Download as pptx, pdf, or txt

You might also like

- Auditing-Non Profit Entities and HospitalsDocument12 pagesAuditing-Non Profit Entities and HospitalsVirgie MartinezNo ratings yet

- Chap 1 - Tutorial QDocument3 pagesChap 1 - Tutorial QHanis ZahiraNo ratings yet

- Just For Feet, Inc.: CASE 1.3Document11 pagesJust For Feet, Inc.: CASE 1.3ffffffff dfdfdfNo ratings yet

- Controlling in Nursing ManagementDocument45 pagesControlling in Nursing Managementverna92% (37)

- Audit Program ITGCDocument40 pagesAudit Program ITGCJp CadenasNo ratings yet

- Chapter 7 Illustrative Solutions PDFDocument12 pagesChapter 7 Illustrative Solutions PDFNaeemNo ratings yet

- CHAPTER 8 - Internal Audit Tools and Techniques STDTDocument39 pagesCHAPTER 8 - Internal Audit Tools and Techniques STDTNor Syahra AjinimNo ratings yet

- CHAPTER 8 - Internal Audit Tools and Techniques 2019Document41 pagesCHAPTER 8 - Internal Audit Tools and Techniques 2019NORAZIAN HUSSINNo ratings yet

- Int Aud Chapter 8Document17 pagesInt Aud Chapter 8atiah zakariaNo ratings yet

- Information Technoloyg Management - Audit & ControlDocument159 pagesInformation Technoloyg Management - Audit & Controlhamza khan100% (1)

- 02 - AFA - PPT - Unit 5Document38 pages02 - AFA - PPT - Unit 5tfknrNo ratings yet

- Chapter 2.3 Audit, IAMDocument12 pagesChapter 2.3 Audit, IAMSam CurryNo ratings yet

- Chapter Four Information Technology and AuditingDocument78 pagesChapter Four Information Technology and Auditingabel habtamuNo ratings yet

- Internal Control and Is AuditDocument24 pagesInternal Control and Is AuditPinta Saras Puspita100% (1)

- Information Technology AuditDocument2 pagesInformation Technology AuditAsc RaihanNo ratings yet

- Chapter 4 Information Technology ItDocument63 pagesChapter 4 Information Technology It黄勇添No ratings yet

- Bit 2318 Information Systems Audit NotesDocument38 pagesBit 2318 Information Systems Audit NotestomNo ratings yet

- AUDCISE Unit 4 Lecture Notes 2022-2023Document32 pagesAUDCISE Unit 4 Lecture Notes 2022-2023Eijoj MaeNo ratings yet

- INFORMATIONS SYSTEMS AUDIT NOTES MucheluleDocument60 pagesINFORMATIONS SYSTEMS AUDIT NOTES MucheluleDHIVYA M SEC 2020No ratings yet

- 1.ISAUD - Information Technology Risk and Controls PDFDocument28 pages1.ISAUD - Information Technology Risk and Controls PDFRabbani AzizNo ratings yet

- Module 5 Part 2 Computer ControlsDocument77 pagesModule 5 Part 2 Computer Controlsarehonematodzi11No ratings yet

- Audit and Review Its Role in Information TechnologyDocument33 pagesAudit and Review Its Role in Information TechnologyTeddy Haryadi100% (1)

- Topic 10 - The Impact of IT On Audit ProcessDocument34 pagesTopic 10 - The Impact of IT On Audit Process2022930579No ratings yet

- Pertemuan 2 - Information System Risk and ControlDocument72 pagesPertemuan 2 - Information System Risk and ControlRey RaNo ratings yet

- Day 3 Uittenboogaard It Audit 1 The Hague 130515Document66 pagesDay 3 Uittenboogaard It Audit 1 The Hague 130515Aleksandar KNo ratings yet

- Update Intro To IT Audit Support v4Document41 pagesUpdate Intro To IT Audit Support v4Handayani Tri WijayantiNo ratings yet

- Pertemuan 3 - Sesi 5 Dan 6Document70 pagesPertemuan 3 - Sesi 5 Dan 6Sheila NajlaNo ratings yet

- Internal Control Over Financial Reporting: An IS Control PerspectiveDocument36 pagesInternal Control Over Financial Reporting: An IS Control PerspectiveCalebNo ratings yet

- M1 - Auditing in CIS EnvironmentDocument29 pagesM1 - Auditing in CIS Environmentamorejoya143No ratings yet

- Audit Management 2015 PDFDocument9 pagesAudit Management 2015 PDFRoni YunisNo ratings yet

- Chapter 3Document4 pagesChapter 3sicelosmavusoNo ratings yet

- Information System Audit Process: by Dr. Selasi OcanseyDocument17 pagesInformation System Audit Process: by Dr. Selasi OcanseyHannett WoodNo ratings yet

- How To Do A General IT ContrDocument46 pagesHow To Do A General IT ContrNicolas Astudillo100% (2)

- Audit Planning and Risk Assessment in A ComputerizedDocument6 pagesAudit Planning and Risk Assessment in A Computerizedalexissosing.cpaNo ratings yet

- Nature of Computer AuditDocument39 pagesNature of Computer AuditKryss Clyde Tabligan0% (1)

- Sox GC Ac SpreadsheetcompressedDocument92 pagesSox GC Ac SpreadsheetcompressedSaugat BoseNo ratings yet

- INFORMATIONS SYSTEMS AUDIT NOTES MucheluleDocument59 pagesINFORMATIONS SYSTEMS AUDIT NOTES MuchelulevortebognuNo ratings yet

- Module VI - Business Application Software Audit - EmailDocument91 pagesModule VI - Business Application Software Audit - EmailJYOTSNANo ratings yet

- Chapter 20 IT Concepts and ControlsDocument10 pagesChapter 20 IT Concepts and ControlsJaalib MehmoodNo ratings yet

- CH 11Document63 pagesCH 11Sello MafantiriNo ratings yet

- System Control AudhitDocument5 pagesSystem Control Audhittabrej khanNo ratings yet

- Assignment 3 1Document46 pagesAssignment 3 1Dine CapuaNo ratings yet

- Information TechnologyDocument15 pagesInformation Technologyabebe kumelaNo ratings yet

- The Role of IT AuditDocument30 pagesThe Role of IT AuditTrifan_DumitruNo ratings yet

- 5 Session Five Information Technology AuditingDocument32 pages5 Session Five Information Technology AuditingISAACNo ratings yet

- IT InfrastructureDocument4 pagesIT InfrastructuresicelosmavusoNo ratings yet

- It AuditDocument15 pagesIt AuditaleeshatenetNo ratings yet

- Nota Audit PoliteknikDocument24 pagesNota Audit PoliteknikShiraz Ahmad100% (1)

- Section 302 Section 404: 1. Organizational Structure ControlDocument6 pagesSection 302 Section 404: 1. Organizational Structure Controlfathma azzahroNo ratings yet

- QG To IT Audit 9.1Document81 pagesQG To IT Audit 9.1Rhad EstoqueNo ratings yet

- Computer Assisted Audit Tools (CAAT)Document33 pagesComputer Assisted Audit Tools (CAAT)Irish Keith Sanchez100% (1)

- Chapter 7 QuizDocument3 pagesChapter 7 QuizFitri-ssiNo ratings yet

- Auditing in A Computer Systems (Cis)Document8 pagesAuditing in A Computer Systems (Cis)John David Alfred EndicoNo ratings yet

- Quick Guide To Auditing in An IT EnvironmentDocument8 pagesQuick Guide To Auditing in An IT EnvironmentKarlayaanNo ratings yet

- Computer AuditDocument8 pagesComputer AuditReycelyn BallesterosNo ratings yet

- Chapter 1 Introduction On Is AuditDocument5 pagesChapter 1 Introduction On Is AuditSteffany RoqueNo ratings yet

- Ais Chapter 12Document20 pagesAis Chapter 12Clarissa A. FababairNo ratings yet

- Binod Information Technology PresentationDocument3 pagesBinod Information Technology PresentationankitbhangadiyaNo ratings yet

- Accounting Information Systems: Dr. Hisham MadiDocument24 pagesAccounting Information Systems: Dr. Hisham MadiIrish Keith SanchezNo ratings yet

- Audit ToolsDocument24 pagesAudit ToolsIrish Keith SanchezNo ratings yet

- Topic ThirteenDocument37 pagesTopic ThirteenGordar BuberwaNo ratings yet

- CIS Modules 1-7 - GachalianDocument247 pagesCIS Modules 1-7 - GachalianKelly Brenda CruzNo ratings yet

- Tri Nguyen - Cyber Risk Management and AuditsDocument35 pagesTri Nguyen - Cyber Risk Management and Auditsstrawhat470No ratings yet

- Far660 Jan 2018 SolutionDocument7 pagesFar660 Jan 2018 SolutionHanis ZahiraNo ratings yet

- Chap 1 - Tutorial SDocument11 pagesChap 1 - Tutorial SHanis ZahiraNo ratings yet

- Far660 - July 2020 Set 1 SolutionDocument8 pagesFar660 - July 2020 Set 1 SolutionHanis ZahiraNo ratings yet

- Far660 - Special Feb 2020 SolutionDocument7 pagesFar660 - Special Feb 2020 SolutionHanis ZahiraNo ratings yet

- Far660 - Dec 2019 QuestionDocument5 pagesFar660 - Dec 2019 QuestionHanis ZahiraNo ratings yet

- Far660 - Special Feb 2020 QuestionDocument5 pagesFar660 - Special Feb 2020 QuestionHanis ZahiraNo ratings yet

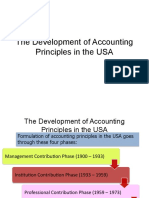

- Development of Accounting Principles in The UsaDocument6 pagesDevelopment of Accounting Principles in The UsaHanis ZahiraNo ratings yet

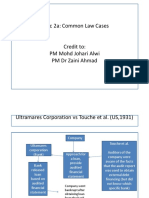

- TOPIC 2a 2 Common Law CasesDocument7 pagesTOPIC 2a 2 Common Law CasesHanis ZahiraNo ratings yet

- Topic 1 MIA by LawsDocument70 pagesTopic 1 MIA by LawsHanis ZahiraNo ratings yet

- TOPIC 2a 1 Auditor S Legal LiabilityDocument56 pagesTOPIC 2a 1 Auditor S Legal LiabilityHanis ZahiraNo ratings yet

- CHAPTER 5 Managing The Internal Audit FunctionDocument31 pagesCHAPTER 5 Managing The Internal Audit FunctionHanis ZahiraNo ratings yet

- CHAPTER 8 Investigation of FraudDocument45 pagesCHAPTER 8 Investigation of FraudHanis ZahiraNo ratings yet

- CHAPTER 6 Quality Assurance and Improvement ProgramDocument20 pagesCHAPTER 6 Quality Assurance and Improvement ProgramHanis ZahiraNo ratings yet

- CHAPTER 4 International Professional Practice Framework IPPFDocument14 pagesCHAPTER 4 International Professional Practice Framework IPPFHanis ZahiraNo ratings yet

- 02 Chapter 2 - Corporate Governance MechanismDocument19 pages02 Chapter 2 - Corporate Governance MechanismHanis ZahiraNo ratings yet

- CHAPTER 3 Risk and Control FazDocument22 pagesCHAPTER 3 Risk and Control FazHanis ZahiraNo ratings yet

- 01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceDocument30 pages01 CHAPTER - 2 - Internal - Auditing - and - Corporate - GovernanceHanis ZahiraNo ratings yet

- CHAPTER 1 Overview of Internal Auditing FazDocument22 pagesCHAPTER 1 Overview of Internal Auditing FazHanis ZahiraNo ratings yet

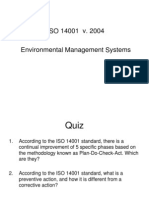

- Iso 14001Document61 pagesIso 14001kiranshingote100% (1)

- Auditing: Types of AuditDocument43 pagesAuditing: Types of Auditjohn paolo josonNo ratings yet

- Practice of Human Resource Accounting in Banking Sector of BangladeshDocument11 pagesPractice of Human Resource Accounting in Banking Sector of BangladeshSucheta SahaNo ratings yet

- IQA QuestionsDocument8 pagesIQA QuestionsProf C.S.PurushothamanNo ratings yet

- Accounting Information Systems Research Paper TopicsDocument6 pagesAccounting Information Systems Research Paper TopicsukldyebkfNo ratings yet

- 06 William R. Kinney Jr. - Issues in Accounting Research Design EducationDocument5 pages06 William R. Kinney Jr. - Issues in Accounting Research Design EducationFabian QuincheNo ratings yet

- PSA-720 (Revised) PDFDocument98 pagesPSA-720 (Revised) PDFehlayzaaNo ratings yet

- DuPont - STOPDocument40 pagesDuPont - STOPJana KusumaNo ratings yet

- Special Investigation Terms of ReferenceDocument3 pagesSpecial Investigation Terms of ReferenceKendra MangioneNo ratings yet

- Revenue Memorandum Order No. 20-2012: Bureau of Internal RevenueDocument6 pagesRevenue Memorandum Order No. 20-2012: Bureau of Internal RevenueGedan TanNo ratings yet

- 20J E1 Addendum 1Document3 pages20J E1 Addendum 1AshNo ratings yet

- Sar Spring15Document81 pagesSar Spring15Hariadi WidodoNo ratings yet

- Nuli 2022 IOP Conf. Ser. Earth Environ. Sci. 1086 012028Document9 pagesNuli 2022 IOP Conf. Ser. Earth Environ. Sci. 1086 012028BiniNo ratings yet

- 08 Project Quality ManagementDocument18 pages08 Project Quality ManagementChris GonzalesNo ratings yet

- 8 Draft Statutory Bank Branch Audit ReportDocument2 pages8 Draft Statutory Bank Branch Audit ReportCma Saurabh AroraNo ratings yet

- Icaew Cfab Asr 2019 SyllabusDocument12 pagesIcaew Cfab Asr 2019 SyllabusAnonymous ulFku1vNo ratings yet

- Fuentes Vs Sandiganbayn Case DigestDocument2 pagesFuentes Vs Sandiganbayn Case DigestsujeeNo ratings yet

- Privacy-Preserving Public Auditing For Secure Cloud Storage About The ProjectDocument10 pagesPrivacy-Preserving Public Auditing For Secure Cloud Storage About The Projectajesh_gmNo ratings yet

- Topic 1 - Code of EthicsDocument89 pagesTopic 1 - Code of EthicsMohd NuuranNo ratings yet

- July 2021 Interreg Checklist SCOs v1Document17 pagesJuly 2021 Interreg Checklist SCOs v1Alexandra BallaNo ratings yet

- Group 5 - Assignment 5Document40 pagesGroup 5 - Assignment 5Rhad Lester C. MaestradoNo ratings yet

- The Application of Benford's Law in Fraud Detection: A Systematic MethodologyDocument10 pagesThe Application of Benford's Law in Fraud Detection: A Systematic MethodologyAmr AwadNo ratings yet

- Bank Companies Act 1991Document21 pagesBank Companies Act 1991Subarna pal100% (1)

- ISO 39001 Lead Auditor - Four Page BrochureDocument4 pagesISO 39001 Lead Auditor - Four Page BrochurePECBCERTIFICATIONNo ratings yet

- DMGC, Maimpis, City of San Fernando, Pampanga Tel/Fax Nos.: (045) 455-2472 455-3208Document25 pagesDMGC, Maimpis, City of San Fernando, Pampanga Tel/Fax Nos.: (045) 455-2472 455-3208angelromNo ratings yet

- PFM Reform Strategy 2016-21 FinalDocument104 pagesPFM Reform Strategy 2016-21 FinalShafiqulHasanNo ratings yet

- SWIFT Joining Process: List of DocumentsDocument35 pagesSWIFT Joining Process: List of DocumentsJohn SamboNo ratings yet