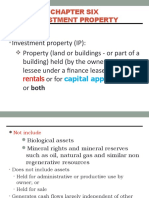

Property Revaluation

Property Revaluation

You might also like

- Airline Cabin Crew Training IATA Training Course PDFDocument3 pagesAirline Cabin Crew Training IATA Training Course PDFwin computer0% (1)

- Skittles Fractions Math Target Lesson PlanDocument8 pagesSkittles Fractions Math Target Lesson Planapi-396384317No ratings yet

- Audit of PpeDocument19 pagesAudit of PpeLiezel LaborteNo ratings yet

- ARTHUR - Early Greece: The Origins of The Western Attitude Towards WomenDocument53 pagesARTHUR - Early Greece: The Origins of The Western Attitude Towards WomenCamila BelelliNo ratings yet

- FR-Property Plant N Equipment PDFDocument60 pagesFR-Property Plant N Equipment PDFimrul kaishNo ratings yet

- International Accounting Standard 16Document100 pagesInternational Accounting Standard 16ClarkMaasNo ratings yet

- Ias 16Document39 pagesIas 16Asad KhanafzalNo ratings yet

- F7.1 Chap 3 Tangible AssetDocument47 pagesF7.1 Chap 3 Tangible AssetTrang TranNo ratings yet

- F-II ChapterTwoDocument59 pagesF-II ChapterTwoMohammed AbdulselamNo ratings yet

- Chapter 14 Investment Property StudentsDocument38 pagesChapter 14 Investment Property StudentsBình QuốcNo ratings yet

- PPE - FinalDocument71 pagesPPE - FinalKristen KooNo ratings yet

- Chapter 7 Investment PropertyDocument8 pagesChapter 7 Investment PropertyKrissa Mae Longos100% (2)

- Plant Property and Equipment On Merchandising BusinessDocument5 pagesPlant Property and Equipment On Merchandising BusinessarjohnyabutNo ratings yet

- Property, Plant and EquipmentDocument40 pagesProperty, Plant and EquipmentNatalie SerranoNo ratings yet

- IFA I ChapterDocument12 pagesIFA I Chapteryiberta69No ratings yet

- 9.2 IAS36 - Impairment of Assets 1Document41 pages9.2 IAS36 - Impairment of Assets 1Given RefilweNo ratings yet

- Chapter 9 Lecture NoteDocument47 pagesChapter 9 Lecture Note김가온No ratings yet

- Investment PropertyDocument31 pagesInvestment PropertyHanh CaoNo ratings yet

- Property, Plant and EquipmentDocument46 pagesProperty, Plant and EquipmentAATHARSH RADHAKRISHNANNo ratings yet

- Lecture # 31Document11 pagesLecture # 31HussainNo ratings yet

- Presentationprint TempDocument67 pagesPresentationprint TempMd EndrisNo ratings yet

- International Accounting Standards: IAS 40 Investment PropertyDocument22 pagesInternational Accounting Standards: IAS 40 Investment PropertyPrudence MagaragadaNo ratings yet

- Property, Plant and EquipmentDocument41 pagesProperty, Plant and EquipmentdaisyNo ratings yet

- Assets and Depreciation: October 18, 2018Document14 pagesAssets and Depreciation: October 18, 2018Hareem SattarNo ratings yet

- Corporate Financial Accounting SLE Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 IND AS 40 Investment PropertyDocument12 pagesCorporate Financial Accounting SLE Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 IND AS 40 Investment PropertyDev ShahNo ratings yet

- Property, Plant and EquipmentDocument66 pagesProperty, Plant and EquipmentThanos The titanNo ratings yet

- IAS 40 - Investment PropertyDocument21 pagesIAS 40 - Investment PropertyGift MaluluNo ratings yet

- IAS 16 - Property Plant and EquipmentDocument35 pagesIAS 16 - Property Plant and EquipmentlaaybaNo ratings yet

- ACCT1111 Chapter 7 LectureDocument62 pagesACCT1111 Chapter 7 LectureWky JimNo ratings yet

- Property Plant Tutorials Number OneDocument46 pagesProperty Plant Tutorials Number OneNatalie SerranoNo ratings yet

- Ias 16Document5 pagesIas 16Edga WariobaNo ratings yet

- Week - 2 Handouts-1 PDFDocument3 pagesWeek - 2 Handouts-1 PDFsumanNo ratings yet

- P1.001 - PPE Revaluation (Lecture Notes & Illustrative Problems)Document2 pagesP1.001 - PPE Revaluation (Lecture Notes & Illustrative Problems)Patrick Kyle Agraviador0% (1)

- Pas 16 PpeDocument37 pagesPas 16 PpeHelaena Ruvie Quitoras PallayaNo ratings yet

- Property, Plant & EquipmentDocument26 pagesProperty, Plant & EquipmentRosalie E. BalhagNo ratings yet

- Financial Accounting: Topic 2: Accounting For Plant AssetsDocument58 pagesFinancial Accounting: Topic 2: Accounting For Plant AssetsDanielle ObenNo ratings yet

- International Financial Reporting Standard IAS 16Document83 pagesInternational Financial Reporting Standard IAS 16tthanh020306No ratings yet

- IPSAS 17. Property-Plant - EquipmentDocument28 pagesIPSAS 17. Property-Plant - EquipmentKibromWeldegiyorgisNo ratings yet

- Ias 16Document46 pagesIas 16Gail BermudezNo ratings yet

- FAR270 MFRS 140 LectureDocument14 pagesFAR270 MFRS 140 LectureNUR HASWANIE MOHD SALMI100% (1)

- Ias 40 - Investment Property - 2Document53 pagesIas 40 - Investment Property - 2penehafoshilengifaNo ratings yet

- Chapter 9 Financial AccountingDocument18 pagesChapter 9 Financial AccountingYukino YukinoshitaNo ratings yet

- IA1 8 Intangible AssetDocument51 pagesIA1 8 Intangible AssetKristel FieldsNo ratings yet

- Financial Accounting Chapter 9Document66 pagesFinancial Accounting Chapter 9Jihen SmariNo ratings yet

- Fundamentals of AccountingDocument76 pagesFundamentals of AccountingNo MoreNo ratings yet

- Unit 2 PpeDocument82 pagesUnit 2 PpeHirut GetachewNo ratings yet

- Module 9Document9 pagesModule 9Althea mary kate MorenoNo ratings yet

- Intacc 1 NotesDocument19 pagesIntacc 1 NotesLouiseNo ratings yet

- Lecture Notes Iass 16 EtcDocument31 pagesLecture Notes Iass 16 Etcmayillahmansaray40No ratings yet

- Plant AssetsDocument41 pagesPlant AssetsShawon RahmanNo ratings yet

- Financial Accounting IIDocument24 pagesFinancial Accounting IIsalman siddiquiNo ratings yet

- Fixed Assets IAS 16Document40 pagesFixed Assets IAS 16feliz100% (1)

- Accounting TerminologyDocument37 pagesAccounting Terminologyjhj01No ratings yet

- Chapter 8 STDocument31 pagesChapter 8 STK60 Triệu Thùy LinhNo ratings yet

- Plant Aset NoteDocument14 pagesPlant Aset NoteFeyorinaNo ratings yet

- Acct2102 CH.6 NotesDocument9 pagesAcct2102 CH.6 NotesChing Tin LamNo ratings yet

- Accounting For PPE Part 1Document20 pagesAccounting For PPE Part 1Keenly ChokeNo ratings yet

- 6902 PPT Materials For UploadDocument13 pages6902 PPT Materials For UploadAljur SalamedaNo ratings yet

- Chapter 7: Ppe and Intangibles: 1. Types of Non-Current AssetsDocument14 pagesChapter 7: Ppe and Intangibles: 1. Types of Non-Current AssetsMarine De CocquéauNo ratings yet

- Gorakhpur Chapter 13052018Document37 pagesGorakhpur Chapter 13052018Sangita NataniNo ratings yet

- Ccounting Principles,: Weygandt, Kieso, & KimmelDocument77 pagesCcounting Principles,: Weygandt, Kieso, & KimmelMUHAMMAD JAMILNo ratings yet

- T7 Accounting For Non Current AssetsDocument45 pagesT7 Accounting For Non Current AssetsHD D100% (1)

- Dental Act 2018Document110 pagesDental Act 2018copyourpairNo ratings yet

- Invoice 360520Document1 pageInvoice 360520Sumaiya AzadNo ratings yet

- 5G NG RAN Ts 138413v150000p PDFDocument256 pages5G NG RAN Ts 138413v150000p PDFSrinath VasamNo ratings yet

- Rubber Technology-I PDFDocument130 pagesRubber Technology-I PDFMohamad SharifiNo ratings yet

- M I N D Mentalism in New Directions TwoDocument268 pagesM I N D Mentalism in New Directions TwoDherendra Kumar YadavNo ratings yet

- If IM LUCKY She Thought About It Mostly As We WalkedDocument13 pagesIf IM LUCKY She Thought About It Mostly As We WalkedTomas D ChaconNo ratings yet

- White Paper Introduction of SAP GTS - The Customs Solution: SapstroomDocument7 pagesWhite Paper Introduction of SAP GTS - The Customs Solution: SapstroomRafael RibNo ratings yet

- Sec5a4 Abs AsrDocument94 pagesSec5a4 Abs AsrTadas PNo ratings yet

- FBI - Table 43Document1 pageFBI - Table 43eonwuka15No ratings yet

- CIA Unclassified: Threat of Serbian Terrorist Attacks, "Kamikaze Pilots" On Nuclear Power StationsDocument10 pagesCIA Unclassified: Threat of Serbian Terrorist Attacks, "Kamikaze Pilots" On Nuclear Power StationsSrebrenica Genocide LibraryNo ratings yet

- Authentication of Instruments and Documents Without The Philippine IslandsDocument19 pagesAuthentication of Instruments and Documents Without The Philippine Islandswakadu095068No ratings yet

- Certificate of Participation: Republic of The PhilippinesDocument2 pagesCertificate of Participation: Republic of The PhilippinesYuri PamaranNo ratings yet

- Geofile 454 - Population PoliciesDocument4 pagesGeofile 454 - Population PolicieshafsabobatNo ratings yet

- 3703 ManualDocument42 pages3703 Manualelectronics malayalamNo ratings yet

- MBA Project Report of Indira Gandhi National Open UniversityDocument4 pagesMBA Project Report of Indira Gandhi National Open UniversityPrakashB144No ratings yet

- Good Quotes VenkatDocument10 pagesGood Quotes Venkatbhappy4ever100% (2)

- End-Time Events and The Last Generation by George R Knight Z-LiborgDocument138 pagesEnd-Time Events and The Last Generation by George R Knight Z-LiborgyaneciticaNo ratings yet

- Vilas County News-Review, July 27, 2011Document28 pagesVilas County News-Review, July 27, 2011News-ReviewNo ratings yet

- DTDC Express Limited: Virtual Campus Recruitment - 2021 Passing Out BatchDocument6 pagesDTDC Express Limited: Virtual Campus Recruitment - 2021 Passing Out BatchVAMSHI MNo ratings yet

- Book 3 SuccessionDocument189 pagesBook 3 SuccessiontatatalaNo ratings yet

- Hanson PLC Case StudyDocument5 pagesHanson PLC Case StudykuntodarpitoNo ratings yet

- Curated List of AI and Machine Learning Resources From Around The Web - by Robbie Allen - Machine Learning in Practice - MediumDocument9 pagesCurated List of AI and Machine Learning Resources From Around The Web - by Robbie Allen - Machine Learning in Practice - Mediumsachin kundalNo ratings yet

- Different Approaches To Atopic Dermatitis by Allergists, Dermatologists, and PediatriciansDocument9 pagesDifferent Approaches To Atopic Dermatitis by Allergists, Dermatologists, and PediatriciansyelsiNo ratings yet

- 3rd Installment - Moreh College, Moreh Arrear W.E.F. 1-10-2020 To 30-06-2021Document14 pages3rd Installment - Moreh College, Moreh Arrear W.E.F. 1-10-2020 To 30-06-2021Celebrity CelebrityNo ratings yet

- Cold Rooms Amp Insulated Panels TSSCDocument32 pagesCold Rooms Amp Insulated Panels TSSCZar KhariNo ratings yet

- Group 9 FOREX Rate Determination and InterventionDocument37 pagesGroup 9 FOREX Rate Determination and InterventionShean BucayNo ratings yet

- 5G Certification OverviewDocument14 pages5G Certification Overviewluis100% (1)

Download as ppt, pdf, or txt

You might also like

- Airline Cabin Crew Training IATA Training Course PDFDocument3 pagesAirline Cabin Crew Training IATA Training Course PDFwin computer0% (1)

- Skittles Fractions Math Target Lesson PlanDocument8 pagesSkittles Fractions Math Target Lesson Planapi-396384317No ratings yet

- Audit of PpeDocument19 pagesAudit of PpeLiezel LaborteNo ratings yet

- ARTHUR - Early Greece: The Origins of The Western Attitude Towards WomenDocument53 pagesARTHUR - Early Greece: The Origins of The Western Attitude Towards WomenCamila BelelliNo ratings yet

- FR-Property Plant N Equipment PDFDocument60 pagesFR-Property Plant N Equipment PDFimrul kaishNo ratings yet

- International Accounting Standard 16Document100 pagesInternational Accounting Standard 16ClarkMaasNo ratings yet

- Ias 16Document39 pagesIas 16Asad KhanafzalNo ratings yet

- F7.1 Chap 3 Tangible AssetDocument47 pagesF7.1 Chap 3 Tangible AssetTrang TranNo ratings yet

- F-II ChapterTwoDocument59 pagesF-II ChapterTwoMohammed AbdulselamNo ratings yet

- Chapter 14 Investment Property StudentsDocument38 pagesChapter 14 Investment Property StudentsBình QuốcNo ratings yet

- PPE - FinalDocument71 pagesPPE - FinalKristen KooNo ratings yet

- Chapter 7 Investment PropertyDocument8 pagesChapter 7 Investment PropertyKrissa Mae Longos100% (2)

- Plant Property and Equipment On Merchandising BusinessDocument5 pagesPlant Property and Equipment On Merchandising BusinessarjohnyabutNo ratings yet

- Property, Plant and EquipmentDocument40 pagesProperty, Plant and EquipmentNatalie SerranoNo ratings yet

- IFA I ChapterDocument12 pagesIFA I Chapteryiberta69No ratings yet

- 9.2 IAS36 - Impairment of Assets 1Document41 pages9.2 IAS36 - Impairment of Assets 1Given RefilweNo ratings yet

- Chapter 9 Lecture NoteDocument47 pagesChapter 9 Lecture Note김가온No ratings yet

- Investment PropertyDocument31 pagesInvestment PropertyHanh CaoNo ratings yet

- Property, Plant and EquipmentDocument46 pagesProperty, Plant and EquipmentAATHARSH RADHAKRISHNANNo ratings yet

- Lecture # 31Document11 pagesLecture # 31HussainNo ratings yet

- Presentationprint TempDocument67 pagesPresentationprint TempMd EndrisNo ratings yet

- International Accounting Standards: IAS 40 Investment PropertyDocument22 pagesInternational Accounting Standards: IAS 40 Investment PropertyPrudence MagaragadaNo ratings yet

- Property, Plant and EquipmentDocument41 pagesProperty, Plant and EquipmentdaisyNo ratings yet

- Assets and Depreciation: October 18, 2018Document14 pagesAssets and Depreciation: October 18, 2018Hareem SattarNo ratings yet

- Corporate Financial Accounting SLE Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 IND AS 40 Investment PropertyDocument12 pagesCorporate Financial Accounting SLE Roll No KSPMCAA012 Dev Shah Mcom Part 2 Sem 4 2022-2023 IND AS 40 Investment PropertyDev ShahNo ratings yet

- Property, Plant and EquipmentDocument66 pagesProperty, Plant and EquipmentThanos The titanNo ratings yet

- IAS 40 - Investment PropertyDocument21 pagesIAS 40 - Investment PropertyGift MaluluNo ratings yet

- IAS 16 - Property Plant and EquipmentDocument35 pagesIAS 16 - Property Plant and EquipmentlaaybaNo ratings yet

- ACCT1111 Chapter 7 LectureDocument62 pagesACCT1111 Chapter 7 LectureWky JimNo ratings yet

- Property Plant Tutorials Number OneDocument46 pagesProperty Plant Tutorials Number OneNatalie SerranoNo ratings yet

- Ias 16Document5 pagesIas 16Edga WariobaNo ratings yet

- Week - 2 Handouts-1 PDFDocument3 pagesWeek - 2 Handouts-1 PDFsumanNo ratings yet

- P1.001 - PPE Revaluation (Lecture Notes & Illustrative Problems)Document2 pagesP1.001 - PPE Revaluation (Lecture Notes & Illustrative Problems)Patrick Kyle Agraviador0% (1)

- Pas 16 PpeDocument37 pagesPas 16 PpeHelaena Ruvie Quitoras PallayaNo ratings yet

- Property, Plant & EquipmentDocument26 pagesProperty, Plant & EquipmentRosalie E. BalhagNo ratings yet

- Financial Accounting: Topic 2: Accounting For Plant AssetsDocument58 pagesFinancial Accounting: Topic 2: Accounting For Plant AssetsDanielle ObenNo ratings yet

- International Financial Reporting Standard IAS 16Document83 pagesInternational Financial Reporting Standard IAS 16tthanh020306No ratings yet

- IPSAS 17. Property-Plant - EquipmentDocument28 pagesIPSAS 17. Property-Plant - EquipmentKibromWeldegiyorgisNo ratings yet

- Ias 16Document46 pagesIas 16Gail BermudezNo ratings yet

- FAR270 MFRS 140 LectureDocument14 pagesFAR270 MFRS 140 LectureNUR HASWANIE MOHD SALMI100% (1)

- Ias 40 - Investment Property - 2Document53 pagesIas 40 - Investment Property - 2penehafoshilengifaNo ratings yet

- Chapter 9 Financial AccountingDocument18 pagesChapter 9 Financial AccountingYukino YukinoshitaNo ratings yet

- IA1 8 Intangible AssetDocument51 pagesIA1 8 Intangible AssetKristel FieldsNo ratings yet

- Financial Accounting Chapter 9Document66 pagesFinancial Accounting Chapter 9Jihen SmariNo ratings yet

- Fundamentals of AccountingDocument76 pagesFundamentals of AccountingNo MoreNo ratings yet

- Unit 2 PpeDocument82 pagesUnit 2 PpeHirut GetachewNo ratings yet

- Module 9Document9 pagesModule 9Althea mary kate MorenoNo ratings yet

- Intacc 1 NotesDocument19 pagesIntacc 1 NotesLouiseNo ratings yet

- Lecture Notes Iass 16 EtcDocument31 pagesLecture Notes Iass 16 Etcmayillahmansaray40No ratings yet

- Plant AssetsDocument41 pagesPlant AssetsShawon RahmanNo ratings yet

- Financial Accounting IIDocument24 pagesFinancial Accounting IIsalman siddiquiNo ratings yet

- Fixed Assets IAS 16Document40 pagesFixed Assets IAS 16feliz100% (1)

- Accounting TerminologyDocument37 pagesAccounting Terminologyjhj01No ratings yet

- Chapter 8 STDocument31 pagesChapter 8 STK60 Triệu Thùy LinhNo ratings yet

- Plant Aset NoteDocument14 pagesPlant Aset NoteFeyorinaNo ratings yet

- Acct2102 CH.6 NotesDocument9 pagesAcct2102 CH.6 NotesChing Tin LamNo ratings yet

- Accounting For PPE Part 1Document20 pagesAccounting For PPE Part 1Keenly ChokeNo ratings yet

- 6902 PPT Materials For UploadDocument13 pages6902 PPT Materials For UploadAljur SalamedaNo ratings yet

- Chapter 7: Ppe and Intangibles: 1. Types of Non-Current AssetsDocument14 pagesChapter 7: Ppe and Intangibles: 1. Types of Non-Current AssetsMarine De CocquéauNo ratings yet

- Gorakhpur Chapter 13052018Document37 pagesGorakhpur Chapter 13052018Sangita NataniNo ratings yet

- Ccounting Principles,: Weygandt, Kieso, & KimmelDocument77 pagesCcounting Principles,: Weygandt, Kieso, & KimmelMUHAMMAD JAMILNo ratings yet

- T7 Accounting For Non Current AssetsDocument45 pagesT7 Accounting For Non Current AssetsHD D100% (1)

- Dental Act 2018Document110 pagesDental Act 2018copyourpairNo ratings yet

- Invoice 360520Document1 pageInvoice 360520Sumaiya AzadNo ratings yet

- 5G NG RAN Ts 138413v150000p PDFDocument256 pages5G NG RAN Ts 138413v150000p PDFSrinath VasamNo ratings yet

- Rubber Technology-I PDFDocument130 pagesRubber Technology-I PDFMohamad SharifiNo ratings yet

- M I N D Mentalism in New Directions TwoDocument268 pagesM I N D Mentalism in New Directions TwoDherendra Kumar YadavNo ratings yet

- If IM LUCKY She Thought About It Mostly As We WalkedDocument13 pagesIf IM LUCKY She Thought About It Mostly As We WalkedTomas D ChaconNo ratings yet

- White Paper Introduction of SAP GTS - The Customs Solution: SapstroomDocument7 pagesWhite Paper Introduction of SAP GTS - The Customs Solution: SapstroomRafael RibNo ratings yet

- Sec5a4 Abs AsrDocument94 pagesSec5a4 Abs AsrTadas PNo ratings yet

- FBI - Table 43Document1 pageFBI - Table 43eonwuka15No ratings yet

- CIA Unclassified: Threat of Serbian Terrorist Attacks, "Kamikaze Pilots" On Nuclear Power StationsDocument10 pagesCIA Unclassified: Threat of Serbian Terrorist Attacks, "Kamikaze Pilots" On Nuclear Power StationsSrebrenica Genocide LibraryNo ratings yet

- Authentication of Instruments and Documents Without The Philippine IslandsDocument19 pagesAuthentication of Instruments and Documents Without The Philippine Islandswakadu095068No ratings yet

- Certificate of Participation: Republic of The PhilippinesDocument2 pagesCertificate of Participation: Republic of The PhilippinesYuri PamaranNo ratings yet

- Geofile 454 - Population PoliciesDocument4 pagesGeofile 454 - Population PolicieshafsabobatNo ratings yet

- 3703 ManualDocument42 pages3703 Manualelectronics malayalamNo ratings yet

- MBA Project Report of Indira Gandhi National Open UniversityDocument4 pagesMBA Project Report of Indira Gandhi National Open UniversityPrakashB144No ratings yet

- Good Quotes VenkatDocument10 pagesGood Quotes Venkatbhappy4ever100% (2)

- End-Time Events and The Last Generation by George R Knight Z-LiborgDocument138 pagesEnd-Time Events and The Last Generation by George R Knight Z-LiborgyaneciticaNo ratings yet

- Vilas County News-Review, July 27, 2011Document28 pagesVilas County News-Review, July 27, 2011News-ReviewNo ratings yet

- DTDC Express Limited: Virtual Campus Recruitment - 2021 Passing Out BatchDocument6 pagesDTDC Express Limited: Virtual Campus Recruitment - 2021 Passing Out BatchVAMSHI MNo ratings yet

- Book 3 SuccessionDocument189 pagesBook 3 SuccessiontatatalaNo ratings yet

- Hanson PLC Case StudyDocument5 pagesHanson PLC Case StudykuntodarpitoNo ratings yet

- Curated List of AI and Machine Learning Resources From Around The Web - by Robbie Allen - Machine Learning in Practice - MediumDocument9 pagesCurated List of AI and Machine Learning Resources From Around The Web - by Robbie Allen - Machine Learning in Practice - Mediumsachin kundalNo ratings yet

- Different Approaches To Atopic Dermatitis by Allergists, Dermatologists, and PediatriciansDocument9 pagesDifferent Approaches To Atopic Dermatitis by Allergists, Dermatologists, and PediatriciansyelsiNo ratings yet

- 3rd Installment - Moreh College, Moreh Arrear W.E.F. 1-10-2020 To 30-06-2021Document14 pages3rd Installment - Moreh College, Moreh Arrear W.E.F. 1-10-2020 To 30-06-2021Celebrity CelebrityNo ratings yet

- Cold Rooms Amp Insulated Panels TSSCDocument32 pagesCold Rooms Amp Insulated Panels TSSCZar KhariNo ratings yet

- Group 9 FOREX Rate Determination and InterventionDocument37 pagesGroup 9 FOREX Rate Determination and InterventionShean BucayNo ratings yet

- 5G Certification OverviewDocument14 pages5G Certification Overviewluis100% (1)