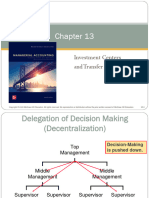

CH 13

CH 13

You might also like

- FSA Prepaid Legal ServicesDocument3 pagesFSA Prepaid Legal ServicesRyanNo ratings yet

- Introduction To Managerial Accounting 6th Edition Brewer Solutions ManualDocument63 pagesIntroduction To Managerial Accounting 6th Edition Brewer Solutions Manualgiaocleopatra192y100% (37)

- Tata Motors $ Volkswagen: A Strategic Alliance in IndiaDocument27 pagesTata Motors $ Volkswagen: A Strategic Alliance in Indiasanchit taneja100% (5)

- Solution Manual For Financial Management Theory and Practice Brigham Ehrhardt 13th EditionDocument27 pagesSolution Manual For Financial Management Theory and Practice Brigham Ehrhardt 13th EditionKennethOrrmsqi100% (44)

- Libby 10e Chap013Document53 pagesLibby 10e Chap013rakan.cocoNo ratings yet

- Introduction To Managerial Accounting 7th Edition Brewer Solutions ManualDocument63 pagesIntroduction To Managerial Accounting 7th Edition Brewer Solutions Manualgiaocleopatra192y100% (31)

- FIN 340 Final ProjectDocument12 pagesFIN 340 Final ProjectBrandon100% (1)

- PHEI Yield Curve: Daily Fair Price & Yield Indonesia Government Securities September 28, 2021Document3 pagesPHEI Yield Curve: Daily Fair Price & Yield Indonesia Government Securities September 28, 2021Oki TriangganaNo ratings yet

- Hilton Chapter 13 SolutionsDocument71 pagesHilton Chapter 13 SolutionsSharkManLazersNo ratings yet

- Day5 - Margin vs. MarkupDocument14 pagesDay5 - Margin vs. MarkupFfrekgtreh FygkohkNo ratings yet

- Methods of Sales Forecasting HILTON PHARMACEUTICALSDocument21 pagesMethods of Sales Forecasting HILTON PHARMACEUTICALSFaizmeen N. Shehzad0% (1)

- Case 3 LilypadDocument19 pagesCase 3 LilypaddeiyeaneNo ratings yet

- Investment Centers and Transfer PricingDocument42 pagesInvestment Centers and Transfer PricingSayadi AdiihNo ratings yet

- Investment Centers and Transfer PricingDocument53 pagesInvestment Centers and Transfer PricingArlene DacpanoNo ratings yet

- Investment Centers and Transfer PricingDocument23 pagesInvestment Centers and Transfer PricingWailNo ratings yet

- MINGGU 11 B INVESTEMENT CENTER - BAHAN AM RONALDDocument22 pagesMINGGU 11 B INVESTEMENT CENTER - BAHAN AM RONALDamoyyNo ratings yet

- Thirteen: Investment Centers and Transfer PricingDocument63 pagesThirteen: Investment Centers and Transfer PricingDenNo ratings yet

- EVA Investment Center Hilton Chapter 13Document62 pagesEVA Investment Center Hilton Chapter 13Riedy RiandaniNo ratings yet

- Investment Centers and Transfer PricingDocument61 pagesInvestment Centers and Transfer PricingIman NessaNo ratings yet

- Chap 009Document41 pagesChap 009jeraldtomas12No ratings yet

- Ch11accessible 200101213935 PDFDocument61 pagesCh11accessible 200101213935 PDFسامر الخطيبNo ratings yet

- Chap013 TNx2Document69 pagesChap013 TNx2Ashesh DasNo ratings yet

- Hilton MA 12e Chap013Document43 pagesHilton MA 12e Chap013cmxzerostartNo ratings yet

- Performance Measurement in Decentralized OrganizationsDocument56 pagesPerformance Measurement in Decentralized OrganizationsEman AhmedNo ratings yet

- Garrison Lecture Chapter 11Document57 pagesGarrison Lecture Chapter 11sofikhdyNo ratings yet

- Measuring and Controlling Assets EmployedDocument30 pagesMeasuring and Controlling Assets EmployedRhaymond MonterdeNo ratings yet

- 4e NBG CH12 SMDocument72 pages4e NBG CH12 SM胡振猷No ratings yet

- Chapter 11 PDFDocument65 pagesChapter 11 PDFAftarur Rahaman AnikNo ratings yet

- CH09Document62 pagesCH09Lê Chấn PhongNo ratings yet

- Unit - 6 محاسبه اداريهDocument47 pagesUnit - 6 محاسبه اداريهsuperstreem.9No ratings yet

- Investment Centers and Transfer Pricing: Answers To Review QuestionsDocument45 pagesInvestment Centers and Transfer Pricing: Answers To Review QuestionsShey INFTNo ratings yet

- Week 10 ImaDocument49 pagesWeek 10 ImaWai Ying LaiNo ratings yet

- Cap 8 Performance CH09 SM 1Document61 pagesCap 8 Performance CH09 SM 1Lê Chấn PhongNo ratings yet

- Investment Centers and Transfer Pricing: Answers To Review QuestionsDocument43 pagesInvestment Centers and Transfer Pricing: Answers To Review QuestionsYong RenNo ratings yet

- Chapter 11Document61 pagesChapter 11Samaaraa NorNo ratings yet

- Division Performance MeasurementDocument31 pagesDivision Performance MeasurementKetan DedhaNo ratings yet

- Roi, RiDocument17 pagesRoi, RiGalan PagehgiriNo ratings yet

- Performance Evaluation in The Decentralized FirmDocument38 pagesPerformance Evaluation in The Decentralized FirmMuhammad Rusydi AzizNo ratings yet

- Performance Evaluation in The Decentralized FirmDocument38 pagesPerformance Evaluation in The Decentralized FirmNana LeeNo ratings yet

- CH 10Document37 pagesCH 10billybuttonNo ratings yet

- Chap 013Document49 pagesChap 013palak32100% (1)

- ROI Pak DhaniDocument26 pagesROI Pak DhaniCahya PerdanaNo ratings yet

- Divisional Performance Measures and Transfer Pricing NotesDocument83 pagesDivisional Performance Measures and Transfer Pricing NotesShreya PatelNo ratings yet

- Ch10 - Guan CM - AISEDocument40 pagesCh10 - Guan CM - AISEzputrinabila4No ratings yet

- Accounting & Control: Cost ManagementDocument40 pagesAccounting & Control: Cost ManagementMeriskaNo ratings yet

- Accounting & Control: Cost ManagementDocument40 pagesAccounting & Control: Cost ManagementBusiness MatterNo ratings yet

- Solution Manual For Financial Management Theory and Practice 14th Edition by BrighamDocument28 pagesSolution Manual For Financial Management Theory and Practice 14th Edition by BrighamKennethOrrmsqi100% (49)

- Accounts PresentationDocument16 pagesAccounts PresentationsansarwalNo ratings yet

- CMA CH 5 - Responsibility Centers and Performance Measurement March 2019-1Document39 pagesCMA CH 5 - Responsibility Centers and Performance Measurement March 2019-1Henok FikaduNo ratings yet

- Pusat Prtanggung Jawaban Dan Transfer PricingDocument40 pagesPusat Prtanggung Jawaban Dan Transfer PricingmayaNo ratings yet

- Cuacm413 Presentation Group 9..Qns 21Document13 pagesCuacm413 Presentation Group 9..Qns 21Jeremiah NcubeNo ratings yet

- Decentralization: Mcgraw-Hill /irwinDocument53 pagesDecentralization: Mcgraw-Hill /irwinYHNo ratings yet

- 4 - Topic4DividendPolicy-editedDocument35 pages4 - Topic4DividendPolicy-editedCOCONUTNo ratings yet

- MergedDocument634 pagesMergedRishabh DabasNo ratings yet

- Noreen5e Ch11Document48 pagesNoreen5e Ch11algokar999No ratings yet

- A Guide To Calculating Return On Investment (ROI) - InvestopediaDocument9 pagesA Guide To Calculating Return On Investment (ROI) - InvestopediaBob KaneNo ratings yet

- Control: The Management Control EnvironmentDocument49 pagesControl: The Management Control EnvironmentvinnaNo ratings yet

- Is Your Private Company Return On Investment Adequate-How To Correctly Measure Adn Significantly Improve ROI - Long VersionDocument12 pagesIs Your Private Company Return On Investment Adequate-How To Correctly Measure Adn Significantly Improve ROI - Long Versionsakron100% (1)

- Hilton7e SM CH13Document50 pagesHilton7e SM CH13VivekRaptorNo ratings yet

- Performance Evaluation in The Decentralized FirmDocument55 pagesPerformance Evaluation in The Decentralized FirmIstiq OmahNo ratings yet

- MGRL Corner 4e SM AISE 14Document36 pagesMGRL Corner 4e SM AISE 14vem arcayanNo ratings yet

- L 6 Performance MeasurementDocument14 pagesL 6 Performance MeasurementMist FactorNo ratings yet

- Analysis of Southwest AirlinesDocument2 pagesAnalysis of Southwest AirlinesspiffykyleNo ratings yet

- CHP 3 Insurer Ownership, Financial & - Operational StructureDocument24 pagesCHP 3 Insurer Ownership, Financial & - Operational StructureIskandar Zulkarnain Kamalluddin100% (1)

- Marketing Report - Bread and Beyond Group - CDocument37 pagesMarketing Report - Bread and Beyond Group - Cziafat shehzadNo ratings yet

- CavinKare EditedDocument5 pagesCavinKare Editedshelter innNo ratings yet

- TASC Magazine January 2009Document51 pagesTASC Magazine January 2009Trend Imperator100% (1)

- Essay Topics: Corporate FinanceDocument3 pagesEssay Topics: Corporate FinanceBen SetoNo ratings yet

- The Goals and Functions of Financial ManagementDocument55 pagesThe Goals and Functions of Financial ManagementwerlamodeNo ratings yet

- Percent Word Problems WorksheetDocument3 pagesPercent Word Problems WorksheetjaiNo ratings yet

- Tutorial 6 - TRMDocument9 pagesTutorial 6 - TRMHằngg ĐỗNo ratings yet

- Capital Market ReformsDocument8 pagesCapital Market ReformsRiyas ParakkattilNo ratings yet

- Chapter 1Document28 pagesChapter 1Zaid NaveedNo ratings yet

- 3ps and 3s of BusinessDocument7 pages3ps and 3s of Businessjoel lopezNo ratings yet

- Endowments - A Critique of The ModelDocument10 pagesEndowments - A Critique of The ModelOMiNYCNo ratings yet

- Target Costing and Cost Analysis For Pricing DecisionsDocument23 pagesTarget Costing and Cost Analysis For Pricing DecisionsWailNo ratings yet

- Article 246 (SEVENTH SCHEDULE) of The Indian Constitution, Distributes Legislative PowersDocument10 pagesArticle 246 (SEVENTH SCHEDULE) of The Indian Constitution, Distributes Legislative PowersRaGa JoThi0% (1)

- CIE Notes 2509Document3 pagesCIE Notes 2509HA CskNo ratings yet

- Sample Praposal of Tetley TeaDocument7 pagesSample Praposal of Tetley TeaYusuf RafiNo ratings yet

- SuperbizDocument11 pagesSuperbizeng20072007No ratings yet

- Integrated Energy-Environment Modeling and LEAP: Charlie Heaps SEI-Boston and Tellus InstituteDocument44 pagesIntegrated Energy-Environment Modeling and LEAP: Charlie Heaps SEI-Boston and Tellus InstitutePaula BorbaNo ratings yet

- BA363 Beta Golf Case AnalysisDocument2 pagesBA363 Beta Golf Case AnalysisAdisorn SribuaNo ratings yet

- Executive SummaryDocument17 pagesExecutive SummarySiva GuruNo ratings yet

- Baltic Guide 2011-ViewingDocument41 pagesBaltic Guide 2011-ViewingPaul JärvetNo ratings yet

Download as pptx, pdf, or txt

You might also like

- FSA Prepaid Legal ServicesDocument3 pagesFSA Prepaid Legal ServicesRyanNo ratings yet

- Introduction To Managerial Accounting 6th Edition Brewer Solutions ManualDocument63 pagesIntroduction To Managerial Accounting 6th Edition Brewer Solutions Manualgiaocleopatra192y100% (37)

- Tata Motors $ Volkswagen: A Strategic Alliance in IndiaDocument27 pagesTata Motors $ Volkswagen: A Strategic Alliance in Indiasanchit taneja100% (5)

- Solution Manual For Financial Management Theory and Practice Brigham Ehrhardt 13th EditionDocument27 pagesSolution Manual For Financial Management Theory and Practice Brigham Ehrhardt 13th EditionKennethOrrmsqi100% (44)

- Libby 10e Chap013Document53 pagesLibby 10e Chap013rakan.cocoNo ratings yet

- Introduction To Managerial Accounting 7th Edition Brewer Solutions ManualDocument63 pagesIntroduction To Managerial Accounting 7th Edition Brewer Solutions Manualgiaocleopatra192y100% (31)

- FIN 340 Final ProjectDocument12 pagesFIN 340 Final ProjectBrandon100% (1)

- PHEI Yield Curve: Daily Fair Price & Yield Indonesia Government Securities September 28, 2021Document3 pagesPHEI Yield Curve: Daily Fair Price & Yield Indonesia Government Securities September 28, 2021Oki TriangganaNo ratings yet

- Hilton Chapter 13 SolutionsDocument71 pagesHilton Chapter 13 SolutionsSharkManLazersNo ratings yet

- Day5 - Margin vs. MarkupDocument14 pagesDay5 - Margin vs. MarkupFfrekgtreh FygkohkNo ratings yet

- Methods of Sales Forecasting HILTON PHARMACEUTICALSDocument21 pagesMethods of Sales Forecasting HILTON PHARMACEUTICALSFaizmeen N. Shehzad0% (1)

- Case 3 LilypadDocument19 pagesCase 3 LilypaddeiyeaneNo ratings yet

- Investment Centers and Transfer PricingDocument42 pagesInvestment Centers and Transfer PricingSayadi AdiihNo ratings yet

- Investment Centers and Transfer PricingDocument53 pagesInvestment Centers and Transfer PricingArlene DacpanoNo ratings yet

- Investment Centers and Transfer PricingDocument23 pagesInvestment Centers and Transfer PricingWailNo ratings yet

- MINGGU 11 B INVESTEMENT CENTER - BAHAN AM RONALDDocument22 pagesMINGGU 11 B INVESTEMENT CENTER - BAHAN AM RONALDamoyyNo ratings yet

- Thirteen: Investment Centers and Transfer PricingDocument63 pagesThirteen: Investment Centers and Transfer PricingDenNo ratings yet

- EVA Investment Center Hilton Chapter 13Document62 pagesEVA Investment Center Hilton Chapter 13Riedy RiandaniNo ratings yet

- Investment Centers and Transfer PricingDocument61 pagesInvestment Centers and Transfer PricingIman NessaNo ratings yet

- Chap 009Document41 pagesChap 009jeraldtomas12No ratings yet

- Ch11accessible 200101213935 PDFDocument61 pagesCh11accessible 200101213935 PDFسامر الخطيبNo ratings yet

- Chap013 TNx2Document69 pagesChap013 TNx2Ashesh DasNo ratings yet

- Hilton MA 12e Chap013Document43 pagesHilton MA 12e Chap013cmxzerostartNo ratings yet

- Performance Measurement in Decentralized OrganizationsDocument56 pagesPerformance Measurement in Decentralized OrganizationsEman AhmedNo ratings yet

- Garrison Lecture Chapter 11Document57 pagesGarrison Lecture Chapter 11sofikhdyNo ratings yet

- Measuring and Controlling Assets EmployedDocument30 pagesMeasuring and Controlling Assets EmployedRhaymond MonterdeNo ratings yet

- 4e NBG CH12 SMDocument72 pages4e NBG CH12 SM胡振猷No ratings yet

- Chapter 11 PDFDocument65 pagesChapter 11 PDFAftarur Rahaman AnikNo ratings yet

- CH09Document62 pagesCH09Lê Chấn PhongNo ratings yet

- Unit - 6 محاسبه اداريهDocument47 pagesUnit - 6 محاسبه اداريهsuperstreem.9No ratings yet

- Investment Centers and Transfer Pricing: Answers To Review QuestionsDocument45 pagesInvestment Centers and Transfer Pricing: Answers To Review QuestionsShey INFTNo ratings yet

- Week 10 ImaDocument49 pagesWeek 10 ImaWai Ying LaiNo ratings yet

- Cap 8 Performance CH09 SM 1Document61 pagesCap 8 Performance CH09 SM 1Lê Chấn PhongNo ratings yet

- Investment Centers and Transfer Pricing: Answers To Review QuestionsDocument43 pagesInvestment Centers and Transfer Pricing: Answers To Review QuestionsYong RenNo ratings yet

- Chapter 11Document61 pagesChapter 11Samaaraa NorNo ratings yet

- Division Performance MeasurementDocument31 pagesDivision Performance MeasurementKetan DedhaNo ratings yet

- Roi, RiDocument17 pagesRoi, RiGalan PagehgiriNo ratings yet

- Performance Evaluation in The Decentralized FirmDocument38 pagesPerformance Evaluation in The Decentralized FirmMuhammad Rusydi AzizNo ratings yet

- Performance Evaluation in The Decentralized FirmDocument38 pagesPerformance Evaluation in The Decentralized FirmNana LeeNo ratings yet

- CH 10Document37 pagesCH 10billybuttonNo ratings yet

- Chap 013Document49 pagesChap 013palak32100% (1)

- ROI Pak DhaniDocument26 pagesROI Pak DhaniCahya PerdanaNo ratings yet

- Divisional Performance Measures and Transfer Pricing NotesDocument83 pagesDivisional Performance Measures and Transfer Pricing NotesShreya PatelNo ratings yet

- Ch10 - Guan CM - AISEDocument40 pagesCh10 - Guan CM - AISEzputrinabila4No ratings yet

- Accounting & Control: Cost ManagementDocument40 pagesAccounting & Control: Cost ManagementMeriskaNo ratings yet

- Accounting & Control: Cost ManagementDocument40 pagesAccounting & Control: Cost ManagementBusiness MatterNo ratings yet

- Solution Manual For Financial Management Theory and Practice 14th Edition by BrighamDocument28 pagesSolution Manual For Financial Management Theory and Practice 14th Edition by BrighamKennethOrrmsqi100% (49)

- Accounts PresentationDocument16 pagesAccounts PresentationsansarwalNo ratings yet

- CMA CH 5 - Responsibility Centers and Performance Measurement March 2019-1Document39 pagesCMA CH 5 - Responsibility Centers and Performance Measurement March 2019-1Henok FikaduNo ratings yet

- Pusat Prtanggung Jawaban Dan Transfer PricingDocument40 pagesPusat Prtanggung Jawaban Dan Transfer PricingmayaNo ratings yet

- Cuacm413 Presentation Group 9..Qns 21Document13 pagesCuacm413 Presentation Group 9..Qns 21Jeremiah NcubeNo ratings yet

- Decentralization: Mcgraw-Hill /irwinDocument53 pagesDecentralization: Mcgraw-Hill /irwinYHNo ratings yet

- 4 - Topic4DividendPolicy-editedDocument35 pages4 - Topic4DividendPolicy-editedCOCONUTNo ratings yet

- MergedDocument634 pagesMergedRishabh DabasNo ratings yet

- Noreen5e Ch11Document48 pagesNoreen5e Ch11algokar999No ratings yet

- A Guide To Calculating Return On Investment (ROI) - InvestopediaDocument9 pagesA Guide To Calculating Return On Investment (ROI) - InvestopediaBob KaneNo ratings yet

- Control: The Management Control EnvironmentDocument49 pagesControl: The Management Control EnvironmentvinnaNo ratings yet

- Is Your Private Company Return On Investment Adequate-How To Correctly Measure Adn Significantly Improve ROI - Long VersionDocument12 pagesIs Your Private Company Return On Investment Adequate-How To Correctly Measure Adn Significantly Improve ROI - Long Versionsakron100% (1)

- Hilton7e SM CH13Document50 pagesHilton7e SM CH13VivekRaptorNo ratings yet

- Performance Evaluation in The Decentralized FirmDocument55 pagesPerformance Evaluation in The Decentralized FirmIstiq OmahNo ratings yet

- MGRL Corner 4e SM AISE 14Document36 pagesMGRL Corner 4e SM AISE 14vem arcayanNo ratings yet

- L 6 Performance MeasurementDocument14 pagesL 6 Performance MeasurementMist FactorNo ratings yet

- Analysis of Southwest AirlinesDocument2 pagesAnalysis of Southwest AirlinesspiffykyleNo ratings yet

- CHP 3 Insurer Ownership, Financial & - Operational StructureDocument24 pagesCHP 3 Insurer Ownership, Financial & - Operational StructureIskandar Zulkarnain Kamalluddin100% (1)

- Marketing Report - Bread and Beyond Group - CDocument37 pagesMarketing Report - Bread and Beyond Group - Cziafat shehzadNo ratings yet

- CavinKare EditedDocument5 pagesCavinKare Editedshelter innNo ratings yet

- TASC Magazine January 2009Document51 pagesTASC Magazine January 2009Trend Imperator100% (1)

- Essay Topics: Corporate FinanceDocument3 pagesEssay Topics: Corporate FinanceBen SetoNo ratings yet

- The Goals and Functions of Financial ManagementDocument55 pagesThe Goals and Functions of Financial ManagementwerlamodeNo ratings yet

- Percent Word Problems WorksheetDocument3 pagesPercent Word Problems WorksheetjaiNo ratings yet

- Tutorial 6 - TRMDocument9 pagesTutorial 6 - TRMHằngg ĐỗNo ratings yet

- Capital Market ReformsDocument8 pagesCapital Market ReformsRiyas ParakkattilNo ratings yet

- Chapter 1Document28 pagesChapter 1Zaid NaveedNo ratings yet

- 3ps and 3s of BusinessDocument7 pages3ps and 3s of Businessjoel lopezNo ratings yet

- Endowments - A Critique of The ModelDocument10 pagesEndowments - A Critique of The ModelOMiNYCNo ratings yet

- Target Costing and Cost Analysis For Pricing DecisionsDocument23 pagesTarget Costing and Cost Analysis For Pricing DecisionsWailNo ratings yet

- Article 246 (SEVENTH SCHEDULE) of The Indian Constitution, Distributes Legislative PowersDocument10 pagesArticle 246 (SEVENTH SCHEDULE) of The Indian Constitution, Distributes Legislative PowersRaGa JoThi0% (1)

- CIE Notes 2509Document3 pagesCIE Notes 2509HA CskNo ratings yet

- Sample Praposal of Tetley TeaDocument7 pagesSample Praposal of Tetley TeaYusuf RafiNo ratings yet

- SuperbizDocument11 pagesSuperbizeng20072007No ratings yet

- Integrated Energy-Environment Modeling and LEAP: Charlie Heaps SEI-Boston and Tellus InstituteDocument44 pagesIntegrated Energy-Environment Modeling and LEAP: Charlie Heaps SEI-Boston and Tellus InstitutePaula BorbaNo ratings yet

- BA363 Beta Golf Case AnalysisDocument2 pagesBA363 Beta Golf Case AnalysisAdisorn SribuaNo ratings yet

- Executive SummaryDocument17 pagesExecutive SummarySiva GuruNo ratings yet

- Baltic Guide 2011-ViewingDocument41 pagesBaltic Guide 2011-ViewingPaul JärvetNo ratings yet