Lecture 5 Shariah Stocks

Lecture 5 Shariah Stocks

You might also like

- Topic 2 - Concept of Shariah Compliance InvestmentDocument31 pagesTopic 2 - Concept of Shariah Compliance Investmenthidayatul raihanNo ratings yet

- Utilization of Plastic Wastes in The Production of Hollow BlocksDocument15 pagesUtilization of Plastic Wastes in The Production of Hollow BlocksVince BonosNo ratings yet

- 4bMFA3053 SharesDocument40 pages4bMFA3053 Sharesksenju47No ratings yet

- 7-Shariah Compliance StocksDocument35 pages7-Shariah Compliance StocksNurin HannaniNo ratings yet

- Islamic Capital MarketDocument21 pagesIslamic Capital MarketMasha Naizli MenhatNo ratings yet

- Gimlegal Company ProfileDocument21 pagesGimlegal Company Profilejoe musiwaNo ratings yet

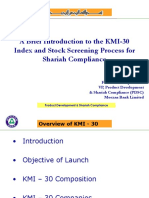

- A Brief Introduction To The KMI-30 Index and Stock Screening Process For Shariah ComplianceDocument12 pagesA Brief Introduction To The KMI-30 Index and Stock Screening Process For Shariah ComplianceAbdul RafayNo ratings yet

- Sec Reg - Carlson - Spring2011Document51 pagesSec Reg - Carlson - Spring2011Akansha SethiNo ratings yet

- Shariah Screening CriteriaDocument5 pagesShariah Screening CriteriaNoman KhanNo ratings yet

- Chapter 8 Non-IfIDocument25 pagesChapter 8 Non-IfIamirul hakimNo ratings yet

- Mutual Fund-PresentationDocument31 pagesMutual Fund-Presentationraju100% (12)

- Career Focus in FinanceDocument24 pagesCareer Focus in Financerbiswal57No ratings yet

- Intro Mon Pol - Oct 19 ABRDocument150 pagesIntro Mon Pol - Oct 19 ABRSoumya JainNo ratings yet

- Topic 2 - Revised Shariah Screening Methodology - CLASS - NOV2018)Document40 pagesTopic 2 - Revised Shariah Screening Methodology - CLASS - NOV2018)KiMi MooeNa100% (1)

- PSX According To Islamic ShariaDocument14 pagesPSX According To Islamic Shariaansary75No ratings yet

- Equity Securities MarketDocument23 pagesEquity Securities MarketILOVE MATURED FANSNo ratings yet

- Asset ManagementDocument12 pagesAsset ManagementSantosh JhawarNo ratings yet

- 001 FMI Mod1 Investment Industry V09!20!01 22 RTDocument69 pages001 FMI Mod1 Investment Industry V09!20!01 22 RTFumani ShipalanaNo ratings yet

- CHAPTER 1 FMDocument26 pagesCHAPTER 1 FMZati TyNo ratings yet

- Session 1 Introduction To Corporate FinanceDocument7 pagesSession 1 Introduction To Corporate FinanceAYUSHI SINGHNo ratings yet

- Islamic Investment Funds: A General IntroductionDocument26 pagesIslamic Investment Funds: A General Introductionafrican universityNo ratings yet

- 33 Introduction To M A - 5 Jun 2020Document37 pages33 Introduction To M A - 5 Jun 2020Bhavin SagarNo ratings yet

- S1 IntroDocument20 pagesS1 IntroMayank SinghNo ratings yet

- Regulation & Supervision of The Insurance Sector in IndiaDocument28 pagesRegulation & Supervision of The Insurance Sector in IndiaMohit NagotraNo ratings yet

- Project - Portfolio Management Services - Renu Maria XavierDocument11 pagesProject - Portfolio Management Services - Renu Maria XaviermegamegeshNo ratings yet

- 上海CMA新P2 5Document67 pages上海CMA新P2 5geng chenNo ratings yet

- Anisation of The Financial SystemDocument31 pagesAnisation of The Financial SystemNiharika SinghNo ratings yet

- Joint Venture & Acquisition: Incorporation of The Company The Shareholders' AgreementDocument56 pagesJoint Venture & Acquisition: Incorporation of The Company The Shareholders' AgreementSalil SheikhNo ratings yet

- Part 2 - Chapter 26 Saving, Investment, and The Financial SystemDocument20 pagesPart 2 - Chapter 26 Saving, Investment, and The Financial SystemCon CừuNo ratings yet

- Operations SampleDocument21 pagesOperations SampleAlexusPastranaNo ratings yet

- Shariah Compliant Risk ManagementDocument32 pagesShariah Compliant Risk ManagementUzair ZulkiflyNo ratings yet

- MBFS Unit 1Document48 pagesMBFS Unit 1pearlksrNo ratings yet

- Financial InstrumentsDocument70 pagesFinancial Instrumentsharesh swaminathanNo ratings yet

- Lesson+1 +Introduction+to+Financial+Management - FinalDocument33 pagesLesson+1 +Introduction+to+Financial+Management - Finalweird childNo ratings yet

- EmbarkingJoint VenturesJulyDocument27 pagesEmbarkingJoint VenturesJulyYashwant MisaleNo ratings yet

- Financial MarketsDocument30 pagesFinancial MarketsAshutosh SharmaNo ratings yet

- Original 1683521375 Equity SharesDocument40 pagesOriginal 1683521375 Equity SharesJaval ChoksiNo ratings yet

- Session - 01 Introduction: Fundamentals of Finance and Financial ManagementDocument48 pagesSession - 01 Introduction: Fundamentals of Finance and Financial ManagementSamantha Meril PandithaNo ratings yet

- Session - 01 Introduction: Fundamentals of Finance and Financial ManagementDocument48 pagesSession - 01 Introduction: Fundamentals of Finance and Financial ManagementSamantha Meril PandithaNo ratings yet

- Security Analysis and Portfolio Management: Rahul KumarDocument28 pagesSecurity Analysis and Portfolio Management: Rahul KumarDhruv MishraNo ratings yet

- Unit 2Document31 pagesUnit 2Vanshita MalviyaNo ratings yet

- Jaiib Module ADocument25 pagesJaiib Module Aeknath2000No ratings yet

- Session 1 - Introduction of Corporate FinanceDocument14 pagesSession 1 - Introduction of Corporate Financeluoyifei1988No ratings yet

- Asset Class-Securities & Financial AssetsDocument5 pagesAsset Class-Securities & Financial AssetsShivamNo ratings yet

- 2011 PPPCh8Document21 pages2011 PPPCh8BH Plus أخبار البحرينNo ratings yet

- Role of Regulators in Indian Market: Presented By:mohd HuzaifaDocument31 pagesRole of Regulators in Indian Market: Presented By:mohd HuzaifaMuhammed HuzaifaNo ratings yet

- Investment BankingDocument74 pagesInvestment Bankingjoecool9969No ratings yet

- Financial MarketsDocument30 pagesFinancial MarketsAshutosh SharmaNo ratings yet

- KUPres 7 Nov 2010Document63 pagesKUPres 7 Nov 2010Hasan Irfan SiddiquiNo ratings yet

- Slide 2-Lecture - Islamic Financial SystemDocument10 pagesSlide 2-Lecture - Islamic Financial Systemaiman azizNo ratings yet

- Shariah Screening Process in Islamic Capital Market DR MD Nurdin NgadimonDocument40 pagesShariah Screening Process in Islamic Capital Market DR MD Nurdin NgadimonGabriel Sim0% (1)

- M.osama NaseemDocument2 pagesM.osama NaseemMUHAMMAD AMMARNo ratings yet

- 28 Financial System and IPOsDocument30 pages28 Financial System and IPOsSINGH GITIKA JAINARAIN IPM 2019-24 BatchNo ratings yet

- Financial MarketsDocument26 pagesFinancial MarketsAshutosh SharmaNo ratings yet

- Chapter 3 Common Takeover Tactics and DefensesDocument25 pagesChapter 3 Common Takeover Tactics and DefensesK60 Phạm Thị Phương AnhNo ratings yet

- Intermediate Accounting: The Canadian Financial Reporting EnvironmentDocument35 pagesIntermediate Accounting: The Canadian Financial Reporting EnvironmentashleyalicerogersNo ratings yet

- Important Insurance Concepts (INS-21) Discussion - Part 1Document47 pagesImportant Insurance Concepts (INS-21) Discussion - Part 1Bhupinder SinghNo ratings yet

- 03 Success of Equity Funding Deal v2 11-07-2020 AJDocument42 pages03 Success of Equity Funding Deal v2 11-07-2020 AJarunjoshi12345No ratings yet

- Ipology: The Science of the Initial Public OfferingFrom EverandIpology: The Science of the Initial Public OfferingRating: 5 out of 5 stars5/5 (1)

- Wealth: How the World's High-Net-Worth Grow, Sustain, and Manage Their FortunesFrom EverandWealth: How the World's High-Net-Worth Grow, Sustain, and Manage Their FortunesRating: 1 out of 5 stars1/5 (1)

- Statistics Lecture 1Document53 pagesStatistics Lecture 1Abdulrahman SharifNo ratings yet

- Money Market 1Document48 pagesMoney Market 1Abdulrahman SharifNo ratings yet

- IIUM 2may17 V3Document22 pagesIIUM 2may17 V3Abdulrahman SharifNo ratings yet

- Airline Sukuk by Robert FugardDocument14 pagesAirline Sukuk by Robert FugardAbdulrahman SharifNo ratings yet

- Module 4 GE Elect 3Document25 pagesModule 4 GE Elect 3mallarialdrain03No ratings yet

- Full Report Ubs Group Ag Consolidated 2018 enDocument542 pagesFull Report Ubs Group Ag Consolidated 2018 enMAHINo ratings yet

- Schedule IagoDocument8 pagesSchedule IagoIago MartinsNo ratings yet

- Manufacturing ManagementDocument332 pagesManufacturing ManagementPugdug 209No ratings yet

- MasanDocument46 pagesMasanNgọc BíchNo ratings yet

- Mech Polytechnic Engineering-Industrial Engineering and Management Semester 6 Text BooksDocument205 pagesMech Polytechnic Engineering-Industrial Engineering and Management Semester 6 Text BooksBalasubramanyam PtrNo ratings yet

- 4009 Monticello CT Mrs Cindy Thaxton: Make Checks Payable To Og&EDocument1 page4009 Monticello CT Mrs Cindy Thaxton: Make Checks Payable To Og&EA Random GamerNo ratings yet

- Economics ISC 11Document2 pagesEconomics ISC 11Sriyaa SunkuNo ratings yet

- Ramky One Symphony Price SheetDocument2 pagesRamky One Symphony Price SheetkrishnaNo ratings yet

- BackFlush CostingDocument6 pagesBackFlush CostingEmmaNo ratings yet

- Effects of Inventory Control System-5076Document12 pagesEffects of Inventory Control System-5076Shekinah HinkertNo ratings yet

- Review of The Accounting CycleDocument35 pagesReview of The Accounting CycleKylene Edelle LeonardoNo ratings yet

- Group 3 Topic Potential Suppliers Inputs in Production 1Document16 pagesGroup 3 Topic Potential Suppliers Inputs in Production 1Angelo SorianoNo ratings yet

- JTD Group in Africa - Group 1Document9 pagesJTD Group in Africa - Group 1wipbanuaNo ratings yet

- Form 4 English Paper1 Ujian Pengesanan Sept2021Document16 pagesForm 4 English Paper1 Ujian Pengesanan Sept2021NAJWA ZAHIDAH BINTI RAZALI MoeNo ratings yet

- Statistique Du 01/03/2022 Au 31/03/2022: Matricule Type Controleur Date de Début Résultat Client Numéro de PVDocument23 pagesStatistique Du 01/03/2022 Au 31/03/2022: Matricule Type Controleur Date de Début Résultat Client Numéro de PVmbarek jariNo ratings yet

- Fabm2 q2 m3 Bank Reconciliation EditedDocument29 pagesFabm2 q2 m3 Bank Reconciliation EditedMaria anjilu VillanuevaNo ratings yet

- Clog On RedemptionDocument1 pageClog On RedemptionNikhilparakhNo ratings yet

- (Xi) 2023 Target Paper Eco, Poc, Acc & Bmaths by Sir IrfanDocument17 pages(Xi) 2023 Target Paper Eco, Poc, Acc & Bmaths by Sir IrfanMosa AbdullahNo ratings yet

- In The Strawberry Fields: by Eric SchfosserDocument20 pagesIn The Strawberry Fields: by Eric SchfosserOne PieceNo ratings yet

- Practical Examination Max. Marks: 30 Time: 1.0 HR: Agricultural Marketing and Price Analysis (AGECON-505)Document2 pagesPractical Examination Max. Marks: 30 Time: 1.0 HR: Agricultural Marketing and Price Analysis (AGECON-505)sumitNo ratings yet

- Alok IndustriesDocument61 pagesAlok IndustriesNeel DesaiNo ratings yet

- Market Analysis On Shoe Industry: BY Arun Kumar.K 1091004Document19 pagesMarket Analysis On Shoe Industry: BY Arun Kumar.K 1091004arunkumarkalimuthuNo ratings yet

- Fee ChallanDocument2 pagesFee Challanasad7241486No ratings yet

- Personal Loan Application Form: Salaried Self-EmployedDocument3 pagesPersonal Loan Application Form: Salaried Self-EmployedThee BouyyNo ratings yet

- AshewaDocument6 pagesAshewauniteddesyibel2018No ratings yet

- Financial Derivative AssignmentDocument14 pagesFinancial Derivative AssignmentSriSaraswathyNo ratings yet

- The City of Calgary 2020 Infrastructure Status Report - Early VersionDocument30 pagesThe City of Calgary 2020 Infrastructure Status Report - Early VersionAdam ToyNo ratings yet

- Report of Thorough ExaminationDocument2 pagesReport of Thorough ExaminationHasanagha Rasulzade100% (1)

Download as pptx, pdf, or txt

You might also like

- Topic 2 - Concept of Shariah Compliance InvestmentDocument31 pagesTopic 2 - Concept of Shariah Compliance Investmenthidayatul raihanNo ratings yet

- Utilization of Plastic Wastes in The Production of Hollow BlocksDocument15 pagesUtilization of Plastic Wastes in The Production of Hollow BlocksVince BonosNo ratings yet

- 4bMFA3053 SharesDocument40 pages4bMFA3053 Sharesksenju47No ratings yet

- 7-Shariah Compliance StocksDocument35 pages7-Shariah Compliance StocksNurin HannaniNo ratings yet

- Islamic Capital MarketDocument21 pagesIslamic Capital MarketMasha Naizli MenhatNo ratings yet

- Gimlegal Company ProfileDocument21 pagesGimlegal Company Profilejoe musiwaNo ratings yet

- A Brief Introduction To The KMI-30 Index and Stock Screening Process For Shariah ComplianceDocument12 pagesA Brief Introduction To The KMI-30 Index and Stock Screening Process For Shariah ComplianceAbdul RafayNo ratings yet

- Sec Reg - Carlson - Spring2011Document51 pagesSec Reg - Carlson - Spring2011Akansha SethiNo ratings yet

- Shariah Screening CriteriaDocument5 pagesShariah Screening CriteriaNoman KhanNo ratings yet

- Chapter 8 Non-IfIDocument25 pagesChapter 8 Non-IfIamirul hakimNo ratings yet

- Mutual Fund-PresentationDocument31 pagesMutual Fund-Presentationraju100% (12)

- Career Focus in FinanceDocument24 pagesCareer Focus in Financerbiswal57No ratings yet

- Intro Mon Pol - Oct 19 ABRDocument150 pagesIntro Mon Pol - Oct 19 ABRSoumya JainNo ratings yet

- Topic 2 - Revised Shariah Screening Methodology - CLASS - NOV2018)Document40 pagesTopic 2 - Revised Shariah Screening Methodology - CLASS - NOV2018)KiMi MooeNa100% (1)

- PSX According To Islamic ShariaDocument14 pagesPSX According To Islamic Shariaansary75No ratings yet

- Equity Securities MarketDocument23 pagesEquity Securities MarketILOVE MATURED FANSNo ratings yet

- Asset ManagementDocument12 pagesAsset ManagementSantosh JhawarNo ratings yet

- 001 FMI Mod1 Investment Industry V09!20!01 22 RTDocument69 pages001 FMI Mod1 Investment Industry V09!20!01 22 RTFumani ShipalanaNo ratings yet

- CHAPTER 1 FMDocument26 pagesCHAPTER 1 FMZati TyNo ratings yet

- Session 1 Introduction To Corporate FinanceDocument7 pagesSession 1 Introduction To Corporate FinanceAYUSHI SINGHNo ratings yet

- Islamic Investment Funds: A General IntroductionDocument26 pagesIslamic Investment Funds: A General Introductionafrican universityNo ratings yet

- 33 Introduction To M A - 5 Jun 2020Document37 pages33 Introduction To M A - 5 Jun 2020Bhavin SagarNo ratings yet

- S1 IntroDocument20 pagesS1 IntroMayank SinghNo ratings yet

- Regulation & Supervision of The Insurance Sector in IndiaDocument28 pagesRegulation & Supervision of The Insurance Sector in IndiaMohit NagotraNo ratings yet

- Project - Portfolio Management Services - Renu Maria XavierDocument11 pagesProject - Portfolio Management Services - Renu Maria XaviermegamegeshNo ratings yet

- 上海CMA新P2 5Document67 pages上海CMA新P2 5geng chenNo ratings yet

- Anisation of The Financial SystemDocument31 pagesAnisation of The Financial SystemNiharika SinghNo ratings yet

- Joint Venture & Acquisition: Incorporation of The Company The Shareholders' AgreementDocument56 pagesJoint Venture & Acquisition: Incorporation of The Company The Shareholders' AgreementSalil SheikhNo ratings yet

- Part 2 - Chapter 26 Saving, Investment, and The Financial SystemDocument20 pagesPart 2 - Chapter 26 Saving, Investment, and The Financial SystemCon CừuNo ratings yet

- Operations SampleDocument21 pagesOperations SampleAlexusPastranaNo ratings yet

- Shariah Compliant Risk ManagementDocument32 pagesShariah Compliant Risk ManagementUzair ZulkiflyNo ratings yet

- MBFS Unit 1Document48 pagesMBFS Unit 1pearlksrNo ratings yet

- Financial InstrumentsDocument70 pagesFinancial Instrumentsharesh swaminathanNo ratings yet

- Lesson+1 +Introduction+to+Financial+Management - FinalDocument33 pagesLesson+1 +Introduction+to+Financial+Management - Finalweird childNo ratings yet

- EmbarkingJoint VenturesJulyDocument27 pagesEmbarkingJoint VenturesJulyYashwant MisaleNo ratings yet

- Financial MarketsDocument30 pagesFinancial MarketsAshutosh SharmaNo ratings yet

- Original 1683521375 Equity SharesDocument40 pagesOriginal 1683521375 Equity SharesJaval ChoksiNo ratings yet

- Session - 01 Introduction: Fundamentals of Finance and Financial ManagementDocument48 pagesSession - 01 Introduction: Fundamentals of Finance and Financial ManagementSamantha Meril PandithaNo ratings yet

- Session - 01 Introduction: Fundamentals of Finance and Financial ManagementDocument48 pagesSession - 01 Introduction: Fundamentals of Finance and Financial ManagementSamantha Meril PandithaNo ratings yet

- Security Analysis and Portfolio Management: Rahul KumarDocument28 pagesSecurity Analysis and Portfolio Management: Rahul KumarDhruv MishraNo ratings yet

- Unit 2Document31 pagesUnit 2Vanshita MalviyaNo ratings yet

- Jaiib Module ADocument25 pagesJaiib Module Aeknath2000No ratings yet

- Session 1 - Introduction of Corporate FinanceDocument14 pagesSession 1 - Introduction of Corporate Financeluoyifei1988No ratings yet

- Asset Class-Securities & Financial AssetsDocument5 pagesAsset Class-Securities & Financial AssetsShivamNo ratings yet

- 2011 PPPCh8Document21 pages2011 PPPCh8BH Plus أخبار البحرينNo ratings yet

- Role of Regulators in Indian Market: Presented By:mohd HuzaifaDocument31 pagesRole of Regulators in Indian Market: Presented By:mohd HuzaifaMuhammed HuzaifaNo ratings yet

- Investment BankingDocument74 pagesInvestment Bankingjoecool9969No ratings yet

- Financial MarketsDocument30 pagesFinancial MarketsAshutosh SharmaNo ratings yet

- KUPres 7 Nov 2010Document63 pagesKUPres 7 Nov 2010Hasan Irfan SiddiquiNo ratings yet

- Slide 2-Lecture - Islamic Financial SystemDocument10 pagesSlide 2-Lecture - Islamic Financial Systemaiman azizNo ratings yet

- Shariah Screening Process in Islamic Capital Market DR MD Nurdin NgadimonDocument40 pagesShariah Screening Process in Islamic Capital Market DR MD Nurdin NgadimonGabriel Sim0% (1)

- M.osama NaseemDocument2 pagesM.osama NaseemMUHAMMAD AMMARNo ratings yet

- 28 Financial System and IPOsDocument30 pages28 Financial System and IPOsSINGH GITIKA JAINARAIN IPM 2019-24 BatchNo ratings yet

- Financial MarketsDocument26 pagesFinancial MarketsAshutosh SharmaNo ratings yet

- Chapter 3 Common Takeover Tactics and DefensesDocument25 pagesChapter 3 Common Takeover Tactics and DefensesK60 Phạm Thị Phương AnhNo ratings yet

- Intermediate Accounting: The Canadian Financial Reporting EnvironmentDocument35 pagesIntermediate Accounting: The Canadian Financial Reporting EnvironmentashleyalicerogersNo ratings yet

- Important Insurance Concepts (INS-21) Discussion - Part 1Document47 pagesImportant Insurance Concepts (INS-21) Discussion - Part 1Bhupinder SinghNo ratings yet

- 03 Success of Equity Funding Deal v2 11-07-2020 AJDocument42 pages03 Success of Equity Funding Deal v2 11-07-2020 AJarunjoshi12345No ratings yet

- Ipology: The Science of the Initial Public OfferingFrom EverandIpology: The Science of the Initial Public OfferingRating: 5 out of 5 stars5/5 (1)

- Wealth: How the World's High-Net-Worth Grow, Sustain, and Manage Their FortunesFrom EverandWealth: How the World's High-Net-Worth Grow, Sustain, and Manage Their FortunesRating: 1 out of 5 stars1/5 (1)

- Statistics Lecture 1Document53 pagesStatistics Lecture 1Abdulrahman SharifNo ratings yet

- Money Market 1Document48 pagesMoney Market 1Abdulrahman SharifNo ratings yet

- IIUM 2may17 V3Document22 pagesIIUM 2may17 V3Abdulrahman SharifNo ratings yet

- Airline Sukuk by Robert FugardDocument14 pagesAirline Sukuk by Robert FugardAbdulrahman SharifNo ratings yet

- Module 4 GE Elect 3Document25 pagesModule 4 GE Elect 3mallarialdrain03No ratings yet

- Full Report Ubs Group Ag Consolidated 2018 enDocument542 pagesFull Report Ubs Group Ag Consolidated 2018 enMAHINo ratings yet

- Schedule IagoDocument8 pagesSchedule IagoIago MartinsNo ratings yet

- Manufacturing ManagementDocument332 pagesManufacturing ManagementPugdug 209No ratings yet

- MasanDocument46 pagesMasanNgọc BíchNo ratings yet

- Mech Polytechnic Engineering-Industrial Engineering and Management Semester 6 Text BooksDocument205 pagesMech Polytechnic Engineering-Industrial Engineering and Management Semester 6 Text BooksBalasubramanyam PtrNo ratings yet

- 4009 Monticello CT Mrs Cindy Thaxton: Make Checks Payable To Og&EDocument1 page4009 Monticello CT Mrs Cindy Thaxton: Make Checks Payable To Og&EA Random GamerNo ratings yet

- Economics ISC 11Document2 pagesEconomics ISC 11Sriyaa SunkuNo ratings yet

- Ramky One Symphony Price SheetDocument2 pagesRamky One Symphony Price SheetkrishnaNo ratings yet

- BackFlush CostingDocument6 pagesBackFlush CostingEmmaNo ratings yet

- Effects of Inventory Control System-5076Document12 pagesEffects of Inventory Control System-5076Shekinah HinkertNo ratings yet

- Review of The Accounting CycleDocument35 pagesReview of The Accounting CycleKylene Edelle LeonardoNo ratings yet

- Group 3 Topic Potential Suppliers Inputs in Production 1Document16 pagesGroup 3 Topic Potential Suppliers Inputs in Production 1Angelo SorianoNo ratings yet

- JTD Group in Africa - Group 1Document9 pagesJTD Group in Africa - Group 1wipbanuaNo ratings yet

- Form 4 English Paper1 Ujian Pengesanan Sept2021Document16 pagesForm 4 English Paper1 Ujian Pengesanan Sept2021NAJWA ZAHIDAH BINTI RAZALI MoeNo ratings yet

- Statistique Du 01/03/2022 Au 31/03/2022: Matricule Type Controleur Date de Début Résultat Client Numéro de PVDocument23 pagesStatistique Du 01/03/2022 Au 31/03/2022: Matricule Type Controleur Date de Début Résultat Client Numéro de PVmbarek jariNo ratings yet

- Fabm2 q2 m3 Bank Reconciliation EditedDocument29 pagesFabm2 q2 m3 Bank Reconciliation EditedMaria anjilu VillanuevaNo ratings yet

- Clog On RedemptionDocument1 pageClog On RedemptionNikhilparakhNo ratings yet

- (Xi) 2023 Target Paper Eco, Poc, Acc & Bmaths by Sir IrfanDocument17 pages(Xi) 2023 Target Paper Eco, Poc, Acc & Bmaths by Sir IrfanMosa AbdullahNo ratings yet

- In The Strawberry Fields: by Eric SchfosserDocument20 pagesIn The Strawberry Fields: by Eric SchfosserOne PieceNo ratings yet

- Practical Examination Max. Marks: 30 Time: 1.0 HR: Agricultural Marketing and Price Analysis (AGECON-505)Document2 pagesPractical Examination Max. Marks: 30 Time: 1.0 HR: Agricultural Marketing and Price Analysis (AGECON-505)sumitNo ratings yet

- Alok IndustriesDocument61 pagesAlok IndustriesNeel DesaiNo ratings yet

- Market Analysis On Shoe Industry: BY Arun Kumar.K 1091004Document19 pagesMarket Analysis On Shoe Industry: BY Arun Kumar.K 1091004arunkumarkalimuthuNo ratings yet

- Fee ChallanDocument2 pagesFee Challanasad7241486No ratings yet

- Personal Loan Application Form: Salaried Self-EmployedDocument3 pagesPersonal Loan Application Form: Salaried Self-EmployedThee BouyyNo ratings yet

- AshewaDocument6 pagesAshewauniteddesyibel2018No ratings yet

- Financial Derivative AssignmentDocument14 pagesFinancial Derivative AssignmentSriSaraswathyNo ratings yet

- The City of Calgary 2020 Infrastructure Status Report - Early VersionDocument30 pagesThe City of Calgary 2020 Infrastructure Status Report - Early VersionAdam ToyNo ratings yet

- Report of Thorough ExaminationDocument2 pagesReport of Thorough ExaminationHasanagha Rasulzade100% (1)