Topic 4 - The Housing Decision

Topic 4 - The Housing Decision

You might also like

- Personal Finance Canadian 7th Edition Kapoor Solutions ManualDocument27 pagesPersonal Finance Canadian 7th Edition Kapoor Solutions Manualischiummargrave80ep100% (29)

- Rick Makoujy - How To Read A Balance Sheet - The Bottom Line On What You Need To Know About Cash Flow, Assets, Debt, Equity, Profit... and How It All Comes Together-McGraw-Hill (2010) PDFDocument209 pagesRick Makoujy - How To Read A Balance Sheet - The Bottom Line On What You Need To Know About Cash Flow, Assets, Debt, Equity, Profit... and How It All Comes Together-McGraw-Hill (2010) PDFanshul jain100% (4)

- Brokerage PracticeDocument26 pagesBrokerage PracticeElwin F. BuenaventuraNo ratings yet

- Nedbank Buyers GuideDocument25 pagesNedbank Buyers GuideMonde IdeaNo ratings yet

- Home Buyers Guide Standard BankDocument32 pagesHome Buyers Guide Standard Bank07961056320% (1)

- Prakash Selvaraj - ResumeDocument6 pagesPrakash Selvaraj - ResumePrakash AkashNo ratings yet

- CIPM Exam Pass Question - Insurance - Pensions MGTDocument7 pagesCIPM Exam Pass Question - Insurance - Pensions MGTVictory M. DankardNo ratings yet

- The Housing Decision: Factors and FinancesDocument37 pagesThe Housing Decision: Factors and Finances09Hasyim AlattasNo ratings yet

- C3-Mua NhaDocument10 pagesC3-Mua Nhaphankhacbien2511No ratings yet

- 2.3 The Home and Automobile DecisionDocument13 pages2.3 The Home and Automobile Decisionakshaygangarde143No ratings yet

- The Housing Decision: Factors and Finances: Sajid MehmudDocument34 pagesThe Housing Decision: Factors and Finances: Sajid Mehmudmana gNo ratings yet

- Complete Buyers PacketDocument9 pagesComplete Buyers Packetapi-125614979100% (1)

- Perfect Buyer Doc 2017 2 1Document9 pagesPerfect Buyer Doc 2017 2 1api-74153077No ratings yet

- Bael ReportingDocument23 pagesBael Reportingbisana.alangeloNo ratings yet

- Renting A HOMEDocument6 pagesRenting A HOMEJhon Mary MarcellanaNo ratings yet

- Making Automobile and Housing DecisionsDocument70 pagesMaking Automobile and Housing DecisionsAbigail ConstantinoNo ratings yet

- Week 3b-Real Estate LendingDocument26 pagesWeek 3b-Real Estate LendingSenuri AlmeidaNo ratings yet

- Lease Options: Own A Property For £1!: Property Investor, #5From EverandLease Options: Own A Property For £1!: Property Investor, #5No ratings yet

- Real Estate BriefDocument20 pagesReal Estate BriefRichard Max BazarNo ratings yet

- Buying or Selling A PropertyDocument24 pagesBuying or Selling A PropertyMark 'Mcduff' StevensonNo ratings yet

- Rent To Own A HomeDocument55 pagesRent To Own A HomeShane BeardNo ratings yet

- Kapoor PF 13e PPT Ch009Document39 pagesKapoor PF 13e PPT Ch009cuteserese roseNo ratings yet

- Selling Real PropertyDocument3 pagesSelling Real PropertyFrancise Mae Montilla MordenoNo ratings yet

- Buying A Home 1Document12 pagesBuying A Home 1FlyEngineerNo ratings yet

- Focus On Personal Finance 5Th Edition Kapoor Solutions Manual Full Chapter PDFDocument45 pagesFocus On Personal Finance 5Th Edition Kapoor Solutions Manual Full Chapter PDFmiguelstone5tt0f100% (14)

- Focus On Personal Finance 5th Edition Kapoor Solutions ManualDocument24 pagesFocus On Personal Finance 5th Edition Kapoor Solutions Manualdrkarenboltonddsqjtgwxzmbr100% (32)

- Home Buying GuideDocument27 pagesHome Buying GuideNidhi Rathi Mantri0% (1)

- Guide To Purchase Your HomeDocument28 pagesGuide To Purchase Your HomeDavid WangNo ratings yet

- S Lesson05 Buyinghome 100709Document16 pagesS Lesson05 Buyinghome 100709api-344973256No ratings yet

- Buying - A - House - in - The - Netherlands ABNDocument24 pagesBuying - A - House - in - The - Netherlands ABNilkerNo ratings yet

- Chapter-13-Housing-RentingDocument4 pagesChapter-13-Housing-RentingElvira NiepesNo ratings yet

- Housing Bond Basics: A Developer's PerspectiveDocument37 pagesHousing Bond Basics: A Developer's PerspectiveSrikanth VukkaNo ratings yet

- Review On LiteratureDocument7 pagesReview On LiteratureJenifer SathaNo ratings yet

- Personal Financial Planning 13th Edition Gitman Solutions Manual 1Document24 pagesPersonal Financial Planning 13th Edition Gitman Solutions Manual 1elizabeth100% (57)

- Personal Financial Planning 13th Edition Gitman Solutions Manual 1Document36 pagesPersonal Financial Planning 13th Edition Gitman Solutions Manual 1shirleybartlettndbyqeoaxi100% (32)

- MandbDocument2 pagesMandbNanz11 SerranoNo ratings yet

- Our Guide To Buying Off-The-PlanDocument47 pagesOur Guide To Buying Off-The-PlanProperty Bugs Pty LtdNo ratings yet

- Your Home Buying GuideDocument13 pagesYour Home Buying Guideapi-182635653No ratings yet

- Loans and MortgagesDocument26 pagesLoans and Mortgagesparkerroach21No ratings yet

- A Detailed Look at Equity Release Lifetime Mortgages in BirminghamDocument4 pagesA Detailed Look at Equity Release Lifetime Mortgages in BirminghamJoan SullivanNo ratings yet

- Glossary Home Buying2 Tcm21-108363Document13 pagesGlossary Home Buying2 Tcm21-108363rkrgupta991No ratings yet

- Keown Perfin5 Im 08Document24 pagesKeown Perfin5 Im 08a_hslr100% (1)

- Personal FinanceDocument14 pagesPersonal FinanceHoneylyn V. ChavitNo ratings yet

- Sean P. Callan, EsqDocument32 pagesSean P. Callan, EsqImran ShaNo ratings yet

- Home Buyers GuideDocument33 pagesHome Buyers Guidejimsnelling100% (3)

- 4.4 Task - Rent vs. Buy A HouseDocument4 pages4.4 Task - Rent vs. Buy A Housegsean399No ratings yet

- A. Describe in Detail The Advantages and Disadvantages of Renting Versus Owning A HomeDocument2 pagesA. Describe in Detail The Advantages and Disadvantages of Renting Versus Owning A HomefrankhNo ratings yet

- First-Time Landlords GuideDocument15 pagesFirst-Time Landlords GuideWaseem KhanNo ratings yet

- Chap 14 - Real EstateDocument34 pagesChap 14 - Real Estatesongan301002No ratings yet

- Valuation and ArbitationDocument9 pagesValuation and ArbitationNanshal BajajNo ratings yet

- Residential Tenancy Risk AnalysisDocument4 pagesResidential Tenancy Risk AnalysisIkem IsiekwenaNo ratings yet

- Legal Practice CourseDocument11 pagesLegal Practice CoursedixitNo ratings yet

- Real Estate Acquisition Process From A Legal Perspective 2 21Document11 pagesReal Estate Acquisition Process From A Legal Perspective 2 21mzhao8No ratings yet

- Home Owning, Renting, and Home PurchaseDocument5 pagesHome Owning, Renting, and Home PurchaseFeven MezemirNo ratings yet

- Chapter 15 Closing The Real Estate Transaction CombinedDocument54 pagesChapter 15 Closing The Real Estate Transaction CombinedRain BidesNo ratings yet

- Real EstateDocument14 pagesReal EstateRohan KapleNo ratings yet

- Long Term Sources of FinanceDocument23 pagesLong Term Sources of Financehitisha agrawalNo ratings yet

- Section A: Soham Chauhan - Roll No. 57 - REP&E - AIIMDocument10 pagesSection A: Soham Chauhan - Roll No. 57 - REP&E - AIIMSoham ChauhanNo ratings yet

- Tax Consequences of Home OwnershipDocument53 pagesTax Consequences of Home OwnershipMo ZhuNo ratings yet

- Buying A Property in SwedenDocument12 pagesBuying A Property in SwedenmailprasanaNo ratings yet

- Lab 2 - Get Data With Power BIDocument39 pagesLab 2 - Get Data With Power BIaarzu dangiNo ratings yet

- Lab 3 - Visualize Data in Power BIDocument42 pagesLab 3 - Visualize Data in Power BIaarzu dangiNo ratings yet

- Lab 1 - Getting Started With Power BIDocument33 pagesLab 1 - Getting Started With Power BIaarzu dangiNo ratings yet

- Topic 13 - Estate PlanningDocument62 pagesTopic 13 - Estate Planningaarzu dangiNo ratings yet

- Assignment of Pranaw Bikram KCDocument23 pagesAssignment of Pranaw Bikram KCaarzu dangiNo ratings yet

- Topic 2 Practice QuestionDocument4 pagesTopic 2 Practice Questionaarzu dangiNo ratings yet

- Topic 1 Practice QuestionDocument2 pagesTopic 1 Practice Questionaarzu dangiNo ratings yet

- Fin 204Document6 pagesFin 204aarzu dangiNo ratings yet

- Fin 203 Assignment 1Document12 pagesFin 203 Assignment 1aarzu dangiNo ratings yet

- Payout Policy: Test Bank, Chapter 16 168Document31 pagesPayout Policy: Test Bank, Chapter 16 168HuyenKhanhNo ratings yet

- IAS 38 - Intangible Assets PDFDocument7 pagesIAS 38 - Intangible Assets PDFADNo ratings yet

- Welcome To Our Presentation Monetary System in BangladeshDocument22 pagesWelcome To Our Presentation Monetary System in BangladeshHasan RishaNo ratings yet

- The Role of Financial Management: Instructor: Ajab Khan BurkiDocument20 pagesThe Role of Financial Management: Instructor: Ajab Khan BurkiGaurav KarkiNo ratings yet

- FEDEX - Stock & Performance Analysis: Group MembersDocument15 pagesFEDEX - Stock & Performance Analysis: Group MembersWebCutPasteNo ratings yet

- Annual Report of IOCL 174Document1 pageAnnual Report of IOCL 174Nikunj ParmarNo ratings yet

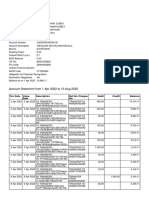

- Account Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceShubham TyagiNo ratings yet

- BCG InsideSherpa Core Strategy - Telco (Task 2 Additional Data) - UpdateDocument9 pagesBCG InsideSherpa Core Strategy - Telco (Task 2 Additional Data) - UpdateAbinash AgrawalNo ratings yet

- FAR-1 Mock Question PaperDocument9 pagesFAR-1 Mock Question Papernazish ilyasNo ratings yet

- Law of Contract IIDocument58 pagesLaw of Contract IIranjusanjuNo ratings yet

- REXEL SA - Research Report - FinalDocument6 pagesREXEL SA - Research Report - FinalGlen BorgNo ratings yet

- Money (Part II) Please Go Over The Following Terms and Their DefinitionsDocument4 pagesMoney (Part II) Please Go Over The Following Terms and Their DefinitionsDelia LupascuNo ratings yet

- Accounting For A Merchandising BusinessDocument5 pagesAccounting For A Merchandising BusinessMarvin AlmariaNo ratings yet

- 2023 Training Calendar Alphapartnerspdf 1671724768Document81 pages2023 Training Calendar Alphapartnerspdf 1671724768adenike adepojuNo ratings yet

- HDFC Bank LimitedDocument5 pagesHDFC Bank LimitedRaushan MehrotraNo ratings yet

- Dcimp 607550Document3 pagesDcimp 607550Hasibul Ehsan KhanNo ratings yet

- LLM Sebi Act 12122022Document37 pagesLLM Sebi Act 12122022KavyaNo ratings yet

- Report - 06 03 2024 - 03 59 20Document1 pageReport - 06 03 2024 - 03 59 20vlasbod18No ratings yet

- Hindustan Oil Exploration Company LimitedDocument20 pagesHindustan Oil Exploration Company LimitedBhunesh VaswaniNo ratings yet

- FinMan Module 5 Time Value of MoneyDocument9 pagesFinMan Module 5 Time Value of Moneyerickson hernanNo ratings yet

- School Finance and Business Administration SYLLABUSDocument9 pagesSchool Finance and Business Administration SYLLABUSnoreen fuentesNo ratings yet

- CFAS. Pages 3Document5 pagesCFAS. Pages 3Julienne CaitNo ratings yet

- Accounting Fraud in HistoryDocument3 pagesAccounting Fraud in Historyaya galsinNo ratings yet

- Hindu Undivided Family (HUF) For AY 2022-2023 - Income Tax DepartmentDocument13 pagesHindu Undivided Family (HUF) For AY 2022-2023 - Income Tax DepartmentAnkit A DesaiNo ratings yet

- Business Mathematics Lesson 3 Key Concepts in Buying and Selling Part 1 Mark-Up, Markdown, and Mark-On (Week6)Document18 pagesBusiness Mathematics Lesson 3 Key Concepts in Buying and Selling Part 1 Mark-Up, Markdown, and Mark-On (Week6)Dearla Bitoon100% (5)

- Payment Instructions: Banking Instructions: You're Nearly There!Document2 pagesPayment Instructions: Banking Instructions: You're Nearly There!Tiguidanke KeitaNo ratings yet

- Kotak Indigo Ka-Ching Credit Card BrochureDocument12 pagesKotak Indigo Ka-Ching Credit Card BrochureSahal RizviNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Personal Finance Canadian 7th Edition Kapoor Solutions ManualDocument27 pagesPersonal Finance Canadian 7th Edition Kapoor Solutions Manualischiummargrave80ep100% (29)

- Rick Makoujy - How To Read A Balance Sheet - The Bottom Line On What You Need To Know About Cash Flow, Assets, Debt, Equity, Profit... and How It All Comes Together-McGraw-Hill (2010) PDFDocument209 pagesRick Makoujy - How To Read A Balance Sheet - The Bottom Line On What You Need To Know About Cash Flow, Assets, Debt, Equity, Profit... and How It All Comes Together-McGraw-Hill (2010) PDFanshul jain100% (4)

- Brokerage PracticeDocument26 pagesBrokerage PracticeElwin F. BuenaventuraNo ratings yet

- Nedbank Buyers GuideDocument25 pagesNedbank Buyers GuideMonde IdeaNo ratings yet

- Home Buyers Guide Standard BankDocument32 pagesHome Buyers Guide Standard Bank07961056320% (1)

- Prakash Selvaraj - ResumeDocument6 pagesPrakash Selvaraj - ResumePrakash AkashNo ratings yet

- CIPM Exam Pass Question - Insurance - Pensions MGTDocument7 pagesCIPM Exam Pass Question - Insurance - Pensions MGTVictory M. DankardNo ratings yet

- The Housing Decision: Factors and FinancesDocument37 pagesThe Housing Decision: Factors and Finances09Hasyim AlattasNo ratings yet

- C3-Mua NhaDocument10 pagesC3-Mua Nhaphankhacbien2511No ratings yet

- 2.3 The Home and Automobile DecisionDocument13 pages2.3 The Home and Automobile Decisionakshaygangarde143No ratings yet

- The Housing Decision: Factors and Finances: Sajid MehmudDocument34 pagesThe Housing Decision: Factors and Finances: Sajid Mehmudmana gNo ratings yet

- Complete Buyers PacketDocument9 pagesComplete Buyers Packetapi-125614979100% (1)

- Perfect Buyer Doc 2017 2 1Document9 pagesPerfect Buyer Doc 2017 2 1api-74153077No ratings yet

- Bael ReportingDocument23 pagesBael Reportingbisana.alangeloNo ratings yet

- Renting A HOMEDocument6 pagesRenting A HOMEJhon Mary MarcellanaNo ratings yet

- Making Automobile and Housing DecisionsDocument70 pagesMaking Automobile and Housing DecisionsAbigail ConstantinoNo ratings yet

- Week 3b-Real Estate LendingDocument26 pagesWeek 3b-Real Estate LendingSenuri AlmeidaNo ratings yet

- Lease Options: Own A Property For £1!: Property Investor, #5From EverandLease Options: Own A Property For £1!: Property Investor, #5No ratings yet

- Real Estate BriefDocument20 pagesReal Estate BriefRichard Max BazarNo ratings yet

- Buying or Selling A PropertyDocument24 pagesBuying or Selling A PropertyMark 'Mcduff' StevensonNo ratings yet

- Rent To Own A HomeDocument55 pagesRent To Own A HomeShane BeardNo ratings yet

- Kapoor PF 13e PPT Ch009Document39 pagesKapoor PF 13e PPT Ch009cuteserese roseNo ratings yet

- Selling Real PropertyDocument3 pagesSelling Real PropertyFrancise Mae Montilla MordenoNo ratings yet

- Buying A Home 1Document12 pagesBuying A Home 1FlyEngineerNo ratings yet

- Focus On Personal Finance 5Th Edition Kapoor Solutions Manual Full Chapter PDFDocument45 pagesFocus On Personal Finance 5Th Edition Kapoor Solutions Manual Full Chapter PDFmiguelstone5tt0f100% (14)

- Focus On Personal Finance 5th Edition Kapoor Solutions ManualDocument24 pagesFocus On Personal Finance 5th Edition Kapoor Solutions Manualdrkarenboltonddsqjtgwxzmbr100% (32)

- Home Buying GuideDocument27 pagesHome Buying GuideNidhi Rathi Mantri0% (1)

- Guide To Purchase Your HomeDocument28 pagesGuide To Purchase Your HomeDavid WangNo ratings yet

- S Lesson05 Buyinghome 100709Document16 pagesS Lesson05 Buyinghome 100709api-344973256No ratings yet

- Buying - A - House - in - The - Netherlands ABNDocument24 pagesBuying - A - House - in - The - Netherlands ABNilkerNo ratings yet

- Chapter-13-Housing-RentingDocument4 pagesChapter-13-Housing-RentingElvira NiepesNo ratings yet

- Housing Bond Basics: A Developer's PerspectiveDocument37 pagesHousing Bond Basics: A Developer's PerspectiveSrikanth VukkaNo ratings yet

- Review On LiteratureDocument7 pagesReview On LiteratureJenifer SathaNo ratings yet

- Personal Financial Planning 13th Edition Gitman Solutions Manual 1Document24 pagesPersonal Financial Planning 13th Edition Gitman Solutions Manual 1elizabeth100% (57)

- Personal Financial Planning 13th Edition Gitman Solutions Manual 1Document36 pagesPersonal Financial Planning 13th Edition Gitman Solutions Manual 1shirleybartlettndbyqeoaxi100% (32)

- MandbDocument2 pagesMandbNanz11 SerranoNo ratings yet

- Our Guide To Buying Off-The-PlanDocument47 pagesOur Guide To Buying Off-The-PlanProperty Bugs Pty LtdNo ratings yet

- Your Home Buying GuideDocument13 pagesYour Home Buying Guideapi-182635653No ratings yet

- Loans and MortgagesDocument26 pagesLoans and Mortgagesparkerroach21No ratings yet

- A Detailed Look at Equity Release Lifetime Mortgages in BirminghamDocument4 pagesA Detailed Look at Equity Release Lifetime Mortgages in BirminghamJoan SullivanNo ratings yet

- Glossary Home Buying2 Tcm21-108363Document13 pagesGlossary Home Buying2 Tcm21-108363rkrgupta991No ratings yet

- Keown Perfin5 Im 08Document24 pagesKeown Perfin5 Im 08a_hslr100% (1)

- Personal FinanceDocument14 pagesPersonal FinanceHoneylyn V. ChavitNo ratings yet

- Sean P. Callan, EsqDocument32 pagesSean P. Callan, EsqImran ShaNo ratings yet

- Home Buyers GuideDocument33 pagesHome Buyers Guidejimsnelling100% (3)

- 4.4 Task - Rent vs. Buy A HouseDocument4 pages4.4 Task - Rent vs. Buy A Housegsean399No ratings yet

- A. Describe in Detail The Advantages and Disadvantages of Renting Versus Owning A HomeDocument2 pagesA. Describe in Detail The Advantages and Disadvantages of Renting Versus Owning A HomefrankhNo ratings yet

- First-Time Landlords GuideDocument15 pagesFirst-Time Landlords GuideWaseem KhanNo ratings yet

- Chap 14 - Real EstateDocument34 pagesChap 14 - Real Estatesongan301002No ratings yet

- Valuation and ArbitationDocument9 pagesValuation and ArbitationNanshal BajajNo ratings yet

- Residential Tenancy Risk AnalysisDocument4 pagesResidential Tenancy Risk AnalysisIkem IsiekwenaNo ratings yet

- Legal Practice CourseDocument11 pagesLegal Practice CoursedixitNo ratings yet

- Real Estate Acquisition Process From A Legal Perspective 2 21Document11 pagesReal Estate Acquisition Process From A Legal Perspective 2 21mzhao8No ratings yet

- Home Owning, Renting, and Home PurchaseDocument5 pagesHome Owning, Renting, and Home PurchaseFeven MezemirNo ratings yet

- Chapter 15 Closing The Real Estate Transaction CombinedDocument54 pagesChapter 15 Closing The Real Estate Transaction CombinedRain BidesNo ratings yet

- Real EstateDocument14 pagesReal EstateRohan KapleNo ratings yet

- Long Term Sources of FinanceDocument23 pagesLong Term Sources of Financehitisha agrawalNo ratings yet

- Section A: Soham Chauhan - Roll No. 57 - REP&E - AIIMDocument10 pagesSection A: Soham Chauhan - Roll No. 57 - REP&E - AIIMSoham ChauhanNo ratings yet

- Tax Consequences of Home OwnershipDocument53 pagesTax Consequences of Home OwnershipMo ZhuNo ratings yet

- Buying A Property in SwedenDocument12 pagesBuying A Property in SwedenmailprasanaNo ratings yet

- Lab 2 - Get Data With Power BIDocument39 pagesLab 2 - Get Data With Power BIaarzu dangiNo ratings yet

- Lab 3 - Visualize Data in Power BIDocument42 pagesLab 3 - Visualize Data in Power BIaarzu dangiNo ratings yet

- Lab 1 - Getting Started With Power BIDocument33 pagesLab 1 - Getting Started With Power BIaarzu dangiNo ratings yet

- Topic 13 - Estate PlanningDocument62 pagesTopic 13 - Estate Planningaarzu dangiNo ratings yet

- Assignment of Pranaw Bikram KCDocument23 pagesAssignment of Pranaw Bikram KCaarzu dangiNo ratings yet

- Topic 2 Practice QuestionDocument4 pagesTopic 2 Practice Questionaarzu dangiNo ratings yet

- Topic 1 Practice QuestionDocument2 pagesTopic 1 Practice Questionaarzu dangiNo ratings yet

- Fin 204Document6 pagesFin 204aarzu dangiNo ratings yet

- Fin 203 Assignment 1Document12 pagesFin 203 Assignment 1aarzu dangiNo ratings yet

- Payout Policy: Test Bank, Chapter 16 168Document31 pagesPayout Policy: Test Bank, Chapter 16 168HuyenKhanhNo ratings yet

- IAS 38 - Intangible Assets PDFDocument7 pagesIAS 38 - Intangible Assets PDFADNo ratings yet

- Welcome To Our Presentation Monetary System in BangladeshDocument22 pagesWelcome To Our Presentation Monetary System in BangladeshHasan RishaNo ratings yet

- The Role of Financial Management: Instructor: Ajab Khan BurkiDocument20 pagesThe Role of Financial Management: Instructor: Ajab Khan BurkiGaurav KarkiNo ratings yet

- FEDEX - Stock & Performance Analysis: Group MembersDocument15 pagesFEDEX - Stock & Performance Analysis: Group MembersWebCutPasteNo ratings yet

- Annual Report of IOCL 174Document1 pageAnnual Report of IOCL 174Nikunj ParmarNo ratings yet

- Account Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Apr 2022 To 13 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceShubham TyagiNo ratings yet

- BCG InsideSherpa Core Strategy - Telco (Task 2 Additional Data) - UpdateDocument9 pagesBCG InsideSherpa Core Strategy - Telco (Task 2 Additional Data) - UpdateAbinash AgrawalNo ratings yet

- FAR-1 Mock Question PaperDocument9 pagesFAR-1 Mock Question Papernazish ilyasNo ratings yet

- Law of Contract IIDocument58 pagesLaw of Contract IIranjusanjuNo ratings yet

- REXEL SA - Research Report - FinalDocument6 pagesREXEL SA - Research Report - FinalGlen BorgNo ratings yet

- Money (Part II) Please Go Over The Following Terms and Their DefinitionsDocument4 pagesMoney (Part II) Please Go Over The Following Terms and Their DefinitionsDelia LupascuNo ratings yet

- Accounting For A Merchandising BusinessDocument5 pagesAccounting For A Merchandising BusinessMarvin AlmariaNo ratings yet

- 2023 Training Calendar Alphapartnerspdf 1671724768Document81 pages2023 Training Calendar Alphapartnerspdf 1671724768adenike adepojuNo ratings yet

- HDFC Bank LimitedDocument5 pagesHDFC Bank LimitedRaushan MehrotraNo ratings yet

- Dcimp 607550Document3 pagesDcimp 607550Hasibul Ehsan KhanNo ratings yet

- LLM Sebi Act 12122022Document37 pagesLLM Sebi Act 12122022KavyaNo ratings yet

- Report - 06 03 2024 - 03 59 20Document1 pageReport - 06 03 2024 - 03 59 20vlasbod18No ratings yet

- Hindustan Oil Exploration Company LimitedDocument20 pagesHindustan Oil Exploration Company LimitedBhunesh VaswaniNo ratings yet

- FinMan Module 5 Time Value of MoneyDocument9 pagesFinMan Module 5 Time Value of Moneyerickson hernanNo ratings yet

- School Finance and Business Administration SYLLABUSDocument9 pagesSchool Finance and Business Administration SYLLABUSnoreen fuentesNo ratings yet

- CFAS. Pages 3Document5 pagesCFAS. Pages 3Julienne CaitNo ratings yet

- Accounting Fraud in HistoryDocument3 pagesAccounting Fraud in Historyaya galsinNo ratings yet

- Hindu Undivided Family (HUF) For AY 2022-2023 - Income Tax DepartmentDocument13 pagesHindu Undivided Family (HUF) For AY 2022-2023 - Income Tax DepartmentAnkit A DesaiNo ratings yet

- Business Mathematics Lesson 3 Key Concepts in Buying and Selling Part 1 Mark-Up, Markdown, and Mark-On (Week6)Document18 pagesBusiness Mathematics Lesson 3 Key Concepts in Buying and Selling Part 1 Mark-Up, Markdown, and Mark-On (Week6)Dearla Bitoon100% (5)

- Payment Instructions: Banking Instructions: You're Nearly There!Document2 pagesPayment Instructions: Banking Instructions: You're Nearly There!Tiguidanke KeitaNo ratings yet

- Kotak Indigo Ka-Ching Credit Card BrochureDocument12 pagesKotak Indigo Ka-Ching Credit Card BrochureSahal RizviNo ratings yet