internasional 9-10Putu PurwataNo ratings yet

- ER Ch05 Solution ManualDocument14 pagesER Ch05 Solution Manualsupering143No ratings yet

- Chapter 11 Walter Nicholson Microcenomic TheoryDocument15 pagesChapter 11 Walter Nicholson Microcenomic TheoryUmair QaziNo ratings yet

- Chapter 15: Foreign Exchange (FX) MarketsDocument32 pagesChapter 15: Foreign Exchange (FX) MarketsjoannamanngoNo ratings yet

- CH 09 Hull OFOD9 TH EditionDocument18 pagesCH 09 Hull OFOD9 TH Editionseanwu95No ratings yet

- Chapter 8 PDFDocument43 pagesChapter 8 PDFCarlosNo ratings yet

- Lec 7 FX Swaps Ver2Document45 pagesLec 7 FX Swaps Ver2AprilNo ratings yet

- Summary MKI Chapter 7Document5 pagesSummary MKI Chapter 7DeviNo ratings yet

- Foreign Exchange MarketDocument20 pagesForeign Exchange MarketJhianne Mae Albag100% (1)

- Quiz 1 SolutionDocument5 pagesQuiz 1 SolutionPritesh GehlotNo ratings yet

- Thinking Like An EconomistDocument40 pagesThinking Like An EconomistMarcella Alifia Kuswana Putri100% (1)

- Chapter 3Document22 pagesChapter 3Feriel El IlmiNo ratings yet

- Dealing Room, ERM, FX Risk, DerivativesDocument37 pagesDealing Room, ERM, FX Risk, DerivativesSanchit AroraNo ratings yet

- Imt Interest SwapDocument44 pagesImt Interest SwapRisris RismayaniNo ratings yet

- Ch08 ShowDocument47 pagesCh08 ShowAri ApriantoNo ratings yet

- Interest Rate DeteminationnDocument13 pagesInterest Rate DeteminationnkafiNo ratings yet

- Ifm Forex MarketDocument42 pagesIfm Forex MarketAruna BetageriNo ratings yet

- CHAPTER 2 Chapter 1 - Exchange Rate DeterminationDocument48 pagesCHAPTER 2 Chapter 1 - Exchange Rate Determinationupf123100% (2)

- CH 01 Hull OFOD10 TH EditionDocument62 pagesCH 01 Hull OFOD10 TH EditionPedestal ConciergeNo ratings yet

- FuturesDocument102 pagesFuturesSon LamNo ratings yet

- 1 PDFDocument36 pages1 PDFKevin CheNo ratings yet

- Chap 6 ProblemsDocument5 pagesChap 6 ProblemsCecilia Ooi Shu QingNo ratings yet

- Forex PPTDocument35 pagesForex PPTRohan TrivediNo ratings yet

- ECON3007 Tutorial 2 2017Document3 pagesECON3007 Tutorial 2 2017Sta KerNo ratings yet

- Forward and Futures PricingDocument13 pagesForward and Futures PricingMandar Priya PhatakNo ratings yet

- Week 2 Tutorial QuestionsDocument4 pagesWeek 2 Tutorial QuestionsWOP INVESTNo ratings yet

- Exchange Rate Regimes of The WorldDocument14 pagesExchange Rate Regimes of The WorldPaavni SharmaNo ratings yet

- 2839 Financial Globalization Chapter May30Document45 pages2839 Financial Globalization Chapter May30indiaholicNo ratings yet

- BOP TheoriesDocument33 pagesBOP TheoriesArmin AmraNo ratings yet

- Lecture Interest Rate ParityDocument10 pagesLecture Interest Rate ParityomeedjanNo ratings yet

- L2 R11 CERD Q-Bank Set 2 With AnswerDocument16 pagesL2 R11 CERD Q-Bank Set 2 With AnswerAhsan RasheedNo ratings yet

- Chapter 14 Exchange Rates and The Foreign Exchange Market An Asset ApproachDocument61 pagesChapter 14 Exchange Rates and The Foreign Exchange Market An Asset ApproachBill BennttNo ratings yet

- Iso Currency CodingDocument19 pagesIso Currency CodingSalamat AliNo ratings yet

- Macroeconomic Factors Affecting USD INRDocument16 pagesMacroeconomic Factors Affecting USD INRtamanna210% (1)

- 3rd LectureDocument4 pages3rd LectureHarpal Singh HansNo ratings yet

- Ch01HullOFOD9thEdition - EditedDocument36 pagesCh01HullOFOD9thEdition - EditedHarshvardhan MohataNo ratings yet

- Interest Rate FuturesDocument22 pagesInterest Rate FuturesHerojianbuNo ratings yet

- Lecture04 Derivatives StudentDocument22 pagesLecture04 Derivatives StudentMit DaveNo ratings yet

- Treasury Overview Sesssion 1Document30 pagesTreasury Overview Sesssion 1ravitmadanNo ratings yet

- Theories of Exchange RateDocument11 pagesTheories of Exchange RateNiharika Satyadev Jaiswal100% (1)

- Parity Conditions in International Finance and Currency ForecastingDocument31 pagesParity Conditions in International Finance and Currency ForecastingMahima AgrawalNo ratings yet

- L2 Exchange Rate DeterminationDocument25 pagesL2 Exchange Rate DeterminationKent ChinNo ratings yet

- Regulations of FOREXDocument72 pagesRegulations of FOREXApoorv SharmaNo ratings yet

- DerivativesDocument21 pagesDerivativesMandar Priya PhatakNo ratings yet

- FX Options 0907 Poster 1Document1 pageFX Options 0907 Poster 1ajayvmehtaNo ratings yet

- Swaps by DR B Brahmaiah: Presentation OnDocument60 pagesSwaps by DR B Brahmaiah: Presentation Onbatx708100% (4)

- Lecture03 Parity StudentDocument23 pagesLecture03 Parity StudentMit DaveNo ratings yet

- International Monetary FundDocument19 pagesInternational Monetary FundSunni ZaraNo ratings yet

- mgnt-4670-ch-10-foreign-exchange-fall-2007-1194589053952028-3-đã chuyển đổiDocument68 pagesmgnt-4670-ch-10-foreign-exchange-fall-2007-1194589053952028-3-đã chuyển đổiDương Thị Kiều TrangNo ratings yet

- (TCQT) Slide - Group 1Document53 pages(TCQT) Slide - Group 1hoangminh01122019No ratings yet

- Saman RomanDocument9 pagesSaman Romanggi2022.1928No ratings yet

- Saman RomanDocument8 pagesSaman Romanggi2022.1928No ratings yet

- International Trade Policy 08Document34 pagesInternational Trade Policy 08Arshad AbbasNo ratings yet

- Aggregate Planning: Translating Demand Forecasts Production Capacity LevelsDocument27 pagesAggregate Planning: Translating Demand Forecasts Production Capacity LevelsArshad AbbasNo ratings yet

- Productivity Concepts..: A Little Different Way of Looking at ProductivityDocument8 pagesProductivity Concepts..: A Little Different Way of Looking at ProductivityArshad AbbasNo ratings yet

- Inventory Planning and ControlDocument14 pagesInventory Planning and ControlArshad AbbasNo ratings yet

- Maintenance ManagementDocument23 pagesMaintenance ManagementArshad AbbasNo ratings yet

- Noun ModifierDocument129 pagesNoun ModifierArshad AbbasNo ratings yet

- Noun ModifierDocument129 pagesNoun ModifierArshad AbbasNo ratings yet

- Dell DnaDocument5 pagesDell DnaArshad AbbasNo ratings yet

- Sem III Schedule (July 2010-12)Document66 pagesSem III Schedule (July 2010-12)Arshad AbbasNo ratings yet

- Reliace FreshDocument103 pagesReliace FreshrebelddevilNo ratings yet

- Economies of Scale and Economies of Scope: by Group 1Document8 pagesEconomies of Scale and Economies of Scope: by Group 1Arshad AbbasNo ratings yet

- Er SH IpDocument16 pagesEr SH IpArshad AbbasNo ratings yet

- The Bottom Line July 2023Document25 pagesThe Bottom Line July 2023Vinayak ChaturvediNo ratings yet

- BAGNETified 08102015 Final For EMAILDocument19 pagesBAGNETified 08102015 Final For EMAILBong LazaroNo ratings yet

- Valix TOADocument51 pagesValix TOARose Aubrey A CordovaNo ratings yet

- Dokumen - Tips - MCQ Working Capital Management Cpar 1 84Document18 pagesDokumen - Tips - MCQ Working Capital Management Cpar 1 84Sabahat JavedNo ratings yet

- Special Topics in Financial ManagementDocument36 pagesSpecial Topics in Financial ManagementChristel Mae Boseo100% (1)

- Exam QuestionsDocument9 pagesExam Questionssivasamy Sundara MorthiNo ratings yet

- 10e CH 20Document22 pages10e CH 20Maria SyNo ratings yet

- Centronics Corporation v. Genicom CorporationDocument1 pageCentronics Corporation v. Genicom CorporationcrlstinaaaNo ratings yet

- Accounting12 3ed Ch01Document14 pagesAccounting12 3ed Ch01rs8j4c4b5pNo ratings yet

- Up To 74+ KYC, 120+ KYT Data PointsDocument40 pagesUp To 74+ KYC, 120+ KYT Data PointsDanielNo ratings yet

- Study Plan For JaiibDocument21 pagesStudy Plan For JaiibMahirNo ratings yet

- Questionnaire of SBIDocument5 pagesQuestionnaire of SBIthegame110165% (17)

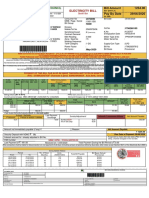

- New Delhi Municipal Council: Electricity BillDocument1 pageNew Delhi Municipal Council: Electricity BillMayank Subhash Balodi0% (1)

- Topic 7 Fixed IncomeDocument13 pagesTopic 7 Fixed Incomepepemanila101No ratings yet

- Indus Motor Ratio AnalysisDocument4 pagesIndus Motor Ratio AnalysisNabil QaziNo ratings yet

- A Study On Impact of Phone Pe Payment With Special Reference To YouthDocument110 pagesA Study On Impact of Phone Pe Payment With Special Reference To YouthAJAY RATHORENo ratings yet

- Input TaxDocument10 pagesInput TaxJan ernie MorillaNo ratings yet

- Account Statement From 1 Jan 2018 To 31 Jan 2018: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Jan 2018 To 31 Jan 2018: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceATULNo ratings yet

- Gen Math Nat ReviewerDocument4 pagesGen Math Nat ReviewerLee GorgonioNo ratings yet

- Module 5 - Cost of CapitalDocument5 pagesModule 5 - Cost of Capitaljay-ar dimaculanganNo ratings yet

- Debt MarketDocument15 pagesDebt MarketChetal BholeNo ratings yet

- HW4 - Ch.4 Completing The Accounting CycleDocument9 pagesHW4 - Ch.4 Completing The Accounting Cyclevico lorenzoNo ratings yet

- Checklist of Documentary Requirements For Additional CategoryDocument1 pageChecklist of Documentary Requirements For Additional CategoryLorilyn JaysonNo ratings yet

- Apple Card Statement - April 2023Document4 pagesApple Card Statement - April 2023bugzy000No ratings yet

- CORPFIN 7040: Fixed Income Securities (M) Embedded Research ProjectDocument12 pagesCORPFIN 7040: Fixed Income Securities (M) Embedded Research Project邓媛No ratings yet

- Analysis of Cryptocurrency, People and FutureDocument7 pagesAnalysis of Cryptocurrency, People and FutureIJRASETPublicationsNo ratings yet

- MoneyCard StatementPDF 22235621Document3 pagesMoneyCard StatementPDF 22235621Ruby Jones100% (1)

- Commission StructureDocument3 pagesCommission StructureRandom ManiacNo ratings yet

- Sinking Fund MethodDocument3 pagesSinking Fund MethodJoanna DuqueNo ratings yet