Download as pptx, pdf, or txt

You might also like

- Managerial Eco1Document190 pagesManagerial Eco1ManojNo ratings yet

- Buying Power of Suppliers and BuyersDocument36 pagesBuying Power of Suppliers and BuyersIam JaiNo ratings yet

- Valuation 1Document36 pagesValuation 1aanchalchoubeyNo ratings yet

- Introduction To Business Administration EconomicsDocument26 pagesIntroduction To Business Administration EconomicsTrueMastaNo ratings yet

- Economic and Industry Analysis Co Combined 9-2010Document62 pagesEconomic and Industry Analysis Co Combined 9-2010Rohit BansalNo ratings yet

- MG Eco Chapter 1Document25 pagesMG Eco Chapter 1Fatima KhalidNo ratings yet

- Nature and Scope of Managerial EconomicsDocument19 pagesNature and Scope of Managerial EconomicsCasillar, Irish JoyNo ratings yet

- 01 Managerial EconomicsDocument24 pages01 Managerial EconomicsscribdwithyouNo ratings yet

- Lesson 01b, BB Managerial Econ & Goals of The FirmDocument68 pagesLesson 01b, BB Managerial Econ & Goals of The FirmAbdiweli mohamedNo ratings yet

- Iapm Unit 3 PDFDocument69 pagesIapm Unit 3 PDFHaripriya VNo ratings yet

- Managerial Economics (ME) - 2-3 Nature and Scope: Dr. Anil K KanungoDocument57 pagesManagerial Economics (ME) - 2-3 Nature and Scope: Dr. Anil K KanungoFiyanshu TambiNo ratings yet

- Unit 1Document101 pagesUnit 1atulkumar.rise1No ratings yet

- Theory of Firm - YKK - PPTDocument46 pagesTheory of Firm - YKK - PPTdivvyaapNo ratings yet

- Fundamental Analysis: DR Saif SiddiquiDocument32 pagesFundamental Analysis: DR Saif SiddiquiMohd Mudassir RahatNo ratings yet

- MEco. Module 1 Study MaterialDocument92 pagesMEco. Module 1 Study Material21MBA BARATH M.No ratings yet

- Business Economics: Sisdjiatmo K. WidhaningratDocument35 pagesBusiness Economics: Sisdjiatmo K. WidhaningratHisyam FarabiNo ratings yet

- Nature and Scope of Managerial EconomicsDocument70 pagesNature and Scope of Managerial Economicsnatalie clyde matesNo ratings yet

- Monti Maam Business EconomicsDocument193 pagesMonti Maam Business Economicssjst0709No ratings yet

- Fundamental AnalysisDocument32 pagesFundamental AnalysisfahreezNo ratings yet

- Risk Management Systems: © Marcus Mcinerney 1Document22 pagesRisk Management Systems: © Marcus Mcinerney 1Qi ZhuNo ratings yet

- Business Economics: Sisdjiatmo K. WidhaningratDocument35 pagesBusiness Economics: Sisdjiatmo K. Widhaningratneni bangunNo ratings yet

- Industry Analysis: What Is The Objectives of Performing Industry Analysis?Document25 pagesIndustry Analysis: What Is The Objectives of Performing Industry Analysis?UDIT GUPTANo ratings yet

- Introduction To Managerial EconomicsDocument15 pagesIntroduction To Managerial EconomicsMatthew Rogers100% (1)

- Basic Economic ProblemsDocument146 pagesBasic Economic ProblemsRichard DancelNo ratings yet

- ME-Unit 1Document16 pagesME-Unit 1Sanjana A 1910217No ratings yet

- Reporting On Financial Performance-UpdateDocument17 pagesReporting On Financial Performance-UpdateMD. AZMAL HOSSAINNo ratings yet

- Fundamental AnalysisDocument25 pagesFundamental AnalysissahadcptNo ratings yet

- Nature of Operation MGTDocument56 pagesNature of Operation MGTAhmed HonestNo ratings yet

- Introduction MBA I (13 15) FDocument17 pagesIntroduction MBA I (13 15) Fmanishkhandal88No ratings yet

- Objectives of Business Firm-FinalDocument43 pagesObjectives of Business Firm-FinalId Mohammad100% (3)

- Managerial Economics: Applications, Strategy, and Tactics, 10 EditionDocument18 pagesManagerial Economics: Applications, Strategy, and Tactics, 10 EditionMoshNo ratings yet

- Business Economics: Dr. Ashaq HussainDocument27 pagesBusiness Economics: Dr. Ashaq HussainMaanvi RockzzNo ratings yet

- Class 2 - Ratio AnalysisDocument36 pagesClass 2 - Ratio AnalysisShreyans JainNo ratings yet

- 3B - Chapter 4 - OperationsDocument78 pages3B - Chapter 4 - OperationsLit Jhun Yeang BenjaminNo ratings yet

- Nature and Scope of Managerial EconomicsDocument26 pagesNature and Scope of Managerial EconomicsPawan KumarNo ratings yet

- Business Environment Unit IDocument24 pagesBusiness Environment Unit ImanojNo ratings yet

- ECON Managerial AccountingDocument33 pagesECON Managerial AccountingmichellevngNo ratings yet

- Managerial Economics 1Document15 pagesManagerial Economics 1Manoj Kumar JoshiNo ratings yet

- Unit 3Document35 pagesUnit 3Barath LNo ratings yet

- Introduction To Business Administration: Economics (Managerial Economics, Part I)Document28 pagesIntroduction To Business Administration: Economics (Managerial Economics, Part I)Zohaib AhmedNo ratings yet

- b3ca3da0-50aa-4e21-9ded-f39804d929b5Document35 pagesb3ca3da0-50aa-4e21-9ded-f39804d929b5Hanumanthappa NNo ratings yet

- Managerial Economics For ManagersDocument30 pagesManagerial Economics For ManagersGautam BindlishNo ratings yet

- SM-Overview of StrategyDocument21 pagesSM-Overview of Strategyandvp002No ratings yet

- Lecture Two - Goals, Constraints, CostsDocument30 pagesLecture Two - Goals, Constraints, CostsClive NyowanaNo ratings yet

- Chapter 01 Introduction To M and ADocument28 pagesChapter 01 Introduction To M and ASattagouda M PatilNo ratings yet

- Managerial Economics:: Theory, Applications, and CasesDocument50 pagesManagerial Economics:: Theory, Applications, and CasesAbeer ShamiNo ratings yet

- Chapter-Four 4. Security Analysis Fundamental and Technical AnalysisDocument23 pagesChapter-Four 4. Security Analysis Fundamental and Technical AnalysisTedros BelaynehNo ratings yet

- Lecture 4 - Security AnalysisDocument22 pagesLecture 4 - Security AnalysisKenneth Wen Xuan TiongNo ratings yet

- What Is Managerial Economics?Document24 pagesWhat Is Managerial Economics?ChandanMatoliaNo ratings yet

- Earnings Management: Instructor: M.Jibran Sheikh E-Mail: Jibransheikh@comsats - Edu.pkDocument46 pagesEarnings Management: Instructor: M.Jibran Sheikh E-Mail: Jibransheikh@comsats - Edu.pkMah Zeb SyyedNo ratings yet

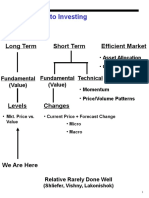

- Approaches To Investing: Long Term Short Term Efficient MarketDocument71 pagesApproaches To Investing: Long Term Short Term Efficient MarketPeter WarmeNo ratings yet

- MS-03 Economic and Social EnvironmentDocument33 pagesMS-03 Economic and Social EnvironmentMagdi NakhlaNo ratings yet

- Unit 1 Business EnvironmentDocument80 pagesUnit 1 Business EnvironmentEvangelineNo ratings yet

- Managerial Economics L1 IntroductionDocument43 pagesManagerial Economics L1 IntroductionRifat al haque DhruboNo ratings yet

- Chapter2 Managerial-Economics P1Document15 pagesChapter2 Managerial-Economics P1Yve LuelleNo ratings yet

- Distress AnalysisDocument18 pagesDistress AnalysisManvinder SinghNo ratings yet

- Introduction To Accounting and Business Decision Making: ©2020 John Wiley & Sons Australia LTDDocument44 pagesIntroduction To Accounting and Business Decision Making: ©2020 John Wiley & Sons Australia LTDHasan FiqihNo ratings yet

- ACCT1116 Chapter 1 Instructor SlidesDocument49 pagesACCT1116 Chapter 1 Instructor Slidesmikewithers41No ratings yet

- IntroductionDocument1 pageIntroductionVishala GudageriNo ratings yet

- 2 Report NiruDocument33 pages2 Report NiruVishala GudageriNo ratings yet

- College CertificateDocument1 pageCollege CertificateVishala GudageriNo ratings yet

- First PageDocument1 pageFirst PageVishala GudageriNo ratings yet

- ACKNOWDLEGEMENTDocument1 pageACKNOWDLEGEMENTVishala GudageriNo ratings yet

- IntershipDocument9 pagesIntershipVishala GudageriNo ratings yet

- Declaration SIPDocument1 pageDeclaration SIPVishala GudageriNo ratings yet

- Document 1Document7 pagesDocument 1Vishala GudageriNo ratings yet

- School Management of Studies and ResearchDocument6 pagesSchool Management of Studies and ResearchVishala GudageriNo ratings yet

- 5TH (1) MaheshDocument1 page5TH (1) MaheshVishala GudageriNo ratings yet

- Tableau ReportDocument4 pagesTableau ReportVishala GudageriNo ratings yet

- Direct TaxsationDocument8 pagesDirect TaxsationVishala GudageriNo ratings yet

- M3-Exiting The VentureDocument14 pagesM3-Exiting The VentureVishala GudageriNo ratings yet

- Report 2Document20 pagesReport 2Vishala GudageriNo ratings yet

- Commencement SpeechesDocument3 pagesCommencement SpeechesVishala GudageriNo ratings yet

- ReportDocument12 pagesReportVishala GudageriNo ratings yet

- Differences Between Industrial BuyersDocument2 pagesDifferences Between Industrial BuyersVishala GudageriNo ratings yet

- Batch - 3 Policies in IndiaDocument51 pagesBatch - 3 Policies in IndiaVishala GudageriNo ratings yet

- VishalaDocument5 pagesVishalaVishala GudageriNo ratings yet

- Job Evaluation and SatisfactionDocument6 pagesJob Evaluation and SatisfactionVishala GudageriNo ratings yet

- Kle Techonological UniversityDocument7 pagesKle Techonological UniversityVishala GudageriNo ratings yet

- KIRANYADocument1 pageKIRANYAVishala GudageriNo ratings yet

- History - Planning Commission: Set Up by A Resolution of The Govt. of India in March 1950. ObjectiveDocument23 pagesHistory - Planning Commission: Set Up by A Resolution of The Govt. of India in March 1950. ObjectiveVishala GudageriNo ratings yet

- HR Policies in IndiaDocument5 pagesHR Policies in IndiaVishala GudageriNo ratings yet

- CSR IndiaDocument11 pagesCSR IndiaVishala GudageriNo ratings yet

- Absolute Advantage Theory 1Document39 pagesAbsolute Advantage Theory 1Vishala GudageriNo ratings yet

- Gratuity PolicyDocument2 pagesGratuity PolicyVishala GudageriNo ratings yet

- Employment Contract PolicyDocument2 pagesEmployment Contract PolicyVishala GudageriNo ratings yet