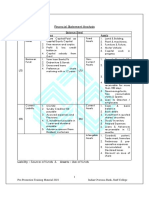

Balance Sheet - Ratio Analysis

Balance Sheet - Ratio Analysis

You might also like

- Kohler DCFDocument1 pageKohler DCFJennifer Langton100% (1)

- LBO Case Study - Volta Electronics Co. - v3Document14 pagesLBO Case Study - Volta Electronics Co. - v3madamaNo ratings yet

- Accounting For LawyersDocument51 pagesAccounting For Lawyersnamratha minupuri100% (2)

- Accounting Finals 1 ReviewerDocument5 pagesAccounting Finals 1 ReviewerlaurenNo ratings yet

- Assets Liabilities (Debt) & EquityDocument2 pagesAssets Liabilities (Debt) & Equitythe learners club5No ratings yet

- FinnanceDocument17 pagesFinnanceبكرة جاىNo ratings yet

- ACCOUNTING CYCLE STEP 1 TO 4 With IllustrationsDocument6 pagesACCOUNTING CYCLE STEP 1 TO 4 With IllustrationsmallarilecarNo ratings yet

- Fundamentals of AccountingDocument27 pagesFundamentals of AccountingMajariya Sahar SabladNo ratings yet

- Module 2 - Slides - Introducing Financial StatementsDocument12 pagesModule 2 - Slides - Introducing Financial StatementsElizabethNo ratings yet

- Pointers To Review: FABM 2: Recording Phase: Answer KeyDocument9 pagesPointers To Review: FABM 2: Recording Phase: Answer KeyMaria Janelle BlanzaNo ratings yet

- BS BasicsDocument2 pagesBS BasicsAbhinav AnandNo ratings yet

- Fabm 4THDocument3 pagesFabm 4THDrahneel MarasiganNo ratings yet

- Financial StatementsDocument27 pagesFinancial StatementsIrish Castillo100% (2)

- Format & ListDocument2 pagesFormat & ListJyotirmoy Chowdhury100% (1)

- 1 Statement of Financial Position - Part 1Document14 pages1 Statement of Financial Position - Part 1Johann LeoncitoNo ratings yet

- ACC406 - Chapter 3Document32 pagesACC406 - Chapter 3Carol Lesly100% (1)

- FABM2 ReviewerDocument7 pagesFABM2 ReviewerMakmak NoblezaNo ratings yet

- Accounting Simplified 1Document6 pagesAccounting Simplified 1kala1975No ratings yet

- Financial Statement Analysis: Balance Sheet Liabilities AssetsDocument17 pagesFinancial Statement Analysis: Balance Sheet Liabilities AssetsAman MujeebNo ratings yet

- ACC106 - Chapter 3Document30 pagesACC106 - Chapter 3Nealie100% (1)

- Entrep - Debit Credit JournalDocument47 pagesEntrep - Debit Credit JournalCampos, Kristine Joyce A.No ratings yet

- (En) DF FINANCIACIÓN TEMA 1 2021 - 2022Document76 pages(En) DF FINANCIACIÓN TEMA 1 2021 - 2022pau1976No ratings yet

- Statement of Financial Position ReviewerDocument2 pagesStatement of Financial Position ReviewerRyzaNo ratings yet

- FINC6021 - Financial StatementsDocument126 pagesFINC6021 - Financial Statements尹米勒No ratings yet

- Two-Date Bank Reconciliation Receivables: Example Format OnlyDocument2 pagesTwo-Date Bank Reconciliation Receivables: Example Format Onlymagic costaNo ratings yet

- Fin QuestionsDocument22 pagesFin Questionsvikki2point9No ratings yet

- Chapter 3-Accrual Accounting and The Balance SheetDocument2 pagesChapter 3-Accrual Accounting and The Balance SheetPriyanka KambleNo ratings yet

- Accounting PointsDocument4 pagesAccounting PointsLovely IñigoNo ratings yet

- Accounting at A GlanceDocument14 pagesAccounting at A GlanceNiyaz AhamedNo ratings yet

- EntrepreneurshipDocument3 pagesEntrepreneurshipXty CtyiuNo ratings yet

- Accounting NotesDocument6 pagesAccounting NotesD AngelaNo ratings yet

- Las 3Document8 pagesLas 3Venus Abarico Banque-AbenionNo ratings yet

- Accounting: Nature of Accounting Business OrganizationDocument2 pagesAccounting: Nature of Accounting Business OrganizationRochelle Joy CruzNo ratings yet

- Benefits of Global Accounting StandardsDocument16 pagesBenefits of Global Accounting StandardsJones EdombingoNo ratings yet

- Chapter 2Document27 pagesChapter 2Mohamad SyafiqNo ratings yet

- Chapter 2 Profit and Loss Account L1Document24 pagesChapter 2 Profit and Loss Account L1Sathya ManoharanNo ratings yet

- Current Vs Non-Current AssetsDocument3 pagesCurrent Vs Non-Current AssetsTrisha GarciaNo ratings yet

- Chapter 2 NLKTDocument58 pagesChapter 2 NLKTPhan Lê Anh Đào100% (1)

- 3 Ch2 - InvestmentCriteria - ForCampusDocument47 pages3 Ch2 - InvestmentCriteria - ForCampusrkswrt7t9dNo ratings yet

- Types of Accounts and The Account TitlesDocument25 pagesTypes of Accounts and The Account TitlesSeung BatumbakalNo ratings yet

- Financial Statements As A Management ToolDocument20 pagesFinancial Statements As A Management TooldavidimolaNo ratings yet

- FABM2 (1st)Document3 pagesFABM2 (1st)7xnc4st2g8No ratings yet

- Session 2Document27 pagesSession 2I don't knowNo ratings yet

- FABM Q3 M4 (Output No. 4 - Five Major Accounts)Document4 pagesFABM Q3 M4 (Output No. 4 - Five Major Accounts)Sophia MagdaraogNo ratings yet

- 20 IDM Recall 21feb24Document34 pages20 IDM Recall 21feb24ankitNo ratings yet

- Accounting Classification & Accounting EquationDocument25 pagesAccounting Classification & Accounting EquationMadadib 08No ratings yet

- Ratio Analysis: RatiosDocument18 pagesRatio Analysis: RatiosPhanishayan Kaniyar SampathNo ratings yet

- Financial Concepts 18 AprilDocument33 pagesFinancial Concepts 18 Aprilapi-295284877100% (1)

- Topic 2Document48 pagesTopic 2Marie JulienNo ratings yet

- Current Assets:: What Is The Statement of Financial PositionDocument4 pagesCurrent Assets:: What Is The Statement of Financial PositionEmar KimNo ratings yet

- Types of Major Accounts & Chart of AccountsDocument7 pagesTypes of Major Accounts & Chart of AccountsMary Gold Mosquera EsparteroNo ratings yet

- FabmDocument5 pagesFabmJihane TanogNo ratings yet

- Accounting Equation and TitlesDocument3 pagesAccounting Equation and TitlesErica Lalaine SalazarNo ratings yet

- Fabm 4THDocument3 pagesFabm 4THDrahneel MarasiganNo ratings yet

- (Total Expenses) (Treasury Shares at Cost-Ordinary) (Dividends)Document2 pages(Total Expenses) (Treasury Shares at Cost-Ordinary) (Dividends)lykajbmNo ratings yet

- 1 Balance SheeetDocument15 pages1 Balance SheeetAdnan RizviNo ratings yet

- Account ClassificationDocument3 pagesAccount ClassificationUsama MukhtarNo ratings yet

- Account Classification and Presentation: Account Title Classification Financial Statement A Normal BalanceDocument4 pagesAccount Classification and Presentation: Account Title Classification Financial Statement A Normal BalanceGurusamy KNo ratings yet

- ACC525 Week 1 AssignmentDocument3 pagesACC525 Week 1 AssignmentRung'Minoz KittiNo ratings yet

- Analysis of Balancesheet ItlDocument78 pagesAnalysis of Balancesheet Itlnational coursesNo ratings yet

- 3 FinalAccounts - AFB - Module CDocument23 pages3 FinalAccounts - AFB - Module Cwaste mailNo ratings yet

- Internal Control of Fixed Assets: A Controller and Auditor's GuideFrom EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideRating: 4 out of 5 stars4/5 (1)

- Aud ReconDocument8 pagesAud ReconShaine PacsonNo ratings yet

- Chapter 4Document50 pagesChapter 422GayeonNo ratings yet

- Basic Financial StatementsDocument44 pagesBasic Financial Statementsfikru terfaNo ratings yet

- Reading 25 Non-Current (Long-Term) LiabilitiesDocument18 pagesReading 25 Non-Current (Long-Term) LiabilitiesARPIT ARYANo ratings yet

- Capital Budgeting PDFDocument49 pagesCapital Budgeting PDFbaldoewszxcNo ratings yet

- Swaps Cms CMTDocument7 pagesSwaps Cms CMTmarketfolly.comNo ratings yet

- Chapter 25 - AnswerDocument10 pagesChapter 25 - AnswerReanne Claudine Laguna71% (7)

- Sibany Case StudyDocument3 pagesSibany Case StudyMattia AmbrosiniNo ratings yet

- Kosamattam Finance Limited Prospectus AprilDocument287 pagesKosamattam Finance Limited Prospectus Aprilmehtarahul999No ratings yet

- Ratio Problems 2Document7 pagesRatio Problems 2Vivek Mathi100% (1)

- Multiple Choice Questions & Answers: Banking LawDocument2 pagesMultiple Choice Questions & Answers: Banking LawArun Kumar TripathyNo ratings yet

- Chp2 - Bank Negara Malaysia and The Financial SystemDocument48 pagesChp2 - Bank Negara Malaysia and The Financial SystemRhazes Zy75% (8)

- Way2wealth Org Study Report 8 Nov 2022Document65 pagesWay2wealth Org Study Report 8 Nov 2022Manu DvNo ratings yet

- Transaction Dispute FormDocument1 pageTransaction Dispute FormashokjpNo ratings yet

- Up To 74+ KYC, 120+ KYT Data PointsDocument40 pagesUp To 74+ KYC, 120+ KYT Data PointsDanielNo ratings yet

- FM 1Document3 pagesFM 1anon-940489No ratings yet

- Afterpay Research PDFDocument33 pagesAfterpay Research PDFNikhil JoyNo ratings yet

- GR 10 Edwardsmaths Test or Assignment Finance and Growth T3 2022 MemoDocument4 pagesGR 10 Edwardsmaths Test or Assignment Finance and Growth T3 2022 MemomackersoapNo ratings yet

- Cipla Valuation ModelDocument17 pagesCipla Valuation ModelPuneet GirdharNo ratings yet

- Excel Fundamentals - Formulas For Finance (Template)Document7 pagesExcel Fundamentals - Formulas For Finance (Template)jitaNo ratings yet

- Test Bank For Macroeconomics 2nd Edition Full DownloadDocument48 pagesTest Bank For Macroeconomics 2nd Edition Full Downloadmichaelbirdgznspejbwa100% (22)

- CaiaDocument5 pagesCaiaRohan Haldankar0% (1)

- Volume Vs Open InterestDocument17 pagesVolume Vs Open InterestVivek AryaNo ratings yet

- Study Plan For JaiibDocument21 pagesStudy Plan For JaiibMahirNo ratings yet

- Dalio Ebook FINAL PDFDocument48 pagesDalio Ebook FINAL PDFvuhieptran100% (1)

- Launching An ICODocument8 pagesLaunching An ICOIdzwan RamliNo ratings yet

- Chapter 8 PDFDocument28 pagesChapter 8 PDFHarsh Sharma100% (1)

- Private Credit - Time To Consider Special Situations - (J.P. Morgan Asset Management)Document4 pagesPrivate Credit - Time To Consider Special Situations - (J.P. Morgan Asset Management)QuantDev-MNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Kohler DCFDocument1 pageKohler DCFJennifer Langton100% (1)

- LBO Case Study - Volta Electronics Co. - v3Document14 pagesLBO Case Study - Volta Electronics Co. - v3madamaNo ratings yet

- Accounting For LawyersDocument51 pagesAccounting For Lawyersnamratha minupuri100% (2)

- Accounting Finals 1 ReviewerDocument5 pagesAccounting Finals 1 ReviewerlaurenNo ratings yet

- Assets Liabilities (Debt) & EquityDocument2 pagesAssets Liabilities (Debt) & Equitythe learners club5No ratings yet

- FinnanceDocument17 pagesFinnanceبكرة جاىNo ratings yet

- ACCOUNTING CYCLE STEP 1 TO 4 With IllustrationsDocument6 pagesACCOUNTING CYCLE STEP 1 TO 4 With IllustrationsmallarilecarNo ratings yet

- Fundamentals of AccountingDocument27 pagesFundamentals of AccountingMajariya Sahar SabladNo ratings yet

- Module 2 - Slides - Introducing Financial StatementsDocument12 pagesModule 2 - Slides - Introducing Financial StatementsElizabethNo ratings yet

- Pointers To Review: FABM 2: Recording Phase: Answer KeyDocument9 pagesPointers To Review: FABM 2: Recording Phase: Answer KeyMaria Janelle BlanzaNo ratings yet

- BS BasicsDocument2 pagesBS BasicsAbhinav AnandNo ratings yet

- Fabm 4THDocument3 pagesFabm 4THDrahneel MarasiganNo ratings yet

- Financial StatementsDocument27 pagesFinancial StatementsIrish Castillo100% (2)

- Format & ListDocument2 pagesFormat & ListJyotirmoy Chowdhury100% (1)

- 1 Statement of Financial Position - Part 1Document14 pages1 Statement of Financial Position - Part 1Johann LeoncitoNo ratings yet

- ACC406 - Chapter 3Document32 pagesACC406 - Chapter 3Carol Lesly100% (1)

- FABM2 ReviewerDocument7 pagesFABM2 ReviewerMakmak NoblezaNo ratings yet

- Accounting Simplified 1Document6 pagesAccounting Simplified 1kala1975No ratings yet

- Financial Statement Analysis: Balance Sheet Liabilities AssetsDocument17 pagesFinancial Statement Analysis: Balance Sheet Liabilities AssetsAman MujeebNo ratings yet

- ACC106 - Chapter 3Document30 pagesACC106 - Chapter 3Nealie100% (1)

- Entrep - Debit Credit JournalDocument47 pagesEntrep - Debit Credit JournalCampos, Kristine Joyce A.No ratings yet

- (En) DF FINANCIACIÓN TEMA 1 2021 - 2022Document76 pages(En) DF FINANCIACIÓN TEMA 1 2021 - 2022pau1976No ratings yet

- Statement of Financial Position ReviewerDocument2 pagesStatement of Financial Position ReviewerRyzaNo ratings yet

- FINC6021 - Financial StatementsDocument126 pagesFINC6021 - Financial Statements尹米勒No ratings yet

- Two-Date Bank Reconciliation Receivables: Example Format OnlyDocument2 pagesTwo-Date Bank Reconciliation Receivables: Example Format Onlymagic costaNo ratings yet

- Fin QuestionsDocument22 pagesFin Questionsvikki2point9No ratings yet

- Chapter 3-Accrual Accounting and The Balance SheetDocument2 pagesChapter 3-Accrual Accounting and The Balance SheetPriyanka KambleNo ratings yet

- Accounting PointsDocument4 pagesAccounting PointsLovely IñigoNo ratings yet

- Accounting at A GlanceDocument14 pagesAccounting at A GlanceNiyaz AhamedNo ratings yet

- EntrepreneurshipDocument3 pagesEntrepreneurshipXty CtyiuNo ratings yet

- Accounting NotesDocument6 pagesAccounting NotesD AngelaNo ratings yet

- Las 3Document8 pagesLas 3Venus Abarico Banque-AbenionNo ratings yet

- Accounting: Nature of Accounting Business OrganizationDocument2 pagesAccounting: Nature of Accounting Business OrganizationRochelle Joy CruzNo ratings yet

- Benefits of Global Accounting StandardsDocument16 pagesBenefits of Global Accounting StandardsJones EdombingoNo ratings yet

- Chapter 2Document27 pagesChapter 2Mohamad SyafiqNo ratings yet

- Chapter 2 Profit and Loss Account L1Document24 pagesChapter 2 Profit and Loss Account L1Sathya ManoharanNo ratings yet

- Current Vs Non-Current AssetsDocument3 pagesCurrent Vs Non-Current AssetsTrisha GarciaNo ratings yet

- Chapter 2 NLKTDocument58 pagesChapter 2 NLKTPhan Lê Anh Đào100% (1)

- 3 Ch2 - InvestmentCriteria - ForCampusDocument47 pages3 Ch2 - InvestmentCriteria - ForCampusrkswrt7t9dNo ratings yet

- Types of Accounts and The Account TitlesDocument25 pagesTypes of Accounts and The Account TitlesSeung BatumbakalNo ratings yet

- Financial Statements As A Management ToolDocument20 pagesFinancial Statements As A Management TooldavidimolaNo ratings yet

- FABM2 (1st)Document3 pagesFABM2 (1st)7xnc4st2g8No ratings yet

- Session 2Document27 pagesSession 2I don't knowNo ratings yet

- FABM Q3 M4 (Output No. 4 - Five Major Accounts)Document4 pagesFABM Q3 M4 (Output No. 4 - Five Major Accounts)Sophia MagdaraogNo ratings yet

- 20 IDM Recall 21feb24Document34 pages20 IDM Recall 21feb24ankitNo ratings yet

- Accounting Classification & Accounting EquationDocument25 pagesAccounting Classification & Accounting EquationMadadib 08No ratings yet

- Ratio Analysis: RatiosDocument18 pagesRatio Analysis: RatiosPhanishayan Kaniyar SampathNo ratings yet

- Financial Concepts 18 AprilDocument33 pagesFinancial Concepts 18 Aprilapi-295284877100% (1)

- Topic 2Document48 pagesTopic 2Marie JulienNo ratings yet

- Current Assets:: What Is The Statement of Financial PositionDocument4 pagesCurrent Assets:: What Is The Statement of Financial PositionEmar KimNo ratings yet

- Types of Major Accounts & Chart of AccountsDocument7 pagesTypes of Major Accounts & Chart of AccountsMary Gold Mosquera EsparteroNo ratings yet

- FabmDocument5 pagesFabmJihane TanogNo ratings yet

- Accounting Equation and TitlesDocument3 pagesAccounting Equation and TitlesErica Lalaine SalazarNo ratings yet

- Fabm 4THDocument3 pagesFabm 4THDrahneel MarasiganNo ratings yet

- (Total Expenses) (Treasury Shares at Cost-Ordinary) (Dividends)Document2 pages(Total Expenses) (Treasury Shares at Cost-Ordinary) (Dividends)lykajbmNo ratings yet

- 1 Balance SheeetDocument15 pages1 Balance SheeetAdnan RizviNo ratings yet

- Account ClassificationDocument3 pagesAccount ClassificationUsama MukhtarNo ratings yet

- Account Classification and Presentation: Account Title Classification Financial Statement A Normal BalanceDocument4 pagesAccount Classification and Presentation: Account Title Classification Financial Statement A Normal BalanceGurusamy KNo ratings yet

- ACC525 Week 1 AssignmentDocument3 pagesACC525 Week 1 AssignmentRung'Minoz KittiNo ratings yet

- Analysis of Balancesheet ItlDocument78 pagesAnalysis of Balancesheet Itlnational coursesNo ratings yet

- 3 FinalAccounts - AFB - Module CDocument23 pages3 FinalAccounts - AFB - Module Cwaste mailNo ratings yet

- Internal Control of Fixed Assets: A Controller and Auditor's GuideFrom EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideRating: 4 out of 5 stars4/5 (1)

- Aud ReconDocument8 pagesAud ReconShaine PacsonNo ratings yet

- Chapter 4Document50 pagesChapter 422GayeonNo ratings yet

- Basic Financial StatementsDocument44 pagesBasic Financial Statementsfikru terfaNo ratings yet

- Reading 25 Non-Current (Long-Term) LiabilitiesDocument18 pagesReading 25 Non-Current (Long-Term) LiabilitiesARPIT ARYANo ratings yet

- Capital Budgeting PDFDocument49 pagesCapital Budgeting PDFbaldoewszxcNo ratings yet

- Swaps Cms CMTDocument7 pagesSwaps Cms CMTmarketfolly.comNo ratings yet

- Chapter 25 - AnswerDocument10 pagesChapter 25 - AnswerReanne Claudine Laguna71% (7)

- Sibany Case StudyDocument3 pagesSibany Case StudyMattia AmbrosiniNo ratings yet

- Kosamattam Finance Limited Prospectus AprilDocument287 pagesKosamattam Finance Limited Prospectus Aprilmehtarahul999No ratings yet

- Ratio Problems 2Document7 pagesRatio Problems 2Vivek Mathi100% (1)

- Multiple Choice Questions & Answers: Banking LawDocument2 pagesMultiple Choice Questions & Answers: Banking LawArun Kumar TripathyNo ratings yet

- Chp2 - Bank Negara Malaysia and The Financial SystemDocument48 pagesChp2 - Bank Negara Malaysia and The Financial SystemRhazes Zy75% (8)

- Way2wealth Org Study Report 8 Nov 2022Document65 pagesWay2wealth Org Study Report 8 Nov 2022Manu DvNo ratings yet

- Transaction Dispute FormDocument1 pageTransaction Dispute FormashokjpNo ratings yet

- Up To 74+ KYC, 120+ KYT Data PointsDocument40 pagesUp To 74+ KYC, 120+ KYT Data PointsDanielNo ratings yet

- FM 1Document3 pagesFM 1anon-940489No ratings yet

- Afterpay Research PDFDocument33 pagesAfterpay Research PDFNikhil JoyNo ratings yet

- GR 10 Edwardsmaths Test or Assignment Finance and Growth T3 2022 MemoDocument4 pagesGR 10 Edwardsmaths Test or Assignment Finance and Growth T3 2022 MemomackersoapNo ratings yet

- Cipla Valuation ModelDocument17 pagesCipla Valuation ModelPuneet GirdharNo ratings yet

- Excel Fundamentals - Formulas For Finance (Template)Document7 pagesExcel Fundamentals - Formulas For Finance (Template)jitaNo ratings yet

- Test Bank For Macroeconomics 2nd Edition Full DownloadDocument48 pagesTest Bank For Macroeconomics 2nd Edition Full Downloadmichaelbirdgznspejbwa100% (22)

- CaiaDocument5 pagesCaiaRohan Haldankar0% (1)

- Volume Vs Open InterestDocument17 pagesVolume Vs Open InterestVivek AryaNo ratings yet

- Study Plan For JaiibDocument21 pagesStudy Plan For JaiibMahirNo ratings yet

- Dalio Ebook FINAL PDFDocument48 pagesDalio Ebook FINAL PDFvuhieptran100% (1)

- Launching An ICODocument8 pagesLaunching An ICOIdzwan RamliNo ratings yet

- Chapter 8 PDFDocument28 pagesChapter 8 PDFHarsh Sharma100% (1)

- Private Credit - Time To Consider Special Situations - (J.P. Morgan Asset Management)Document4 pagesPrivate Credit - Time To Consider Special Situations - (J.P. Morgan Asset Management)QuantDev-MNo ratings yet