Download as pptx, pdf, or txt

You might also like

- Payment Systems: Dominique Rambure and Alec NacamuliDocument260 pagesPayment Systems: Dominique Rambure and Alec Nacamulimy name is hwat100% (2)

- Travel-Agency - Market StudyDocument32 pagesTravel-Agency - Market StudyJelly Anne50% (6)

- Oil Skimmer Project Report FinalDocument22 pagesOil Skimmer Project Report FinalGC C100% (1)

- Acca106 Midterms ExaminationDocument20 pagesAcca106 Midterms ExaminationNicole Anne Santiago SibuloNo ratings yet

- Human Resource Management Practices QuestionnaireDocument1 pageHuman Resource Management Practices QuestionnaireAravind RNo ratings yet

- Chapter 10Document22 pagesChapter 10Ryze100% (1)

- Joint Report On Corporate Practice of Dentistry in The Medicaid Program July 2013Document1,517 pagesJoint Report On Corporate Practice of Dentistry in The Medicaid Program July 2013Dentist The MenaceNo ratings yet

- Ias - 16 - PpeDocument25 pagesIas - 16 - PpeRMG Career Society BDNo ratings yet

- IAS 16 Property, Plant and EquipmentDocument18 pagesIAS 16 Property, Plant and EquipmentMuhammad Umar IqbalNo ratings yet

- Acca106 Midterm Exam 1st20212022 KeyDocument28 pagesAcca106 Midterm Exam 1st20212022 KeyNicole Anne Santiago SibuloNo ratings yet

- Quizzer #8 PPEDocument13 pagesQuizzer #8 PPEAseya CaloNo ratings yet

- Workbook-CH10-MCQ-Theory and PracticalDocument26 pagesWorkbook-CH10-MCQ-Theory and PracticalMaddy SyNo ratings yet

- 10a IAS 16Document30 pages10a IAS 16Ian chisema100% (1)

- Theories Intangible 3Document24 pagesTheories Intangible 3BLN-Hulo- Ronaldo M. Valdez SRNo ratings yet

- ACC107 P1 EXAM With Key AnswerDocument9 pagesACC107 P1 EXAM With Key AnswerRyan Malanum AbrioNo ratings yet

- Part D-8 Tangible Non Current Assests (ch06)Document68 pagesPart D-8 Tangible Non Current Assests (ch06)hyangNo ratings yet

- 7 - Property, Plant and Equipment and Related Accounts Theory of AccountsDocument15 pages7 - Property, Plant and Equipment and Related Accounts Theory of AccountsandreamrieNo ratings yet

- 22 - Intangible Assets - TheoryDocument3 pages22 - Intangible Assets - TheoryralphalonzoNo ratings yet

- IFA-I Chapter 5Document58 pagesIFA-I Chapter 5fikruhope533No ratings yet

- Intangible AssetsDocument4 pagesIntangible Assetsbrooke100% (1)

- Ias 16Document5 pagesIas 16Edga WariobaNo ratings yet

- Chapter 22 - Intangible AssetsDocument9 pagesChapter 22 - Intangible AssetsXiena100% (1)

- Pas 38 - Intangible AssetsDocument21 pagesPas 38 - Intangible AssetsMa. Franceska Loiz T. RiveraNo ratings yet

- Camilon Francisco PPEDocument21 pagesCamilon Francisco PPEGrace GamillaNo ratings yet

- I-Theories: Intangibles & Other AssetsDocument19 pagesI-Theories: Intangibles & Other Assetsaccounting filesNo ratings yet

- M2.5G Post-Test 5 - Ppe (Questionnaire)Document8 pagesM2.5G Post-Test 5 - Ppe (Questionnaire)soleilNo ratings yet

- Mayo Ining Ans Sa PrelimsDocument8 pagesMayo Ining Ans Sa PrelimsMary Rose DacuroNo ratings yet

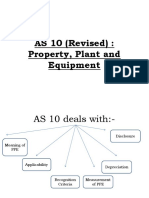

- AS 10 (Revised) : Property, Plant and EquipmentDocument34 pagesAS 10 (Revised) : Property, Plant and EquipmentAkshay PatilNo ratings yet

- BPS Midterm Exam KADocument5 pagesBPS Midterm Exam KASheena CalderonNo ratings yet

- Accounting Policies of Force Motors LTDDocument3 pagesAccounting Policies of Force Motors LTDNikhil GangwaniNo ratings yet

- F7.1 Chap 3 Tangible AssetDocument47 pagesF7.1 Chap 3 Tangible AssetTrang TranNo ratings yet

- Chapter 8 - Tangible Non-Current AssetsDocument23 pagesChapter 8 - Tangible Non-Current AssetsSyed Huzaifa SamiNo ratings yet

- 08 Fisher Account 5e v1 PPT ch08Document54 pages08 Fisher Account 5e v1 PPT ch08yuqi liuNo ratings yet

- Acco 4103 AP Reviewer Eval2 QaDocument7 pagesAcco 4103 AP Reviewer Eval2 QaJayrick James AriscoNo ratings yet

- Ind As 16Document57 pagesInd As 16Karthik Purohit100% (1)

- Property Plant and Equipment Practice SetDocument5 pagesProperty Plant and Equipment Practice SetpolxrixNo ratings yet

- Chapter 1 PPEDocument22 pagesChapter 1 PPEGirma NegashNo ratings yet

- 2022 06 DepreciationDocument46 pages2022 06 DepreciationSafi UllahNo ratings yet

- Pas 16 (Property, Plant and Equipment) : Names: Jon Rigo Caruz Hosea Earl CollongDocument22 pagesPas 16 (Property, Plant and Equipment) : Names: Jon Rigo Caruz Hosea Earl CollongKaren Mae Oculam CerinoNo ratings yet

- Ch8 HKAS16Document29 pagesCh8 HKAS16jaberalislamNo ratings yet

- Property Plant and EquipmentDocument10 pagesProperty Plant and EquipmentJhonrey BragaisNo ratings yet

- 01 Ias 16Document9 pages01 Ias 16salman jabbarNo ratings yet

- Intangibles PDFDocument5 pagesIntangibles PDFJer RamaNo ratings yet

- AnnMariaRenny PGP13032 JoanDocument2 pagesAnnMariaRenny PGP13032 JoanMayank BhattNo ratings yet

- SOP For Fixed Assets - FinalDocument7 pagesSOP For Fixed Assets - Finalwenhong.tan88No ratings yet

- Property Plant and EquipmentDocument10 pagesProperty Plant and Equipmentrt2222100% (1)

- Unit 2 PpeDocument82 pagesUnit 2 PpeHirut GetachewNo ratings yet

- Pre BoardDocument16 pagesPre BoardPatrick WaltersNo ratings yet

- 11 Intangible AssetsDocument16 pages11 Intangible AssetsGagandeep KaurNo ratings yet

- International Financial Reporting Standard IAS 16Document83 pagesInternational Financial Reporting Standard IAS 16tthanh020306No ratings yet

- Intacc 1 NotesDocument19 pagesIntacc 1 NotesLouiseNo ratings yet

- Ias 16Document46 pagesIas 16Gail BermudezNo ratings yet

- LQ5 AnswersDocument2 pagesLQ5 AnswersJohanna HamdanNo ratings yet

- Chapter 10 KDocument51 pagesChapter 10 KNhel AlvaroNo ratings yet

- اسئلة اقتصادية باللغة الانجليزيةDocument5 pagesاسئلة اقتصادية باللغة الانجليزيةMoun DirNo ratings yet

- Property, Plant and EquipmentDocument41 pagesProperty, Plant and EquipmentdaisyNo ratings yet

- Quiz Chapter-22 Intangible-AssetsDocument9 pagesQuiz Chapter-22 Intangible-Assetsjiachi.04212004No ratings yet

- (H) - 3rd Year - BCH 6.4 (DSE-4) - Sem-6 - Financial Reporting and Analysis - Week 4 - Himani DahiyaDocument19 pages(H) - 3rd Year - BCH 6.4 (DSE-4) - Sem-6 - Financial Reporting and Analysis - Week 4 - Himani DahiyaARGHYA MANDALNo ratings yet

- Lecture Notes On PPE - Acq & RecDocument6 pagesLecture Notes On PPE - Acq & Recjudel ArielNo ratings yet

- Leveraging on India: Best Practices Related to Manufacturing, Engineering, and ItFrom EverandLeveraging on India: Best Practices Related to Manufacturing, Engineering, and ItNo ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Supply Chain Management of HondaDocument25 pagesSupply Chain Management of HondaVaibhav Patel0% (1)

- Chapter One: Introduction To Marketing ResearchDocument35 pagesChapter One: Introduction To Marketing ResearchEmjae ColmenaresNo ratings yet

- CV K.Anbumani (Revised)Document6 pagesCV K.Anbumani (Revised)olimanikkamNo ratings yet

- Law On Partnerships and CorporationDocument113 pagesLaw On Partnerships and CorporationJessaNo ratings yet

- Credit and CollectionDocument21 pagesCredit and CollectionMara Pancho75% (4)

- Model Kontingensi & Model SituasionalDocument143 pagesModel Kontingensi & Model SituasionalNehto JhanNo ratings yet

- A Study On Customer Prefernces Towards Credit Cards in HDFC BankDocument40 pagesA Study On Customer Prefernces Towards Credit Cards in HDFC BankSharath100% (1)

- Armscor Official ReceiptsDocument6 pagesArmscor Official Receipts16michaelaganaNo ratings yet

- REPUBLIC ACT No. 9520Document74 pagesREPUBLIC ACT No. 9520CLARISSE ILAGANNo ratings yet

- Sea Risk Deloitte Ers Sap GRC ServicesDocument8 pagesSea Risk Deloitte Ers Sap GRC ServicesAllen WsyNo ratings yet

- Chris Aloysius Dmello 20200920Document13 pagesChris Aloysius Dmello 20200920partha sarathiNo ratings yet

- INTOSAI Internal Control StandardsDocument210 pagesINTOSAI Internal Control StandardsfriedricNo ratings yet

- Adidas Growth StrategiesDocument5 pagesAdidas Growth StrategiesbigbosssongnguNo ratings yet

- Activity 2.A: Illegal Use of ElectricityDocument26 pagesActivity 2.A: Illegal Use of ElectricityMark Lawrence BuenviajeNo ratings yet

- Application of IT in Our Daily Life PDFDocument26 pagesApplication of IT in Our Daily Life PDFjaweriaNo ratings yet

- Cost Leadership and DifferentiationDocument44 pagesCost Leadership and DifferentiationkevrysantosaNo ratings yet

- Chapter 3 - RevenueDocument4 pagesChapter 3 - RevenuejasonNo ratings yet

- Opentext™ Extended Ecm For Sap® Solutions Release NotesDocument82 pagesOpentext™ Extended Ecm For Sap® Solutions Release NotespeptaNo ratings yet

- Devops and MicroservicesDocument37 pagesDevops and Microservicesokello pablo100% (1)

- Financial ManagementDocument9 pagesFinancial ManagementMiconNo ratings yet

- Advanced - Collocations (Verbs and Nouns)Document5 pagesAdvanced - Collocations (Verbs and Nouns)Yabrud100% (1)

- Principles of Management-OpenStax-part 1Document402 pagesPrinciples of Management-OpenStax-part 1lt castro100% (1)

- OK Ainer Eries Ever Actuated Hassis Ount ON OLD ALL: FeaturesDocument2 pagesOK Ainer Eries Ever Actuated Hassis Ount ON OLD ALL: FeaturesirinaNo ratings yet

- Art of WarDocument3 pagesArt of WarAbby NavarroNo ratings yet

- Cheerinet Jul To OctDocument1 pageCheerinet Jul To OctNagaraj SNo ratings yet