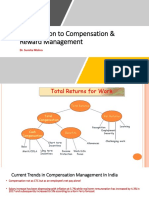

L8 Remuneration

L8 Remuneration

You might also like

- Lessons from Private Equity Any Company Can UseFrom EverandLessons from Private Equity Any Company Can UseRating: 4.5 out of 5 stars4.5/5 (12)

- What Is CEO Talent Worth?Document7 pagesWhat Is CEO Talent Worth?Brian TayanNo ratings yet

- 4 Hoi and RobinDocument7 pages4 Hoi and RobinelizabetaangelovaNo ratings yet

- Director Optimal Pay Against Fat Cats in Taiwan: and Finance Research Vol. 4, No. 3 2015Document9 pagesDirector Optimal Pay Against Fat Cats in Taiwan: and Finance Research Vol. 4, No. 3 2015peter weinNo ratings yet

- Dividend Policy As Strategic Tool of Financing in Public Firms: Evidence From NigeriaDocument24 pagesDividend Policy As Strategic Tool of Financing in Public Firms: Evidence From Nigeriay_378602342No ratings yet

- 08 Chapter 1 - Managerial RemunerationDocument26 pages08 Chapter 1 - Managerial RemunerationMbaStudent56No ratings yet

- Determinants of Dividend Payout Ratios: Evidence From United StatesDocument7 pagesDeterminants of Dividend Payout Ratios: Evidence From United StatesSri Wahyuningsih AhmadNo ratings yet

- Subba ReddyDocument47 pagesSubba Reddyankitjaipur0% (1)

- Chap 8 - Executive Compensation and IncentivesDocument19 pagesChap 8 - Executive Compensation and IncentivesHM.No ratings yet

- Journal of Accounting and Economics 7Document35 pagesJournal of Accounting and Economics 7Ovilia Intan DoniarNo ratings yet

- DGYoung Dentist PresentationDocument103 pagesDGYoung Dentist PresentationD.WorkuNo ratings yet

- Distributions To Shareholders: Dividends and Repurchases: Batangas State UniversityDocument41 pagesDistributions To Shareholders: Dividends and Repurchases: Batangas State UniversityNicole AnditNo ratings yet

- Chapter 17 - Earnings Per Share and Retained Earnings PDFDocument59 pagesChapter 17 - Earnings Per Share and Retained Earnings PDFDaniela MacaveiuNo ratings yet

- 6818-Article Text-13380-1-10-20210226Document7 pages6818-Article Text-13380-1-10-20210226maruzaks123No ratings yet

- International Review of Economics and FinanceDocument16 pagesInternational Review of Economics and FinanceAYUNo ratings yet

- Is The Dividend Puzzle Solved - RDocument9 pagesIs The Dividend Puzzle Solved - RUyen TranNo ratings yet

- Rvunc Department of Management: Mba Program Course Title: Financial and Managerial Accounting Course Code: Mbad612Document3 pagesRvunc Department of Management: Mba Program Course Title: Financial and Managerial Accounting Course Code: Mbad612markosNo ratings yet

- Dividend Policy: Saurty Shekyn Das (1310709) BSC (Hons) Finance (Minor: Law) Dfa2002Y (3) Corporate Finance 20 April 2015Document9 pagesDividend Policy: Saurty Shekyn Das (1310709) BSC (Hons) Finance (Minor: Law) Dfa2002Y (3) Corporate Finance 20 April 2015Anonymous H2L7lwBs3No ratings yet

- The Relationship Between Dividend Payout and Financial Performance: Evidence From Top40 JSE FirmsDocument15 pagesThe Relationship Between Dividend Payout and Financial Performance: Evidence From Top40 JSE FirmsLouise Barik- بريطانية مغربيةNo ratings yet

- Matolcsy 2010Document19 pagesMatolcsy 2010amirhayat15No ratings yet

- Pledge (And Hedge) Allegiance To The CompanyDocument6 pagesPledge (And Hedge) Allegiance To The CompanyBrian TayanNo ratings yet

- Cesari 2015Document17 pagesCesari 2015Nicoara AdrianNo ratings yet

- Advances Research DocumentDocument12 pagesAdvances Research DocumentParvez AliNo ratings yet

- Developing Performance Incentives and Sustaining Engagement in A Volatile EnvironmentDocument42 pagesDeveloping Performance Incentives and Sustaining Engagement in A Volatile EnvironmentPrathamesh ParkarNo ratings yet

- American Accounting Association The Accounting ReviewDocument22 pagesAmerican Accounting Association The Accounting ReviewFTU.CS2 Nguyễn Hồ DanhNo ratings yet

- Dividend Policy: Firm Has 2 ChoicesDocument18 pagesDividend Policy: Firm Has 2 ChoicesRajat LoyaNo ratings yet

- The Role of Employees in Corporate GovernanceDocument19 pagesThe Role of Employees in Corporate Governancemanish byanjankarNo ratings yet

- Corm 1Document38 pagesCorm 1MAYURIKANo ratings yet

- C30CY Week 8 LectureDocument50 pagesC30CY Week 8 Lecturejohnshabin123No ratings yet

- C2A October 2011 Exam PDFDocument8 pagesC2A October 2011 Exam PDFJeff GundyNo ratings yet

- Nnadi Et Tanna 2011 Multivariate Analyses of Factors Affecting Dividend Policy of AcquiredDocument20 pagesNnadi Et Tanna 2011 Multivariate Analyses of Factors Affecting Dividend Policy of AcquiredismailNo ratings yet

- The Determinants of Dividend Policy: Evidence From Malaysian FirmsDocument20 pagesThe Determinants of Dividend Policy: Evidence From Malaysian FirmsIzzatieNo ratings yet

- Corm 1Document38 pagesCorm 1MAYURIKANo ratings yet

- Impact of Firm Specific Variables On Dividend Payout of Nepalese BanksDocument13 pagesImpact of Firm Specific Variables On Dividend Payout of Nepalese BanksMani ManandharNo ratings yet

- Healy-The Effect of Bonus Schemes On Accounting DecisionsDocument23 pagesHealy-The Effect of Bonus Schemes On Accounting DecisionsarfanysNo ratings yet

- 12 - 8 - Determinants of Dividend Payout in Private Insurance Companies of Ethiopia - PDFDocument7 pages12 - 8 - Determinants of Dividend Payout in Private Insurance Companies of Ethiopia - PDFYohanisNo ratings yet

- Total Shareholders' ReturnDocument32 pagesTotal Shareholders' ReturnAmmi JulianNo ratings yet

- International Journal in Multidisciplinary and Academic Research (SSIJMAR) Vol. 3, No. 1, February-March - 2014 (ISSN 2278 - 5973)Document16 pagesInternational Journal in Multidisciplinary and Academic Research (SSIJMAR) Vol. 3, No. 1, February-March - 2014 (ISSN 2278 - 5973)Siva KalimuthuNo ratings yet

- Stakeholders 2Document25 pagesStakeholders 2Sebastián Posada100% (1)

- Chap 001Document17 pagesChap 001Raju_RNO EnggNo ratings yet

- DividendDocument30 pagesDividendFaruqNo ratings yet

- Stock Buyback 4Document15 pagesStock Buyback 4sethNo ratings yet

- Assignment 14Document7 pagesAssignment 14Satishkumar NagarajNo ratings yet

- Corporate Finance in 30 Minutes: A Guide For Directors and ShareholdersDocument14 pagesCorporate Finance in 30 Minutes: A Guide For Directors and ShareholdersMarcelo Vieira100% (1)

- The Relationship Between Dividend Payout and Financial Performance: Evidence From Top40 JSE FirmsDocument16 pagesThe Relationship Between Dividend Payout and Financial Performance: Evidence From Top40 JSE Firmsmaruzaks123No ratings yet

- Finance QuestionsDocument6 pagesFinance QuestionsCream FamilyNo ratings yet

- Pensions As A Form of Executive Compensation: L G Y LDocument35 pagesPensions As A Form of Executive Compensation: L G Y LFabiana SeverianoNo ratings yet

- The Macro Impact of Short-Termism15420-4Document45 pagesThe Macro Impact of Short-Termism15420-4dk773No ratings yet

- Assignment - VALIDITY OF THE LINTNER MODEL ON MAURITIAN CAPITAL MARKET PDFDocument25 pagesAssignment - VALIDITY OF THE LINTNER MODEL ON MAURITIAN CAPITAL MARKET PDFSamba BahNo ratings yet

- Dividend PolicyDocument8 pagesDividend PolicyHarsh SethiaNo ratings yet

- Presentation On: Compensation ManagementDocument29 pagesPresentation On: Compensation Managementarun_aglNo ratings yet

- Journal of Corporate Finance: Naoya Mori, Naoshi IkedaDocument10 pagesJournal of Corporate Finance: Naoya Mori, Naoshi IkedaZahra BatoolNo ratings yet

- Pay Perf Report 110812Document25 pagesPay Perf Report 110812brandon-harris-6868No ratings yet

- 7 Myths of Corporate GovernanceDocument10 pages7 Myths of Corporate GovernanceJawad UmarNo ratings yet

- Dividend Policy, Agency Costs, and Earned EquityDocument35 pagesDividend Policy, Agency Costs, and Earned EquityhhhhhhhNo ratings yet

- R&D Investments and Dividend Payout: Evidence Concerning The Semi-Mandatory Dividend Policy in ChinaDocument37 pagesR&D Investments and Dividend Payout: Evidence Concerning The Semi-Mandatory Dividend Policy in ChinadeviundipNo ratings yet

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveFrom EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNo ratings yet

- The Declaration of Dependence: Dividends in the Twenty-First CenturyFrom EverandThe Declaration of Dependence: Dividends in the Twenty-First CenturyNo ratings yet

- Outperform with Expectations-Based Management: A State-of-the-Art Approach to Creating and Enhancing Shareholder ValueFrom EverandOutperform with Expectations-Based Management: A State-of-the-Art Approach to Creating and Enhancing Shareholder ValueNo ratings yet

- Dividend Growth Investing: The Ultimate Investing Guide. Learn Effective Strategies to Create Passive Income for Your Future.From EverandDividend Growth Investing: The Ultimate Investing Guide. Learn Effective Strategies to Create Passive Income for Your Future.No ratings yet

- Bbi 2Document39 pagesBbi 2RESHMANo ratings yet

- Isda 2002 Master Agreement: Understanding The New Isda Documentation ConferenceDocument66 pagesIsda 2002 Master Agreement: Understanding The New Isda Documentation ConferencepapillonnnnNo ratings yet

- Corporate Governance (Baec0007) NewDocument46 pagesCorporate Governance (Baec0007) NewankitaaecsaxenaNo ratings yet

- Century Enka Limited: Analysis of Company's Financial StatementDocument24 pagesCentury Enka Limited: Analysis of Company's Financial StatementAnand PurohitNo ratings yet

- SM Prime Holdings Inc.: Integrated Annual Corporate Governance Report Analysis ReportDocument2 pagesSM Prime Holdings Inc.: Integrated Annual Corporate Governance Report Analysis Reportbelle crisNo ratings yet

- W1-Part 2-Additional-Ch 3-SaT-FIN 410Document7 pagesW1-Part 2-Additional-Ch 3-SaT-FIN 410Syed Aquib AbbasNo ratings yet

- Penerapan Sistem Pengendalian Internal Dengan CosoDocument17 pagesPenerapan Sistem Pengendalian Internal Dengan CosoFardian FardianNo ratings yet

- What Is Auditing ProcessDocument3 pagesWhat Is Auditing ProcessAizaButtNo ratings yet

- CJR English For BusinessDocument18 pagesCJR English For BusinessKristina SihombingNo ratings yet

- Various Committees On Corporate GovernanceDocument11 pagesVarious Committees On Corporate GovernanceFouzia imzNo ratings yet

- BAFI1018 International FinanceDocument109 pagesBAFI1018 International FinanceSteven NgNo ratings yet

- Lovello Annual Report 2021 22Document159 pagesLovello Annual Report 2021 22aribNo ratings yet

- Annual Report PT Pegadaian 2021Document536 pagesAnnual Report PT Pegadaian 2021bseptiyantoNo ratings yet

- Models of Corporate GovernanceDocument10 pagesModels of Corporate GovernanceNeil patrickNo ratings yet

- AccountabilityDocument15 pagesAccountabilityRavi SinghNo ratings yet

- Session 2. The COSO ERM Framework in DetailDocument18 pagesSession 2. The COSO ERM Framework in DetailManish AroraNo ratings yet

- Corporate Accounting Frauds 16112013Document27 pagesCorporate Accounting Frauds 16112013teammrauNo ratings yet

- Transportation 4-5-17Document39 pagesTransportation 4-5-17Punit Singh SardarNo ratings yet

- 7.1a Principal-Protected Notes: Trading Strategies Involving OptionsDocument14 pages7.1a Principal-Protected Notes: Trading Strategies Involving OptionsAnDy YiMNo ratings yet

- Agenda Item 1.4: IPSAS-IFRS Alignment Dashboard OverviewDocument23 pagesAgenda Item 1.4: IPSAS-IFRS Alignment Dashboard OverviewHadera TesfayNo ratings yet

- 20 ArrendamientosDocument87 pages20 ArrendamientosCarlos Eduardo LoveraNo ratings yet

- Code of Corporate Governance As Issued by Bangladesh Securities Exchange Commission in 2006 and Subsequent Modifications To Highlight Measures Aimed at Better Financial ManagementDocument4 pagesCode of Corporate Governance As Issued by Bangladesh Securities Exchange Commission in 2006 and Subsequent Modifications To Highlight Measures Aimed at Better Financial ManagementMahin KhanNo ratings yet

- Annual Report 2017-2018 PDFDocument90 pagesAnnual Report 2017-2018 PDFMuhmmad Sheikh AmanNo ratings yet

- Comparison Between HK Financial Reporting Standards and International Financial Reporting StandardsDocument29 pagesComparison Between HK Financial Reporting Standards and International Financial Reporting Standardsisaac2008100% (1)

- Takis Katsoulakos and Yannis KatsoulacosDocument15 pagesTakis Katsoulakos and Yannis KatsoulacosSebastianNo ratings yet

- Audit Committee, Internal Audit Function and Earnings Management: Evidence From JordanDocument19 pagesAudit Committee, Internal Audit Function and Earnings Management: Evidence From JordanNadeem TahaNo ratings yet

- KESC Annual-Report-2013Document197 pagesKESC Annual-Report-2013makhalidiNo ratings yet

- Bahan Metod 1Document7 pagesBahan Metod 1Gaura HarieNo ratings yet

- Naked OptionDocument3 pagesNaked OptionRayzwanRayzmanNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Lessons from Private Equity Any Company Can UseFrom EverandLessons from Private Equity Any Company Can UseRating: 4.5 out of 5 stars4.5/5 (12)

- What Is CEO Talent Worth?Document7 pagesWhat Is CEO Talent Worth?Brian TayanNo ratings yet

- 4 Hoi and RobinDocument7 pages4 Hoi and RobinelizabetaangelovaNo ratings yet

- Director Optimal Pay Against Fat Cats in Taiwan: and Finance Research Vol. 4, No. 3 2015Document9 pagesDirector Optimal Pay Against Fat Cats in Taiwan: and Finance Research Vol. 4, No. 3 2015peter weinNo ratings yet

- Dividend Policy As Strategic Tool of Financing in Public Firms: Evidence From NigeriaDocument24 pagesDividend Policy As Strategic Tool of Financing in Public Firms: Evidence From Nigeriay_378602342No ratings yet

- 08 Chapter 1 - Managerial RemunerationDocument26 pages08 Chapter 1 - Managerial RemunerationMbaStudent56No ratings yet

- Determinants of Dividend Payout Ratios: Evidence From United StatesDocument7 pagesDeterminants of Dividend Payout Ratios: Evidence From United StatesSri Wahyuningsih AhmadNo ratings yet

- Subba ReddyDocument47 pagesSubba Reddyankitjaipur0% (1)

- Chap 8 - Executive Compensation and IncentivesDocument19 pagesChap 8 - Executive Compensation and IncentivesHM.No ratings yet

- Journal of Accounting and Economics 7Document35 pagesJournal of Accounting and Economics 7Ovilia Intan DoniarNo ratings yet

- DGYoung Dentist PresentationDocument103 pagesDGYoung Dentist PresentationD.WorkuNo ratings yet

- Distributions To Shareholders: Dividends and Repurchases: Batangas State UniversityDocument41 pagesDistributions To Shareholders: Dividends and Repurchases: Batangas State UniversityNicole AnditNo ratings yet

- Chapter 17 - Earnings Per Share and Retained Earnings PDFDocument59 pagesChapter 17 - Earnings Per Share and Retained Earnings PDFDaniela MacaveiuNo ratings yet

- 6818-Article Text-13380-1-10-20210226Document7 pages6818-Article Text-13380-1-10-20210226maruzaks123No ratings yet

- International Review of Economics and FinanceDocument16 pagesInternational Review of Economics and FinanceAYUNo ratings yet

- Is The Dividend Puzzle Solved - RDocument9 pagesIs The Dividend Puzzle Solved - RUyen TranNo ratings yet

- Rvunc Department of Management: Mba Program Course Title: Financial and Managerial Accounting Course Code: Mbad612Document3 pagesRvunc Department of Management: Mba Program Course Title: Financial and Managerial Accounting Course Code: Mbad612markosNo ratings yet

- Dividend Policy: Saurty Shekyn Das (1310709) BSC (Hons) Finance (Minor: Law) Dfa2002Y (3) Corporate Finance 20 April 2015Document9 pagesDividend Policy: Saurty Shekyn Das (1310709) BSC (Hons) Finance (Minor: Law) Dfa2002Y (3) Corporate Finance 20 April 2015Anonymous H2L7lwBs3No ratings yet

- The Relationship Between Dividend Payout and Financial Performance: Evidence From Top40 JSE FirmsDocument15 pagesThe Relationship Between Dividend Payout and Financial Performance: Evidence From Top40 JSE FirmsLouise Barik- بريطانية مغربيةNo ratings yet

- Matolcsy 2010Document19 pagesMatolcsy 2010amirhayat15No ratings yet

- Pledge (And Hedge) Allegiance To The CompanyDocument6 pagesPledge (And Hedge) Allegiance To The CompanyBrian TayanNo ratings yet

- Cesari 2015Document17 pagesCesari 2015Nicoara AdrianNo ratings yet

- Advances Research DocumentDocument12 pagesAdvances Research DocumentParvez AliNo ratings yet

- Developing Performance Incentives and Sustaining Engagement in A Volatile EnvironmentDocument42 pagesDeveloping Performance Incentives and Sustaining Engagement in A Volatile EnvironmentPrathamesh ParkarNo ratings yet

- American Accounting Association The Accounting ReviewDocument22 pagesAmerican Accounting Association The Accounting ReviewFTU.CS2 Nguyễn Hồ DanhNo ratings yet

- Dividend Policy: Firm Has 2 ChoicesDocument18 pagesDividend Policy: Firm Has 2 ChoicesRajat LoyaNo ratings yet

- The Role of Employees in Corporate GovernanceDocument19 pagesThe Role of Employees in Corporate Governancemanish byanjankarNo ratings yet

- Corm 1Document38 pagesCorm 1MAYURIKANo ratings yet

- C30CY Week 8 LectureDocument50 pagesC30CY Week 8 Lecturejohnshabin123No ratings yet

- C2A October 2011 Exam PDFDocument8 pagesC2A October 2011 Exam PDFJeff GundyNo ratings yet

- Nnadi Et Tanna 2011 Multivariate Analyses of Factors Affecting Dividend Policy of AcquiredDocument20 pagesNnadi Et Tanna 2011 Multivariate Analyses of Factors Affecting Dividend Policy of AcquiredismailNo ratings yet

- The Determinants of Dividend Policy: Evidence From Malaysian FirmsDocument20 pagesThe Determinants of Dividend Policy: Evidence From Malaysian FirmsIzzatieNo ratings yet

- Corm 1Document38 pagesCorm 1MAYURIKANo ratings yet

- Impact of Firm Specific Variables On Dividend Payout of Nepalese BanksDocument13 pagesImpact of Firm Specific Variables On Dividend Payout of Nepalese BanksMani ManandharNo ratings yet

- Healy-The Effect of Bonus Schemes On Accounting DecisionsDocument23 pagesHealy-The Effect of Bonus Schemes On Accounting DecisionsarfanysNo ratings yet

- 12 - 8 - Determinants of Dividend Payout in Private Insurance Companies of Ethiopia - PDFDocument7 pages12 - 8 - Determinants of Dividend Payout in Private Insurance Companies of Ethiopia - PDFYohanisNo ratings yet

- Total Shareholders' ReturnDocument32 pagesTotal Shareholders' ReturnAmmi JulianNo ratings yet

- International Journal in Multidisciplinary and Academic Research (SSIJMAR) Vol. 3, No. 1, February-March - 2014 (ISSN 2278 - 5973)Document16 pagesInternational Journal in Multidisciplinary and Academic Research (SSIJMAR) Vol. 3, No. 1, February-March - 2014 (ISSN 2278 - 5973)Siva KalimuthuNo ratings yet

- Stakeholders 2Document25 pagesStakeholders 2Sebastián Posada100% (1)

- Chap 001Document17 pagesChap 001Raju_RNO EnggNo ratings yet

- DividendDocument30 pagesDividendFaruqNo ratings yet

- Stock Buyback 4Document15 pagesStock Buyback 4sethNo ratings yet

- Assignment 14Document7 pagesAssignment 14Satishkumar NagarajNo ratings yet

- Corporate Finance in 30 Minutes: A Guide For Directors and ShareholdersDocument14 pagesCorporate Finance in 30 Minutes: A Guide For Directors and ShareholdersMarcelo Vieira100% (1)

- The Relationship Between Dividend Payout and Financial Performance: Evidence From Top40 JSE FirmsDocument16 pagesThe Relationship Between Dividend Payout and Financial Performance: Evidence From Top40 JSE Firmsmaruzaks123No ratings yet

- Finance QuestionsDocument6 pagesFinance QuestionsCream FamilyNo ratings yet

- Pensions As A Form of Executive Compensation: L G Y LDocument35 pagesPensions As A Form of Executive Compensation: L G Y LFabiana SeverianoNo ratings yet

- The Macro Impact of Short-Termism15420-4Document45 pagesThe Macro Impact of Short-Termism15420-4dk773No ratings yet

- Assignment - VALIDITY OF THE LINTNER MODEL ON MAURITIAN CAPITAL MARKET PDFDocument25 pagesAssignment - VALIDITY OF THE LINTNER MODEL ON MAURITIAN CAPITAL MARKET PDFSamba BahNo ratings yet

- Dividend PolicyDocument8 pagesDividend PolicyHarsh SethiaNo ratings yet

- Presentation On: Compensation ManagementDocument29 pagesPresentation On: Compensation Managementarun_aglNo ratings yet

- Journal of Corporate Finance: Naoya Mori, Naoshi IkedaDocument10 pagesJournal of Corporate Finance: Naoya Mori, Naoshi IkedaZahra BatoolNo ratings yet

- Pay Perf Report 110812Document25 pagesPay Perf Report 110812brandon-harris-6868No ratings yet

- 7 Myths of Corporate GovernanceDocument10 pages7 Myths of Corporate GovernanceJawad UmarNo ratings yet

- Dividend Policy, Agency Costs, and Earned EquityDocument35 pagesDividend Policy, Agency Costs, and Earned EquityhhhhhhhNo ratings yet

- R&D Investments and Dividend Payout: Evidence Concerning The Semi-Mandatory Dividend Policy in ChinaDocument37 pagesR&D Investments and Dividend Payout: Evidence Concerning The Semi-Mandatory Dividend Policy in ChinadeviundipNo ratings yet

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveFrom EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNo ratings yet

- The Declaration of Dependence: Dividends in the Twenty-First CenturyFrom EverandThe Declaration of Dependence: Dividends in the Twenty-First CenturyNo ratings yet

- Outperform with Expectations-Based Management: A State-of-the-Art Approach to Creating and Enhancing Shareholder ValueFrom EverandOutperform with Expectations-Based Management: A State-of-the-Art Approach to Creating and Enhancing Shareholder ValueNo ratings yet

- Dividend Growth Investing: The Ultimate Investing Guide. Learn Effective Strategies to Create Passive Income for Your Future.From EverandDividend Growth Investing: The Ultimate Investing Guide. Learn Effective Strategies to Create Passive Income for Your Future.No ratings yet

- Bbi 2Document39 pagesBbi 2RESHMANo ratings yet

- Isda 2002 Master Agreement: Understanding The New Isda Documentation ConferenceDocument66 pagesIsda 2002 Master Agreement: Understanding The New Isda Documentation ConferencepapillonnnnNo ratings yet

- Corporate Governance (Baec0007) NewDocument46 pagesCorporate Governance (Baec0007) NewankitaaecsaxenaNo ratings yet

- Century Enka Limited: Analysis of Company's Financial StatementDocument24 pagesCentury Enka Limited: Analysis of Company's Financial StatementAnand PurohitNo ratings yet

- SM Prime Holdings Inc.: Integrated Annual Corporate Governance Report Analysis ReportDocument2 pagesSM Prime Holdings Inc.: Integrated Annual Corporate Governance Report Analysis Reportbelle crisNo ratings yet

- W1-Part 2-Additional-Ch 3-SaT-FIN 410Document7 pagesW1-Part 2-Additional-Ch 3-SaT-FIN 410Syed Aquib AbbasNo ratings yet

- Penerapan Sistem Pengendalian Internal Dengan CosoDocument17 pagesPenerapan Sistem Pengendalian Internal Dengan CosoFardian FardianNo ratings yet

- What Is Auditing ProcessDocument3 pagesWhat Is Auditing ProcessAizaButtNo ratings yet

- CJR English For BusinessDocument18 pagesCJR English For BusinessKristina SihombingNo ratings yet

- Various Committees On Corporate GovernanceDocument11 pagesVarious Committees On Corporate GovernanceFouzia imzNo ratings yet

- BAFI1018 International FinanceDocument109 pagesBAFI1018 International FinanceSteven NgNo ratings yet

- Lovello Annual Report 2021 22Document159 pagesLovello Annual Report 2021 22aribNo ratings yet

- Annual Report PT Pegadaian 2021Document536 pagesAnnual Report PT Pegadaian 2021bseptiyantoNo ratings yet

- Models of Corporate GovernanceDocument10 pagesModels of Corporate GovernanceNeil patrickNo ratings yet

- AccountabilityDocument15 pagesAccountabilityRavi SinghNo ratings yet

- Session 2. The COSO ERM Framework in DetailDocument18 pagesSession 2. The COSO ERM Framework in DetailManish AroraNo ratings yet

- Corporate Accounting Frauds 16112013Document27 pagesCorporate Accounting Frauds 16112013teammrauNo ratings yet

- Transportation 4-5-17Document39 pagesTransportation 4-5-17Punit Singh SardarNo ratings yet

- 7.1a Principal-Protected Notes: Trading Strategies Involving OptionsDocument14 pages7.1a Principal-Protected Notes: Trading Strategies Involving OptionsAnDy YiMNo ratings yet

- Agenda Item 1.4: IPSAS-IFRS Alignment Dashboard OverviewDocument23 pagesAgenda Item 1.4: IPSAS-IFRS Alignment Dashboard OverviewHadera TesfayNo ratings yet

- 20 ArrendamientosDocument87 pages20 ArrendamientosCarlos Eduardo LoveraNo ratings yet

- Code of Corporate Governance As Issued by Bangladesh Securities Exchange Commission in 2006 and Subsequent Modifications To Highlight Measures Aimed at Better Financial ManagementDocument4 pagesCode of Corporate Governance As Issued by Bangladesh Securities Exchange Commission in 2006 and Subsequent Modifications To Highlight Measures Aimed at Better Financial ManagementMahin KhanNo ratings yet

- Annual Report 2017-2018 PDFDocument90 pagesAnnual Report 2017-2018 PDFMuhmmad Sheikh AmanNo ratings yet

- Comparison Between HK Financial Reporting Standards and International Financial Reporting StandardsDocument29 pagesComparison Between HK Financial Reporting Standards and International Financial Reporting Standardsisaac2008100% (1)

- Takis Katsoulakos and Yannis KatsoulacosDocument15 pagesTakis Katsoulakos and Yannis KatsoulacosSebastianNo ratings yet

- Audit Committee, Internal Audit Function and Earnings Management: Evidence From JordanDocument19 pagesAudit Committee, Internal Audit Function and Earnings Management: Evidence From JordanNadeem TahaNo ratings yet

- KESC Annual-Report-2013Document197 pagesKESC Annual-Report-2013makhalidiNo ratings yet

- Bahan Metod 1Document7 pagesBahan Metod 1Gaura HarieNo ratings yet

- Naked OptionDocument3 pagesNaked OptionRayzwanRayzmanNo ratings yet