Curency Derivatives - Forwards, Futures, Forward Rate Agreement, Options, Swaps - Foreign Exchange Management Act

Curency Derivatives - Forwards, Futures, Forward Rate Agreement, Options, Swaps - Foreign Exchange Management Act

You might also like

- Problems Sub-IfDocument11 pagesProblems Sub-IfChintakunta PreethiNo ratings yet

- WAC On Kodak: The Rebirth of An Iconic Brand Case StudyDocument7 pagesWAC On Kodak: The Rebirth of An Iconic Brand Case Studyritam chakrabortyNo ratings yet

- Introduction To Currency DerivativesDocument12 pagesIntroduction To Currency Derivativesquadeer791No ratings yet

- CAPMDocument12 pagesCAPMAkash TiwariNo ratings yet

- JETBLUE CaseDocument33 pagesJETBLUE CaseMarcellia Crenata100% (1)

- Derivatives - Unit 3 (Autosaved)Document54 pagesDerivatives - Unit 3 (Autosaved)learnerme129No ratings yet

- Currency Future DerivativesDocument18 pagesCurrency Future DerivativesrudraNo ratings yet

- Derivativesmarket 111006143752 Phpapp02Document21 pagesDerivativesmarket 111006143752 Phpapp02sejalahir30_40759023No ratings yet

- FRGN Curr Derivatives - FandO Os1qImUSkGDocument50 pagesFRGN Curr Derivatives - FandO Os1qImUSkGNikitha NithyanandhamNo ratings yet

- Frm2 Derivatives BasicsDocument34 pagesFrm2 Derivatives BasicsDîvýâñshü MâhâwârNo ratings yet

- What Is Currency DerivativeDocument16 pagesWhat Is Currency DerivativeShweta RajputNo ratings yet

- Derivatives 1Document91 pagesDerivatives 1sharath haradyNo ratings yet

- Derivative 1Document39 pagesDerivative 1Heera JhaNo ratings yet

- Introduction To Derivatives BasicsDocument34 pagesIntroduction To Derivatives Basicsmihir popatNo ratings yet

- Instruments of Foreign ExchangeDocument14 pagesInstruments of Foreign ExchangeMansi KoliyanNo ratings yet

- Introductory+Notes+on+Derivative+Securities+ (Fall+2009+ +SFR)Document16 pagesIntroductory+Notes+on+Derivative+Securities+ (Fall+2009+ +SFR)M. Khairul IslamNo ratings yet

- Forex Derivatives in India Its Implications - Currency Futures and Its Implications in Forex TradingDocument23 pagesForex Derivatives in India Its Implications - Currency Futures and Its Implications in Forex TradingamansinghaniaiipmNo ratings yet

- Module 2Document41 pagesModule 2bhargaviNo ratings yet

- Currency Futures NivDocument37 pagesCurrency Futures Nivpratibhashetty_87No ratings yet

- Currency Derivatives: by "Me"Document15 pagesCurrency Derivatives: by "Me"Shikhar AroraNo ratings yet

- Derivatives - FinalDocument34 pagesDerivatives - FinalGagan AnandNo ratings yet

- If 4Document79 pagesIf 4Aalfin MariyaNo ratings yet

- Financial Derivatives Assignment IDocument12 pagesFinancial Derivatives Assignment Iamit_harry100% (3)

- BFN 427 Business Scenarios Using Swaps, Options and FuturesDocument68 pagesBFN 427 Business Scenarios Using Swaps, Options and FuturesgeorgeNo ratings yet

- Market For Foreign ExchangeDocument43 pagesMarket For Foreign ExchangeAsha SoniNo ratings yet

- Forex by NageshDocument44 pagesForex by NageshNagesh KumarNo ratings yet

- Lala Lajpatrai College of Commerce & EconomicsDocument26 pagesLala Lajpatrai College of Commerce & EconomicsvorachiragNo ratings yet

- CURR NC FUTUR $ - FinalDocument25 pagesCURR NC FUTUR $ - FinalParidhi KhemkaNo ratings yet

- Currency Futures Market in India: at India Info Line LTD, HyderabadDocument19 pagesCurrency Futures Market in India: at India Info Line LTD, HyderabadSubodh KothariNo ratings yet

- UNIT 3 ForexDocument47 pagesUNIT 3 Forexsaurabh thakurNo ratings yet

- Introduction To DerivativesDocument41 pagesIntroduction To DerivativessmitajNo ratings yet

- Unit - 2Document39 pagesUnit - 2DivyanshuNo ratings yet

- Module 1 - Introduction To DerivativesDocument29 pagesModule 1 - Introduction To DerivativesSunny SinghNo ratings yet

- Derivatives Managing Financial RiskDocument17 pagesDerivatives Managing Financial RiskbaboabNo ratings yet

- Introduction:-: Rate, Such As The Euro To US Dollar Exchange Rate, or The British Pound To US Dollar ExchangeDocument34 pagesIntroduction:-: Rate, Such As The Euro To US Dollar Exchange Rate, or The British Pound To US Dollar Exchangesarabjeet_toriNo ratings yet

- Currency Derivatives Research PaperDocument6 pagesCurrency Derivatives Research Paperpimywinihyj3100% (1)

- FDM (Unit I-V)Document27 pagesFDM (Unit I-V)KathiravanNo ratings yet

- Financial Derivatives Market and Its Development in IndiaDocument6 pagesFinancial Derivatives Market and Its Development in Indiaanshulnatani4uNo ratings yet

- Unit 6 FM IDocument12 pagesUnit 6 FM IJay ༄᭄ShahNo ratings yet

- Role of Financial Futures With Reference To Nse NiftyDocument58 pagesRole of Financial Futures With Reference To Nse NiftyWebsoft Tech-HydNo ratings yet

- UNIT 3 ForexDocument47 pagesUNIT 3 Forexraj kumarNo ratings yet

- Derivatives: A Presentation by Harita Chanda Sneha Rampalli Nilesh KotereDocument15 pagesDerivatives: A Presentation by Harita Chanda Sneha Rampalli Nilesh KotereNilesh KotereNo ratings yet

- Unit One.Document41 pagesUnit One.Manas JainNo ratings yet

- Concepts Relating To Foreign ExchangeDocument89 pagesConcepts Relating To Foreign Exchangedeepakpandeyji2001No ratings yet

- Slide 1Document23 pagesSlide 1Shashika Anuradha KoswaththaNo ratings yet

- Work Sheet 02 - FDDocument4 pagesWork Sheet 02 - FDBhavesh RathiNo ratings yet

- Introduction To Derivatives: By: Nilima DasDocument103 pagesIntroduction To Derivatives: By: Nilima DasDilip ThakurNo ratings yet

- Lecture No. 7 International FinanceDocument31 pagesLecture No. 7 International FinanceNadia MurtazaNo ratings yet

- Financial Futures With Reference To NiftyDocument73 pagesFinancial Futures With Reference To Niftyjitendra jaushik75% (4)

- Unit Vi: Financial Risk ManagementDocument23 pagesUnit Vi: Financial Risk Managementmtechvlsitd labNo ratings yet

- Chap05 Ques MBF14eDocument6 pagesChap05 Ques MBF14eÂn TrầnNo ratings yet

- Financial Derivatives: Naman Jain (3254) Sabbani Maruthi (3276) Pranav Arora (3285) Sambit Ghosh (3286)Document21 pagesFinancial Derivatives: Naman Jain (3254) Sabbani Maruthi (3276) Pranav Arora (3285) Sambit Ghosh (3286)fhv hugNo ratings yet

- Futures and OptionsDocument51 pagesFutures and OptionsRitik VermaniNo ratings yet

- Derivative Markets and Instruments: Module # 6Document10 pagesDerivative Markets and Instruments: Module # 6Apoorv AnandNo ratings yet

- Foreign ExchangeDocument19 pagesForeign ExchangeradhikaNo ratings yet

- Before Commitment Commits You, Commit To The Commitment: Sundar B. N. Assistant Professor Coordinator ofDocument34 pagesBefore Commitment Commits You, Commit To The Commitment: Sundar B. N. Assistant Professor Coordinator ofH B SantoshNo ratings yet

- Currency DerivativesDocument12 pagesCurrency DerivativesNazneen100% (2)

- Futures and OptionsDocument4 pagesFutures and OptionsLucky_boy_87No ratings yet

- Mission RBI 2018 - Financial System: DerivativesDocument21 pagesMission RBI 2018 - Financial System: DerivativesAnonymous kj9KW15CQnNo ratings yet

- FuturesDocument30 pagesFuturessoujee60No ratings yet

- Forex for Beginners: The Most Comprehensive Guide to Making Money in the Forex Market (2022 Crash Course for Newbies)From EverandForex for Beginners: The Most Comprehensive Guide to Making Money in the Forex Market (2022 Crash Course for Newbies)No ratings yet

- Structure of Foreign Exchange Market in India, Exchange Rate Mexchanism-Quotes in Spot Market and Forward MarketDocument7 pagesStructure of Foreign Exchange Market in India, Exchange Rate Mexchanism-Quotes in Spot Market and Forward MarketChintakunta PreethiNo ratings yet

- Unit-Ii Foreign ExchangeDocument55 pagesUnit-Ii Foreign ExchangeChintakunta PreethiNo ratings yet

- International Financial InstrumentsDocument25 pagesInternational Financial InstrumentsChintakunta Preethi100% (1)

- Tarapore Committee ReportDocument14 pagesTarapore Committee ReportChintakunta PreethiNo ratings yet

- Q.8b IF 2019Document7 pagesQ.8b IF 2019Chintakunta PreethiNo ratings yet

- Gold Standard-Bretton Woods Standard 2Document39 pagesGold Standard-Bretton Woods Standard 2Chintakunta PreethiNo ratings yet

- Bop in IndiaDocument54 pagesBop in IndiaChintakunta PreethiNo ratings yet

- Calculation of Forward RateDocument8 pagesCalculation of Forward RateChintakunta PreethiNo ratings yet

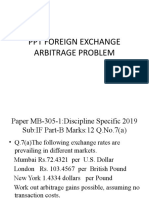

- Foreign Exchange Arbitrage ProblemDocument7 pagesForeign Exchange Arbitrage ProblemChintakunta PreethiNo ratings yet

- International Banking-Euro Bank, Types of Banking Offices, Correspondent Bank, Representative Bank 5Document20 pagesInternational Banking-Euro Bank, Types of Banking Offices, Correspondent Bank, Representative Bank 5Chintakunta PreethiNo ratings yet

- Balance of Payments (Bop)Document29 pagesBalance of Payments (Bop)Chintakunta PreethiNo ratings yet

- Case Study BARGAIN CITYDocument1 pageCase Study BARGAIN CITYValentin KhoNo ratings yet

- Lauren Chen: Career ObjectiveDocument3 pagesLauren Chen: Career ObjectiveJacobNo ratings yet

- PMT 30101Document37 pagesPMT 30101Yousef Adel HassanenNo ratings yet

- Automobile Dealer Sales & Service-Critical IncidentsDocument4 pagesAutomobile Dealer Sales & Service-Critical IncidentsSIDDHARTH BANRANo ratings yet

- Form - Nonconforming Part DispositionDocument1 pageForm - Nonconforming Part DispositionDavidNo ratings yet

- September Month Current AffairsDocument7 pagesSeptember Month Current AffairsGoogle AccountNo ratings yet

- One Stop Centre (Osc) : Lessons On Best Practices in Planning System DeliveryDocument12 pagesOne Stop Centre (Osc) : Lessons On Best Practices in Planning System DeliveryShamiel AmirulNo ratings yet

- Building Acoustic Comfort White Paper 02-16 PDFDocument16 pagesBuilding Acoustic Comfort White Paper 02-16 PDFyaredNo ratings yet

- Tutorial 4 - UncertaintyDocument3 pagesTutorial 4 - UncertaintyCarine TeeNo ratings yet

- Bussiness EconomicsDocument5 pagesBussiness EconomicsAbdul Hadi SheikhNo ratings yet

- 1 Practice Exercise - Break Even PointDocument2 pages1 Practice Exercise - Break Even PointBhargav D.S.No ratings yet

- Buying Motives & Theories of Selling: Presented By: Navya Tandon (190677) Sarika Nangia (200004) Tinisha Chhabra (200003)Document56 pagesBuying Motives & Theories of Selling: Presented By: Navya Tandon (190677) Sarika Nangia (200004) Tinisha Chhabra (200003)NAVYA TANDON 190677No ratings yet

- Jain2014 - Decoding The Strike at Bajaj Auto's Chakan PlantDocument8 pagesJain2014 - Decoding The Strike at Bajaj Auto's Chakan PlantBRYAN VIDAURRE APAZA100% (1)

- AFAR05 07 Joint ArrangementsDocument10 pagesAFAR05 07 Joint ArrangementsAngeline ManuelNo ratings yet

- Reshare Commerce Et. Al. v. DotfitDocument5 pagesReshare Commerce Et. Al. v. DotfitPriorSmartNo ratings yet

- CRM-V-DAK48: UL Certified IntercomDocument3 pagesCRM-V-DAK48: UL Certified IntercomSODEX FRANCENo ratings yet

- St. Nicholas Cemetery Response To The NewsDocument1 pageSt. Nicholas Cemetery Response To The NewsActionNewsJaxNo ratings yet

- SOP 185 - Ambulance Billing - 4Document2 pagesSOP 185 - Ambulance Billing - 4khallushaik424No ratings yet

- How To Build An Activity Based Sales Strategy LevelElevenDocument14 pagesHow To Build An Activity Based Sales Strategy LevelElevenRogerNo ratings yet

- Two-Way Table of Specification: Name: Angelica H. Paras Subject: Applied Entrepreneurship Quarter: FirstDocument2 pagesTwo-Way Table of Specification: Name: Angelica H. Paras Subject: Applied Entrepreneurship Quarter: FirstAngelicaHermoParasNo ratings yet

- Service-Management Solved MCQs (Set-3)Document9 pagesService-Management Solved MCQs (Set-3)Priyanka KalyanamNo ratings yet

- HRIS-SurveyPDF 221105 140131Document5 pagesHRIS-SurveyPDF 221105 140131Veda PrakashNo ratings yet

- Ind As 7Document5 pagesInd As 7qwertyNo ratings yet

- Into To E-Commerce Module 1 MM3Document16 pagesInto To E-Commerce Module 1 MM3Vhonz Sugatan100% (1)

- Qatar Construction Sites Magazine August 2012Document32 pagesQatar Construction Sites Magazine August 2012Joseph Marriott Anderson100% (3)

- Payslip Oct 2022Document1 pagePayslip Oct 2022ryeshwanth999No ratings yet

- Quiz 1Document6 pagesQuiz 1Jonathan VidarNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Problems Sub-IfDocument11 pagesProblems Sub-IfChintakunta PreethiNo ratings yet

- WAC On Kodak: The Rebirth of An Iconic Brand Case StudyDocument7 pagesWAC On Kodak: The Rebirth of An Iconic Brand Case Studyritam chakrabortyNo ratings yet

- Introduction To Currency DerivativesDocument12 pagesIntroduction To Currency Derivativesquadeer791No ratings yet

- CAPMDocument12 pagesCAPMAkash TiwariNo ratings yet

- JETBLUE CaseDocument33 pagesJETBLUE CaseMarcellia Crenata100% (1)

- Derivatives - Unit 3 (Autosaved)Document54 pagesDerivatives - Unit 3 (Autosaved)learnerme129No ratings yet

- Currency Future DerivativesDocument18 pagesCurrency Future DerivativesrudraNo ratings yet

- Derivativesmarket 111006143752 Phpapp02Document21 pagesDerivativesmarket 111006143752 Phpapp02sejalahir30_40759023No ratings yet

- FRGN Curr Derivatives - FandO Os1qImUSkGDocument50 pagesFRGN Curr Derivatives - FandO Os1qImUSkGNikitha NithyanandhamNo ratings yet

- Frm2 Derivatives BasicsDocument34 pagesFrm2 Derivatives BasicsDîvýâñshü MâhâwârNo ratings yet

- What Is Currency DerivativeDocument16 pagesWhat Is Currency DerivativeShweta RajputNo ratings yet

- Derivatives 1Document91 pagesDerivatives 1sharath haradyNo ratings yet

- Derivative 1Document39 pagesDerivative 1Heera JhaNo ratings yet

- Introduction To Derivatives BasicsDocument34 pagesIntroduction To Derivatives Basicsmihir popatNo ratings yet

- Instruments of Foreign ExchangeDocument14 pagesInstruments of Foreign ExchangeMansi KoliyanNo ratings yet

- Introductory+Notes+on+Derivative+Securities+ (Fall+2009+ +SFR)Document16 pagesIntroductory+Notes+on+Derivative+Securities+ (Fall+2009+ +SFR)M. Khairul IslamNo ratings yet

- Forex Derivatives in India Its Implications - Currency Futures and Its Implications in Forex TradingDocument23 pagesForex Derivatives in India Its Implications - Currency Futures and Its Implications in Forex TradingamansinghaniaiipmNo ratings yet

- Module 2Document41 pagesModule 2bhargaviNo ratings yet

- Currency Futures NivDocument37 pagesCurrency Futures Nivpratibhashetty_87No ratings yet

- Currency Derivatives: by "Me"Document15 pagesCurrency Derivatives: by "Me"Shikhar AroraNo ratings yet

- Derivatives - FinalDocument34 pagesDerivatives - FinalGagan AnandNo ratings yet

- If 4Document79 pagesIf 4Aalfin MariyaNo ratings yet

- Financial Derivatives Assignment IDocument12 pagesFinancial Derivatives Assignment Iamit_harry100% (3)

- BFN 427 Business Scenarios Using Swaps, Options and FuturesDocument68 pagesBFN 427 Business Scenarios Using Swaps, Options and FuturesgeorgeNo ratings yet

- Market For Foreign ExchangeDocument43 pagesMarket For Foreign ExchangeAsha SoniNo ratings yet

- Forex by NageshDocument44 pagesForex by NageshNagesh KumarNo ratings yet

- Lala Lajpatrai College of Commerce & EconomicsDocument26 pagesLala Lajpatrai College of Commerce & EconomicsvorachiragNo ratings yet

- CURR NC FUTUR $ - FinalDocument25 pagesCURR NC FUTUR $ - FinalParidhi KhemkaNo ratings yet

- Currency Futures Market in India: at India Info Line LTD, HyderabadDocument19 pagesCurrency Futures Market in India: at India Info Line LTD, HyderabadSubodh KothariNo ratings yet

- UNIT 3 ForexDocument47 pagesUNIT 3 Forexsaurabh thakurNo ratings yet

- Introduction To DerivativesDocument41 pagesIntroduction To DerivativessmitajNo ratings yet

- Unit - 2Document39 pagesUnit - 2DivyanshuNo ratings yet

- Module 1 - Introduction To DerivativesDocument29 pagesModule 1 - Introduction To DerivativesSunny SinghNo ratings yet

- Derivatives Managing Financial RiskDocument17 pagesDerivatives Managing Financial RiskbaboabNo ratings yet

- Introduction:-: Rate, Such As The Euro To US Dollar Exchange Rate, or The British Pound To US Dollar ExchangeDocument34 pagesIntroduction:-: Rate, Such As The Euro To US Dollar Exchange Rate, or The British Pound To US Dollar Exchangesarabjeet_toriNo ratings yet

- Currency Derivatives Research PaperDocument6 pagesCurrency Derivatives Research Paperpimywinihyj3100% (1)

- FDM (Unit I-V)Document27 pagesFDM (Unit I-V)KathiravanNo ratings yet

- Financial Derivatives Market and Its Development in IndiaDocument6 pagesFinancial Derivatives Market and Its Development in Indiaanshulnatani4uNo ratings yet

- Unit 6 FM IDocument12 pagesUnit 6 FM IJay ༄᭄ShahNo ratings yet

- Role of Financial Futures With Reference To Nse NiftyDocument58 pagesRole of Financial Futures With Reference To Nse NiftyWebsoft Tech-HydNo ratings yet

- UNIT 3 ForexDocument47 pagesUNIT 3 Forexraj kumarNo ratings yet

- Derivatives: A Presentation by Harita Chanda Sneha Rampalli Nilesh KotereDocument15 pagesDerivatives: A Presentation by Harita Chanda Sneha Rampalli Nilesh KotereNilesh KotereNo ratings yet

- Unit One.Document41 pagesUnit One.Manas JainNo ratings yet

- Concepts Relating To Foreign ExchangeDocument89 pagesConcepts Relating To Foreign Exchangedeepakpandeyji2001No ratings yet

- Slide 1Document23 pagesSlide 1Shashika Anuradha KoswaththaNo ratings yet

- Work Sheet 02 - FDDocument4 pagesWork Sheet 02 - FDBhavesh RathiNo ratings yet

- Introduction To Derivatives: By: Nilima DasDocument103 pagesIntroduction To Derivatives: By: Nilima DasDilip ThakurNo ratings yet

- Lecture No. 7 International FinanceDocument31 pagesLecture No. 7 International FinanceNadia MurtazaNo ratings yet

- Financial Futures With Reference To NiftyDocument73 pagesFinancial Futures With Reference To Niftyjitendra jaushik75% (4)

- Unit Vi: Financial Risk ManagementDocument23 pagesUnit Vi: Financial Risk Managementmtechvlsitd labNo ratings yet

- Chap05 Ques MBF14eDocument6 pagesChap05 Ques MBF14eÂn TrầnNo ratings yet

- Financial Derivatives: Naman Jain (3254) Sabbani Maruthi (3276) Pranav Arora (3285) Sambit Ghosh (3286)Document21 pagesFinancial Derivatives: Naman Jain (3254) Sabbani Maruthi (3276) Pranav Arora (3285) Sambit Ghosh (3286)fhv hugNo ratings yet

- Futures and OptionsDocument51 pagesFutures and OptionsRitik VermaniNo ratings yet

- Derivative Markets and Instruments: Module # 6Document10 pagesDerivative Markets and Instruments: Module # 6Apoorv AnandNo ratings yet

- Foreign ExchangeDocument19 pagesForeign ExchangeradhikaNo ratings yet

- Before Commitment Commits You, Commit To The Commitment: Sundar B. N. Assistant Professor Coordinator ofDocument34 pagesBefore Commitment Commits You, Commit To The Commitment: Sundar B. N. Assistant Professor Coordinator ofH B SantoshNo ratings yet

- Currency DerivativesDocument12 pagesCurrency DerivativesNazneen100% (2)

- Futures and OptionsDocument4 pagesFutures and OptionsLucky_boy_87No ratings yet

- Mission RBI 2018 - Financial System: DerivativesDocument21 pagesMission RBI 2018 - Financial System: DerivativesAnonymous kj9KW15CQnNo ratings yet

- FuturesDocument30 pagesFuturessoujee60No ratings yet

- Forex for Beginners: The Most Comprehensive Guide to Making Money in the Forex Market (2022 Crash Course for Newbies)From EverandForex for Beginners: The Most Comprehensive Guide to Making Money in the Forex Market (2022 Crash Course for Newbies)No ratings yet

- Structure of Foreign Exchange Market in India, Exchange Rate Mexchanism-Quotes in Spot Market and Forward MarketDocument7 pagesStructure of Foreign Exchange Market in India, Exchange Rate Mexchanism-Quotes in Spot Market and Forward MarketChintakunta PreethiNo ratings yet

- Unit-Ii Foreign ExchangeDocument55 pagesUnit-Ii Foreign ExchangeChintakunta PreethiNo ratings yet

- International Financial InstrumentsDocument25 pagesInternational Financial InstrumentsChintakunta Preethi100% (1)

- Tarapore Committee ReportDocument14 pagesTarapore Committee ReportChintakunta PreethiNo ratings yet

- Q.8b IF 2019Document7 pagesQ.8b IF 2019Chintakunta PreethiNo ratings yet

- Gold Standard-Bretton Woods Standard 2Document39 pagesGold Standard-Bretton Woods Standard 2Chintakunta PreethiNo ratings yet

- Bop in IndiaDocument54 pagesBop in IndiaChintakunta PreethiNo ratings yet

- Calculation of Forward RateDocument8 pagesCalculation of Forward RateChintakunta PreethiNo ratings yet

- Foreign Exchange Arbitrage ProblemDocument7 pagesForeign Exchange Arbitrage ProblemChintakunta PreethiNo ratings yet

- International Banking-Euro Bank, Types of Banking Offices, Correspondent Bank, Representative Bank 5Document20 pagesInternational Banking-Euro Bank, Types of Banking Offices, Correspondent Bank, Representative Bank 5Chintakunta PreethiNo ratings yet

- Balance of Payments (Bop)Document29 pagesBalance of Payments (Bop)Chintakunta PreethiNo ratings yet

- Case Study BARGAIN CITYDocument1 pageCase Study BARGAIN CITYValentin KhoNo ratings yet

- Lauren Chen: Career ObjectiveDocument3 pagesLauren Chen: Career ObjectiveJacobNo ratings yet

- PMT 30101Document37 pagesPMT 30101Yousef Adel HassanenNo ratings yet

- Automobile Dealer Sales & Service-Critical IncidentsDocument4 pagesAutomobile Dealer Sales & Service-Critical IncidentsSIDDHARTH BANRANo ratings yet

- Form - Nonconforming Part DispositionDocument1 pageForm - Nonconforming Part DispositionDavidNo ratings yet

- September Month Current AffairsDocument7 pagesSeptember Month Current AffairsGoogle AccountNo ratings yet

- One Stop Centre (Osc) : Lessons On Best Practices in Planning System DeliveryDocument12 pagesOne Stop Centre (Osc) : Lessons On Best Practices in Planning System DeliveryShamiel AmirulNo ratings yet

- Building Acoustic Comfort White Paper 02-16 PDFDocument16 pagesBuilding Acoustic Comfort White Paper 02-16 PDFyaredNo ratings yet

- Tutorial 4 - UncertaintyDocument3 pagesTutorial 4 - UncertaintyCarine TeeNo ratings yet

- Bussiness EconomicsDocument5 pagesBussiness EconomicsAbdul Hadi SheikhNo ratings yet

- 1 Practice Exercise - Break Even PointDocument2 pages1 Practice Exercise - Break Even PointBhargav D.S.No ratings yet

- Buying Motives & Theories of Selling: Presented By: Navya Tandon (190677) Sarika Nangia (200004) Tinisha Chhabra (200003)Document56 pagesBuying Motives & Theories of Selling: Presented By: Navya Tandon (190677) Sarika Nangia (200004) Tinisha Chhabra (200003)NAVYA TANDON 190677No ratings yet

- Jain2014 - Decoding The Strike at Bajaj Auto's Chakan PlantDocument8 pagesJain2014 - Decoding The Strike at Bajaj Auto's Chakan PlantBRYAN VIDAURRE APAZA100% (1)

- AFAR05 07 Joint ArrangementsDocument10 pagesAFAR05 07 Joint ArrangementsAngeline ManuelNo ratings yet

- Reshare Commerce Et. Al. v. DotfitDocument5 pagesReshare Commerce Et. Al. v. DotfitPriorSmartNo ratings yet

- CRM-V-DAK48: UL Certified IntercomDocument3 pagesCRM-V-DAK48: UL Certified IntercomSODEX FRANCENo ratings yet

- St. Nicholas Cemetery Response To The NewsDocument1 pageSt. Nicholas Cemetery Response To The NewsActionNewsJaxNo ratings yet

- SOP 185 - Ambulance Billing - 4Document2 pagesSOP 185 - Ambulance Billing - 4khallushaik424No ratings yet

- How To Build An Activity Based Sales Strategy LevelElevenDocument14 pagesHow To Build An Activity Based Sales Strategy LevelElevenRogerNo ratings yet

- Two-Way Table of Specification: Name: Angelica H. Paras Subject: Applied Entrepreneurship Quarter: FirstDocument2 pagesTwo-Way Table of Specification: Name: Angelica H. Paras Subject: Applied Entrepreneurship Quarter: FirstAngelicaHermoParasNo ratings yet

- Service-Management Solved MCQs (Set-3)Document9 pagesService-Management Solved MCQs (Set-3)Priyanka KalyanamNo ratings yet

- HRIS-SurveyPDF 221105 140131Document5 pagesHRIS-SurveyPDF 221105 140131Veda PrakashNo ratings yet

- Ind As 7Document5 pagesInd As 7qwertyNo ratings yet

- Into To E-Commerce Module 1 MM3Document16 pagesInto To E-Commerce Module 1 MM3Vhonz Sugatan100% (1)

- Qatar Construction Sites Magazine August 2012Document32 pagesQatar Construction Sites Magazine August 2012Joseph Marriott Anderson100% (3)

- Payslip Oct 2022Document1 pagePayslip Oct 2022ryeshwanth999No ratings yet

- Quiz 1Document6 pagesQuiz 1Jonathan VidarNo ratings yet