Download as pptx, pdf, or txt

You might also like

- Gulfood Exhibitor List M 2Document19 pagesGulfood Exhibitor List M 2Lupu CarmenNo ratings yet

- Corporate Identity & Graphics Standards Manual: External VersionDocument19 pagesCorporate Identity & Graphics Standards Manual: External VersionEdgar Alan Garduño PadillaNo ratings yet

- Costing ModuleDocument7 pagesCosting ModuleJoneric RamosNo ratings yet

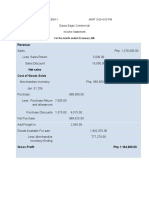

- Financial StatementsDocument8 pagesFinancial StatementsJohn Carldel VivoNo ratings yet

- PFRS 9 &PAS 32 Financial Instrument: Conceptual Framework and Reporting StandardDocument7 pagesPFRS 9 &PAS 32 Financial Instrument: Conceptual Framework and Reporting StandardMeg sharkNo ratings yet

- Overview of Er and Rea ApproachDocument7 pagesOverview of Er and Rea ApproachTEph App100% (3)

- FAR - Midterms and FinalsDocument14 pagesFAR - Midterms and FinalsShanley Vanna EscalonaNo ratings yet

- AIS 01 - Handout - 1Document7 pagesAIS 01 - Handout - 1Melchie RepospoloNo ratings yet

- Chapter 17 and 18 - Investment in Associates What Is An Associate? Accounting Procedures of Investment in AssociateDocument2 pagesChapter 17 and 18 - Investment in Associates What Is An Associate? Accounting Procedures of Investment in AssociateRanee DeeNo ratings yet

- Davao - Eagle - Com JOSEPHDocument6 pagesDavao - Eagle - Com JOSEPHablay logeneNo ratings yet

- 11 - Bank Reconciliation NotesDocument3 pages11 - Bank Reconciliation NotesJann GataNo ratings yet

- Accounting RefresherDocument2 pagesAccounting RefresherAlbert MorenoNo ratings yet

- FinMan (Common-Size Analysis)Document4 pagesFinMan (Common-Size Analysis)Lorren Graze RamiroNo ratings yet

- Module For ACC 206 Understanding ExpensesDocument12 pagesModule For ACC 206 Understanding ExpensesMerecci Angela De ChavezNo ratings yet

- Finals Non Graded Exercises 002 - Journalizing Under Mechandising Concern With Vat Page 28Document6 pagesFinals Non Graded Exercises 002 - Journalizing Under Mechandising Concern With Vat Page 28Garpt KudasaiNo ratings yet

- ACCTG 124 Chapter 7Document5 pagesACCTG 124 Chapter 7John Vincent A DioNo ratings yet

- Partnership FormationDocument3 pagesPartnership Formationmiss independent100% (1)

- Cost Accounting CycleDocument8 pagesCost Accounting CycleRosiel Mae CadungogNo ratings yet

- Chapter 2 Cost AcctngDocument10 pagesChapter 2 Cost AcctngJustine Reine CornicoNo ratings yet

- Chapter 5Document19 pagesChapter 5Rochelle Esquivel ManaloNo ratings yet

- Corporate Reporting Manual Part 2 - Up To 2018Document774 pagesCorporate Reporting Manual Part 2 - Up To 2018Masum GaziNo ratings yet

- Actual Costing Illustrative ProblemDocument5 pagesActual Costing Illustrative ProblemJuan Dela CruzNo ratings yet

- CF04 Part 3 - Petty Cash FundDocument51 pagesCF04 Part 3 - Petty Cash FundABMAYALADANO ,ErvinNo ratings yet

- Quiz 2 Cost AccountingDocument1 pageQuiz 2 Cost AccountingRocel DomingoNo ratings yet

- Acct-111e - Quiz CompDocument18 pagesAcct-111e - Quiz CompJap Keren LirazanNo ratings yet

- Chapter 7Document18 pagesChapter 7Raven Vargas DayritNo ratings yet

- RFBT03 17 Revised Corporation Code of The PhilippinesDocument115 pagesRFBT03 17 Revised Corporation Code of The PhilippinesKrissy PepsNo ratings yet

- Mwehehe May Sagot 2Document7 pagesMwehehe May Sagot 2Lizzeille Anne Amor MacalintalNo ratings yet

- Exercises in MerchandisingDocument10 pagesExercises in MerchandisingJhon Robert BelandoNo ratings yet

- Beg. Balance Sales Journal Voucher Registry Check Register Cash Receipt Account TitleDocument12 pagesBeg. Balance Sales Journal Voucher Registry Check Register Cash Receipt Account TitleFred WilsonNo ratings yet

- Accounting Concepts and PrinciplesDocument4 pagesAccounting Concepts and Principlesdane alvarezNo ratings yet

- Intacc 3 HWDocument7 pagesIntacc 3 HWMelissa Kayla ManiulitNo ratings yet

- Sec Code of Corporate Governance AnswerDocument3 pagesSec Code of Corporate Governance AnswerHechel DatinguinooNo ratings yet

- (Academic Review and Training School, Inc.) 2F & 3F Crème BLDG., Abella ST., Naga City Tel No.: (054) 472-9104 E-Mail: - Inventory (Pas 2)Document10 pages(Academic Review and Training School, Inc.) 2F & 3F Crème BLDG., Abella ST., Naga City Tel No.: (054) 472-9104 E-Mail: - Inventory (Pas 2)Snow TurnerNo ratings yet

- Accounting MaterialsDocument20 pagesAccounting MaterialsBhoxzs Mel Ikaw LngNo ratings yet

- Seatwork 10.6.21Document6 pagesSeatwork 10.6.21Ashley MarloweNo ratings yet

- Jedah Noel - ASSIGNMENT 1 - Partnership FormationDocument2 pagesJedah Noel - ASSIGNMENT 1 - Partnership FormationJeddieh NoelNo ratings yet

- Variable and Absorption CostingDocument2 pagesVariable and Absorption CostingLaura OliviaNo ratings yet

- Worksheet On Accounting For Merchandising OperationDocument11 pagesWorksheet On Accounting For Merchandising Operationbereket nigussieNo ratings yet

- CFAS Questions Chaps 1 and 2Document13 pagesCFAS Questions Chaps 1 and 2King SigueNo ratings yet

- 2019 Vol 1 CH 1 AnswersDocument17 pages2019 Vol 1 CH 1 AnswersTatangNo ratings yet

- Pas 8Document3 pagesPas 8Sacedon, Trishia Mae C.No ratings yet

- Accounting Analyzing Business Transaction ReviewerDocument7 pagesAccounting Analyzing Business Transaction Reviewerandreajade.cawaya10No ratings yet

- October To September Sales Report Movies by GenreDocument3 pagesOctober To September Sales Report Movies by GenreAngelica Austria-MantalNo ratings yet

- Term Exam Essay PartDocument1 pageTerm Exam Essay PartCristine Jewel CorpuzNo ratings yet

- PARCORDocument5 pagesPARCORjelai anselmoNo ratings yet

- Investment Property Is Defined As Property (Land and Building of Part of A Building or Both) HeldDocument11 pagesInvestment Property Is Defined As Property (Land and Building of Part of A Building or Both) HeldRNo ratings yet

- Inter-Acct1Document6 pagesInter-Acct1.No ratings yet

- Chapter 7 Acctng For Materials Activity PDFDocument3 pagesChapter 7 Acctng For Materials Activity PDFGwyneth Hannah Sator RupacNo ratings yet

- What Is The Difference Between An Adjunct Account and A Contra AccountDocument1 pageWhat Is The Difference Between An Adjunct Account and A Contra AccountDarlene SarcinoNo ratings yet

- Worksheet Problem #5Document104 pagesWorksheet Problem #5Gutierrez Ronalyn Y.No ratings yet

- Las 6Document4 pagesLas 6Venus Abarico Banque-AbenionNo ratings yet

- Answer Key - M1L4 PDFDocument4 pagesAnswer Key - M1L4 PDFEricka Mher IsletaNo ratings yet

- Problem 4-9 Requirement 1 (Journal Entries) : Accounts Receivable 950,000 3,150,000Document5 pagesProblem 4-9 Requirement 1 (Journal Entries) : Accounts Receivable 950,000 3,150,000John SenaNo ratings yet

- Unadjusted Trial BalanceDocument4 pagesUnadjusted Trial BalanceJemma Rose BagalacsaNo ratings yet

- Review Materials in Cost AccountingDocument10 pagesReview Materials in Cost AccountingCARMELITA CUETONo ratings yet

- Conceptual Framework and Accounting Standards - Chapter 2 - NotesDocument5 pagesConceptual Framework and Accounting Standards - Chapter 2 - NotesKhey KheyNo ratings yet

- Bart MDocument3 pagesBart MSteph Borinaga0% (1)

- First Time Adoption of PFRSDocument5 pagesFirst Time Adoption of PFRSPia ArellanoNo ratings yet

- Ch8 HKAS16Document29 pagesCh8 HKAS16jaberalislamNo ratings yet

- Chapter 1 Property Plant and EquipmentDocument26 pagesChapter 1 Property Plant and EquipmentJellai TejeroNo ratings yet

- ARDF DF3090 (D779-17) Parts CatalogDocument26 pagesARDF DF3090 (D779-17) Parts CatalogmaxmaracatuNo ratings yet

- Ashish Krishnankutty - 10727 - R - Indian Register of ShippingDocument2 pagesAshish Krishnankutty - 10727 - R - Indian Register of ShippingAshish KrishnankuttyNo ratings yet

- Supply Chain ManagementDocument15 pagesSupply Chain ManagementMadhan KumarNo ratings yet

- Haake PDFDocument26 pagesHaake PDFSimão PintoNo ratings yet

- Urbanization and Risk - Challenges and OpportunitiesDocument6 pagesUrbanization and Risk - Challenges and OpportunitiesMarien BañezNo ratings yet

- ABS Warning Light CircuitDocument2 pagesABS Warning Light CircuitErln LimaNo ratings yet

- Final Constant Maturity Swap CappedDocument2 pagesFinal Constant Maturity Swap CappedLeo YamauchiNo ratings yet

- Phpmyadmin Web Application Security AssessmentDocument16 pagesPhpmyadmin Web Application Security AssessmentybNo ratings yet

- Company Profile Monjil PrivateDocument2 pagesCompany Profile Monjil PrivateYousuf MunniNo ratings yet

- Scaffolding and Centering ChargesDocument1 pageScaffolding and Centering ChargesdeepakNo ratings yet

- Exploring The Real Life Applications of Taylors TheoremDocument26 pagesExploring The Real Life Applications of Taylors TheorempaheldharodNo ratings yet

- Iat-4 McesDocument12 pagesIat-4 Mcesbhatt bhattNo ratings yet

- Proposed Construction of Swimming Pool Beside Vinayak Sagar Under Implementation of Smart City Mission in TirupatiDocument54 pagesProposed Construction of Swimming Pool Beside Vinayak Sagar Under Implementation of Smart City Mission in TirupatiaaaNo ratings yet

- Advertisement - UPPSCDocument10 pagesAdvertisement - UPPSCHimanshu MauryaNo ratings yet

- CA Assignment QuestionsDocument7 pagesCA Assignment QuestionsShagunNo ratings yet

- Design and Implementations of Control System Quadruped Robot Driver Application Based On Windows PlatformDocument8 pagesDesign and Implementations of Control System Quadruped Robot Driver Application Based On Windows Platformpuskesmas III denpasar utaraNo ratings yet

- G.R. No. 178713 LORENZO SHIPPING CORPORATION, Petitioner, vs. FLORENCIO O. VILLARINDocument4 pagesG.R. No. 178713 LORENZO SHIPPING CORPORATION, Petitioner, vs. FLORENCIO O. VILLARINMark VirayNo ratings yet

- DFT TopicsDocument3 pagesDFT TopicsRedouaneTahraouiNo ratings yet

- Private Label Sourcing For: Lessons, Mistakes and StrategiesDocument15 pagesPrivate Label Sourcing For: Lessons, Mistakes and StrategiesДенис АкуляковNo ratings yet

- Oisd STD 118Document31 pagesOisd STD 118rajwadi50% (2)

- Cryptography Session 2020 v1Document98 pagesCryptography Session 2020 v1GlmNo ratings yet

- Sonus Faber Olympica III Loudspeakers Review Test LoresDocument6 pagesSonus Faber Olympica III Loudspeakers Review Test LoresMilan TrengovskiNo ratings yet

- ITC Arise Plus Philippines - Ecosystem Mapping Report - Pre-Validation - FinalDocument60 pagesITC Arise Plus Philippines - Ecosystem Mapping Report - Pre-Validation - FinalCarlos JesenaNo ratings yet

- Engineering Mechanics Mech-A 2021-22 Assignment-IIDocument32 pagesEngineering Mechanics Mech-A 2021-22 Assignment-IIunachieved FilmsNo ratings yet

- Socleg 66 CasesDocument303 pagesSocleg 66 CasesKen LimNo ratings yet

- Proof of Residency TemplateDocument1 pageProof of Residency Templateshelley lovellNo ratings yet

- Trainning ReportDocument81 pagesTrainning ReportRohan PandeNo ratings yet