WRD - Ab - Az.ch06 - SV Accounting For Merchandising Business

WRD - Ab - Az.ch06 - SV Accounting For Merchandising Business

You might also like

- Bitcoin To $1M, Ethereum To $180,000 by 2030 ARKDocument1 pageBitcoin To $1M, Ethereum To $180,000 by 2030 ARKOwen HalpertNo ratings yet

- Libby Financial Accounting Chapter6Document6 pagesLibby Financial Accounting Chapter6Jie Bo TiNo ratings yet

- Scope of White Label ATMs Business in PakistanDocument15 pagesScope of White Label ATMs Business in PakistanSay Pakistan100% (1)

- Brand Building Blocks: First Pepsi AdDocument2 pagesBrand Building Blocks: First Pepsi AdBarson MithunNo ratings yet

- Monitoring and Controlling Accounts Receivable PDFDocument45 pagesMonitoring and Controlling Accounts Receivable PDFnigusNo ratings yet

- AIS Chapter FourDocument14 pagesAIS Chapter FourNaod MekonnenNo ratings yet

- Administering Subsidiary Accounts and Ledgers PDFDocument33 pagesAdministering Subsidiary Accounts and Ledgers PDFnigus78% (9)

- Bonds and Stocks SolutionsDocument3 pagesBonds and Stocks SolutionsLucas AbudNo ratings yet

- Savca GidsDocument164 pagesSavca GidsNetwerk24SakeNo ratings yet

- Resource - Case StudyDocument7 pagesResource - Case StudyYuuki KiryuuNo ratings yet

- Accounting BasicsDocument124 pagesAccounting Basicssalman3533467No ratings yet

- Chapter ThreeDocument20 pagesChapter ThreeNatty STAN100% (1)

- Accounting For Merchandising Activities: Solutions Manual For Chapter 6 435Document163 pagesAccounting For Merchandising Activities: Solutions Manual For Chapter 6 435debora yosikaNo ratings yet

- Horngrens Financial and Managerial Accounting The Financial Chapters 5Th Edition Miller Nobles Solutions Manual Full Chapter PDFDocument36 pagesHorngrens Financial and Managerial Accounting The Financial Chapters 5Th Edition Miller Nobles Solutions Manual Full Chapter PDFjestine.wesson615100% (17)

- 605 Chapter 6Document26 pages605 Chapter 6阿锭No ratings yet

- ACCT 1005 - Summary Notes 5 - Merchandising Businesses - 2015Document6 pagesACCT 1005 - Summary Notes 5 - Merchandising Businesses - 2015Kenya LevyNo ratings yet

- Lecture Notes - Topic 3Document22 pagesLecture Notes - Topic 3Nguyen LauraNo ratings yet

- Tools For Business Decision Making, 2nd Ed.: Kimmel, Weygandt, KiesoDocument61 pagesTools For Business Decision Making, 2nd Ed.: Kimmel, Weygandt, KiesoMoath AlobaidyNo ratings yet

- IFA Chapter 3Document97 pagesIFA Chapter 3kqk07829No ratings yet

- Periodic PerpetualDocument25 pagesPeriodic PerpetualNunung Nurul100% (1)

- 4 Exam Part 2Document4 pages4 Exam Part 2RJ DAVE DURUHANo ratings yet

- Group Work #11 FinishedDocument4 pagesGroup Work #11 FinishedМиша КосяковNo ratings yet

- Answer To Account RecivablesDocument2 pagesAnswer To Account RecivablesEleni MulualemNo ratings yet

- Achievement Test 3.chapters 5&6Document9 pagesAchievement Test 3.chapters 5&6Quỳnh Vũ100% (1)

- CH06Document80 pagesCH06shelategosongNo ratings yet

- VET PROGRAM TITLE: Accounts and Budget Support LevelDocument3 pagesVET PROGRAM TITLE: Accounts and Budget Support LevelRuth AsratNo ratings yet

- MBA - Accounting Management: Group 2 Ms. Odessa Jarina Ms. Beatrix Rose Beltijar Mr. Edmer GatchalianDocument10 pagesMBA - Accounting Management: Group 2 Ms. Odessa Jarina Ms. Beatrix Rose Beltijar Mr. Edmer Gatchaliancluadine dinerosNo ratings yet

- ACCT101 Chapter 4Document14 pagesACCT101 Chapter 4Lez MarquezNo ratings yet

- Chapter 6 SolutionsDocument12 pagesChapter 6 SolutionsLaura CarsonNo ratings yet

- Intermediate Accounting IFRS 3rd Edition-574-576Document3 pagesIntermediate Accounting IFRS 3rd Edition-574-576dindaNo ratings yet

- Module 11 - Accounting Cycle For Merchandising BusDocument29 pagesModule 11 - Accounting Cycle For Merchandising Busgerlie gabriel100% (1)

- Chapter 61Document7 pagesChapter 61Jay PaleroNo ratings yet

- Chapter 8Document11 pagesChapter 8Paw VerdilloNo ratings yet

- Chapter 6 - ACCT 3311 FlashcardsDocument5 pagesChapter 6 - ACCT 3311 Flashcardsanissa claritaNo ratings yet

- Chapter 8Document44 pagesChapter 8Rifki OksantikaNo ratings yet

- Fa-I Chapter 7Document16 pagesFa-I Chapter 7Hussen AbdulkadirNo ratings yet

- Accounting Chapter 3Document6 pagesAccounting Chapter 3Yana PrihartiniNo ratings yet

- 4 Special Journal UDDocument33 pages4 Special Journal UDERICK MLINGWA100% (1)

- Chapter 3 ReceivablesDocument22 pagesChapter 3 ReceivablesCale Robert RascoNo ratings yet

- Cash Management TechniquesDocument39 pagesCash Management TechniquesDharmendra ThakurNo ratings yet

- IPPTChap 006 Williams 17 eDocument70 pagesIPPTChap 006 Williams 17 eRida ChamiNo ratings yet

- Reporting and Analyzing Receivables Answers To QuestionsDocument57 pagesReporting and Analyzing Receivables Answers To Questionsislandguy19100% (3)

- Module 3. Part 1 - Accounts Receivable For StudentsDocument36 pagesModule 3. Part 1 - Accounts Receivable For Studentslord kwantoniumNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument21 pagesAccounting Cycle of A Merchandising Businesszedrick edenNo ratings yet

- Audit of The Sales and Collection Cycle: Tests of Controls Review Questions 12-1Document22 pagesAudit of The Sales and Collection Cycle: Tests of Controls Review Questions 12-1Tilahun MikiasNo ratings yet

- Periodic Inventory PDFDocument33 pagesPeriodic Inventory PDF48pgcw62kkNo ratings yet

- 3.03 Key TermsDocument95 pages3.03 Key Termsapi-262218593No ratings yet

- Thẻ ghi nhớ - Finacial Accounting Chapter 5 Review - QuizletDocument6 pagesThẻ ghi nhớ - Finacial Accounting Chapter 5 Review - QuizletAn Ngoc CồNo ratings yet

- Chapter 7-8 QuestionsDocument5 pagesChapter 7-8 QuestionsMya B. WalkerNo ratings yet

- Merchandising BusinessDocument89 pagesMerchandising BusinessGSOCION LOUSELLE LALAINE D.No ratings yet

- Financial AccountingDocument66 pagesFinancial AccountingFaisal SaleemNo ratings yet

- ACCT - Quiz 4Document3 pagesACCT - Quiz 4Florencio FanoNo ratings yet

- Chapter 5 2nd TermDocument6 pagesChapter 5 2nd TermFintech GroupNo ratings yet

- Perpetual Inventory SystemDocument8 pagesPerpetual Inventory SystemJancee kye BarcemoNo ratings yet

- FAC1501 Study Guide 2024 - Learning Unit 6Document44 pagesFAC1501 Study Guide 2024 - Learning Unit 6SneguguNo ratings yet

- Fabm 1: Accounting For Merchandising ConcernDocument29 pagesFabm 1: Accounting For Merchandising ConcernJan Vincent A. LadresNo ratings yet

- Dr. Filemon C. Aguilar Memorial College of Las Pinas: Golden Gate Subdivision, Talon III, Las Pinas, 1747 Metro ManilaDocument18 pagesDr. Filemon C. Aguilar Memorial College of Las Pinas: Golden Gate Subdivision, Talon III, Las Pinas, 1747 Metro ManilaOliver AbordoNo ratings yet

- Chap 05 - Merchandising Operations and The Multiple-Step Income Statement (ICA)Document7 pagesChap 05 - Merchandising Operations and The Multiple-Step Income Statement (ICA)Mohamed DiabNo ratings yet

- Acctg Introduction To Merchandising BusinessDocument39 pagesAcctg Introduction To Merchandising BusinessDaisy Marie A. RoselNo ratings yet

- Lecture, Chap. 5Document5 pagesLecture, Chap. 5Moshe FarzanNo ratings yet

- Accounting CH 5Document13 pagesAccounting CH 5Kristilyn CartaNo ratings yet

- Cash and Receivables: ObjectivesDocument25 pagesCash and Receivables: ObjectivesAlex OuedraogoNo ratings yet

- QuickBooks Online for Beginners: A Quick Reference and Step-by-Step Guide to Mastering QuickBooks Online for Small Business Owners from Beginners to ExpertFrom EverandQuickBooks Online for Beginners: A Quick Reference and Step-by-Step Guide to Mastering QuickBooks Online for Small Business Owners from Beginners to ExpertNo ratings yet

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- Ch07 WRD25e Instructor-1Document87 pagesCh07 WRD25e Instructor-1fahri kurniawanNo ratings yet

- PPT Chapter 8 Internal Control and CashDocument39 pagesPPT Chapter 8 Internal Control and Cashfahri kurniawanNo ratings yet

- Subjek, Objek, Peristiwa & Perbuatan Hukum - D Iii Akunt 2018 - 2019Document16 pagesSubjek, Objek, Peristiwa & Perbuatan Hukum - D Iii Akunt 2018 - 2019fahri kurniawanNo ratings yet

- Week 13 - Conditionals 2019Document20 pagesWeek 13 - Conditionals 2019fahri kurniawanNo ratings yet

- Week 9 - Noun ClauseDocument31 pagesWeek 9 - Noun Clausefahri kurniawanNo ratings yet

- UUEG Chapter17 Adverb ClausesDocument34 pagesUUEG Chapter17 Adverb Clausesfahri kurniawanNo ratings yet

- TRADE THE MARKETS Week3Document9 pagesTRADE THE MARKETS Week3Nidhi0% (1)

- Lecture Notes - International Business Environment PDFDocument87 pagesLecture Notes - International Business Environment PDFPoudel SathiNo ratings yet

- Policies & Founder Characteristics of New Technology A Comparison Between British & Indian FirmsDocument47 pagesPolicies & Founder Characteristics of New Technology A Comparison Between British & Indian Firmspearll86No ratings yet

- PO Defaulting RuleDocument9 pagesPO Defaulting Rulecoolguy0606No ratings yet

- Anmol - Choubey - e - 07 - Anmol ChoubeyDocument15 pagesAnmol - Choubey - e - 07 - Anmol ChoubeyTabrej AlamNo ratings yet

- Capital Gains - Stocks-GrowwDocument11 pagesCapital Gains - Stocks-Growwriyagupta10122000No ratings yet

- 19Document3 pages19Kristine Arsolon100% (2)

- Executive Summary: S11158164 S11157500 S11157427 S11159403 S11158400Document12 pagesExecutive Summary: S11158164 S11157500 S11157427 S11159403 S11158400Navin N Meenakshi ChandraNo ratings yet

- Chapter 7 - SCMDocument11 pagesChapter 7 - SCMhieuanhshinochiNo ratings yet

- Bri AgustusDocument3 pagesBri AgustusdinoNo ratings yet

- CRM at HDFCDocument16 pagesCRM at HDFCjini54No ratings yet

- ARK Innovation ETF: Holdings Data - ARKKDocument2 pagesARK Innovation ETF: Holdings Data - ARKKtimNo ratings yet

- Chapter 9 Multiple-Choice QuizDocument4 pagesChapter 9 Multiple-Choice Quizලකි යාNo ratings yet

- Tax Invoice: Shipping AddressDocument1 pageTax Invoice: Shipping AddressK4TALIN K4TALINNo ratings yet

- fb-2018Document832 pagesfb-2018Gabrielle GeraldineNo ratings yet

- Importance of Gold: in Indian EconomyDocument4 pagesImportance of Gold: in Indian EconomyTapan anandNo ratings yet

- CRM in Airline IndustryDocument19 pagesCRM in Airline IndustryPooja PatnaikNo ratings yet

- Armarium Report - Group 1Document5 pagesArmarium Report - Group 1mitali.199022100% (1)

- Sample of mkt202 ProjectDocument16 pagesSample of mkt202 ProjectMohammad Sohan Khan 2121426630No ratings yet

- 378490Document24 pages378490Sarin SayalNo ratings yet

- Start Your Business 1-7-2004Document91 pagesStart Your Business 1-7-2004strength, courage, and wisdomNo ratings yet

- FNB Statement May 2023Document2 pagesFNB Statement May 2023Danny Wilson100% (1)

- Clothing Business PlanDocument30 pagesClothing Business PlanBabmani Mani50% (2)

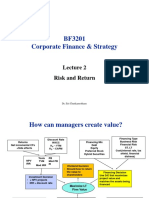

- BF3201 Corporate Finance & Strategy: Risk and ReturnDocument54 pagesBF3201 Corporate Finance & Strategy: Risk and ReturnkaiwenNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Bitcoin To $1M, Ethereum To $180,000 by 2030 ARKDocument1 pageBitcoin To $1M, Ethereum To $180,000 by 2030 ARKOwen HalpertNo ratings yet

- Libby Financial Accounting Chapter6Document6 pagesLibby Financial Accounting Chapter6Jie Bo TiNo ratings yet

- Scope of White Label ATMs Business in PakistanDocument15 pagesScope of White Label ATMs Business in PakistanSay Pakistan100% (1)

- Brand Building Blocks: First Pepsi AdDocument2 pagesBrand Building Blocks: First Pepsi AdBarson MithunNo ratings yet

- Monitoring and Controlling Accounts Receivable PDFDocument45 pagesMonitoring and Controlling Accounts Receivable PDFnigusNo ratings yet

- AIS Chapter FourDocument14 pagesAIS Chapter FourNaod MekonnenNo ratings yet

- Administering Subsidiary Accounts and Ledgers PDFDocument33 pagesAdministering Subsidiary Accounts and Ledgers PDFnigus78% (9)

- Bonds and Stocks SolutionsDocument3 pagesBonds and Stocks SolutionsLucas AbudNo ratings yet

- Savca GidsDocument164 pagesSavca GidsNetwerk24SakeNo ratings yet

- Resource - Case StudyDocument7 pagesResource - Case StudyYuuki KiryuuNo ratings yet

- Accounting BasicsDocument124 pagesAccounting Basicssalman3533467No ratings yet

- Chapter ThreeDocument20 pagesChapter ThreeNatty STAN100% (1)

- Accounting For Merchandising Activities: Solutions Manual For Chapter 6 435Document163 pagesAccounting For Merchandising Activities: Solutions Manual For Chapter 6 435debora yosikaNo ratings yet

- Horngrens Financial and Managerial Accounting The Financial Chapters 5Th Edition Miller Nobles Solutions Manual Full Chapter PDFDocument36 pagesHorngrens Financial and Managerial Accounting The Financial Chapters 5Th Edition Miller Nobles Solutions Manual Full Chapter PDFjestine.wesson615100% (17)

- 605 Chapter 6Document26 pages605 Chapter 6阿锭No ratings yet

- ACCT 1005 - Summary Notes 5 - Merchandising Businesses - 2015Document6 pagesACCT 1005 - Summary Notes 5 - Merchandising Businesses - 2015Kenya LevyNo ratings yet

- Lecture Notes - Topic 3Document22 pagesLecture Notes - Topic 3Nguyen LauraNo ratings yet

- Tools For Business Decision Making, 2nd Ed.: Kimmel, Weygandt, KiesoDocument61 pagesTools For Business Decision Making, 2nd Ed.: Kimmel, Weygandt, KiesoMoath AlobaidyNo ratings yet

- IFA Chapter 3Document97 pagesIFA Chapter 3kqk07829No ratings yet

- Periodic PerpetualDocument25 pagesPeriodic PerpetualNunung Nurul100% (1)

- 4 Exam Part 2Document4 pages4 Exam Part 2RJ DAVE DURUHANo ratings yet

- Group Work #11 FinishedDocument4 pagesGroup Work #11 FinishedМиша КосяковNo ratings yet

- Answer To Account RecivablesDocument2 pagesAnswer To Account RecivablesEleni MulualemNo ratings yet

- Achievement Test 3.chapters 5&6Document9 pagesAchievement Test 3.chapters 5&6Quỳnh Vũ100% (1)

- CH06Document80 pagesCH06shelategosongNo ratings yet

- VET PROGRAM TITLE: Accounts and Budget Support LevelDocument3 pagesVET PROGRAM TITLE: Accounts and Budget Support LevelRuth AsratNo ratings yet

- MBA - Accounting Management: Group 2 Ms. Odessa Jarina Ms. Beatrix Rose Beltijar Mr. Edmer GatchalianDocument10 pagesMBA - Accounting Management: Group 2 Ms. Odessa Jarina Ms. Beatrix Rose Beltijar Mr. Edmer Gatchaliancluadine dinerosNo ratings yet

- ACCT101 Chapter 4Document14 pagesACCT101 Chapter 4Lez MarquezNo ratings yet

- Chapter 6 SolutionsDocument12 pagesChapter 6 SolutionsLaura CarsonNo ratings yet

- Intermediate Accounting IFRS 3rd Edition-574-576Document3 pagesIntermediate Accounting IFRS 3rd Edition-574-576dindaNo ratings yet

- Module 11 - Accounting Cycle For Merchandising BusDocument29 pagesModule 11 - Accounting Cycle For Merchandising Busgerlie gabriel100% (1)

- Chapter 61Document7 pagesChapter 61Jay PaleroNo ratings yet

- Chapter 8Document11 pagesChapter 8Paw VerdilloNo ratings yet

- Chapter 6 - ACCT 3311 FlashcardsDocument5 pagesChapter 6 - ACCT 3311 Flashcardsanissa claritaNo ratings yet

- Chapter 8Document44 pagesChapter 8Rifki OksantikaNo ratings yet

- Fa-I Chapter 7Document16 pagesFa-I Chapter 7Hussen AbdulkadirNo ratings yet

- Accounting Chapter 3Document6 pagesAccounting Chapter 3Yana PrihartiniNo ratings yet

- 4 Special Journal UDDocument33 pages4 Special Journal UDERICK MLINGWA100% (1)

- Chapter 3 ReceivablesDocument22 pagesChapter 3 ReceivablesCale Robert RascoNo ratings yet

- Cash Management TechniquesDocument39 pagesCash Management TechniquesDharmendra ThakurNo ratings yet

- IPPTChap 006 Williams 17 eDocument70 pagesIPPTChap 006 Williams 17 eRida ChamiNo ratings yet

- Reporting and Analyzing Receivables Answers To QuestionsDocument57 pagesReporting and Analyzing Receivables Answers To Questionsislandguy19100% (3)

- Module 3. Part 1 - Accounts Receivable For StudentsDocument36 pagesModule 3. Part 1 - Accounts Receivable For Studentslord kwantoniumNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument21 pagesAccounting Cycle of A Merchandising Businesszedrick edenNo ratings yet

- Audit of The Sales and Collection Cycle: Tests of Controls Review Questions 12-1Document22 pagesAudit of The Sales and Collection Cycle: Tests of Controls Review Questions 12-1Tilahun MikiasNo ratings yet

- Periodic Inventory PDFDocument33 pagesPeriodic Inventory PDF48pgcw62kkNo ratings yet

- 3.03 Key TermsDocument95 pages3.03 Key Termsapi-262218593No ratings yet

- Thẻ ghi nhớ - Finacial Accounting Chapter 5 Review - QuizletDocument6 pagesThẻ ghi nhớ - Finacial Accounting Chapter 5 Review - QuizletAn Ngoc CồNo ratings yet

- Chapter 7-8 QuestionsDocument5 pagesChapter 7-8 QuestionsMya B. WalkerNo ratings yet

- Merchandising BusinessDocument89 pagesMerchandising BusinessGSOCION LOUSELLE LALAINE D.No ratings yet

- Financial AccountingDocument66 pagesFinancial AccountingFaisal SaleemNo ratings yet

- ACCT - Quiz 4Document3 pagesACCT - Quiz 4Florencio FanoNo ratings yet

- Chapter 5 2nd TermDocument6 pagesChapter 5 2nd TermFintech GroupNo ratings yet

- Perpetual Inventory SystemDocument8 pagesPerpetual Inventory SystemJancee kye BarcemoNo ratings yet

- FAC1501 Study Guide 2024 - Learning Unit 6Document44 pagesFAC1501 Study Guide 2024 - Learning Unit 6SneguguNo ratings yet

- Fabm 1: Accounting For Merchandising ConcernDocument29 pagesFabm 1: Accounting For Merchandising ConcernJan Vincent A. LadresNo ratings yet

- Dr. Filemon C. Aguilar Memorial College of Las Pinas: Golden Gate Subdivision, Talon III, Las Pinas, 1747 Metro ManilaDocument18 pagesDr. Filemon C. Aguilar Memorial College of Las Pinas: Golden Gate Subdivision, Talon III, Las Pinas, 1747 Metro ManilaOliver AbordoNo ratings yet

- Chap 05 - Merchandising Operations and The Multiple-Step Income Statement (ICA)Document7 pagesChap 05 - Merchandising Operations and The Multiple-Step Income Statement (ICA)Mohamed DiabNo ratings yet

- Acctg Introduction To Merchandising BusinessDocument39 pagesAcctg Introduction To Merchandising BusinessDaisy Marie A. RoselNo ratings yet

- Lecture, Chap. 5Document5 pagesLecture, Chap. 5Moshe FarzanNo ratings yet

- Accounting CH 5Document13 pagesAccounting CH 5Kristilyn CartaNo ratings yet

- Cash and Receivables: ObjectivesDocument25 pagesCash and Receivables: ObjectivesAlex OuedraogoNo ratings yet

- QuickBooks Online for Beginners: A Quick Reference and Step-by-Step Guide to Mastering QuickBooks Online for Small Business Owners from Beginners to ExpertFrom EverandQuickBooks Online for Beginners: A Quick Reference and Step-by-Step Guide to Mastering QuickBooks Online for Small Business Owners from Beginners to ExpertNo ratings yet

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- Ch07 WRD25e Instructor-1Document87 pagesCh07 WRD25e Instructor-1fahri kurniawanNo ratings yet

- PPT Chapter 8 Internal Control and CashDocument39 pagesPPT Chapter 8 Internal Control and Cashfahri kurniawanNo ratings yet

- Subjek, Objek, Peristiwa & Perbuatan Hukum - D Iii Akunt 2018 - 2019Document16 pagesSubjek, Objek, Peristiwa & Perbuatan Hukum - D Iii Akunt 2018 - 2019fahri kurniawanNo ratings yet

- Week 13 - Conditionals 2019Document20 pagesWeek 13 - Conditionals 2019fahri kurniawanNo ratings yet

- Week 9 - Noun ClauseDocument31 pagesWeek 9 - Noun Clausefahri kurniawanNo ratings yet

- UUEG Chapter17 Adverb ClausesDocument34 pagesUUEG Chapter17 Adverb Clausesfahri kurniawanNo ratings yet

- TRADE THE MARKETS Week3Document9 pagesTRADE THE MARKETS Week3Nidhi0% (1)

- Lecture Notes - International Business Environment PDFDocument87 pagesLecture Notes - International Business Environment PDFPoudel SathiNo ratings yet

- Policies & Founder Characteristics of New Technology A Comparison Between British & Indian FirmsDocument47 pagesPolicies & Founder Characteristics of New Technology A Comparison Between British & Indian Firmspearll86No ratings yet

- PO Defaulting RuleDocument9 pagesPO Defaulting Rulecoolguy0606No ratings yet

- Anmol - Choubey - e - 07 - Anmol ChoubeyDocument15 pagesAnmol - Choubey - e - 07 - Anmol ChoubeyTabrej AlamNo ratings yet

- Capital Gains - Stocks-GrowwDocument11 pagesCapital Gains - Stocks-Growwriyagupta10122000No ratings yet

- 19Document3 pages19Kristine Arsolon100% (2)

- Executive Summary: S11158164 S11157500 S11157427 S11159403 S11158400Document12 pagesExecutive Summary: S11158164 S11157500 S11157427 S11159403 S11158400Navin N Meenakshi ChandraNo ratings yet

- Chapter 7 - SCMDocument11 pagesChapter 7 - SCMhieuanhshinochiNo ratings yet

- Bri AgustusDocument3 pagesBri AgustusdinoNo ratings yet

- CRM at HDFCDocument16 pagesCRM at HDFCjini54No ratings yet

- ARK Innovation ETF: Holdings Data - ARKKDocument2 pagesARK Innovation ETF: Holdings Data - ARKKtimNo ratings yet

- Chapter 9 Multiple-Choice QuizDocument4 pagesChapter 9 Multiple-Choice Quizලකි යාNo ratings yet

- Tax Invoice: Shipping AddressDocument1 pageTax Invoice: Shipping AddressK4TALIN K4TALINNo ratings yet

- fb-2018Document832 pagesfb-2018Gabrielle GeraldineNo ratings yet

- Importance of Gold: in Indian EconomyDocument4 pagesImportance of Gold: in Indian EconomyTapan anandNo ratings yet

- CRM in Airline IndustryDocument19 pagesCRM in Airline IndustryPooja PatnaikNo ratings yet

- Armarium Report - Group 1Document5 pagesArmarium Report - Group 1mitali.199022100% (1)

- Sample of mkt202 ProjectDocument16 pagesSample of mkt202 ProjectMohammad Sohan Khan 2121426630No ratings yet

- 378490Document24 pages378490Sarin SayalNo ratings yet

- Start Your Business 1-7-2004Document91 pagesStart Your Business 1-7-2004strength, courage, and wisdomNo ratings yet

- FNB Statement May 2023Document2 pagesFNB Statement May 2023Danny Wilson100% (1)

- Clothing Business PlanDocument30 pagesClothing Business PlanBabmani Mani50% (2)

- BF3201 Corporate Finance & Strategy: Risk and ReturnDocument54 pagesBF3201 Corporate Finance & Strategy: Risk and ReturnkaiwenNo ratings yet