Download as ppt, pdf, or txt

You might also like

- Mars - Wrigley Case Study - SolutionDocument8 pagesMars - Wrigley Case Study - SolutionSidhartha ModiNo ratings yet

- Business Studies Wiley and SonsDocument534 pagesBusiness Studies Wiley and SonsNate100% (1)

- Tugas 7: Akuntansi Sewa Guna UsahaDocument1 pageTugas 7: Akuntansi Sewa Guna UsahaZazan Zanuwar0% (1)

- Lease Vs Buying, BorrowingDocument3 pagesLease Vs Buying, BorrowingZohaib Hussain75% (4)

- OBM182-Chapter 4Document53 pagesOBM182-Chapter 4NURUL SYAZLEEN ABD MANAP100% (1)

- Standard Operating Procedure: Incase of Invoicing For A Vendor With Whom Agreement Is Already Done, ThenDocument2 pagesStandard Operating Procedure: Incase of Invoicing For A Vendor With Whom Agreement Is Already Done, ThenchandanNo ratings yet

- PP Chapter08Document23 pagesPP Chapter08Dahouk MasaraniNo ratings yet

- PP Chapter 8 EditedDocument31 pagesPP Chapter 8 EditedRáńéśh NeshNo ratings yet

- Mohammed Satheek Ali: ObjectiveDocument3 pagesMohammed Satheek Ali: ObjectiveReza LatNo ratings yet

- Session 9 - Accounting For Fixed AssetsDocument37 pagesSession 9 - Accounting For Fixed AssetsKashish Manish JariwalaNo ratings yet

- Automatic Packaging MachineDocument64 pagesAutomatic Packaging Machinesajid aliNo ratings yet

- CVL KRA Operating Instructions NewDocument19 pagesCVL KRA Operating Instructions NewPuru-the-braveNo ratings yet

- Job Description For KPMGDocument1 pageJob Description For KPMGDulcet LyricsNo ratings yet

- Safety Training PresentationsDocument31 pagesSafety Training PresentationsVirtual almostNo ratings yet

- AP Physics C Electricity and Magnetism Course at A GlanceDocument2 pagesAP Physics C Electricity and Magnetism Course at A GlanceJashanbir SinghNo ratings yet

- Difference Between Export Bill Collection and Export Bill Discounting.Document3 pagesDifference Between Export Bill Collection and Export Bill Discounting.lavanyakotaNo ratings yet

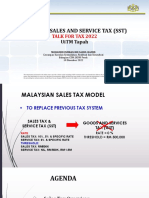

- UiTM SST Talk 2022 - SlidesDocument112 pagesUiTM SST Talk 2022 - SlidesNik Syarizal Nik MahadhirNo ratings yet

- New Lo1Document11 pagesNew Lo1hailu alemuNo ratings yet

- Sec Form 17-A Dec 2020Document92 pagesSec Form 17-A Dec 2020PaulNo ratings yet

- Cash Ops - CR Technical SpecificationDocument16 pagesCash Ops - CR Technical SpecificationKaustubh RaiNo ratings yet

- Garment ManufacturingDocument5 pagesGarment ManufacturingSADIA NAEEM100% (1)

- Income Tax Bba 5 Sem QuestionDocument18 pagesIncome Tax Bba 5 Sem QuestionArun GuptaNo ratings yet

- Job Description - Asistant Store KeeperDocument2 pagesJob Description - Asistant Store KeeperNoel NetteyNo ratings yet

- Receiving Alert Management V6 (ENHANCED Version) PDFDocument13 pagesReceiving Alert Management V6 (ENHANCED Version) PDFRx DentviewNo ratings yet

- Chimay-Mf1 FSM en Final 280219Document847 pagesChimay-Mf1 FSM en Final 280219Nikolaos MavridisNo ratings yet

- Retail Operations ManualDocument253 pagesRetail Operations ManualGF TeamNo ratings yet

- Judicial Officer Station Wise HRDocument68 pagesJudicial Officer Station Wise HRAAKASH BHATIANo ratings yet

- Parryware Toilet Seats PDFDocument53 pagesParryware Toilet Seats PDFSrinivas MVNo ratings yet

- Mitosis in Onion Root TipDocument12 pagesMitosis in Onion Root Tipsunil kumar guptaNo ratings yet

- Indian Public Finance Statistics 2017-18Document101 pagesIndian Public Finance Statistics 2017-18Priyansh ShrivastavNo ratings yet

- Configuring ProStream CAS ServicesDocument43 pagesConfiguring ProStream CAS ServicesRobertNo ratings yet

- CITI Bank Corporate Card Policy: PurposeDocument3 pagesCITI Bank Corporate Card Policy: PurposeAbhishek GuptaNo ratings yet

- Round Tripping - Indian Dilemma and International PerspectiveDocument8 pagesRound Tripping - Indian Dilemma and International PerspectiveINSTITUTE OF LEGAL EDUCATIONNo ratings yet

- Degree School/College/Institute Board/University CGPA/% YearDocument2 pagesDegree School/College/Institute Board/University CGPA/% YearAmit KumarNo ratings yet

- M01 Quality ManualDocument45 pagesM01 Quality Manualarpan shahNo ratings yet

- Baroda Salary Advantage Saving Account: Key BenefitsDocument2 pagesBaroda Salary Advantage Saving Account: Key Benefitsdynamic2004No ratings yet

- SBM Bank India LTD: Whistle Blower PolicyDocument14 pagesSBM Bank India LTD: Whistle Blower PolicyakoNo ratings yet

- HL Pni V1 NTR 3596132948944013913 NTR 7818877607244788448Document2 pagesHL Pni V1 NTR 3596132948944013913 NTR 7818877607244788448KanakaReddyKannaNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument9 pages© The Institute of Chartered Accountants of IndiaGao YungNo ratings yet

- IAF TC Minutes of Meeting and Decision PapersDocument46 pagesIAF TC Minutes of Meeting and Decision PapersArmand LiviuNo ratings yet

- CD06082018 KoDocument2 pagesCD06082018 KoAshwani KumarNo ratings yet

- HRMG (1021) Human Resource Management Unit-5 Separation and MaintenanceDocument22 pagesHRMG (1021) Human Resource Management Unit-5 Separation and Maintenancerakshit konchadaNo ratings yet

- Incab InspectionDocument2 pagesIncab InspectionDispatchNo ratings yet

- Sime Darby: AVP HandbookDocument49 pagesSime Darby: AVP HandbookPND TECHNOLOGY & SKILLS SOLUTIONS PND TECH & SKILLSNo ratings yet

- APN SettingsDocument24 pagesAPN Settingssyed nizam syed omarNo ratings yet

- Lub Catalog 1Document24 pagesLub Catalog 1Muhamad HamzahNo ratings yet

- MC - Reinsurance Market - 1694602900Document76 pagesMC - Reinsurance Market - 1694602900amin.touahriNo ratings yet

- 2023-04-10 OFR Preliminary ReportDocument10 pages2023-04-10 OFR Preliminary ReportMicah AllenNo ratings yet

- Chapter 19 - Introduction To Company AccountingDocument56 pagesChapter 19 - Introduction To Company AccountingK60 Triệu Thùy LinhNo ratings yet

- Internship ProjectDocument61 pagesInternship ProjectQuadri Consultancy ServicesNo ratings yet

- Iom Ylae-2Document32 pagesIom Ylae-2lam100% (1)

- 'Packing Credit Running Account' FacilityDocument2 pages'Packing Credit Running Account' FacilitykunalsukhdeveNo ratings yet

- UniStamp 2C-3SDocument2 pagesUniStamp 2C-3SSonia B100% (1)

- Terlotherm Delta Series: Scraped Surface Heat ExchangerDocument8 pagesTerlotherm Delta Series: Scraped Surface Heat ExchangerericNo ratings yet

- (@) Hydraulic Press Machine For Foundry RammingDocument34 pages(@) Hydraulic Press Machine For Foundry RammingKarthikeyan NNo ratings yet

- Prof. No.2 Project Profile On Cotton Ginning UnitDocument6 pagesProf. No.2 Project Profile On Cotton Ginning UnitssannyNo ratings yet

- 5-6. Overhauling of TGS & CGS JSA HADEED MODULE A-BDocument8 pages5-6. Overhauling of TGS & CGS JSA HADEED MODULE A-Bammar mughalNo ratings yet

- Working Instruction Farmaku - 20230621Document14 pagesWorking Instruction Farmaku - 20230621Muhammad ikhsan Rizki anandaNo ratings yet

- Agricultural Machinery OperDocument485 pagesAgricultural Machinery OperDenis Yasmin AlineNo ratings yet

- Store Management ProcedureDocument27 pagesStore Management ProcedureBhupendra LikhitkarNo ratings yet

- Let Export Copy: Indian Customs Edi SystemDocument5 pagesLet Export Copy: Indian Customs Edi SystemNishantNo ratings yet

- Gcse Ict: by The End of This Session, You Will Be Able ToDocument10 pagesGcse Ict: by The End of This Session, You Will Be Able ToSumathi SelvarajNo ratings yet

- II Sem BOIDocument36 pagesII Sem BOINeha ShuklaNo ratings yet

- You’Re a Business Owner, Not a Dummy!: Understand Your Merchant AccountFrom EverandYou’Re a Business Owner, Not a Dummy!: Understand Your Merchant AccountRating: 2 out of 5 stars2/5 (1)

- OBM182 Chapter 6Document45 pagesOBM182 Chapter 6NURUL SYAZLEEN ABD MANAPNo ratings yet

- OBM182-Chapter 4Document53 pagesOBM182-Chapter 4NURUL SYAZLEEN ABD MANAP100% (1)

- OBM182-Chapter 2Document21 pagesOBM182-Chapter 2NURUL SYAZLEEN ABD MANAPNo ratings yet

- OBM182-Chapter 5Document42 pagesOBM182-Chapter 5NURUL SYAZLEEN ABD MANAPNo ratings yet

- OBM182-Chapter 1Document52 pagesOBM182-Chapter 1NURUL SYAZLEEN ABD MANAPNo ratings yet

- Cis Rene NinžoDocument3 pagesCis Rene NinžoJean Leloup VreavloNo ratings yet

- Sahara PariwarDocument2 pagesSahara Pariwarfaria sobnom munaNo ratings yet

- National Income Accounting PPT MBADocument58 pagesNational Income Accounting PPT MBARhea Mae Caramonte AmitNo ratings yet

- 02 Quiz Bee p1 and Toa Average - Doc2Document2 pages02 Quiz Bee p1 and Toa Average - Doc2Shiela Belle PoppyNo ratings yet

- Probate Final Account Guide 06-2Document2 pagesProbate Final Account Guide 06-2GinaNo ratings yet

- 1.income Tax Declaration FY 2022-23Document49 pages1.income Tax Declaration FY 2022-23vasant ugaleNo ratings yet

- Financial Management June 2010 Marks PlanDocument7 pagesFinancial Management June 2010 Marks Plankarlr9No ratings yet

- Axis 2018-19Document348 pagesAxis 2018-19Drishti RohiraNo ratings yet

- SAP S - 4HANA Central Finance 1610 - Quick Tips (Summary) - LinkedInDocument4 pagesSAP S - 4HANA Central Finance 1610 - Quick Tips (Summary) - LinkedInjsphdvdNo ratings yet

- Capital Spending in Local Government: Providing Context Through The Lens of Government-Wide Financial StatementsDocument14 pagesCapital Spending in Local Government: Providing Context Through The Lens of Government-Wide Financial StatementsMahbub AlamNo ratings yet

- Elliott Management Corporation - Wikipe DiaDocument60 pagesElliott Management Corporation - Wikipe DiaEndhy Wisnu NovindraNo ratings yet

- Lecture 09 - Dual-Listed Company ArbitrageDocument32 pagesLecture 09 - Dual-Listed Company ArbitrageecondocsNo ratings yet

- CT5 PXS 11Document88 pagesCT5 PXS 11Yash Tiwari0% (1)

- Fraud and ErrorDocument6 pagesFraud and ErrorSel AtenionNo ratings yet

- Employee'S Provident Fund: Electronic Challan Cum Return (Ecr)Document3 pagesEmployee'S Provident Fund: Electronic Challan Cum Return (Ecr)Chandan Kumar YadavNo ratings yet

- Solution P6-2Document2 pagesSolution P6-2Frantino M Hutagaol100% (1)

- SyngeneDocument12 pagesSyngeneIndraneel MahantiNo ratings yet

- 10 Chapter 3Document42 pages10 Chapter 3SANJU8795No ratings yet

- Chapter 3 Banking and MGMT of Financial InsDocument8 pagesChapter 3 Banking and MGMT of Financial Insyared kebedeNo ratings yet

- 1 Annual Tanglaw Cup Case Study CompetitionDocument2 pages1 Annual Tanglaw Cup Case Study CompetitionDominic Dela VegaNo ratings yet

- Annexure 5BDocument3 pagesAnnexure 5BANUBHAV UPADHYAYNo ratings yet

- Cfap 2 2021 PKDocument288 pagesCfap 2 2021 PKMaham FatimaNo ratings yet

- ENGIMAN (Outline)Document15 pagesENGIMAN (Outline)Michelle PalconNo ratings yet

- Dutch-Bangla Bank Limited: Account StatementDocument1 pageDutch-Bangla Bank Limited: Account StatementPremaNo ratings yet

- Lecture NotesDocument12 pagesLecture NotesSabina Ioana AioneseiNo ratings yet

- BIR Form No. 0605Document1 pageBIR Form No. 0605Lorraine Steffany BanguisNo ratings yet