Budget Preparation

Budget Preparation

You might also like

- Allen Lane Case Write UpDocument2 pagesAllen Lane Case Write UpAndrew Choi100% (1)

- Analysis of Fertilizer Industry of PakistanDocument59 pagesAnalysis of Fertilizer Industry of PakistanMaryam97% (30)

- Group 6 - GreenDust RevolutionDocument19 pagesGroup 6 - GreenDust RevolutionVipul BhagatNo ratings yet

- Bosa Loan Application FormDocument2 pagesBosa Loan Application Formal lakwena100% (1)

- Research and AnalysisDocument6 pagesResearch and Analysisbawangb210% (1)

- Financial Projections and BudgetsDocument53 pagesFinancial Projections and BudgetsRaquel Sibal RodriguezNo ratings yet

- Planning and Budgetng.: Course: Introduction To FinancialDocument38 pagesPlanning and Budgetng.: Course: Introduction To FinancialMichaelNo ratings yet

- Short-Term BudgetingDocument7 pagesShort-Term BudgetingMary Elaine DiasantaNo ratings yet

- Budgeting 1Document53 pagesBudgeting 1MRIDUL GOELNo ratings yet

- Budgetary Planning and ControlDocument67 pagesBudgetary Planning and ControlJade Ballado-TanNo ratings yet

- Business Finance 2ndquarterDocument176 pagesBusiness Finance 2ndquarterJanelle Dela CruzNo ratings yet

- Businessfinance12 Handout Budget-PreparationDocument5 pagesBusinessfinance12 Handout Budget-PreparationApril Joy De BelenNo ratings yet

- The Use of Budgets in Planning and Decision MakingDocument7 pagesThe Use of Budgets in Planning and Decision MakingKirito UzumakiNo ratings yet

- BudgetDocument5 pagesBudgetmuktaNo ratings yet

- Chapter 9 - Budget PreparationDocument30 pagesChapter 9 - Budget PreparationvdhienNo ratings yet

- MgrawConnect - Chapter 8 Slides - Answer & NotesDocument11 pagesMgrawConnect - Chapter 8 Slides - Answer & NotescNo ratings yet

- CH7 BudgetingDocument51 pagesCH7 BudgetingYMNo ratings yet

- Financial Management 1 - Chapter 16Document6 pagesFinancial Management 1 - Chapter 16lerryroyceNo ratings yet

- Administrative Cost BudgetDocument4 pagesAdministrative Cost BudgetchakriNo ratings yet

- U02 Budget Methodolgies and Budget PreparationDocument26 pagesU02 Budget Methodolgies and Budget PreparationIslam AhmedNo ratings yet

- Individual Assignment 4 - Trần Thị Quỳnh NhiDocument7 pagesIndividual Assignment 4 - Trần Thị Quỳnh NhiTrần Thị Quỳnh NhiNo ratings yet

- Financial Planning Tool and ConceptDocument125 pagesFinancial Planning Tool and ConceptKareen Tapia PublicoNo ratings yet

- 4 - BF - For STUDENTSDocument47 pages4 - BF - For STUDENTSPhill SamonteNo ratings yet

- Chapter-Two: Financial Planning and ProjectionDocument6 pagesChapter-Two: Financial Planning and Projectionমেহেদী হাসানNo ratings yet

- Budget Matterial For The Students NewDocument10 pagesBudget Matterial For The Students NewheysemNo ratings yet

- Group Iii. Business FinanceDocument11 pagesGroup Iii. Business FinanceChristian PhilipNo ratings yet

- Budgeting Planning and ControlDocument31 pagesBudgeting Planning and Controlintan agustina100% (1)

- CHAPTER 3 Financial PlanningDocument7 pagesCHAPTER 3 Financial Planningflorabel parana0% (1)

- Master BudgetDocument6 pagesMaster BudgetPacir QubeNo ratings yet

- Chapter Two The Master BudgetDocument49 pagesChapter Two The Master BudgetGutu Usma'ilNo ratings yet

- Illustrative Problem On Master BudgetingDocument13 pagesIllustrative Problem On Master BudgetingSumendra Shrestha84% (19)

- Teodoro M. Luansing College of Rosario: Senior High School DepartmentDocument7 pagesTeodoro M. Luansing College of Rosario: Senior High School DepartmentSamantha Alice LysanderNo ratings yet

- 8 Comprehensive Examination: Case # 1Document3 pages8 Comprehensive Examination: Case # 1Sajid AliNo ratings yet

- Cost and Management Accounting IIDocument9 pagesCost and Management Accounting IIarefayne wodajoNo ratings yet

- Chapter 4A Financial Planning ManagementDocument20 pagesChapter 4A Financial Planning ManagementAlexa RomarateNo ratings yet

- BUSFIN 6a FINACIAL PLANNING TOOLS AND CONCEPTDocument14 pagesBUSFIN 6a FINACIAL PLANNING TOOLS AND CONCEPTRenz AbadNo ratings yet

- Budgeting Chp9Document30 pagesBudgeting Chp9alp_ganNo ratings yet

- Budgeting 101: By: Limheya Lester Glenn National University-ManilaDocument42 pagesBudgeting 101: By: Limheya Lester Glenn National University-ManilaXXXXXXXXXXXXXXXXXXNo ratings yet

- Chapter 6Document13 pagesChapter 6yana kiutNo ratings yet

- Chapter 9 Profit PlanningDocument3 pagesChapter 9 Profit Planningahmed arfanNo ratings yet

- Study Material of FMDocument22 pagesStudy Material of FMPrakhar SahuNo ratings yet

- Advanced Financial MGMT Notes 1 To 30Document87 pagesAdvanced Financial MGMT Notes 1 To 30Sangeetha K SNo ratings yet

- Chapter 9 Profit PlanningDocument3 pagesChapter 9 Profit Planningahmed arfanNo ratings yet

- Lesson 4 Part 1 Budget PreparationDocument19 pagesLesson 4 Part 1 Budget PreparationmariannedakilaNo ratings yet

- 5PM FinancialAnlysDocument4 pages5PM FinancialAnlysAmba GeetanjaliNo ratings yet

- FM II - Chapter 03, Financial Planning & ForecastingDocument28 pagesFM II - Chapter 03, Financial Planning & ForecastingHace Adis100% (1)

- BudgetingDocument4 pagesBudgetingshielamaelbaisacNo ratings yet

- Module 3 BudgetingDocument8 pagesModule 3 BudgetingMon RamNo ratings yet

- Chapter 9 Review - UpdatedDocument10 pagesChapter 9 Review - UpdatedTamerat FikaduNo ratings yet

- Financial Planning and BudgetingDocument33 pagesFinancial Planning and Budgetingsalonzonicole04No ratings yet

- Budgeting Without AnswersDocument5 pagesBudgeting Without AnswersHertz Dasmariñas GappiNo ratings yet

- Master BudgetDocument15 pagesMaster BudgetHaider AliNo ratings yet

- Business FinanceDocument22 pagesBusiness FinancenattoykoNo ratings yet

- Financial Planning and BudgetingDocument45 pagesFinancial Planning and BudgetingRafael BensigNo ratings yet

- Ch.13 Managing Small Business FinanceDocument5 pagesCh.13 Managing Small Business FinanceBaesick MoviesNo ratings yet

- Lecture Notes On Financial ForecastingDocument7 pagesLecture Notes On Financial Forecastingpalkee100% (3)

- Master BudgetDocument6 pagesMaster BudgetPia LustreNo ratings yet

- Chapter 5 - Strategy and Master BudgetDocument8 pagesChapter 5 - Strategy and Master BudgetNelsie PinedaNo ratings yet

- Business Finance Notes 4thDocument10 pagesBusiness Finance Notes 4thGrobotan LuchiNo ratings yet

- The Importance of Budgets in Financial Planning ClassDocument33 pagesThe Importance of Budgets in Financial Planning ClassMonkey2111No ratings yet

- Midterm Topic 4.1 - Notes - Sales Budgets and Production BudgetsDocument2 pagesMidterm Topic 4.1 - Notes - Sales Budgets and Production BudgetslanoyjessicaellahNo ratings yet

- Budgeting: A Group PresentationDocument43 pagesBudgeting: A Group PresentationSaud Khan WazirNo ratings yet

- Set 2 - Kinematics IIDocument29 pagesSet 2 - Kinematics IILizbethHazelRiveraNo ratings yet

- Lesson 3B - Combinations of FunctionsDocument33 pagesLesson 3B - Combinations of FunctionsLizbethHazelRiveraNo ratings yet

- Time Value of A MoneyDocument23 pagesTime Value of A MoneyLizbethHazelRiveraNo ratings yet

- Bus FinanceDocument13 pagesBus FinanceLizbethHazelRiveraNo ratings yet

- Functions Composite Inverse Forming DemonstrationDocument16 pagesFunctions Composite Inverse Forming DemonstrationLizbethHazelRiveraNo ratings yet

- 01 Financial SystemDocument13 pages01 Financial SystemLizbethHazelRiveraNo ratings yet

- The Firm and Its EnvironmentDocument25 pagesThe Firm and Its EnvironmentLizbethHazelRiveraNo ratings yet

- Business Finance FIDPDocument8 pagesBusiness Finance FIDPLizbethHazelRivera100% (1)

- 01 Introduction To Business FinanceDocument33 pages01 Introduction To Business FinanceLizbethHazelRiveraNo ratings yet

- PlanningsDocument25 pagesPlanningsLizbethHazelRiveraNo ratings yet

- Lesson 1 - Part IIIDocument10 pagesLesson 1 - Part IIILizbethHazelRiveraNo ratings yet

- Lesson 3Document25 pagesLesson 3LizbethHazelRiveraNo ratings yet

- Lesson 2Document23 pagesLesson 2LizbethHazelRiveraNo ratings yet

- Lesson 1 - Part IDocument25 pagesLesson 1 - Part ILizbethHazelRiveraNo ratings yet

- Lesson 1 - Part IiDocument24 pagesLesson 1 - Part IiLizbethHazelRiveraNo ratings yet

- ROI of ElearningDocument18 pagesROI of Elearningnhzaidi100% (1)

- North Dakota State University: Policy ManualDocument6 pagesNorth Dakota State University: Policy ManualTarikua TesfaNo ratings yet

- Toyota Custom ERP System Case Study SumatoSoftDocument2 pagesToyota Custom ERP System Case Study SumatoSoftnishanth4313No ratings yet

- LECT # 1 - Intro To Cost & Mang AccountingDocument28 pagesLECT # 1 - Intro To Cost & Mang Accountingmuhammad.16483.acNo ratings yet

- Scope and Limitation - Printing SystemDocument1 pageScope and Limitation - Printing SystemIvan Bendiola100% (3)

- F 2 HVZL5 TKQ1 ZGejtDocument3 pagesF 2 HVZL5 TKQ1 ZGejtmark3d printersNo ratings yet

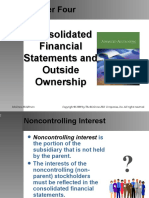

- Chapter 4 - Consolidated Financial Statements and Outside OwnershipDocument25 pagesChapter 4 - Consolidated Financial Statements and Outside OwnershipBLe BerNo ratings yet

- Filed Dakota Patriot PAC 2022 Year EndDocument3 pagesFiled Dakota Patriot PAC 2022 Year EndRob Port100% (1)

- Elasticity and Tax IncidenceDocument11 pagesElasticity and Tax IncidenceKiara RamdhawNo ratings yet

- Bworld Ecoforum 2022Document6 pagesBworld Ecoforum 2022Ralph MontejoNo ratings yet

- Partnership LiquidationDocument10 pagesPartnership LiquidationchristineNo ratings yet

- BA Outline ChecklistDocument44 pagesBA Outline ChecklisttomNo ratings yet

- CH (10) - Book AnswersDocument17 pagesCH (10) - Book AnswersabdulraufdghaybeejNo ratings yet

- Bond and Bond Features and Its Example AssignmentDocument4 pagesBond and Bond Features and Its Example AssignmentWaqaarNo ratings yet

- LatikDocument6 pagesLatikkpk8xnwmfgNo ratings yet

- T26 026 902 PDFDocument7 pagesT26 026 902 PDFBenNo ratings yet

- Standards Australia Case Study Oil GasDocument1 pageStandards Australia Case Study Oil GasJohn cenaNo ratings yet

- MTR Form PDFDocument2 pagesMTR Form PDFUstazFaizalAriffinOriginalNo ratings yet

- Emil Remigio Resume-2Document2 pagesEmil Remigio Resume-2api-509061708No ratings yet

- Sales and Distribution Channel of ITC SADocument12 pagesSales and Distribution Channel of ITC SAPranav ManghatNo ratings yet

- Math 12 ABM Org - MGT Q2-Week 6Document14 pagesMath 12 ABM Org - MGT Q2-Week 6Charlene BorladoNo ratings yet

- POPULAR INDUSTRIES LIMITED V EASTERN GARMENT MANUFACTURING SDN BHD, (1989) 3 MLJ 360Document14 pagesPOPULAR INDUSTRIES LIMITED V EASTERN GARMENT MANUFACTURING SDN BHD, (1989) 3 MLJ 360nurulashikin mursid0% (1)

- Form 1 Math AssignmentDocument4 pagesForm 1 Math Assignmentomimarc6No ratings yet

- Stop Smoking ConsultingDocument16 pagesStop Smoking ConsultingKazim AdilNo ratings yet

- Wa0008.Document2 pagesWa0008.Robert DowneyNo ratings yet

- Best Practice For Refinery FlowsheetsDocument6 pagesBest Practice For Refinery Flowsheetskhaled_behery9934No ratings yet

Download as pptx, pdf, or txt

You might also like

- Allen Lane Case Write UpDocument2 pagesAllen Lane Case Write UpAndrew Choi100% (1)

- Analysis of Fertilizer Industry of PakistanDocument59 pagesAnalysis of Fertilizer Industry of PakistanMaryam97% (30)

- Group 6 - GreenDust RevolutionDocument19 pagesGroup 6 - GreenDust RevolutionVipul BhagatNo ratings yet

- Bosa Loan Application FormDocument2 pagesBosa Loan Application Formal lakwena100% (1)

- Research and AnalysisDocument6 pagesResearch and Analysisbawangb210% (1)

- Financial Projections and BudgetsDocument53 pagesFinancial Projections and BudgetsRaquel Sibal RodriguezNo ratings yet

- Planning and Budgetng.: Course: Introduction To FinancialDocument38 pagesPlanning and Budgetng.: Course: Introduction To FinancialMichaelNo ratings yet

- Short-Term BudgetingDocument7 pagesShort-Term BudgetingMary Elaine DiasantaNo ratings yet

- Budgeting 1Document53 pagesBudgeting 1MRIDUL GOELNo ratings yet

- Budgetary Planning and ControlDocument67 pagesBudgetary Planning and ControlJade Ballado-TanNo ratings yet

- Business Finance 2ndquarterDocument176 pagesBusiness Finance 2ndquarterJanelle Dela CruzNo ratings yet

- Businessfinance12 Handout Budget-PreparationDocument5 pagesBusinessfinance12 Handout Budget-PreparationApril Joy De BelenNo ratings yet

- The Use of Budgets in Planning and Decision MakingDocument7 pagesThe Use of Budgets in Planning and Decision MakingKirito UzumakiNo ratings yet

- BudgetDocument5 pagesBudgetmuktaNo ratings yet

- Chapter 9 - Budget PreparationDocument30 pagesChapter 9 - Budget PreparationvdhienNo ratings yet

- MgrawConnect - Chapter 8 Slides - Answer & NotesDocument11 pagesMgrawConnect - Chapter 8 Slides - Answer & NotescNo ratings yet

- CH7 BudgetingDocument51 pagesCH7 BudgetingYMNo ratings yet

- Financial Management 1 - Chapter 16Document6 pagesFinancial Management 1 - Chapter 16lerryroyceNo ratings yet

- Administrative Cost BudgetDocument4 pagesAdministrative Cost BudgetchakriNo ratings yet

- U02 Budget Methodolgies and Budget PreparationDocument26 pagesU02 Budget Methodolgies and Budget PreparationIslam AhmedNo ratings yet

- Individual Assignment 4 - Trần Thị Quỳnh NhiDocument7 pagesIndividual Assignment 4 - Trần Thị Quỳnh NhiTrần Thị Quỳnh NhiNo ratings yet

- Financial Planning Tool and ConceptDocument125 pagesFinancial Planning Tool and ConceptKareen Tapia PublicoNo ratings yet

- 4 - BF - For STUDENTSDocument47 pages4 - BF - For STUDENTSPhill SamonteNo ratings yet

- Chapter-Two: Financial Planning and ProjectionDocument6 pagesChapter-Two: Financial Planning and Projectionমেহেদী হাসানNo ratings yet

- Budget Matterial For The Students NewDocument10 pagesBudget Matterial For The Students NewheysemNo ratings yet

- Group Iii. Business FinanceDocument11 pagesGroup Iii. Business FinanceChristian PhilipNo ratings yet

- Budgeting Planning and ControlDocument31 pagesBudgeting Planning and Controlintan agustina100% (1)

- CHAPTER 3 Financial PlanningDocument7 pagesCHAPTER 3 Financial Planningflorabel parana0% (1)

- Master BudgetDocument6 pagesMaster BudgetPacir QubeNo ratings yet

- Chapter Two The Master BudgetDocument49 pagesChapter Two The Master BudgetGutu Usma'ilNo ratings yet

- Illustrative Problem On Master BudgetingDocument13 pagesIllustrative Problem On Master BudgetingSumendra Shrestha84% (19)

- Teodoro M. Luansing College of Rosario: Senior High School DepartmentDocument7 pagesTeodoro M. Luansing College of Rosario: Senior High School DepartmentSamantha Alice LysanderNo ratings yet

- 8 Comprehensive Examination: Case # 1Document3 pages8 Comprehensive Examination: Case # 1Sajid AliNo ratings yet

- Cost and Management Accounting IIDocument9 pagesCost and Management Accounting IIarefayne wodajoNo ratings yet

- Chapter 4A Financial Planning ManagementDocument20 pagesChapter 4A Financial Planning ManagementAlexa RomarateNo ratings yet

- BUSFIN 6a FINACIAL PLANNING TOOLS AND CONCEPTDocument14 pagesBUSFIN 6a FINACIAL PLANNING TOOLS AND CONCEPTRenz AbadNo ratings yet

- Budgeting Chp9Document30 pagesBudgeting Chp9alp_ganNo ratings yet

- Budgeting 101: By: Limheya Lester Glenn National University-ManilaDocument42 pagesBudgeting 101: By: Limheya Lester Glenn National University-ManilaXXXXXXXXXXXXXXXXXXNo ratings yet

- Chapter 6Document13 pagesChapter 6yana kiutNo ratings yet

- Chapter 9 Profit PlanningDocument3 pagesChapter 9 Profit Planningahmed arfanNo ratings yet

- Study Material of FMDocument22 pagesStudy Material of FMPrakhar SahuNo ratings yet

- Advanced Financial MGMT Notes 1 To 30Document87 pagesAdvanced Financial MGMT Notes 1 To 30Sangeetha K SNo ratings yet

- Chapter 9 Profit PlanningDocument3 pagesChapter 9 Profit Planningahmed arfanNo ratings yet

- Lesson 4 Part 1 Budget PreparationDocument19 pagesLesson 4 Part 1 Budget PreparationmariannedakilaNo ratings yet

- 5PM FinancialAnlysDocument4 pages5PM FinancialAnlysAmba GeetanjaliNo ratings yet

- FM II - Chapter 03, Financial Planning & ForecastingDocument28 pagesFM II - Chapter 03, Financial Planning & ForecastingHace Adis100% (1)

- BudgetingDocument4 pagesBudgetingshielamaelbaisacNo ratings yet

- Module 3 BudgetingDocument8 pagesModule 3 BudgetingMon RamNo ratings yet

- Chapter 9 Review - UpdatedDocument10 pagesChapter 9 Review - UpdatedTamerat FikaduNo ratings yet

- Financial Planning and BudgetingDocument33 pagesFinancial Planning and Budgetingsalonzonicole04No ratings yet

- Budgeting Without AnswersDocument5 pagesBudgeting Without AnswersHertz Dasmariñas GappiNo ratings yet

- Master BudgetDocument15 pagesMaster BudgetHaider AliNo ratings yet

- Business FinanceDocument22 pagesBusiness FinancenattoykoNo ratings yet

- Financial Planning and BudgetingDocument45 pagesFinancial Planning and BudgetingRafael BensigNo ratings yet

- Ch.13 Managing Small Business FinanceDocument5 pagesCh.13 Managing Small Business FinanceBaesick MoviesNo ratings yet

- Lecture Notes On Financial ForecastingDocument7 pagesLecture Notes On Financial Forecastingpalkee100% (3)

- Master BudgetDocument6 pagesMaster BudgetPia LustreNo ratings yet

- Chapter 5 - Strategy and Master BudgetDocument8 pagesChapter 5 - Strategy and Master BudgetNelsie PinedaNo ratings yet

- Business Finance Notes 4thDocument10 pagesBusiness Finance Notes 4thGrobotan LuchiNo ratings yet

- The Importance of Budgets in Financial Planning ClassDocument33 pagesThe Importance of Budgets in Financial Planning ClassMonkey2111No ratings yet

- Midterm Topic 4.1 - Notes - Sales Budgets and Production BudgetsDocument2 pagesMidterm Topic 4.1 - Notes - Sales Budgets and Production BudgetslanoyjessicaellahNo ratings yet

- Budgeting: A Group PresentationDocument43 pagesBudgeting: A Group PresentationSaud Khan WazirNo ratings yet

- Set 2 - Kinematics IIDocument29 pagesSet 2 - Kinematics IILizbethHazelRiveraNo ratings yet

- Lesson 3B - Combinations of FunctionsDocument33 pagesLesson 3B - Combinations of FunctionsLizbethHazelRiveraNo ratings yet

- Time Value of A MoneyDocument23 pagesTime Value of A MoneyLizbethHazelRiveraNo ratings yet

- Bus FinanceDocument13 pagesBus FinanceLizbethHazelRiveraNo ratings yet

- Functions Composite Inverse Forming DemonstrationDocument16 pagesFunctions Composite Inverse Forming DemonstrationLizbethHazelRiveraNo ratings yet

- 01 Financial SystemDocument13 pages01 Financial SystemLizbethHazelRiveraNo ratings yet

- The Firm and Its EnvironmentDocument25 pagesThe Firm and Its EnvironmentLizbethHazelRiveraNo ratings yet

- Business Finance FIDPDocument8 pagesBusiness Finance FIDPLizbethHazelRivera100% (1)

- 01 Introduction To Business FinanceDocument33 pages01 Introduction To Business FinanceLizbethHazelRiveraNo ratings yet

- PlanningsDocument25 pagesPlanningsLizbethHazelRiveraNo ratings yet

- Lesson 1 - Part IIIDocument10 pagesLesson 1 - Part IIILizbethHazelRiveraNo ratings yet

- Lesson 3Document25 pagesLesson 3LizbethHazelRiveraNo ratings yet

- Lesson 2Document23 pagesLesson 2LizbethHazelRiveraNo ratings yet

- Lesson 1 - Part IDocument25 pagesLesson 1 - Part ILizbethHazelRiveraNo ratings yet

- Lesson 1 - Part IiDocument24 pagesLesson 1 - Part IiLizbethHazelRiveraNo ratings yet

- ROI of ElearningDocument18 pagesROI of Elearningnhzaidi100% (1)

- North Dakota State University: Policy ManualDocument6 pagesNorth Dakota State University: Policy ManualTarikua TesfaNo ratings yet

- Toyota Custom ERP System Case Study SumatoSoftDocument2 pagesToyota Custom ERP System Case Study SumatoSoftnishanth4313No ratings yet

- LECT # 1 - Intro To Cost & Mang AccountingDocument28 pagesLECT # 1 - Intro To Cost & Mang Accountingmuhammad.16483.acNo ratings yet

- Scope and Limitation - Printing SystemDocument1 pageScope and Limitation - Printing SystemIvan Bendiola100% (3)

- F 2 HVZL5 TKQ1 ZGejtDocument3 pagesF 2 HVZL5 TKQ1 ZGejtmark3d printersNo ratings yet

- Chapter 4 - Consolidated Financial Statements and Outside OwnershipDocument25 pagesChapter 4 - Consolidated Financial Statements and Outside OwnershipBLe BerNo ratings yet

- Filed Dakota Patriot PAC 2022 Year EndDocument3 pagesFiled Dakota Patriot PAC 2022 Year EndRob Port100% (1)

- Elasticity and Tax IncidenceDocument11 pagesElasticity and Tax IncidenceKiara RamdhawNo ratings yet

- Bworld Ecoforum 2022Document6 pagesBworld Ecoforum 2022Ralph MontejoNo ratings yet

- Partnership LiquidationDocument10 pagesPartnership LiquidationchristineNo ratings yet

- BA Outline ChecklistDocument44 pagesBA Outline ChecklisttomNo ratings yet

- CH (10) - Book AnswersDocument17 pagesCH (10) - Book AnswersabdulraufdghaybeejNo ratings yet

- Bond and Bond Features and Its Example AssignmentDocument4 pagesBond and Bond Features and Its Example AssignmentWaqaarNo ratings yet

- LatikDocument6 pagesLatikkpk8xnwmfgNo ratings yet

- T26 026 902 PDFDocument7 pagesT26 026 902 PDFBenNo ratings yet

- Standards Australia Case Study Oil GasDocument1 pageStandards Australia Case Study Oil GasJohn cenaNo ratings yet

- MTR Form PDFDocument2 pagesMTR Form PDFUstazFaizalAriffinOriginalNo ratings yet

- Emil Remigio Resume-2Document2 pagesEmil Remigio Resume-2api-509061708No ratings yet

- Sales and Distribution Channel of ITC SADocument12 pagesSales and Distribution Channel of ITC SAPranav ManghatNo ratings yet

- Math 12 ABM Org - MGT Q2-Week 6Document14 pagesMath 12 ABM Org - MGT Q2-Week 6Charlene BorladoNo ratings yet

- POPULAR INDUSTRIES LIMITED V EASTERN GARMENT MANUFACTURING SDN BHD, (1989) 3 MLJ 360Document14 pagesPOPULAR INDUSTRIES LIMITED V EASTERN GARMENT MANUFACTURING SDN BHD, (1989) 3 MLJ 360nurulashikin mursid0% (1)

- Form 1 Math AssignmentDocument4 pagesForm 1 Math Assignmentomimarc6No ratings yet

- Stop Smoking ConsultingDocument16 pagesStop Smoking ConsultingKazim AdilNo ratings yet

- Wa0008.Document2 pagesWa0008.Robert DowneyNo ratings yet

- Best Practice For Refinery FlowsheetsDocument6 pagesBest Practice For Refinery Flowsheetskhaled_behery9934No ratings yet