Download as pptx, pdf, or txt

You might also like

- Statement of AccountDocument2 pagesStatement of AccountSoumya Ranjan Mohanty Pupun100% (1)

- Philippine Accounting Standards 38 (Intangible Assets2)Document72 pagesPhilippine Accounting Standards 38 (Intangible Assets2)Princess Edreah NuñalNo ratings yet

- Ifrs Usgaap NotesDocument38 pagesIfrs Usgaap Notesaum_thai100% (1)

- Auditing and Assurance Chapter 14 MC QuestionsDocument9 pagesAuditing and Assurance Chapter 14 MC Questionsgilli1tr0% (1)

- Investment Property: By: Dr. Angeles A. de Guzman Dean, College of Business EducationDocument21 pagesInvestment Property: By: Dr. Angeles A. de Guzman Dean, College of Business EducationJay-L TanNo ratings yet

- Accounting: For Investment PropertyDocument24 pagesAccounting: For Investment PropertyJay-L TanNo ratings yet

- Investment PropertyDocument19 pagesInvestment PropertyXyrille ReyesNo ratings yet

- IFA I ChapterDocument12 pagesIFA I Chapteryiberta69No ratings yet

- International Accounting Standard 16Document100 pagesInternational Accounting Standard 16ClarkMaasNo ratings yet

- Property Plant and Equipment PPEDocument30 pagesProperty Plant and Equipment PPEMarked BrassNo ratings yet

- Module 15 PAS 40Document5 pagesModule 15 PAS 40Jan JanNo ratings yet

- Section 16Document20 pagesSection 16Abata BageyuNo ratings yet

- IAS 40 Investment Property: Lovely Joy B. AlarconDocument23 pagesIAS 40 Investment Property: Lovely Joy B. AlarconDebbie Grace Latiban LinazaNo ratings yet

- CFAS PAS 40 Q and ADocument2 pagesCFAS PAS 40 Q and AJoseph Andrei BunadoNo ratings yet

- Section 17Document33 pagesSection 17Abata BageyuNo ratings yet

- Borrowing Cost LMSDocument16 pagesBorrowing Cost LMSCyrelle MagpantayNo ratings yet

- Property, Plant & EquipmentDocument26 pagesProperty, Plant & EquipmentRosalie E. BalhagNo ratings yet

- Chapter 7: Ppe and Intangibles: 1. Types of Non-Current AssetsDocument14 pagesChapter 7: Ppe and Intangibles: 1. Types of Non-Current AssetsMarine De CocquéauNo ratings yet

- Session 1 Introduction - Investment ApproachDocument18 pagesSession 1 Introduction - Investment ApproachPratik PatilNo ratings yet

- All SlidesDocument31 pagesAll SlidessinginiwizNo ratings yet

- Investment PropertyDocument31 pagesInvestment PropertyHanh CaoNo ratings yet

- Corporate Financial Accounting SLE Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 IND AS 40 Investment PropertyDocument12 pagesCorporate Financial Accounting SLE Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 IND AS 40 Investment PropertyDev ShahNo ratings yet

- Lkas 23Document20 pagesLkas 23Dhanushika Samarawickrama100% (1)

- 6902 PPT Materials For UploadDocument13 pages6902 PPT Materials For UploadAljur SalamedaNo ratings yet

- Financial Accounting and Reporting - Property, Plant and EquipmentDocument7 pagesFinancial Accounting and Reporting - Property, Plant and EquipmentLuisitoNo ratings yet

- B2 &C1 Ias 40 Investment PropertyDocument32 pagesB2 &C1 Ias 40 Investment Propertyabuumgweno1803No ratings yet

- KM Investment PropertyDocument4 pagesKM Investment Propertynikhilmandlecha6142No ratings yet

- Cfas Pas 40Document3 pagesCfas Pas 40Mich CandiaNo ratings yet

- IA2.102 Investment PropertyDocument10 pagesIA2.102 Investment PropertyPaul BandolaNo ratings yet

- Facilitators Guide For Accenture-IGNOU Diploma Program: Unit 4Document20 pagesFacilitators Guide For Accenture-IGNOU Diploma Program: Unit 4Vinay SinghNo ratings yet

- Investment PropertyDocument16 pagesInvestment PropertyDjunah ArellanoNo ratings yet

- 10 Week 10 CHPT 14n15 NCADocument47 pages10 Week 10 CHPT 14n15 NCA1621995944No ratings yet

- PAS IntangibleDocument21 pagesPAS IntangibleAngela WaganNo ratings yet

- Investment PropertyDocument26 pagesInvestment PropertyLovemore ChigwandaNo ratings yet

- Financial Management I: Session 3, 4 & 5Document26 pagesFinancial Management I: Session 3, 4 & 5Harshit MaheshwariNo ratings yet

- Accounting TerminologyDocument37 pagesAccounting Terminologyjhj01No ratings yet

- Module 3 Intangible AssetsDocument125 pagesModule 3 Intangible AssetsRIZLE SOGRADIELNo ratings yet

- Session 06 - Investment PropertyDocument15 pagesSession 06 - Investment PropertyVidarshaNo ratings yet

- International Accounting Standards: IAS 40 Investment PropertyDocument22 pagesInternational Accounting Standards: IAS 40 Investment PropertyPrudence MagaragadaNo ratings yet

- Real Estate Valuation)Document40 pagesReal Estate Valuation)shivpreetsandhuNo ratings yet

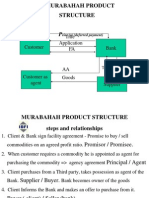

- Murabahah Product Structure: Title Application FADocument26 pagesMurabahah Product Structure: Title Application FAUmair UddinNo ratings yet

- Accounting II Week 4Document8 pagesAccounting II Week 4krushi.ntumunNo ratings yet

- Module 2 Investment Property and FundsDocument6 pagesModule 2 Investment Property and FundsCharice Anne VillamarinNo ratings yet

- Capital & RevenueDocument20 pagesCapital & Revenuebudsy.lambaNo ratings yet

- Property, Plant and EquipmentDocument44 pagesProperty, Plant and EquipmentAngela WaganNo ratings yet

- Capital Financing and AllocationDocument41 pagesCapital Financing and AllocationRhizhail MortallaNo ratings yet

- Accounting Notes: List of Current AssetsDocument3 pagesAccounting Notes: List of Current Assetsfooled chimeraNo ratings yet

- Non-Current AssetsDocument4 pagesNon-Current AssetsJenine BatiancilaNo ratings yet

- Accounting Standards AS - 1Document6 pagesAccounting Standards AS - 1chawlasrishtiNo ratings yet

- CTPM 2Document38 pagesCTPM 2abh ljknNo ratings yet

- MFRS 116 PPE - Part 1 NotesDocument24 pagesMFRS 116 PPE - Part 1 NotesWAN AMIRUL MUHAIMIN WAN ZUKAMALNo ratings yet

- Deductions To Gross IncomeDocument45 pagesDeductions To Gross IncomeKenzel lawasNo ratings yet

- Valuation LectureDocument24 pagesValuation LectureChiaraNo ratings yet

- Engineering Valuation Note 3Document23 pagesEngineering Valuation Note 3Daniel OlayinkaNo ratings yet

- PPEDocument5 pagesPPERodelia MalacastaNo ratings yet

- Gorakhpur Chapter 13052018Document37 pagesGorakhpur Chapter 13052018Sangita NataniNo ratings yet

- Lect 08TVDocument29 pagesLect 08TVsalman siddiquiNo ratings yet

- As 9Document27 pagesAs 9AATHARSH RADHAKRISHNANNo ratings yet

- Lecture Notes Iass 16 EtcDocument31 pagesLecture Notes Iass 16 Etcmayillahmansaray40No ratings yet

- C17 - MFRS 116 PpeDocument15 pagesC17 - MFRS 116 Ppe2022478048No ratings yet

- Benchmarking: Efficiency, and Financial Leverage in Achieving An ROE Figure. For Example, A FirmDocument8 pagesBenchmarking: Efficiency, and Financial Leverage in Achieving An ROE Figure. For Example, A FirmDavidHooNo ratings yet

- FBM-Module 9 Mgt. Information SystemDocument9 pagesFBM-Module 9 Mgt. Information SystemLeviNo ratings yet

- Coop LawDocument31 pagesCoop LawLeviNo ratings yet

- Agnes SlidesManiaDocument10 pagesAgnes SlidesManiaLeviNo ratings yet

- Development and Learning Mr. Juan JavierDocument9 pagesDevelopment and Learning Mr. Juan JavierLeviNo ratings yet

- Module 3 Performance MGT No Act4Document18 pagesModule 3 Performance MGT No Act4LeviNo ratings yet

- Repoprt On Loans & Advances PDFDocument66 pagesRepoprt On Loans & Advances PDFTitas Manower50% (4)

- RA 7653 and RA 11211Document43 pagesRA 7653 and RA 11211Ennavy YongkolNo ratings yet

- Boston Beer Co.Document8 pagesBoston Beer Co.ashimatayal100% (2)

- Finance ProcessesDocument8 pagesFinance ProcessesKushal SharmaNo ratings yet

- Dabur India LimitedDocument47 pagesDabur India Limiteddeegaur100% (2)

- VNO LetterDocument15 pagesVNO LetterZerohedgeNo ratings yet

- Powers & Authority of The Commissioner of Internal Revenue Under Sec. 4-7, Title 1 of The Tax CodeDocument24 pagesPowers & Authority of The Commissioner of Internal Revenue Under Sec. 4-7, Title 1 of The Tax CodeRovi PatinoNo ratings yet

- 18s ECO 341 Syllabus 9-1-17Document7 pages18s ECO 341 Syllabus 9-1-17Gabriel RoblesNo ratings yet

- Form GST RFD 01aDocument8 pagesForm GST RFD 01adizzi dagerNo ratings yet

- Questionnaire: Name .. Age . Gender OccupationDocument3 pagesQuestionnaire: Name .. Age . Gender OccupationAnonymous JLzXarNo ratings yet

- 004 - CAASSST07 - CH02 - Amndd Final BW+HS - RP2 - Sec - noPWDocument20 pages004 - CAASSST07 - CH02 - Amndd Final BW+HS - RP2 - Sec - noPWMahediNo ratings yet

- Chapter 2Document33 pagesChapter 2N KhNo ratings yet

- Nitesh Khandelwal (PGFC1921) - BOCA (Central Bank of India)Document12 pagesNitesh Khandelwal (PGFC1921) - BOCA (Central Bank of India)Surbhî GuptaNo ratings yet

- PER Guide To A Career in SecondariesDocument11 pagesPER Guide To A Career in SecondariesMarco ErmantazziNo ratings yet

- Analysis of Section 139 A IT Act 1961Document13 pagesAnalysis of Section 139 A IT Act 1961padam jainNo ratings yet

- Mock I AnswersDocument18 pagesMock I Answersasamy3010No ratings yet

- Chapter 12Document13 pagesChapter 12Abood Alissa100% (1)

- Government Accounting Rules, 1990 (2019-Edition) : Prepared by Deepak Kumar Rahi, AAO (LAD/Patna)Document16 pagesGovernment Accounting Rules, 1990 (2019-Edition) : Prepared by Deepak Kumar Rahi, AAO (LAD/Patna)ARAVIND K100% (2)

- Location of New Undertaking & Types of ActivityDocument46 pagesLocation of New Undertaking & Types of ActivityKanika KambojNo ratings yet

- Cash Flow From Assets - Solution PDFDocument3 pagesCash Flow From Assets - Solution PDFSeptian Sugestyo PutroNo ratings yet

- Sois (Bi) - 1 PDFDocument10 pagesSois (Bi) - 1 PDFSucipto Fasmita RaffaNo ratings yet

- General Risks: Corporate OfficeDocument154 pagesGeneral Risks: Corporate Officekirubaharan2022No ratings yet

- Module. Partnership AccountingDocument45 pagesModule. Partnership AccountingRonalie Alindugan100% (4)

- Preview of Chapter 10: Intermediate Accounting 17th Edition Kieso Weygandt WarfieldDocument24 pagesPreview of Chapter 10: Intermediate Accounting 17th Edition Kieso Weygandt WarfieldDavid Bradley BeckNo ratings yet

- Winston Shrout Explains BOE Based On Dishonor Amended Complaint AcceptanDocument39 pagesWinston Shrout Explains BOE Based On Dishonor Amended Complaint Acceptanbm100% (2)

- IIFL Internship ReportDocument33 pagesIIFL Internship ReportSURAJ TALEKAR100% (2)

- LIC STMTDocument1 pageLIC STMTEl Solo LoboNo ratings yet