Download as pptx, pdf, or txt

You might also like

- A STUDY On Financial Literacy Among Youths in MumbaiDocument57 pagesA STUDY On Financial Literacy Among Youths in Mumbaibhanushalidhruv590% (1)

- Nmims Final Report123 PDFDocument46 pagesNmims Final Report123 PDFHimanshu KhandelwalNo ratings yet

- Nmims Final Report123 PDFDocument46 pagesNmims Final Report123 PDFHimanshu KhandelwalNo ratings yet

- Raghu Steel Pipes Accoutancy Projects PDFDocument23 pagesRaghu Steel Pipes Accoutancy Projects PDFRachit Jain73% (48)

- Ey Educate To EmpowerDocument52 pagesEy Educate To Empowersidthefreak809No ratings yet

- Research Paper On Financial InclusionDocument36 pagesResearch Paper On Financial Inclusionimsarfrazkhan96% (28)

- Finance ProjectDocument6 pagesFinance ProjectPradeep Mib2022No ratings yet

- Finacial LiterncyDocument48 pagesFinacial LiterncyKiranNo ratings yet

- Black BookDocument23 pagesBlack BookRISHABH KHANDELWALNo ratings yet

- Fs - Financial InclusionDocument7 pagesFs - Financial InclusionWasim SNo ratings yet

- Towards Digital and Financial Literacy (November-2019)Document5 pagesTowards Digital and Financial Literacy (November-2019)Periyasamy KalaivananNo ratings yet

- A Study On Financial Literacy of Women in Hyderabad City (Telangana)Document9 pagesA Study On Financial Literacy of Women in Hyderabad City (Telangana)Editor IJTSRDNo ratings yet

- Kushagra Amrit 1882053Document16 pagesKushagra Amrit 1882053Kushagra AmritNo ratings yet

- V Idhi: Business PlanDocument11 pagesV Idhi: Business PlanShivika MittalNo ratings yet

- Financial Inclusion in India: A Theoritical Assesment: ManagementDocument6 pagesFinancial Inclusion in India: A Theoritical Assesment: ManagementVidhi BansalNo ratings yet

- Research Paper On Financial InclusionDocument57 pagesResearch Paper On Financial InclusionChilaka Pappala0% (1)

- Financial Literacy in India - A New Way ForwardDocument15 pagesFinancial Literacy in India - A New Way Forwardaditya sahooNo ratings yet

- Research Paper On Financial Inclusion in IndiaDocument8 pagesResearch Paper On Financial Inclusion in Indiajicjtjxgf100% (1)

- A Study On Awareness Towards Financial Inclusion Among Rural Areas With Special Reference To CoimbatoreDocument27 pagesA Study On Awareness Towards Financial Inclusion Among Rural Areas With Special Reference To CoimbatoreprathikshaNo ratings yet

- Manage-A Study of Financial Literacy Among Micro-Kama Gupta - 1Document8 pagesManage-A Study of Financial Literacy Among Micro-Kama Gupta - 1Impact JournalsNo ratings yet

- Financial Inclusion in India: An Analysis: Dr. Anurag B. Singh, Priyanka TandonDocument14 pagesFinancial Inclusion in India: An Analysis: Dr. Anurag B. Singh, Priyanka TandonVidhi BansalNo ratings yet

- Research Paper On Microfinance in India PDFDocument8 pagesResearch Paper On Microfinance in India PDFegya6qzc100% (1)

- Financial Literacy Improvement Strategies in Supporting Financial Inclusion Policy in Gorontalo DistrictDocument11 pagesFinancial Literacy Improvement Strategies in Supporting Financial Inclusion Policy in Gorontalo DistrictInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Comparative Analysis of Important Insurance Schemes of Public and Private Life InsurersDocument8 pagesComparative Analysis of Important Insurance Schemes of Public and Private Life Insurersshashikumarb2277No ratings yet

- Fin. LiteracyDocument9 pagesFin. LiteracyX YNo ratings yet

- Charting A Course To Prosperity: The Importance of Financial LiteracyDocument7 pagesCharting A Course To Prosperity: The Importance of Financial LiteracySubodh BansalNo ratings yet

- r140128c PDFDocument3 pagesr140128c PDFmunawar abbasNo ratings yet

- What Is Financial Inclusion?: Providing Formal Credit AvenuesDocument5 pagesWhat Is Financial Inclusion?: Providing Formal Credit AvenuesRahul WaniNo ratings yet

- PRT 2Document54 pagesPRT 2muhammad.salman100No ratings yet

- Need For Financial Inclusion and Challenges Ahead - An Indian PerspectiveDocument4 pagesNeed For Financial Inclusion and Challenges Ahead - An Indian PerspectiveInternational Organization of Scientific Research (IOSR)No ratings yet

- Smu Project ReportDocument78 pagesSmu Project ReportAbhishek AnandNo ratings yet

- Finacial Inclusion and ExclusionDocument20 pagesFinacial Inclusion and Exclusionbeena antuNo ratings yet

- Enhancing Islamic Financial Literacy in Indonesian Youth Generates Broader Societal BenefitsDocument14 pagesEnhancing Islamic Financial Literacy in Indonesian Youth Generates Broader Societal BenefitsGlobal Research and Development ServicesNo ratings yet

- 4-MM 4C-Financial InclusionDocument24 pages4-MM 4C-Financial Inclusionsenthamarai krishnanNo ratings yet

- Financial Inclusion: A Road India Needs To TravelDocument40 pagesFinancial Inclusion: A Road India Needs To TravelGourav PattnaikNo ratings yet

- Micro Finance: Opportunities AheadDocument3 pagesMicro Finance: Opportunities AheadProf S P GargNo ratings yet

- September 2020 NewsletterDocument30 pagesSeptember 2020 NewsletterAnonymous FnM14a0No ratings yet

- Financial Inclusion in India-An Overview: R. Kedaranatha SwamyDocument6 pagesFinancial Inclusion in India-An Overview: R. Kedaranatha SwamyTJPRC PublicationsNo ratings yet

- Financial Inclusion in India-13 PagesDocument14 pagesFinancial Inclusion in India-13 Pagessree anugraphicsNo ratings yet

- 1china's Financial Network With International Spillovers: A First LookDocument2 pages1china's Financial Network With International Spillovers: A First LookMohammad Adil ChoudharyNo ratings yet

- 1china's Financial Network With International Spillovers: A First LookDocument2 pages1china's Financial Network With International Spillovers: A First LookMohammad Adil ChoudharyNo ratings yet

- Improving Financial Literacy Through Teaching Materials On Managing Finance For MillennialsDocument5 pagesImproving Financial Literacy Through Teaching Materials On Managing Finance For MillennialsshandrinelobatonNo ratings yet

- Financial InclusionDocument3 pagesFinancial Inclusionapi-3701467No ratings yet

- Analysis of MSME Players' Financial Literacy in Payakumbuh CityDocument7 pagesAnalysis of MSME Players' Financial Literacy in Payakumbuh CityNurul Izzah FauziyahNo ratings yet

- Financial Inclusion 4Document6 pagesFinancial Inclusion 445satishNo ratings yet

- Financial Inclusion - RBI - S InitiativesDocument12 pagesFinancial Inclusion - RBI - S Initiativessahil_saini298No ratings yet

- Financial Inclusion in India Research Paper PDFDocument8 pagesFinancial Inclusion in India Research Paper PDFaflbtjglu100% (1)

- Jurnal Economica Equivalence of Islamic Financial LiteracyDocument28 pagesJurnal Economica Equivalence of Islamic Financial LiteracyMiftakhul KhasanahNo ratings yet

- Financial InclusionDocument3 pagesFinancial Inclusionputul6No ratings yet

- Edited MicrofinanceDocument59 pagesEdited Microfinancedarthvader005No ratings yet

- Alok Mba Mini ProjectDocument50 pagesAlok Mba Mini ProjectAlok JhaNo ratings yet

- SH As TriDocument5 pagesSH As TriRaqueem KhanNo ratings yet

- HCIDocument77 pagesHCIArvind Sanu MisraNo ratings yet

- How To Make India A Financially Literate Country1Document6 pagesHow To Make India A Financially Literate Country1geet666No ratings yet

- RMFLS 2022 Survey Report FINALDocument23 pagesRMFLS 2022 Survey Report FINALMeng Chuan NgNo ratings yet

- Strategy and Efforts of A Public Sector Bank For Financial InclusionDocument10 pagesStrategy and Efforts of A Public Sector Bank For Financial InclusionKhushi PuriNo ratings yet

- Perspective of Technology in Achieving Financial Inclusion in Rural IndiaDocument9 pagesPerspective of Technology in Achieving Financial Inclusion in Rural IndiaHebaeid200gmail.com New13newNo ratings yet

- Financial InclusionDocument15 pagesFinancial InclusionNitin SharmaNo ratings yet

- Research Paper Financial InclusionDocument6 pagesResearch Paper Financial Inclusionlsfxofrif100% (1)

- Mastering Your Financial Future: A Comprehensive Guide for Gen ZFrom EverandMastering Your Financial Future: A Comprehensive Guide for Gen ZNo ratings yet

- Incubating Indonesia’s Young Entrepreneurs:: Recommendations for Improving Development ProgramsFrom EverandIncubating Indonesia’s Young Entrepreneurs:: Recommendations for Improving Development ProgramsNo ratings yet

- PFRS 3 Business CombinationsDocument34 pagesPFRS 3 Business CombinationseiraNo ratings yet

- CCPSDocument2 pagesCCPSelitevaluation2022No ratings yet

- ISSN: 1520-5509 Clarion University of Pennsylvania, Clarion, PennsylvaniaDocument15 pagesISSN: 1520-5509 Clarion University of Pennsylvania, Clarion, PennsylvaniaShaguolo O. JosephNo ratings yet

- PDF FileDocument15 pagesPDF FileboinnychuttyNo ratings yet

- Money Growth and InflationDocument45 pagesMoney Growth and Inflationguru110No ratings yet

- Chapter One 1.1 Background To The StudyDocument34 pagesChapter One 1.1 Background To The StudyA Chat With AlexNo ratings yet

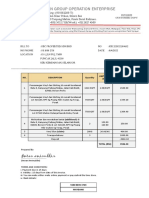

- Ilan Group Operation Enterprise: Imran AminuddinDocument1 pageIlan Group Operation Enterprise: Imran AminuddinIzhar AminuddinNo ratings yet

- HTCROUSARKOTHIpdfDocument102 pagesHTCROUSARKOTHIpdfRahul RawatNo ratings yet

- Journal of Asiatic Society of MumbaiDocument11 pagesJournal of Asiatic Society of MumbaiAbhiNo ratings yet

- Sample - Period Panties Market Report, 2032Document40 pagesSample - Period Panties Market Report, 2032Tu NguyenNo ratings yet

- (Booz Allen Hamilton) The M&a Collar Handbook - How To Manage Equity RiskDocument15 pages(Booz Allen Hamilton) The M&a Collar Handbook - How To Manage Equity RiskanuragNo ratings yet

- Tariff CodeDocument39 pagesTariff CodeAlexPamintuanAbitanNo ratings yet

- The Enterprising Communities and Startup Ecosystem in Iran: Aidin Salamzadeh Hiroko Kawamorita KesimDocument24 pagesThe Enterprising Communities and Startup Ecosystem in Iran: Aidin Salamzadeh Hiroko Kawamorita Kesimpriyankabatra.nicmNo ratings yet

- VCS Program Guide v4.2Document24 pagesVCS Program Guide v4.2Miranti ArianiNo ratings yet

- Licensed Clearing Agents 2006-7 UgandaDocument8 pagesLicensed Clearing Agents 2006-7 UgandaKintu Munabangogo100% (1)

- Changing Profile of Indian ConsumerDocument29 pagesChanging Profile of Indian ConsumerSridhar_Sunchu_8095100% (1)

- Inv 000004Document1 pageInv 000004Ajit GolchhaNo ratings yet

- Ms. Tasneem Bareen HasanDocument13 pagesMs. Tasneem Bareen HasanMahin TabassumNo ratings yet

- Horticulture in EthiopiaDocument7 pagesHorticulture in EthiopiaYoseph WubetNo ratings yet

- Chapter 7 - Rural - Urban MigrationDocument44 pagesChapter 7 - Rural - Urban MigrationKenzel lawasNo ratings yet

- PM (Partial Presentation)Document110 pagesPM (Partial Presentation)sampadaNo ratings yet

- Chapter-4: ConsiderationDocument18 pagesChapter-4: ConsiderationMd. Shadman Sakib 1610973630No ratings yet

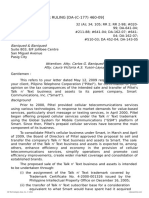

- Bir Ruling (Da - (C-177) 460-09)Document8 pagesBir Ruling (Da - (C-177) 460-09)Jayvee CayabyabNo ratings yet

- Analisis Strategi Bisnis Usaha Mikro Kecil Dan Menengah (UMKM) Dalam Pengembangan Usaha UD. Mete Mubaraq Lombe Kota KendariDocument12 pagesAnalisis Strategi Bisnis Usaha Mikro Kecil Dan Menengah (UMKM) Dalam Pengembangan Usaha UD. Mete Mubaraq Lombe Kota KendariPutri 123No ratings yet

- KPI For LeanDocument3 pagesKPI For LeanSudev NairNo ratings yet

- Mid Term IBFDocument40 pagesMid Term IBFQuỳnh Lê DiễmNo ratings yet

- Practical Examination Max. Marks: 30 Time: 1.0 HR: Agricultural Marketing and Price Analysis (AGECON-505)Document2 pagesPractical Examination Max. Marks: 30 Time: 1.0 HR: Agricultural Marketing and Price Analysis (AGECON-505)sumitNo ratings yet

- Intro Red Co ZZZZDocument3 pagesIntro Red Co ZZZZTutii FarutiNo ratings yet

- Farmer's RightsDocument17 pagesFarmer's RightsAlexandra Lee AbanteNo ratings yet