Download as pptx, pdf, or txt

You might also like

- Questionnaire - An Analysis On Investor Behaviour On Various Investment Avenues in IndiaDocument5 pagesQuestionnaire - An Analysis On Investor Behaviour On Various Investment Avenues in IndiaRakesh80% (51)

- Chapter 5 - Estimating Project Times - CostsDocument29 pagesChapter 5 - Estimating Project Times - CostsAizaz MalikNo ratings yet

- 5 Estimating Times and CostsDocument28 pages5 Estimating Times and CostsasdfaNo ratings yet

- 2021 - #5 Estimating Project Time and CostDocument22 pages2021 - #5 Estimating Project Time and Costghozi azmyNo ratings yet

- Estimating Project Times and Costs: Chapter FiveDocument25 pagesEstimating Project Times and Costs: Chapter FiveNoman CheemaNo ratings yet

- Estimating Project Times and Costs The Mcgraw-Hill Companies, Inc. All Rights Reserved. Mcgraw-Hill/IrwinDocument26 pagesEstimating Project Times and Costs The Mcgraw-Hill Companies, Inc. All Rights Reserved. Mcgraw-Hill/IrwinnanakethanNo ratings yet

- IT Project Management - ch02 by MarchewkaDocument41 pagesIT Project Management - ch02 by Marchewkapiyawat_siriNo ratings yet

- Organization Strategy and Project SelectionDocument40 pagesOrganization Strategy and Project Selectionkashifali3156No ratings yet

- Programme Management and Project EvaluationDocument44 pagesProgramme Management and Project EvaluationrashmiNo ratings yet

- Estimating Project: Times and CostsDocument15 pagesEstimating Project: Times and CostsM Umair ManiNo ratings yet

- Project Management: Estimating Project Times and CostsDocument64 pagesProject Management: Estimating Project Times and CostsRohan RoyNo ratings yet

- SC431 Lecture No.9 - Project Cost Estimating and BudgettingDocument30 pagesSC431 Lecture No.9 - Project Cost Estimating and BudgettingMemphis EmmaNo ratings yet

- Estimating Project Times and CostsDocument28 pagesEstimating Project Times and Costsan leNo ratings yet

- Project Evolution & Estimation:cash Flow Forecasting, Cost Benefit Evolution Techniques, Risk Evolution, Cost Benefit AnalysisDocument26 pagesProject Evolution & Estimation:cash Flow Forecasting, Cost Benefit Evolution Techniques, Risk Evolution, Cost Benefit AnalysisVaishalichoureyNo ratings yet

- Chapter 5Document29 pagesChapter 5janahh.omNo ratings yet

- Project Selection & Approval: Important Factors Selection Methods Value Analysis, OptimizationDocument38 pagesProject Selection & Approval: Important Factors Selection Methods Value Analysis, OptimizationKaikala Ram Charan TejNo ratings yet

- Estimates & Budget FinalDocument49 pagesEstimates & Budget FinalAnkita SharmaNo ratings yet

- APM811S - Estimating Project Times and CostsDocument28 pagesAPM811S - Estimating Project Times and CostskulanjiammalNo ratings yet

- Presentation 1Document45 pagesPresentation 1koky123456789No ratings yet

- Capital Budgeting Part 1Document12 pagesCapital Budgeting Part 1Ammar AsifNo ratings yet

- EMBA, Project Management, Monitoring and IsDocument41 pagesEMBA, Project Management, Monitoring and Isaron khanNo ratings yet

- Information Technology Project Management: by Denny Ganjar Purnama, MTI Universitas Pembangunan Jaya April 2014Document42 pagesInformation Technology Project Management: by Denny Ganjar Purnama, MTI Universitas Pembangunan Jaya April 2014asmaidin asmaidinNo ratings yet

- Lesson 4 - Value - Driven - Delivery - Part 1Document54 pagesLesson 4 - Value - Driven - Delivery - Part 1MAURICIO CARDOZONo ratings yet

- Project EvaluationDocument36 pagesProject EvaluationMazhar AbbasNo ratings yet

- Chapter 4Document24 pagesChapter 4Murre MoneyNo ratings yet

- Estimate ProjectDocument28 pagesEstimate ProjectNishita SinglaNo ratings yet

- Project (Capital Budgeting) and Production Management: by Prof. Ajay GhangareDocument35 pagesProject (Capital Budgeting) and Production Management: by Prof. Ajay GhangareajayghangareNo ratings yet

- Cost Management-V1Document18 pagesCost Management-V1Jide OyenekanNo ratings yet

- Lec 4Document19 pagesLec 4WEI JUN CHONGNo ratings yet

- Project Planning and FinanceDocument79 pagesProject Planning and FinanceajayghangareNo ratings yet

- CH 07Document41 pagesCH 07Mrk KhanNo ratings yet

- Steps in EvaluationDocument18 pagesSteps in EvaluationNivi SenthilNo ratings yet

- PMNotes Lecture4Document42 pagesPMNotes Lecture4Vishwajit NaikNo ratings yet

- Session (17-18) - Cost ManagementDocument48 pagesSession (17-18) - Cost ManagementAliNo ratings yet

- Measuring Project Wealth - 103406Document25 pagesMeasuring Project Wealth - 103406nicodionizrNo ratings yet

- Capital Budgeting Decisions: DR R.S. Aurora, Faculty in FinanceDocument31 pagesCapital Budgeting Decisions: DR R.S. Aurora, Faculty in FinanceAmit KumarNo ratings yet

- PM - Week N 06 - Cost Management 2022Document46 pagesPM - Week N 06 - Cost Management 2022Carlos ParedesNo ratings yet

- DEVELOPMENT APPRAISAL Rev 02Document25 pagesDEVELOPMENT APPRAISAL Rev 02sarcozy922No ratings yet

- Individuals & Project: - Each Citizen Should Play His Part in The Community According To His Individual GiftDocument28 pagesIndividuals & Project: - Each Citizen Should Play His Part in The Community According To His Individual GiftShrgeel HussainNo ratings yet

- MGT 105 Lydeal MsDocument15 pagesMGT 105 Lydeal MsLydeal MagtibayNo ratings yet

- PM 4Document40 pagesPM 4Ahmed SaeedNo ratings yet

- Capital BudgetingDocument34 pagesCapital BudgetingAryan Raj RajputNo ratings yet

- Chapter 5 - Estimating Project Times & CostsDocument27 pagesChapter 5 - Estimating Project Times & CostsJoyce Ann JuyoNo ratings yet

- Chapter 3Document29 pagesChapter 3S Varun SubramanyamNo ratings yet

- Project Integration MGTDocument45 pagesProject Integration MGTAhmad PadhilNo ratings yet

- Lec-7 - Estimation and Its TypesDocument33 pagesLec-7 - Estimation and Its TypesvsvsasasNo ratings yet

- Modul DURASI DAN BIAYA PROYEKDocument25 pagesModul DURASI DAN BIAYA PROYEKArie PrayogiNo ratings yet

- BUS4017 Lecture 9Document31 pagesBUS4017 Lecture 9bhawnaNo ratings yet

- Cost and Time EstimationDocument41 pagesCost and Time EstimationRaunak YadavNo ratings yet

- Chapter 3 - Project SelectionDocument15 pagesChapter 3 - Project SelectionFatin Nabihah100% (2)

- Chapter Learning - Project SelectionDocument5 pagesChapter Learning - Project SelectionKristen StewartNo ratings yet

- Lecture 1 CSRDocument31 pagesLecture 1 CSRPal QtaNo ratings yet

- GL8 e Chap 05 SDocument13 pagesGL8 e Chap 05 SNgoc Quyen NguyenNo ratings yet

- Project Cost Management: Week 8Document16 pagesProject Cost Management: Week 8Gullabudin Hassan ZadaNo ratings yet

- Estimation and Its TypesDocument34 pagesEstimation and Its TypestheNo ratings yet

- Earned Value: Valerie Colber, MBA, PMP, SCPMDocument26 pagesEarned Value: Valerie Colber, MBA, PMP, SCPMHedilberto Armando DelgadoNo ratings yet

- Estimating Project Times and Costs: Mcgraw-Hill/Irwin ReservedDocument23 pagesEstimating Project Times and Costs: Mcgraw-Hill/Irwin ReservedAbdullah TalibNo ratings yet

- Project EvaluationDocument88 pagesProject EvaluationOkothMagsNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Lesson 2Document45 pagesLesson 2Khánh HoàngNo ratings yet

- Lesson 4 - Project PlanningDocument24 pagesLesson 4 - Project PlanningKhánh HoàngNo ratings yet

- Lesson 3Document31 pagesLesson 3Khánh HoàngNo ratings yet

- An Ameloblastin C Terminus Variant Is Present in Human Adipose T 2018 HeliyoDocument17 pagesAn Ameloblastin C Terminus Variant Is Present in Human Adipose T 2018 HeliyoKhánh HoàngNo ratings yet

- An Insight Into The Emergence of Acinetobacter Baumannii As An Oro - 2018 - HelDocument18 pagesAn Insight Into The Emergence of Acinetobacter Baumannii As An Oro - 2018 - HelKhánh HoàngNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document14 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- 10 The History of Derivatives - A Few MilestonesDocument9 pages10 The History of Derivatives - A Few MilestonesmirceaNo ratings yet

- Fee Structure of The SchoolDocument2 pagesFee Structure of The Schoolramu292No ratings yet

- PMS02226310552 LoanApplicationDocument3 pagesPMS02226310552 LoanApplicationMrinal ChakravortyNo ratings yet

- 1,2. SessionDocument19 pages1,2. SessionAman SinghNo ratings yet

- PP Invt Sec 2019Document5 pagesPP Invt Sec 2019Revatee HurilNo ratings yet

- World Bank SME FinanceDocument8 pagesWorld Bank SME Financepaynow580No ratings yet

- BCom Banking and InsuranceDocument106 pagesBCom Banking and InsuranceUtsav SinhaNo ratings yet

- CitiBusiness CurrentAccount SOCDocument1 pageCitiBusiness CurrentAccount SOCbdhariwala48No ratings yet

- CHAPTER 11 Dividend PolicyDocument56 pagesCHAPTER 11 Dividend PolicyMatessa AnneNo ratings yet

- Suman Report Writing 1Document14 pagesSuman Report Writing 1ram binod yadavNo ratings yet

- Asset and The MeasurementsDocument32 pagesAsset and The MeasurementsIdha RahmaNo ratings yet

- Financial Management: Liquidity DecisionsDocument10 pagesFinancial Management: Liquidity Decisionsaryanboxer786No ratings yet

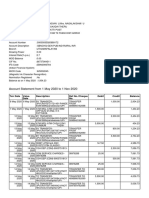

- Account Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument9 pagesAccount Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChellapandiNo ratings yet

- Analysis of Section 139 A IT Act 1961Document13 pagesAnalysis of Section 139 A IT Act 1961padam jainNo ratings yet

- Revenue From Contracts With Customers - IFRS 15Document5 pagesRevenue From Contracts With Customers - IFRS 15Joice BobosNo ratings yet

- 004 - Fiduciarie State For Morocco WhynantDocument5 pages004 - Fiduciarie State For Morocco Whynantlio MwaniaNo ratings yet

- Abhijit Murlidhar Gurav LHTNE00001290914 ENGDocument1 pageAbhijit Murlidhar Gurav LHTNE00001290914 ENGacc.managermarkNo ratings yet

- The Role of The Commercial and Development Banks in Nigeria As Recognised Under The LawDocument9 pagesThe Role of The Commercial and Development Banks in Nigeria As Recognised Under The LawSeedu ElijahNo ratings yet

- Finance Applications and Theory 4th Edition Cornett Test Bank 1Document23 pagesFinance Applications and Theory 4th Edition Cornett Test Bank 1harry100% (49)

- Questionnaire On Impact of GST On Construction Projects in Amravati RegionDocument8 pagesQuestionnaire On Impact of GST On Construction Projects in Amravati RegionKASHYAP TELMORE100% (2)

- Module 2Document41 pagesModule 2Sujata SarkarNo ratings yet

- Introduction To Financial AccountingDocument194 pagesIntroduction To Financial AccountingSrih BANo ratings yet

- Bank SecDocument93 pagesBank SecKrisha FayeNo ratings yet

- Analysis of Profit/Loss Account, Balance Sheet, Statement in Changes in Equity and Cash Flow Statement of Any Listed CompanyDocument25 pagesAnalysis of Profit/Loss Account, Balance Sheet, Statement in Changes in Equity and Cash Flow Statement of Any Listed CompanyMuhammad Hassaan AliNo ratings yet

- The Investment Environment: Bodie, Kane and MarcusDocument25 pagesThe Investment Environment: Bodie, Kane and Marcusvphuc1984No ratings yet

- Financial Market Instructional Material by Lascano CompressDocument72 pagesFinancial Market Instructional Material by Lascano CompressFiona MiralpesNo ratings yet

- Baba2 Fin MidtermDocument8 pagesBaba2 Fin MidtermYu BabylanNo ratings yet

- Inner Circle Trading DocumentDocument74 pagesInner Circle Trading DocumentDaniel Rosca Negrescu100% (2)