Download as ppt, pdf, or txt

You might also like

- BSBFIN601 Project Portfolio 1Document21 pagesBSBFIN601 Project Portfolio 1Zumer Fatima100% (1)

- Christian Walters Explains New Trust Technology - Cantinista's Redoubt 1Document15 pagesChristian Walters Explains New Trust Technology - Cantinista's Redoubt 1johnrose52183% (6)

- Accounting Mcqs 1Document20 pagesAccounting Mcqs 1Pramod Gowda BNo ratings yet

- Economic Returns, Reversion To The Mean, and Total Shareholder Returns Anticipating Change Is Hard But ProfitableDocument15 pagesEconomic Returns, Reversion To The Mean, and Total Shareholder Returns Anticipating Change Is Hard But ProfitableAhmed MadhaNo ratings yet

- Written QuestionsDocument33 pagesWritten QuestionsLet it beNo ratings yet

- Deed of Absolute SaleDocument2 pagesDeed of Absolute Salegilberthufana446877No ratings yet

- Journal, Ledger, TB & Final AccountsDocument11 pagesJournal, Ledger, TB & Final AccountsSanjay Dutta100% (1)

- 11 Accountancy TP Ch04 01 Ladger and Trial BalanceDocument3 pages11 Accountancy TP Ch04 01 Ladger and Trial Balancerenu bhattNo ratings yet

- M2 1.+journal+ +Recording+TransactionsDocument24 pagesM2 1.+journal+ +Recording+TransactionsBhavye GuptaNo ratings yet

- Basics & Journal Entry of AccountancyDocument45 pagesBasics & Journal Entry of AccountancyPrincipal MHK, AnklleshwarNo ratings yet

- Journal, & TB & BsDocument10 pagesJournal, & TB & BsAyushi100% (1)

- Ledger and Trial BalanceDocument24 pagesLedger and Trial BalanceMd.Amir hossain khan100% (1)

- Journal: Illustration - 1 Journalise The Following Transactions in The Books of Shri .HerambhDocument10 pagesJournal: Illustration - 1 Journalise The Following Transactions in The Books of Shri .HerambhAyushi100% (1)

- Assignment - Finanacial Account 2018-Ag-4621 Naveed AhmadDocument8 pagesAssignment - Finanacial Account 2018-Ag-4621 Naveed AhmadNaveed IjazNo ratings yet

- Basic Account 1Document10 pagesBasic Account 1COMPUTER WORLDNo ratings yet

- 110-Chapter 3 - Books of Original Entry-Journal - WMDocument21 pages110-Chapter 3 - Books of Original Entry-Journal - WMaaditya kumar jhaNo ratings yet

- 1june 2009 1 J E Accounts 2Document18 pages1june 2009 1 J E Accounts 2Pravah ShuklaNo ratings yet

- Assignment JournalDocument4 pagesAssignment Journalaishasiddiq5784No ratings yet

- Journal EntryDocument7 pagesJournal Entryshreyu14796No ratings yet

- Homework 27-02-2023 (Journal)Document3 pagesHomework 27-02-2023 (Journal)Akshayaa PrakashNo ratings yet

- Journalize The FollowingDocument11 pagesJournalize The Followingvishal jaiswalNo ratings yet

- Journal Entry Answers 30 Aug 22Document2 pagesJournal Entry Answers 30 Aug 22WarrioropNo ratings yet

- 179200Document13 pages179200Ankita GuptaNo ratings yet

- Chapter - 3 Journal Entries Part 1Document7 pagesChapter - 3 Journal Entries Part 1Abdullah JuttNo ratings yet

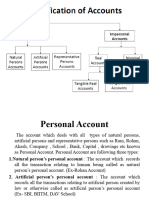

- Basic Terms in Accounts: Assets: Something That You OwnDocument46 pagesBasic Terms in Accounts: Assets: Something That You OwnLeo GladwinNo ratings yet

- FMA 4 Journal Ledger Trial Balance Incomplete Complete As HomeWork 1611996675443Document5 pagesFMA 4 Journal Ledger Trial Balance Incomplete Complete As HomeWork 1611996675443viveo23No ratings yet

- Class 11 Accountancy Chapter-3 Revision NotesDocument11 pagesClass 11 Accountancy Chapter-3 Revision NotesMohd. Khushmeen KhanNo ratings yet

- Unit 7 PDFDocument22 pagesUnit 7 PDFSatti NagendrareddyNo ratings yet

- Financial Accounting: I Term - MbaDocument39 pagesFinancial Accounting: I Term - MbaShujath SharieffNo ratings yet

- Accountancy NotesDocument23 pagesAccountancy NotesAlbana QemaliNo ratings yet

- Account... DR: Date Partucular LF Amount (DR) Amount (CR)Document4 pagesAccount... DR: Date Partucular LF Amount (DR) Amount (CR)Natasha KapoorNo ratings yet

- Project Report in Accountancy: - Submitted by - Nishan Pant - Grade - 11 - Section DDocument13 pagesProject Report in Accountancy: - Submitted by - Nishan Pant - Grade - 11 - Section Dnishan pantNo ratings yet

- Tally Repor1Document74 pagesTally Repor1Ronak JainNo ratings yet

- 1Document5 pages1Steve JacobNo ratings yet

- Assignment 2Document4 pagesAssignment 2Ritika ChoudharyNo ratings yet

- Journal, Ledger TB - Problems SolutionsDocument14 pagesJournal, Ledger TB - Problems Solutionssri lekhaNo ratings yet

- DK Goel Solutions For Class 11 Accountancy Chapter 9 Books of Original EntryDocument47 pagesDK Goel Solutions For Class 11 Accountancy Chapter 9 Books of Original Entrysushantanaskar2021No ratings yet

- TallyDocument27 pagesTallyRonak JainNo ratings yet

- Types of Accounts & DiscountDocument10 pagesTypes of Accounts & Discountsarvesh kumarNo ratings yet

- Debit and Credit Rules-1Document23 pagesDebit and Credit Rules-1Mubeen JavedNo ratings yet

- Journal AssignmentDocument1 pageJournal AssignmentRushikeshNawaleNo ratings yet

- TS Grewal Solution For Class 11 Accountancy Chapter 13 - Rectification of ErrorsDocument7 pagesTS Grewal Solution For Class 11 Accountancy Chapter 13 - Rectification of ErrorssharoonfaruNo ratings yet

- Foa ProjectDocument13 pagesFoa ProjectDrumil KacheriaNo ratings yet

- JournalDocument20 pagesJournalChandrika Prasad DashNo ratings yet

- 59journal Solved Assignment 13-14Document12 pages59journal Solved Assignment 13-14anon_350417051No ratings yet

- 59journal Solved Assignment 13-14Document12 pages59journal Solved Assignment 13-14anon_350417051No ratings yet

- Additional Illustration-9Document12 pagesAdditional Illustration-9alokpandeygenxNo ratings yet

- I. Answer Any TWO of The Following Questions. 2 X 5 10Document3 pagesI. Answer Any TWO of The Following Questions. 2 X 5 10M JEEVARATHNAM NAIDUNo ratings yet

- Question # 01Document15 pagesQuestion # 01SZANo ratings yet

- JDocument13 pagesJpalash khannaNo ratings yet

- Lesson-5 LedgerDocument16 pagesLesson-5 LedgernishaashaxxNo ratings yet

- 3c. Journal, Ledger Trial Balance - Practice File 2Document11 pages3c. Journal, Ledger Trial Balance - Practice File 2Bhai ho to dodoNo ratings yet

- FA Problems SolutionsDocument246 pagesFA Problems SolutionsK. Pavithraa SreeNo ratings yet

- T Accounts and TB by Riffat JabeenDocument4 pagesT Accounts and TB by Riffat JabeenAbie AsifNo ratings yet

- 104c Unit 1 SolutionDocument23 pages104c Unit 1 SolutionDevil 5103No ratings yet

- CCP102Document30 pagesCCP102api-3849444No ratings yet

- Accounting Equation For PracticeDocument3 pagesAccounting Equation For PracticeminalgargNo ratings yet

- MAA Assignment RKDocument9 pagesMAA Assignment RKKrishna RayasamNo ratings yet

- Chapter 13Document12 pagesChapter 13palash khanna100% (1)

- Kendriya Vidyalaya Sangthan, Mumbai Region Marking Scheme Set 1 AccountancyDocument2 pagesKendriya Vidyalaya Sangthan, Mumbai Region Marking Scheme Set 1 AccountancyNitesh KumarNo ratings yet

- DK Goel Solutions For Class 11 Accountancy Chapter 9 Books of Original EntryDocument147 pagesDK Goel Solutions For Class 11 Accountancy Chapter 9 Books of Original Entrysushantanaskar2021No ratings yet

- Afm 4Document3 pagesAfm 4helpevery7No ratings yet

- Class 11 Accounts SP 2 Answer KeyDocument18 pagesClass 11 Accounts SP 2 Answer KeyUdyamGNo ratings yet

- Chapter-2 Double Entry Book Keeping Book SystemDocument5 pagesChapter-2 Double Entry Book Keeping Book SystemgaurabNo ratings yet

- Journal VoucherDocument20 pagesJournal VouchergaurabNo ratings yet

- Basic Accounting Principles and GuidelinesDocument23 pagesBasic Accounting Principles and GuidelinesgaurabNo ratings yet

- BBS 1st Year Globalization ChapterDocument9 pagesBBS 1st Year Globalization ChaptergaurabNo ratings yet

- Chapter - 2.2 Compound InterestDocument18 pagesChapter - 2.2 Compound InterestsaudzulfiquarNo ratings yet

- Superbonga Beauty SalonDocument96 pagesSuperbonga Beauty SalonFatmah100% (1)

- Vda de Albar V. Carangdang: Petitioner Respondent: Josefa Fabie de Carandang Ponencia: Bautista Angelo, JDocument5 pagesVda de Albar V. Carangdang: Petitioner Respondent: Josefa Fabie de Carandang Ponencia: Bautista Angelo, JAleezah Gertrude RaymundoNo ratings yet

- Balance Sheet and Statement of Cash Flows: Intermediate Accounting 12th Edition Kieso, Weygandt, and WarfieldDocument46 pagesBalance Sheet and Statement of Cash Flows: Intermediate Accounting 12th Edition Kieso, Weygandt, and WarfieldGisilowati Dian PurnamaNo ratings yet

- Chapter 1 CLCDocument17 pagesChapter 1 CLCLinh BùiNo ratings yet

- Chapter5 Shariah-Compliant Stocks and ValuationDocument72 pagesChapter5 Shariah-Compliant Stocks and ValuationOctari NabilaNo ratings yet

- Branch BestDocument46 pagesBranch Bestsamuel debebeNo ratings yet

- Mitchell Li - Brookfield Renewable Energy Partners PitchDocument15 pagesMitchell Li - Brookfield Renewable Energy Partners PitchAnonymous Ht0MIJNo ratings yet

- Gis 580 Final Project by Dina YerbolatkyzyDocument10 pagesGis 580 Final Project by Dina Yerbolatkyzyapi-312016442No ratings yet

- FinMan Module 5 Time Value of MoneyDocument9 pagesFinMan Module 5 Time Value of Moneyerickson hernanNo ratings yet

- 05 Allowance 2Document49 pages05 Allowance 2PrashantNo ratings yet

- Investment QuizDocument14 pagesInvestment QuizNavi KaurNo ratings yet

- Income Tax - How Do I Know What Needs To Be Done?Document30 pagesIncome Tax - How Do I Know What Needs To Be Done?Emran AkbarNo ratings yet

- (Ebook PDF) Corporate Finance 13th Edition Bradford D. Jordan Stephen A. Ross - Ebook PDF All ChapterDocument69 pages(Ebook PDF) Corporate Finance 13th Edition Bradford D. Jordan Stephen A. Ross - Ebook PDF All Chaptermushilghrabi100% (9)

- Fnce 220: Business Finance: Lecture 6: Capital Investment DecisionsDocument39 pagesFnce 220: Business Finance: Lecture 6: Capital Investment DecisionsVincent KamemiaNo ratings yet

- Device InvoiceDocument5 pagesDevice InvoiceMohamed ZakiNo ratings yet

- Kve TDI 21.03.2024Document7 pagesKve TDI 21.03.2024anhminhocchoNo ratings yet

- (Download PDF) Between Debt and The Devil Money Credit and Fixing Global Finance Turner Online Ebook All Chapter PDFDocument40 pages(Download PDF) Between Debt and The Devil Money Credit and Fixing Global Finance Turner Online Ebook All Chapter PDFjasmine.newburn311No ratings yet

- Reference Paper Literature ReviewDocument5 pagesReference Paper Literature ReviewAani RashNo ratings yet

- UPSCPORTAL Magazine Civil Services 2009 Pre SpecialDocument113 pagesUPSCPORTAL Magazine Civil Services 2009 Pre SpecialJaya Ram M100% (1)

- Bank SynopsisDocument7 pagesBank SynopsisNiro ThakurNo ratings yet

- Https WWW - Irctc.co - in Eticketing Printticket PDFDocument2 pagesHttps WWW - Irctc.co - in Eticketing Printticket PDFAshish SinhaNo ratings yet

- Bar Exams Suggested AnswerDocument6 pagesBar Exams Suggested AnswerJoe CuraNo ratings yet

- Nepal Stock Exchange Limited: Singhadurbar Plaza, Kathmandu, Nepal. Phone: 977-1-4250758,4250735, Fax: 977-1-4262538Document15 pagesNepal Stock Exchange Limited: Singhadurbar Plaza, Kathmandu, Nepal. Phone: 977-1-4250758,4250735, Fax: 977-1-4262538Jeevan ChaudharyNo ratings yet

- Net Present Value (NPV) : Calculation Methods and FormulasDocument3 pagesNet Present Value (NPV) : Calculation Methods and FormulasjozsefczNo ratings yet