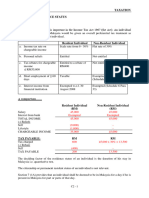

Topic 2-Residence Status For Individual

Topic 2-Residence Status For Individual

You might also like

- Topic 3-Residence Status For IndividualDocument18 pagesTopic 3-Residence Status For IndividualNURUL NUHA BINTI AZIZ HILMI / UPMNo ratings yet

- C2 Resident Status For IndvDocument32 pagesC2 Resident Status For IndvNUR DARWISYAH KAMARUDINNo ratings yet

- ABFT2013 T2-Residence (A)Document5 pagesABFT2013 T2-Residence (A)XindyNo ratings yet

- Taxation Chapter TwoDocument21 pagesTaxation Chapter TwoHazlina HusseinNo ratings yet

- Notes TX Mys Resident StatusDocument8 pagesNotes TX Mys Resident Statusnurinatihani24No ratings yet

- Acb21103 Residence Status 2023Document35 pagesAcb21103 Residence Status 2023Liyana IsmailNo ratings yet

- Malaysian Tax ResidenceDocument7 pagesMalaysian Tax ResidenceramanaraoNo ratings yet

- Chapter 2 Residence Status of IndividualsDocument48 pagesChapter 2 Residence Status of IndividualsHazlina HusseinNo ratings yet

- Resident Status For IndividualDocument24 pagesResident Status For IndividualMalabaris Malaya Umar SiddiqNo ratings yet

- CHAPTER2 Residence StatusDocument42 pagesCHAPTER2 Residence StatusnatlyhNo ratings yet

- Practice QuestionsDocument133 pagesPractice QuestionsSarath KumarNo ratings yet

- Week 2 - Resident StatusDocument9 pagesWeek 2 - Resident Statussam_suhaimiNo ratings yet

- Topic 2 Residence Status For IndividualDocument23 pagesTopic 2 Residence Status For IndividualHANIS IZYAN MAT ISANo ratings yet

- Taxation Unit 3 - Tutorial QuestionDocument8 pagesTaxation Unit 3 - Tutorial QuestionhavengroupnaNo ratings yet

- 2016BTW3153 Lecture 3 - Income Tax LawDocument65 pages2016BTW3153 Lecture 3 - Income Tax LawGwyneth YsNo ratings yet

- 2 RESIDENT STATUS 29sep2023Document10 pages2 RESIDENT STATUS 29sep2023MUHAMMAD AMIR HAMZAH NURZAFILNo ratings yet

- Determination of Residence StatusDocument2 pagesDetermination of Residence StatusMah Jia YongNo ratings yet

- Chapter 2 Determination of Residence StatusDocument27 pagesChapter 2 Determination of Residence Statuswaniy amaniNo ratings yet

- Practice QuestionsDocument134 pagesPractice QuestionsKarthikNo ratings yet

- Screenshot 2023-10-06 at 4.17.34 PMDocument7 pagesScreenshot 2023-10-06 at 4.17.34 PMbkp2022bkpNo ratings yet

- Chapter 2 Resident StatusDocument35 pagesChapter 2 Resident StatusNivaashene SaravananNo ratings yet

- Chapter 2 Residence StatusDocument9 pagesChapter 2 Residence StatusLOO YU HUANGNo ratings yet

- A) Residential Status of An IndividualDocument7 pagesA) Residential Status of An IndividualFaisal NurNo ratings yet

- Income TaxDocument3 pagesIncome TaxskjayasenaNo ratings yet

- Taxation Unit 3 - Concept Questions 2023Document6 pagesTaxation Unit 3 - Concept Questions 2023havengroupnaNo ratings yet

- Kishan Kumar Income Tax Amendments May2021Document6 pagesKishan Kumar Income Tax Amendments May2021ileshrathod0No ratings yet

- CH2 - Residence StatusDocument40 pagesCH2 - Residence Status謝中豪No ratings yet

- Residential Status and Tax IncidenceDocument4 pagesResidential Status and Tax IncidenceAshok Kumar MehetaNo ratings yet

- Topic 2 Resident Status For IndividualDocument23 pagesTopic 2 Resident Status For IndividualTeh Chu LeongNo ratings yet

- @CAhelp23 - Inter IncomeTax Must Do List Dec2021Document100 pages@CAhelp23 - Inter IncomeTax Must Do List Dec2021rajuNo ratings yet

- Domestic 08082022Document5 pagesDomestic 08082022avr3404No ratings yet

- Residential Status of An Individual - R-18-03-2Document6 pagesResidential Status of An Individual - R-18-03-2Dharma ProductionsNo ratings yet

- 1 - Notes - Resident - Individual YA2022Document2 pages1 - Notes - Resident - Individual YA2022pang jing zheNo ratings yet

- TTP Unit IDocument41 pagesTTP Unit IAafreen SiddiquiNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed DepositsY_AZNo ratings yet

- 1 Conceptual Framework Applied To Income Taxation - OutlineDocument4 pages1 Conceptual Framework Applied To Income Taxation - OutlineYong Kwang HanNo ratings yet

- Tax 1 RevisionDocument14 pagesTax 1 RevisionSoon Mei QiNo ratings yet

- Chap 2 - Residence StatusDocument40 pagesChap 2 - Residence StatusIfa Chan100% (1)

- Week 4 - Residence Based TaxationDocument31 pagesWeek 4 - Residence Based Taxationkabir kapoorNo ratings yet

- Tutorial 1Document36 pagesTutorial 1yyyNo ratings yet

- Inland Revenue Board Malaysia: Residence Status of IndividualsDocument21 pagesInland Revenue Board Malaysia: Residence Status of IndividualsNurin HadNo ratings yet

- Revision of Interest Rates On Domestic Term DepositsDocument2 pagesRevision of Interest Rates On Domestic Term DepositsLipsa DhalNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed DepositsRaghav sharmaNo ratings yet

- Super Hot Questions BankDocument56 pagesSuper Hot Questions BankClassicaverNo ratings yet

- 1 Corporate Taxation IDocument21 pages1 Corporate Taxation IHOW BING CHENNo ratings yet

- Dec20 QQ PDFDocument16 pagesDec20 QQ PDFSYAZWINA SUHAILINo ratings yet

- CHAPTER - 2 Residential Status.Document21 pagesCHAPTER - 2 Residential Status.deepikadobriyal1No ratings yet

- ACCA TAX Chapter AssessmentDocument17 pagesACCA TAX Chapter AssessmentAlbee Koh Jia YeeNo ratings yet

- IndividualDocument2 pagesIndividualKatherine MartinNo ratings yet

- Residential StatusDocument18 pagesResidential StatusShruti DoshiNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed Depositssasi 'sNo ratings yet

- Income Tax Brief NotesDocument184 pagesIncome Tax Brief NotesCreanativeNo ratings yet

- Chapter 2 Resident Status A 202Document33 pagesChapter 2 Resident Status A 202ateen rizalmanNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed DepositsV NaveenNo ratings yet

- Clarifications On PBB FY 2022Document1 pageClarifications On PBB FY 2022Jessa May ReyesNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed Depositssaurav katarukaNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed DepositsD SunilNo ratings yet

- 31162sm DTL Finalnew-May-Nov14 Cp2Document25 pages31162sm DTL Finalnew-May-Nov14 Cp2gvcNo ratings yet

- TAX228 2023 - Gross Income Part 2 - Student VersionDocument32 pagesTAX228 2023 - Gross Income Part 2 - Student VersionedwardsyaameenNo ratings yet

- TOPIC 4c - EMPLOYMENT INCOME - Basis Period and DeductionDocument8 pagesTOPIC 4c - EMPLOYMENT INCOME - Basis Period and DeductionAgnesNo ratings yet

- TOPIC 4b - EMPLOYMENT INCOME-typesDocument40 pagesTOPIC 4b - EMPLOYMENT INCOME-typesAgnesNo ratings yet

- TOPIC 6-Business Income and ExpensesDocument43 pagesTOPIC 6-Business Income and ExpensesAgnesNo ratings yet

- Topic 5a - Dividend IncomeDocument17 pagesTopic 5a - Dividend IncomeAgnesNo ratings yet

- Topic 5b-Interest IncomeDocument21 pagesTopic 5b-Interest IncomeAgnesNo ratings yet

- Topic 5c - Rental and Royalty IncomeDocument17 pagesTopic 5c - Rental and Royalty IncomeAgnesNo ratings yet

- Ent526 Midterm NoteDocument25 pagesEnt526 Midterm NotejayannaparkNo ratings yet

- What Is Industrial ConflictDocument4 pagesWhat Is Industrial Conflictcoolguys235100% (2)

- Real Estate Ownership and Investment in Saudi ArabiaDocument3 pagesReal Estate Ownership and Investment in Saudi ArabiasaifNo ratings yet

- Two Column Cash BookDocument24 pagesTwo Column Cash BookDarshans dadNo ratings yet

- Jeffrey A. Mello 4e - Chapter 5 - Strategic Workforce PlanningDocument23 pagesJeffrey A. Mello 4e - Chapter 5 - Strategic Workforce PlanningHuman Resource Management100% (3)

- Dynamics of Regulator Functionality: An Assessment of The Legal and Institutional Frameworks of The Nigeria Securities and Exchange CommissionDocument21 pagesDynamics of Regulator Functionality: An Assessment of The Legal and Institutional Frameworks of The Nigeria Securities and Exchange CommissionGabriel AdenyumaNo ratings yet

- PR2 Questionnaire-2Document5 pagesPR2 Questionnaire-2naxzleidomingoNo ratings yet

- Bachelor in Business Administration (Hons) FINANCE (BA242) : Future Trading Plan (FTP)Document25 pagesBachelor in Business Administration (Hons) FINANCE (BA242) : Future Trading Plan (FTP)Muhammad FaizNo ratings yet

- A & R Insider Trading FinalDocument23 pagesA & R Insider Trading Finalankit_05No ratings yet

- Rural Electrification CorporationDocument13 pagesRural Electrification CorporationmmmmuuuuNo ratings yet

- Food Stall Vendors DraftDocument42 pagesFood Stall Vendors Draftjanssen2000calacalNo ratings yet

- TMPC Employee Movement FormDocument1 pageTMPC Employee Movement FormGabriel GarciaNo ratings yet

- Personal Monthly Budget1Document3 pagesPersonal Monthly Budget1Shah NordinNo ratings yet

- Retail Strategies PDFDocument171 pagesRetail Strategies PDFravindramahadurage0% (1)

- Golf Business Plan TemplateDocument58 pagesGolf Business Plan TemplateBrian JerredNo ratings yet

- Dva1502 10019960Document213 pagesDva1502 10019960Tshepo SibekoNo ratings yet

- Porters Value Chain Divides The Structure of An Organization Into Activities and Does Not Consider The Traditional Departments and FunctionsDocument26 pagesPorters Value Chain Divides The Structure of An Organization Into Activities and Does Not Consider The Traditional Departments and FunctionsMd FerozNo ratings yet

- Operation Management Sports Obermeyer, LTDDocument3 pagesOperation Management Sports Obermeyer, LTDSachin BalahediNo ratings yet

- BSBOPS502 Task 1Document5 pagesBSBOPS502 Task 1Alessandro FonsecaNo ratings yet

- Chap 012 SM Mba Sem 3Document27 pagesChap 012 SM Mba Sem 3rajulramiNo ratings yet

- The Deal: All Stock Deal For $57 BillionDocument2 pagesThe Deal: All Stock Deal For $57 BillionSIDDHARTH PALNo ratings yet

- Daftar Pustaka - 11-34 CrosbyDocument6 pagesDaftar Pustaka - 11-34 CrosbyMuhammad Sidiq ANo ratings yet

- Question Bank MAN 22509 UT1Document17 pagesQuestion Bank MAN 22509 UT1Avinash GarjeNo ratings yet

- Petty Cash SummaryDocument1 pagePetty Cash SummaryBHCU PMNo ratings yet

- BPO1 - Module 5Document11 pagesBPO1 - Module 5Jerecho InatillezaNo ratings yet

- Internal Audit Checksheet 2014 (API 9th Ed)Document22 pagesInternal Audit Checksheet 2014 (API 9th Ed)dekengNo ratings yet

- Structure and Investment Policies of Commercial BanksDocument4 pagesStructure and Investment Policies of Commercial BanksCharu Saxena16No ratings yet

- Brand Management CH 7 Question AnswerDocument2 pagesBrand Management CH 7 Question AnswerFerdows Abid ChowdhuryNo ratings yet

- Marketing Plan ProductDocument3 pagesMarketing Plan ProductShara Mae GarciaNo ratings yet

- R50 Defining ElementsDocument38 pagesR50 Defining ElementsheisenbergNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Topic 3-Residence Status For IndividualDocument18 pagesTopic 3-Residence Status For IndividualNURUL NUHA BINTI AZIZ HILMI / UPMNo ratings yet

- C2 Resident Status For IndvDocument32 pagesC2 Resident Status For IndvNUR DARWISYAH KAMARUDINNo ratings yet

- ABFT2013 T2-Residence (A)Document5 pagesABFT2013 T2-Residence (A)XindyNo ratings yet

- Taxation Chapter TwoDocument21 pagesTaxation Chapter TwoHazlina HusseinNo ratings yet

- Notes TX Mys Resident StatusDocument8 pagesNotes TX Mys Resident Statusnurinatihani24No ratings yet

- Acb21103 Residence Status 2023Document35 pagesAcb21103 Residence Status 2023Liyana IsmailNo ratings yet

- Malaysian Tax ResidenceDocument7 pagesMalaysian Tax ResidenceramanaraoNo ratings yet

- Chapter 2 Residence Status of IndividualsDocument48 pagesChapter 2 Residence Status of IndividualsHazlina HusseinNo ratings yet

- Resident Status For IndividualDocument24 pagesResident Status For IndividualMalabaris Malaya Umar SiddiqNo ratings yet

- CHAPTER2 Residence StatusDocument42 pagesCHAPTER2 Residence StatusnatlyhNo ratings yet

- Practice QuestionsDocument133 pagesPractice QuestionsSarath KumarNo ratings yet

- Week 2 - Resident StatusDocument9 pagesWeek 2 - Resident Statussam_suhaimiNo ratings yet

- Topic 2 Residence Status For IndividualDocument23 pagesTopic 2 Residence Status For IndividualHANIS IZYAN MAT ISANo ratings yet

- Taxation Unit 3 - Tutorial QuestionDocument8 pagesTaxation Unit 3 - Tutorial QuestionhavengroupnaNo ratings yet

- 2016BTW3153 Lecture 3 - Income Tax LawDocument65 pages2016BTW3153 Lecture 3 - Income Tax LawGwyneth YsNo ratings yet

- 2 RESIDENT STATUS 29sep2023Document10 pages2 RESIDENT STATUS 29sep2023MUHAMMAD AMIR HAMZAH NURZAFILNo ratings yet

- Determination of Residence StatusDocument2 pagesDetermination of Residence StatusMah Jia YongNo ratings yet

- Chapter 2 Determination of Residence StatusDocument27 pagesChapter 2 Determination of Residence Statuswaniy amaniNo ratings yet

- Practice QuestionsDocument134 pagesPractice QuestionsKarthikNo ratings yet

- Screenshot 2023-10-06 at 4.17.34 PMDocument7 pagesScreenshot 2023-10-06 at 4.17.34 PMbkp2022bkpNo ratings yet

- Chapter 2 Resident StatusDocument35 pagesChapter 2 Resident StatusNivaashene SaravananNo ratings yet

- Chapter 2 Residence StatusDocument9 pagesChapter 2 Residence StatusLOO YU HUANGNo ratings yet

- A) Residential Status of An IndividualDocument7 pagesA) Residential Status of An IndividualFaisal NurNo ratings yet

- Income TaxDocument3 pagesIncome TaxskjayasenaNo ratings yet

- Taxation Unit 3 - Concept Questions 2023Document6 pagesTaxation Unit 3 - Concept Questions 2023havengroupnaNo ratings yet

- Kishan Kumar Income Tax Amendments May2021Document6 pagesKishan Kumar Income Tax Amendments May2021ileshrathod0No ratings yet

- CH2 - Residence StatusDocument40 pagesCH2 - Residence Status謝中豪No ratings yet

- Residential Status and Tax IncidenceDocument4 pagesResidential Status and Tax IncidenceAshok Kumar MehetaNo ratings yet

- Topic 2 Resident Status For IndividualDocument23 pagesTopic 2 Resident Status For IndividualTeh Chu LeongNo ratings yet

- @CAhelp23 - Inter IncomeTax Must Do List Dec2021Document100 pages@CAhelp23 - Inter IncomeTax Must Do List Dec2021rajuNo ratings yet

- Domestic 08082022Document5 pagesDomestic 08082022avr3404No ratings yet

- Residential Status of An Individual - R-18-03-2Document6 pagesResidential Status of An Individual - R-18-03-2Dharma ProductionsNo ratings yet

- 1 - Notes - Resident - Individual YA2022Document2 pages1 - Notes - Resident - Individual YA2022pang jing zheNo ratings yet

- TTP Unit IDocument41 pagesTTP Unit IAafreen SiddiquiNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed DepositsY_AZNo ratings yet

- 1 Conceptual Framework Applied To Income Taxation - OutlineDocument4 pages1 Conceptual Framework Applied To Income Taxation - OutlineYong Kwang HanNo ratings yet

- Tax 1 RevisionDocument14 pagesTax 1 RevisionSoon Mei QiNo ratings yet

- Chap 2 - Residence StatusDocument40 pagesChap 2 - Residence StatusIfa Chan100% (1)

- Week 4 - Residence Based TaxationDocument31 pagesWeek 4 - Residence Based Taxationkabir kapoorNo ratings yet

- Tutorial 1Document36 pagesTutorial 1yyyNo ratings yet

- Inland Revenue Board Malaysia: Residence Status of IndividualsDocument21 pagesInland Revenue Board Malaysia: Residence Status of IndividualsNurin HadNo ratings yet

- Revision of Interest Rates On Domestic Term DepositsDocument2 pagesRevision of Interest Rates On Domestic Term DepositsLipsa DhalNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed DepositsRaghav sharmaNo ratings yet

- Super Hot Questions BankDocument56 pagesSuper Hot Questions BankClassicaverNo ratings yet

- 1 Corporate Taxation IDocument21 pages1 Corporate Taxation IHOW BING CHENNo ratings yet

- Dec20 QQ PDFDocument16 pagesDec20 QQ PDFSYAZWINA SUHAILINo ratings yet

- CHAPTER - 2 Residential Status.Document21 pagesCHAPTER - 2 Residential Status.deepikadobriyal1No ratings yet

- ACCA TAX Chapter AssessmentDocument17 pagesACCA TAX Chapter AssessmentAlbee Koh Jia YeeNo ratings yet

- IndividualDocument2 pagesIndividualKatherine MartinNo ratings yet

- Residential StatusDocument18 pagesResidential StatusShruti DoshiNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed Depositssasi 'sNo ratings yet

- Income Tax Brief NotesDocument184 pagesIncome Tax Brief NotesCreanativeNo ratings yet

- Chapter 2 Resident Status A 202Document33 pagesChapter 2 Resident Status A 202ateen rizalmanNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed DepositsV NaveenNo ratings yet

- Clarifications On PBB FY 2022Document1 pageClarifications On PBB FY 2022Jessa May ReyesNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed Depositssaurav katarukaNo ratings yet

- Interest Rates For Fixed DepositsDocument2 pagesInterest Rates For Fixed DepositsD SunilNo ratings yet

- 31162sm DTL Finalnew-May-Nov14 Cp2Document25 pages31162sm DTL Finalnew-May-Nov14 Cp2gvcNo ratings yet

- TAX228 2023 - Gross Income Part 2 - Student VersionDocument32 pagesTAX228 2023 - Gross Income Part 2 - Student VersionedwardsyaameenNo ratings yet

- TOPIC 4c - EMPLOYMENT INCOME - Basis Period and DeductionDocument8 pagesTOPIC 4c - EMPLOYMENT INCOME - Basis Period and DeductionAgnesNo ratings yet

- TOPIC 4b - EMPLOYMENT INCOME-typesDocument40 pagesTOPIC 4b - EMPLOYMENT INCOME-typesAgnesNo ratings yet

- TOPIC 6-Business Income and ExpensesDocument43 pagesTOPIC 6-Business Income and ExpensesAgnesNo ratings yet

- Topic 5a - Dividend IncomeDocument17 pagesTopic 5a - Dividend IncomeAgnesNo ratings yet

- Topic 5b-Interest IncomeDocument21 pagesTopic 5b-Interest IncomeAgnesNo ratings yet

- Topic 5c - Rental and Royalty IncomeDocument17 pagesTopic 5c - Rental and Royalty IncomeAgnesNo ratings yet

- Ent526 Midterm NoteDocument25 pagesEnt526 Midterm NotejayannaparkNo ratings yet

- What Is Industrial ConflictDocument4 pagesWhat Is Industrial Conflictcoolguys235100% (2)

- Real Estate Ownership and Investment in Saudi ArabiaDocument3 pagesReal Estate Ownership and Investment in Saudi ArabiasaifNo ratings yet

- Two Column Cash BookDocument24 pagesTwo Column Cash BookDarshans dadNo ratings yet

- Jeffrey A. Mello 4e - Chapter 5 - Strategic Workforce PlanningDocument23 pagesJeffrey A. Mello 4e - Chapter 5 - Strategic Workforce PlanningHuman Resource Management100% (3)

- Dynamics of Regulator Functionality: An Assessment of The Legal and Institutional Frameworks of The Nigeria Securities and Exchange CommissionDocument21 pagesDynamics of Regulator Functionality: An Assessment of The Legal and Institutional Frameworks of The Nigeria Securities and Exchange CommissionGabriel AdenyumaNo ratings yet

- PR2 Questionnaire-2Document5 pagesPR2 Questionnaire-2naxzleidomingoNo ratings yet

- Bachelor in Business Administration (Hons) FINANCE (BA242) : Future Trading Plan (FTP)Document25 pagesBachelor in Business Administration (Hons) FINANCE (BA242) : Future Trading Plan (FTP)Muhammad FaizNo ratings yet

- A & R Insider Trading FinalDocument23 pagesA & R Insider Trading Finalankit_05No ratings yet

- Rural Electrification CorporationDocument13 pagesRural Electrification CorporationmmmmuuuuNo ratings yet

- Food Stall Vendors DraftDocument42 pagesFood Stall Vendors Draftjanssen2000calacalNo ratings yet

- TMPC Employee Movement FormDocument1 pageTMPC Employee Movement FormGabriel GarciaNo ratings yet

- Personal Monthly Budget1Document3 pagesPersonal Monthly Budget1Shah NordinNo ratings yet

- Retail Strategies PDFDocument171 pagesRetail Strategies PDFravindramahadurage0% (1)

- Golf Business Plan TemplateDocument58 pagesGolf Business Plan TemplateBrian JerredNo ratings yet

- Dva1502 10019960Document213 pagesDva1502 10019960Tshepo SibekoNo ratings yet

- Porters Value Chain Divides The Structure of An Organization Into Activities and Does Not Consider The Traditional Departments and FunctionsDocument26 pagesPorters Value Chain Divides The Structure of An Organization Into Activities and Does Not Consider The Traditional Departments and FunctionsMd FerozNo ratings yet

- Operation Management Sports Obermeyer, LTDDocument3 pagesOperation Management Sports Obermeyer, LTDSachin BalahediNo ratings yet

- BSBOPS502 Task 1Document5 pagesBSBOPS502 Task 1Alessandro FonsecaNo ratings yet

- Chap 012 SM Mba Sem 3Document27 pagesChap 012 SM Mba Sem 3rajulramiNo ratings yet

- The Deal: All Stock Deal For $57 BillionDocument2 pagesThe Deal: All Stock Deal For $57 BillionSIDDHARTH PALNo ratings yet

- Daftar Pustaka - 11-34 CrosbyDocument6 pagesDaftar Pustaka - 11-34 CrosbyMuhammad Sidiq ANo ratings yet

- Question Bank MAN 22509 UT1Document17 pagesQuestion Bank MAN 22509 UT1Avinash GarjeNo ratings yet

- Petty Cash SummaryDocument1 pagePetty Cash SummaryBHCU PMNo ratings yet

- BPO1 - Module 5Document11 pagesBPO1 - Module 5Jerecho InatillezaNo ratings yet

- Internal Audit Checksheet 2014 (API 9th Ed)Document22 pagesInternal Audit Checksheet 2014 (API 9th Ed)dekengNo ratings yet

- Structure and Investment Policies of Commercial BanksDocument4 pagesStructure and Investment Policies of Commercial BanksCharu Saxena16No ratings yet

- Brand Management CH 7 Question AnswerDocument2 pagesBrand Management CH 7 Question AnswerFerdows Abid ChowdhuryNo ratings yet

- Marketing Plan ProductDocument3 pagesMarketing Plan ProductShara Mae GarciaNo ratings yet

- R50 Defining ElementsDocument38 pagesR50 Defining ElementsheisenbergNo ratings yet