Download as pptx, pdf, or txt

You might also like

- Assignment-1 (Eco & Actg For Engineers) Exercise - 1Document4 pagesAssignment-1 (Eco & Actg For Engineers) Exercise - 1Nayeem HossainNo ratings yet

- Module 4Document67 pagesModule 4Chicos tacos100% (3)

- Lesson 2 Formation of PartnershipDocument27 pagesLesson 2 Formation of PartnershipheyheyNo ratings yet

- Financial Guarantee - ProjectDocument3 pagesFinancial Guarantee - ProjectArnab SahaNo ratings yet

- Ameritrade Case SolutionDocument31 pagesAmeritrade Case Solutionsanz0840% (5)

- Closing EntriesDocument6 pagesClosing Entriesspam.ml2023No ratings yet

- Toaz - Info Preparation of Financial Statements and Its Importance PRDocument7 pagesToaz - Info Preparation of Financial Statements and Its Importance PRCriscel SantiagoNo ratings yet

- Class 11 Accountancy NCERT Textbook Part-II Chapter 10 Financial Statements-IIDocument70 pagesClass 11 Accountancy NCERT Textbook Part-II Chapter 10 Financial Statements-IIPathan KausarNo ratings yet

- M8 Correcting Closing Reversing Entries and Financial StatementsDocument10 pagesM8 Correcting Closing Reversing Entries and Financial StatementsMicha AlcainNo ratings yet

- Preparing A Trial Balance: Increase An Account)Document7 pagesPreparing A Trial Balance: Increase An Account)Mubarrach MatabalaoNo ratings yet

- Financial Statements - II: 360 AccountancyDocument65 pagesFinancial Statements - II: 360 AccountancyshantX100% (1)

- Financial Statements 2Document65 pagesFinancial Statements 2srisrirockstarNo ratings yet

- Closing EntriesDocument4 pagesClosing Entriesapi-299265916100% (1)

- ACCOUNTANCY (CA) Answer Key Kerala +2 Annual Exam March 2020Document7 pagesACCOUNTANCY (CA) Answer Key Kerala +2 Annual Exam March 2020soumyabibin573No ratings yet

- Entrepreneurship Q2 Week 8Document10 pagesEntrepreneurship Q2 Week 8Nizel Sherlyn NarsicoNo ratings yet

- ChapterDocument47 pagesChapteralfyomar79No ratings yet

- Business Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business (Part Ii-A)Document9 pagesBusiness Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business (Part Ii-A)Tumamudtamud, JenaNo ratings yet

- FA FOR BADM Unit 3Document10 pagesFA FOR BADM Unit 3GUDATA ABARANo ratings yet

- 30 - 09 - Final AccountsDocument40 pages30 - 09 - Final Accountssachin lanjewarNo ratings yet

- Accounting Cycle of A Service Provider: Closing Entries, Post-Closing Trial Balance and Reversing EntriesDocument7 pagesAccounting Cycle of A Service Provider: Closing Entries, Post-Closing Trial Balance and Reversing EntriesRio GardoceNo ratings yet

- Entrepreneurship Q2 Week 9Document9 pagesEntrepreneurship Q2 Week 9Nizel Sherlyn NarsicoNo ratings yet

- Closing and Worksheet: 20.1 Closing Entries For Revenue AccountsDocument8 pagesClosing and Worksheet: 20.1 Closing Entries For Revenue AccountsZaheer Swati100% (1)

- Class DocsDocument32 pagesClass Docsgeorge antwiNo ratings yet

- Chapter 8 - Sample ProblemDocument2 pagesChapter 8 - Sample ProblemMaDine 19No ratings yet

- Principles of AccountingDocument10 pagesPrinciples of AccountingSohail Liaqat AliNo ratings yet

- FOW 9 - PA - Notes Session 2Document15 pagesFOW 9 - PA - Notes Session 223006022No ratings yet

- Module 9 Completing The Accounting CycleDocument5 pagesModule 9 Completing The Accounting CyclemallarilecarNo ratings yet

- Bài tập C4Document4 pagesBài tập C4Khanh LêNo ratings yet

- 助教課講義 Ch.3 (A4雙面)Document10 pages助教課講義 Ch.3 (A4雙面)5213adamNo ratings yet

- Fundamentals in Accountancy and Business Management Ii: Academic Subject: (GRADE 12 First Semester)Document7 pagesFundamentals in Accountancy and Business Management Ii: Academic Subject: (GRADE 12 First Semester)MarielLee Ramos VillarealNo ratings yet

- CZ21A MODEL Answer KeyDocument7 pagesCZ21A MODEL Answer KeymadhuNo ratings yet

- Financial Statements - II: 372 AccountancyDocument65 pagesFinancial Statements - II: 372 AccountancyBhartiNo ratings yet

- 2nd Summative TestDocument2 pages2nd Summative Testje-ann montejoNo ratings yet

- Solution Manual For Financial Acct2 2nd Edition by GodwinDocument36 pagesSolution Manual For Financial Acct2 2nd Edition by GodwinArielCooperbzqsp100% (87)

- Ac1 Reviewer FinalsDocument5 pagesAc1 Reviewer FinalsMark Christian BrlNo ratings yet

- Page 226 236 - Lyka Mae AdluzDocument9 pagesPage 226 236 - Lyka Mae AdluzWendell Maverick MasuhayNo ratings yet

- Kelompok 9 Closing EntriesDocument17 pagesKelompok 9 Closing EntriesrizkiNo ratings yet

- Financial Accounting 1 Unit 3Document11 pagesFinancial Accounting 1 Unit 3AbdirahmanNo ratings yet

- MODULE 7 and 8 ACCDocument3 pagesMODULE 7 and 8 ACCnorie jane pacisNo ratings yet

- Chapter 6 - Adjusting Closing EntriesDocument5 pagesChapter 6 - Adjusting Closing EntriesSuzanne SenadreNo ratings yet

- Financial Accounting & Analysis Dec'22Document3 pagesFinancial Accounting & Analysis Dec'22ankurNo ratings yet

- Financial Accounting Chapter 9: Accounts Receivable: Classification of ReceivablesDocument2 pagesFinancial Accounting Chapter 9: Accounts Receivable: Classification of ReceivablesMay Grethel Joy PeranteNo ratings yet

- Managerial Accounting1Document33 pagesManagerial Accounting1MM-Tansiongco, Keino R.No ratings yet

- Fundamentals of ABM1 - Q4 - LAS1 DRAFTDocument17 pagesFundamentals of ABM1 - Q4 - LAS1 DRAFTSitti Halima Amilbahar AdgesNo ratings yet

- Financial Reporting and Analysis 7th Edition by Gibson ISBN Solution ManualDocument46 pagesFinancial Reporting and Analysis 7th Edition by Gibson ISBN Solution Manualphyllis100% (38)

- Entrepreneurship - Quarter 2 Week 9Document8 pagesEntrepreneurship - Quarter 2 Week 9SHEEN ALUBANo ratings yet

- Task 13 - 16Document5 pagesTask 13 - 16Ton VossenNo ratings yet

- Financial & Managerial AccountingDocument21 pagesFinancial & Managerial AccountingRifath AhmedNo ratings yet

- Accounts Home Test 2Document7 pagesAccounts Home Test 2Ashish RaiNo ratings yet

- Notes - ACCTG 114 - 04 26 - 04 28 2022Document13 pagesNotes - ACCTG 114 - 04 26 - 04 28 2022Janna Mari FriasNo ratings yet

- Assignment 3Document8 pagesAssignment 3Denny ChakauyaNo ratings yet

- Exercises P Class2-2022Document9 pagesExercises P Class2-2022Angel MéndezNo ratings yet

- ACC 311 PartnershipDocument34 pagesACC 311 PartnershipokeowoNo ratings yet

- Lecture Week 8Document51 pagesLecture Week 8Muhammad HusseinNo ratings yet

- Financial Accounting & AnalysisDocument16 pagesFinancial Accounting & AnalysisMohit ChaudharyNo ratings yet

- Debit Credit Service Revenue Interest Revenue Income SummaryDocument2 pagesDebit Credit Service Revenue Interest Revenue Income SummaryJessa Marie CabugnasonNo ratings yet

- Financial StatementsDocument65 pagesFinancial StatementsApollo Institute of Hospital AdministrationNo ratings yet

- A. MODULE 1a BASIC ACCOUNTING BOOKKEEPINGDocument9 pagesA. MODULE 1a BASIC ACCOUNTING BOOKKEEPINGMer CyNo ratings yet

- Bookkeeping Video Training: (Handout)Document22 pagesBookkeeping Video Training: (Handout)Yusuf RaharjaNo ratings yet

- Final Account (Satyanath Mohapatra)Document38 pagesFinal Account (Satyanath Mohapatra)smrutiranjan swainNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Implementationof Genderand Developmentamong Higher Education Institutions Inputto GADEnhancement ProgramDocument9 pagesImplementationof Genderand Developmentamong Higher Education Institutions Inputto GADEnhancement Programjoel phillip GranadaNo ratings yet

- Feedback FormDocument2 pagesFeedback Formjoel phillip GranadaNo ratings yet

- Creative Writing ActivityDocument3 pagesCreative Writing Activityjoel phillip GranadaNo ratings yet

- P1ban-Fr-017 - Best Practices FormDocument2 pagesP1ban-Fr-017 - Best Practices Formjoel phillip GranadaNo ratings yet

- My Farm Business PlanDocument3 pagesMy Farm Business Planjoel phillip GranadaNo ratings yet

- Tle10 wk2d2Document24 pagesTle10 wk2d2joel phillip GranadaNo ratings yet

- Tle 10Document16 pagesTle 10joel phillip GranadaNo ratings yet

- CW GastemDocument2 pagesCW Gastemjoel phillip GranadaNo ratings yet

- Figurative Language Is Used and Should Be Understood Imaginatively and NonDocument2 pagesFigurative Language Is Used and Should Be Understood Imaginatively and Nonjoel phillip GranadaNo ratings yet

- Forgiveness - FinalDocument15 pagesForgiveness - Finaljoel phillip GranadaNo ratings yet

- SBM WebsiteDocument14 pagesSBM Websitejoel phillip GranadaNo ratings yet

- The Theory of Social EvolutionDocument3 pagesThe Theory of Social Evolutionjoel phillip Granada100% (2)

- SUBJECTS - DM 151 s2019Document23 pagesSUBJECTS - DM 151 s2019joel phillip GranadaNo ratings yet

- Ipcc LK Q4 2017Document84 pagesIpcc LK Q4 2017Andreas PaskalisNo ratings yet

- Chapter 8Document14 pagesChapter 8raghavgarg106No ratings yet

- Accounting For Joint ArrangementsDocument4 pagesAccounting For Joint ArrangementsQuinn Samaon100% (1)

- 2024 05 14 15 34 47mar 24 - 160102Document12 pages2024 05 14 15 34 47mar 24 - 160102deepakpetwal18No ratings yet

- Microfinance: Mario La Torre and Gianfranco A. VentoDocument195 pagesMicrofinance: Mario La Torre and Gianfranco A. VentoDivyanshuNo ratings yet

- Managerial Accounting Chapter 4Document59 pagesManagerial Accounting Chapter 4jesica.k237No ratings yet

- Financial Services: Finance Companies: True / False QuestionsDocument16 pagesFinancial Services: Finance Companies: True / False Questionslatifa hnNo ratings yet

- Lecture 03Document108 pagesLecture 03Masood AliNo ratings yet

- Instruments of Moneytary PolicyDocument3 pagesInstruments of Moneytary PolicyJaydeep Paul100% (1)

- Attempt History: Due Mar 16 at 19:45 Available Mar 16 at 17:45 - Mar 16 at 19:45 1 / 1 PtsDocument5 pagesAttempt History: Due Mar 16 at 19:45 Available Mar 16 at 17:45 - Mar 16 at 19:45 1 / 1 PtsmlaNo ratings yet

- Icici Lombard Mh!49966Document3 pagesIcici Lombard Mh!49966suresh sivadasanNo ratings yet

- Chapter 2Document15 pagesChapter 2Dharani PNo ratings yet

- 2nd Business Finance Q2 W 3 - II by Y.G. - Revised - JOSEPH AURELLODocument12 pages2nd Business Finance Q2 W 3 - II by Y.G. - Revised - JOSEPH AURELLOFairly May LaysonNo ratings yet

- Fundamentals of Accountancy, Business and Management 1: Quarter 3 - Module 5: Books of AccountsDocument29 pagesFundamentals of Accountancy, Business and Management 1: Quarter 3 - Module 5: Books of AccountsMarlyn Lotivio100% (2)

- Time Value of MoneyDocument2 pagesTime Value of Moneyangelavani_16No ratings yet

- Tugas 6 - Aulia KhairaniDocument3 pagesTugas 6 - Aulia KhairaniadvokesmahmmbNo ratings yet

- Janki SinghDocument77 pagesJanki SinghJankiNo ratings yet

- Product Specification GuideDocument7 pagesProduct Specification Guidecrstngnt1991No ratings yet

- CROWN VETERINARY SERVICES PRIVATE LIMITED Financial ReportDocument19 pagesCROWN VETERINARY SERVICES PRIVATE LIMITED Financial ReportVidhi KapurNo ratings yet

- Risk Management With Icici Prudential Life Insurance by Rahul LalDocument72 pagesRisk Management With Icici Prudential Life Insurance by Rahul LalArvind KumarNo ratings yet

- Burgundy Elite Wealth Manager PDFDocument12 pagesBurgundy Elite Wealth Manager PDFRajeev P TibarewalNo ratings yet

- Rickards The Global Elites' Secret Plan For The Next Financial CrisisDocument4 pagesRickards The Global Elites' Secret Plan For The Next Financial CrisisOCHETE AMNo ratings yet

- Legal & Regulatory Aspects of Banking - JAIIBDocument18 pagesLegal & Regulatory Aspects of Banking - JAIIBPrasenjit RoyNo ratings yet

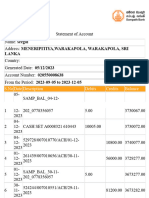

- Lanka: S.No Date Description Debits Credits BalanceDocument34 pagesLanka: S.No Date Description Debits Credits BalanceLasith IsuruNo ratings yet

- Business Combi Part 2Document20 pagesBusiness Combi Part 2Rica Joy RuzgalNo ratings yet

- Types of MortgageDocument5 pagesTypes of MortgageAneeka NiazNo ratings yet

- Management Services Agamata 2014Document12 pagesManagement Services Agamata 2014NICOLE FAYE SAN MIGUELNo ratings yet

- Vidya Mandir Ind. PU College Accountancy 2 PUC Assessment 1-July 2020 Total Marks:30 Answer All QuestionsDocument2 pagesVidya Mandir Ind. PU College Accountancy 2 PUC Assessment 1-July 2020 Total Marks:30 Answer All QuestionsBlahjNo ratings yet