Income Under The Head "Salary"

Income Under The Head "Salary"

You might also like

- Answer Tutorial 5 Basis Period ChangesDocument2 pagesAnswer Tutorial 5 Basis Period Changesathirah jamaludinNo ratings yet

- Time Limits in TdsDocument4 pagesTime Limits in TdsKrishna Chaitanya DammalapatiNo ratings yet

- It - Lesson 4Document26 pagesIt - Lesson 4Sugandha AgarwalNo ratings yet

- ACCA F3 CH#10: Accruals and Prepayments Practice NotesDocument13 pagesACCA F3 CH#10: Accruals and Prepayments Practice NotesMuhammad AzamNo ratings yet

- Payroll PPT FinalDocument39 pagesPayroll PPT FinalKarla MeiNo ratings yet

- Test Paper 1 Salary PDFDocument4 pagesTest Paper 1 Salary PDFShrikant MahajanNo ratings yet

- Test Paper 1 SalaryDocument4 pagesTest Paper 1 SalaryjesurajajosephNo ratings yet

- 162.materials 3.share - Based.payment 001Document2 pages162.materials 3.share - Based.payment 001jpbluejnNo ratings yet

- Revenue Memorandum Circular No. 075-16Document3 pagesRevenue Memorandum Circular No. 075-16Dominique ShoreNo ratings yet

- Concept of Previous Year and Assessment YearDocument7 pagesConcept of Previous Year and Assessment YearGoldi Ks100% (1)

- An Overview On Equalization LevyDocument3 pagesAn Overview On Equalization LevyFlashcap693No ratings yet

- Rsubh 50443916Document1 pageRsubh 50443916Deepak PeriyasamyNo ratings yet

- Tutorial 3 - Basis Period (Continue)Document2 pagesTutorial 3 - Basis Period (Continue)Chan Ying100% (1)

- Accruals and PrepaymentsDocument2 pagesAccruals and PrepaymentsThikundeko EdwardNo ratings yet

- Documents Forms Required For Tax Proofs FY16 17 Ver1 1Document14 pagesDocuments Forms Required For Tax Proofs FY16 17 Ver1 1siddhuemailsNo ratings yet

- Tax ConceptsDocument4 pagesTax Conceptsguptaheena438No ratings yet

- TDS Payment Due Date Every QuarterDocument1 pageTDS Payment Due Date Every QuarterLatha VenugopalNo ratings yet

- Avg Due Date - Assignment AccDocument4 pagesAvg Due Date - Assignment Accdeepaharini918No ratings yet

- Ulep - Future ValueDocument4 pagesUlep - Future ValueNoel BajadaNo ratings yet

- 05032016fin - MS36 - 1Document5 pages05032016fin - MS36 - 1Santtosh Kummar AgathamudiNo ratings yet

- Apgli Revised Slab RatesDocument5 pagesApgli Revised Slab RatesSREEKANTHBABUNo ratings yet

- Presentation 1Document3 pagesPresentation 1priyanka pinkyNo ratings yet

- E-Con 220 TranscriptDocument14 pagesE-Con 220 TranscriptStuti SatraNo ratings yet

- Length of Service Percentage of The Year-End Bonus and Cash GiftDocument2 pagesLength of Service Percentage of The Year-End Bonus and Cash GiftDebz CayNo ratings yet

- Memo Year End Bonus 2020Document2 pagesMemo Year End Bonus 2020Debz CayNo ratings yet

- BonusDocument8 pagesBonusrajanabhishekNo ratings yet

- Thanks & Regards Vaishakhi Thakkar (H.R.Executive)Document2 pagesThanks & Regards Vaishakhi Thakkar (H.R.Executive)Ajay Singh YadavNo ratings yet

- Chapter 2 Interest On CapitalDocument9 pagesChapter 2 Interest On CapitalAparna PNo ratings yet

- There Are Two Types of TaxDocument13 pagesThere Are Two Types of TaxSahil NegiNo ratings yet

- Lecture 3 Concept of Income Accounting Period and Methods of AccountingDocument21 pagesLecture 3 Concept of Income Accounting Period and Methods of AccountingCassie ParkNo ratings yet

- Prashant'S Commerce Academy Fundamentals of PartnershipDocument3 pagesPrashant'S Commerce Academy Fundamentals of PartnershipMuskan TilokaniNo ratings yet

- Sukanya Samriddhi YojanaDocument4 pagesSukanya Samriddhi Yojanaparitosh sharmaNo ratings yet

- Month of Septembar Millon SamadDocument8 pagesMonth of Septembar Millon SamadMitul RahmanNo ratings yet

- Advance Payment of TaxDocument8 pagesAdvance Payment of TaxdeeptiNo ratings yet

- 2017 05 18 Economic and Housing Market Outlook 05-18-2017Document60 pages2017 05 18 Economic and Housing Market Outlook 05-18-2017National Association of REALTORS®100% (1)

- Philhealth Circular 2016-0034 PDFDocument4 pagesPhilhealth Circular 2016-0034 PDFjeanvaljean999No ratings yet

- IMP TDS Return Due Dates For FY 2023-24 - Penalty ForDocument5 pagesIMP TDS Return Due Dates For FY 2023-24 - Penalty Forsukantabera215No ratings yet

- What Are The Changes From 1 January 2016?Document17 pagesWhat Are The Changes From 1 January 2016?Chaitanya KumarNo ratings yet

- Chapter 10 - Adjusting The RecordsDocument24 pagesChapter 10 - Adjusting The RecordsJesseca JosafatNo ratings yet

- Calculation of EMI and Interest On Savings AccountDocument7 pagesCalculation of EMI and Interest On Savings AccountNeeraj DwivediNo ratings yet

- 1 Simple InterestDocument34 pages1 Simple InterestJeremiah DelgadoNo ratings yet

- Chapter 2Document10 pagesChapter 2Tanvir ChowdhuryNo ratings yet

- Audit of Liabilities Seatwork PDFDocument2 pagesAudit of Liabilities Seatwork PDFBbk GamingNo ratings yet

- Lecture 3 - Accounting Period and Methods of AccountingDocument21 pagesLecture 3 - Accounting Period and Methods of AccountingSKEETER BRITNEY COSTANo ratings yet

- Basic ConceptsDocument4 pagesBasic ConceptsHarry IcwaNo ratings yet

- English 1Document1 pageEnglish 1manoja hiroshiniNo ratings yet

- Mauritius Negative Income TaxDocument1 pageMauritius Negative Income Taxsr moosunNo ratings yet

- Personnel Services in GovernmentDocument25 pagesPersonnel Services in GovernmentDarwin D. BrilloNo ratings yet

- Taxation of SalaryDocument27 pagesTaxation of SalaryAshish RanjanNo ratings yet

- Gen Math Q2 - Week1 - Simple and Compound InterestDocument27 pagesGen Math Q2 - Week1 - Simple and Compound InterestJohn Nicholas TabadaNo ratings yet

- GST AssignmentDocument6 pagesGST Assignment13664No ratings yet

- Solve The Following Problems. Show Your SolutionDocument2 pagesSolve The Following Problems. Show Your SolutionPSHNo ratings yet

- Multi Financial YearDocument6 pagesMulti Financial YearA KumarNo ratings yet

- Learn More Salaries - August 2020Document5 pagesLearn More Salaries - August 2020Adarsh PandeyNo ratings yet

- Know Difference Between Assessment Year (AY) and Financial Year (FY)Document4 pagesKnow Difference Between Assessment Year (AY) and Financial Year (FY)vthreefriendsNo ratings yet

- EPFO Circular - Calculation of Higher P - 240214 - 214241Document3 pagesEPFO Circular - Calculation of Higher P - 240214 - 214241dineshp28300No ratings yet

- Basics of Income TaxDocument8 pagesBasics of Income Taxpajowah498No ratings yet

- Session 27-28 Advance TaxDocument5 pagesSession 27-28 Advance Taxomar zohorianNo ratings yet

- Extra Proplem CHP 4Document2 pagesExtra Proplem CHP 4Ali Al AjamiNo ratings yet

- C.H.A.P.P.S.: CLOCKABLE HOURS APPLICATION PROCESS AND PAY SYSTEMFrom EverandC.H.A.P.P.S.: CLOCKABLE HOURS APPLICATION PROCESS AND PAY SYSTEMNo ratings yet

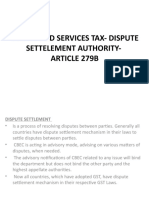

- Goods and Services Tax-Dispute Settelement Authority - Article 279BDocument6 pagesGoods and Services Tax-Dispute Settelement Authority - Article 279Bsuyash dugarNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- Registration Under GSTDocument13 pagesRegistration Under GSTsuyash dugarNo ratings yet

- Basic Principles of Income-Tax: BY Bommaraju Ramakotaiah. M SC, LLB, IrsDocument75 pagesBasic Principles of Income-Tax: BY Bommaraju Ramakotaiah. M SC, LLB, Irssuyash dugarNo ratings yet

- UntitledDocument14 pagesUntitledsuyash dugarNo ratings yet

- UntitledDocument9 pagesUntitledsuyash dugarNo ratings yet

- Transaction Value, Which Is The Price Actually Paid or PayableDocument10 pagesTransaction Value, Which Is The Price Actually Paid or Payablesuyash dugarNo ratings yet

- Connotation of Receipt of Income and Accrual of IncomeDocument8 pagesConnotation of Receipt of Income and Accrual of Incomesuyash dugarNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- UntitledDocument26 pagesUntitledsuyash dugarNo ratings yet

- Historical Development of The Customs Act and Customs DutyDocument47 pagesHistorical Development of The Customs Act and Customs Dutysuyash dugarNo ratings yet

- UntitledDocument14 pagesUntitledsuyash dugarNo ratings yet

- Clubbing of Income-PrintDocument5 pagesClubbing of Income-Printsuyash dugarNo ratings yet

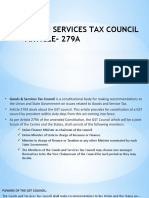

- Goods and Services Tax Council Article-279ADocument5 pagesGoods and Services Tax Council Article-279Asuyash dugarNo ratings yet

- Than Money and Securities But Includes Actionable Claim, Growing CropsDocument8 pagesThan Money and Securities But Includes Actionable Claim, Growing Cropssuyash dugarNo ratings yet

- Customs ValuationDocument6 pagesCustoms Valuationsuyash dugarNo ratings yet

- International TaxationDocument10 pagesInternational Taxationsuyash dugarNo ratings yet

- Income Tax Slabs Tax RateDocument7 pagesIncome Tax Slabs Tax Ratesuyash dugarNo ratings yet

- UntitledDocument7 pagesUntitledsuyash dugarNo ratings yet

- Adv & Dis Adv.Document6 pagesAdv & Dis Adv.suyash dugarNo ratings yet

- UntitledDocument17 pagesUntitledsuyash dugarNo ratings yet

- Constitutional Amendments and Provisions of GST in IndiaDocument20 pagesConstitutional Amendments and Provisions of GST in Indiasuyash dugarNo ratings yet

- International TaxationDocument6 pagesInternational Taxationsuyash dugarNo ratings yet

- UntitledDocument12 pagesUntitledsuyash dugarNo ratings yet

- PrintDocument6 pagesPrintsuyash dugarNo ratings yet

- Taxable EventDocument2 pagesTaxable Eventsuyash dugarNo ratings yet

- A Partnership Firm With A, B and C Partners.: IllustrationsDocument4 pagesA Partnership Firm With A, B and C Partners.: Illustrationssuyash dugarNo ratings yet

- UntitledDocument8 pagesUntitledsuyash dugarNo ratings yet

- Tax FeeDocument1 pageTax Feesuyash dugarNo ratings yet

- Agricultural IncomeDocument16 pagesAgricultural Incomesuyash dugarNo ratings yet

- Straddle StrategyDocument11 pagesStraddle StrategyРуслан СалаватовNo ratings yet

- A Study On The Performance of Valparai Urban Cooperative Bank in Coimabtor District-with-cover-page-V2Document267 pagesA Study On The Performance of Valparai Urban Cooperative Bank in Coimabtor District-with-cover-page-V2Pragathi MittalNo ratings yet

- Transfer Pricing: Impact of Transfer Price On Each Segment and The Company As A WholeDocument3 pagesTransfer Pricing: Impact of Transfer Price On Each Segment and The Company As A Wholezein lopezNo ratings yet

- Exam 3 Practice ProblemsDocument8 pagesExam 3 Practice ProblemsAn KouNo ratings yet

- Mortgage and Pivot Table-RepuelaDocument2 pagesMortgage and Pivot Table-RepuelaFrancis Loie RepuelaNo ratings yet

- Vitting - Format.Document12 pagesVitting - Format.rbn_7225No ratings yet

- Law Institute VictoriaDocument3 pagesLaw Institute VictoriaKaynat KatariaNo ratings yet

- Directors Loan and Tax ImplicationsDocument2 pagesDirectors Loan and Tax ImplicationsMary SmithNo ratings yet

- DBB1104-Unit 06 Product Related DecisionsDocument19 pagesDBB1104-Unit 06 Product Related DecisionsJust SaaNo ratings yet

- Premises MOU NewDocument2 pagesPremises MOU NewRehanNo ratings yet

- COVID-19 and Impact On Export Sector in Sri Lanka: Janaka WijayasiriDocument14 pagesCOVID-19 and Impact On Export Sector in Sri Lanka: Janaka WijayasiriShehan AnuradaNo ratings yet

- HDFC Life Smart Pension Plan BrochureDocument17 pagesHDFC Life Smart Pension Plan BrochureSatyajeet AnandNo ratings yet

- The Two-Gap Model of Economic Growth in Nigeria: Vector Autoregression (Var) ApproachDocument27 pagesThe Two-Gap Model of Economic Growth in Nigeria: Vector Autoregression (Var) ApproachyaredNo ratings yet

- Declercq (1992) : Crafts, 1995Document25 pagesDeclercq (1992) : Crafts, 1995Susovon JanaNo ratings yet

- Disney PestelDocument9 pagesDisney PestelShruti JhunjhunwalaNo ratings yet

- Medhanit Tadesse Thesis Final Doc-1Document76 pagesMedhanit Tadesse Thesis Final Doc-1Tatekia DanielNo ratings yet

- Process Costing TheoryDocument2 pagesProcess Costing TheoryNicoleNo ratings yet

- Executive-Legislative Agenda For Davao City: City Director Vicky P. Sarcena DILG Davao City OfficeDocument33 pagesExecutive-Legislative Agenda For Davao City: City Director Vicky P. Sarcena DILG Davao City OfficeHannah Cris Azcona Echavez100% (1)

- Mid Assignment - ACT 202Document4 pagesMid Assignment - ACT 202ramisa tasrimNo ratings yet

- Audit of Receivables - Notes & ReviewerDocument3 pagesAudit of Receivables - Notes & ReviewerJoshua LisingNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Anusha NairNo ratings yet

- UEF BE Unit 6 Logistics Chau Nguyen Full LectureDocument38 pagesUEF BE Unit 6 Logistics Chau Nguyen Full LectureDuongNo ratings yet

- Excel Bav Vinamilk C A 3 Chúng TaDocument47 pagesExcel Bav Vinamilk C A 3 Chúng TaThu ThuNo ratings yet

- DLP ElementsofstoryDocument33 pagesDLP ElementsofstoryKathlen Aiyanna Salvan BuhatNo ratings yet

- Cash Flow Template From Xlteq LimitedDocument12 pagesCash Flow Template From Xlteq LimitedmuhammadhideyosiNo ratings yet

- Cause and Effect EssayDocument2 pagesCause and Effect EssayAhmad AfiqNo ratings yet

- For Official Use Only: GMP Audit ReportDocument21 pagesFor Official Use Only: GMP Audit ReportserayemaydaNo ratings yet

- Make in IndiaDocument6 pagesMake in Indiasridharvchinni_21769No ratings yet

- Title Defense (SNDH)Document34 pagesTitle Defense (SNDH)sunandar HlaingNo ratings yet

- ECC2Document2 pagesECC2Dana IsabelleNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Answer Tutorial 5 Basis Period ChangesDocument2 pagesAnswer Tutorial 5 Basis Period Changesathirah jamaludinNo ratings yet

- Time Limits in TdsDocument4 pagesTime Limits in TdsKrishna Chaitanya DammalapatiNo ratings yet

- It - Lesson 4Document26 pagesIt - Lesson 4Sugandha AgarwalNo ratings yet

- ACCA F3 CH#10: Accruals and Prepayments Practice NotesDocument13 pagesACCA F3 CH#10: Accruals and Prepayments Practice NotesMuhammad AzamNo ratings yet

- Payroll PPT FinalDocument39 pagesPayroll PPT FinalKarla MeiNo ratings yet

- Test Paper 1 Salary PDFDocument4 pagesTest Paper 1 Salary PDFShrikant MahajanNo ratings yet

- Test Paper 1 SalaryDocument4 pagesTest Paper 1 SalaryjesurajajosephNo ratings yet

- 162.materials 3.share - Based.payment 001Document2 pages162.materials 3.share - Based.payment 001jpbluejnNo ratings yet

- Revenue Memorandum Circular No. 075-16Document3 pagesRevenue Memorandum Circular No. 075-16Dominique ShoreNo ratings yet

- Concept of Previous Year and Assessment YearDocument7 pagesConcept of Previous Year and Assessment YearGoldi Ks100% (1)

- An Overview On Equalization LevyDocument3 pagesAn Overview On Equalization LevyFlashcap693No ratings yet

- Rsubh 50443916Document1 pageRsubh 50443916Deepak PeriyasamyNo ratings yet

- Tutorial 3 - Basis Period (Continue)Document2 pagesTutorial 3 - Basis Period (Continue)Chan Ying100% (1)

- Accruals and PrepaymentsDocument2 pagesAccruals and PrepaymentsThikundeko EdwardNo ratings yet

- Documents Forms Required For Tax Proofs FY16 17 Ver1 1Document14 pagesDocuments Forms Required For Tax Proofs FY16 17 Ver1 1siddhuemailsNo ratings yet

- Tax ConceptsDocument4 pagesTax Conceptsguptaheena438No ratings yet

- TDS Payment Due Date Every QuarterDocument1 pageTDS Payment Due Date Every QuarterLatha VenugopalNo ratings yet

- Avg Due Date - Assignment AccDocument4 pagesAvg Due Date - Assignment Accdeepaharini918No ratings yet

- Ulep - Future ValueDocument4 pagesUlep - Future ValueNoel BajadaNo ratings yet

- 05032016fin - MS36 - 1Document5 pages05032016fin - MS36 - 1Santtosh Kummar AgathamudiNo ratings yet

- Apgli Revised Slab RatesDocument5 pagesApgli Revised Slab RatesSREEKANTHBABUNo ratings yet

- Presentation 1Document3 pagesPresentation 1priyanka pinkyNo ratings yet

- E-Con 220 TranscriptDocument14 pagesE-Con 220 TranscriptStuti SatraNo ratings yet

- Length of Service Percentage of The Year-End Bonus and Cash GiftDocument2 pagesLength of Service Percentage of The Year-End Bonus and Cash GiftDebz CayNo ratings yet

- Memo Year End Bonus 2020Document2 pagesMemo Year End Bonus 2020Debz CayNo ratings yet

- BonusDocument8 pagesBonusrajanabhishekNo ratings yet

- Thanks & Regards Vaishakhi Thakkar (H.R.Executive)Document2 pagesThanks & Regards Vaishakhi Thakkar (H.R.Executive)Ajay Singh YadavNo ratings yet

- Chapter 2 Interest On CapitalDocument9 pagesChapter 2 Interest On CapitalAparna PNo ratings yet

- There Are Two Types of TaxDocument13 pagesThere Are Two Types of TaxSahil NegiNo ratings yet

- Lecture 3 Concept of Income Accounting Period and Methods of AccountingDocument21 pagesLecture 3 Concept of Income Accounting Period and Methods of AccountingCassie ParkNo ratings yet

- Prashant'S Commerce Academy Fundamentals of PartnershipDocument3 pagesPrashant'S Commerce Academy Fundamentals of PartnershipMuskan TilokaniNo ratings yet

- Sukanya Samriddhi YojanaDocument4 pagesSukanya Samriddhi Yojanaparitosh sharmaNo ratings yet

- Month of Septembar Millon SamadDocument8 pagesMonth of Septembar Millon SamadMitul RahmanNo ratings yet

- Advance Payment of TaxDocument8 pagesAdvance Payment of TaxdeeptiNo ratings yet

- 2017 05 18 Economic and Housing Market Outlook 05-18-2017Document60 pages2017 05 18 Economic and Housing Market Outlook 05-18-2017National Association of REALTORS®100% (1)

- Philhealth Circular 2016-0034 PDFDocument4 pagesPhilhealth Circular 2016-0034 PDFjeanvaljean999No ratings yet

- IMP TDS Return Due Dates For FY 2023-24 - Penalty ForDocument5 pagesIMP TDS Return Due Dates For FY 2023-24 - Penalty Forsukantabera215No ratings yet

- What Are The Changes From 1 January 2016?Document17 pagesWhat Are The Changes From 1 January 2016?Chaitanya KumarNo ratings yet

- Chapter 10 - Adjusting The RecordsDocument24 pagesChapter 10 - Adjusting The RecordsJesseca JosafatNo ratings yet

- Calculation of EMI and Interest On Savings AccountDocument7 pagesCalculation of EMI and Interest On Savings AccountNeeraj DwivediNo ratings yet

- 1 Simple InterestDocument34 pages1 Simple InterestJeremiah DelgadoNo ratings yet

- Chapter 2Document10 pagesChapter 2Tanvir ChowdhuryNo ratings yet

- Audit of Liabilities Seatwork PDFDocument2 pagesAudit of Liabilities Seatwork PDFBbk GamingNo ratings yet

- Lecture 3 - Accounting Period and Methods of AccountingDocument21 pagesLecture 3 - Accounting Period and Methods of AccountingSKEETER BRITNEY COSTANo ratings yet

- Basic ConceptsDocument4 pagesBasic ConceptsHarry IcwaNo ratings yet

- English 1Document1 pageEnglish 1manoja hiroshiniNo ratings yet

- Mauritius Negative Income TaxDocument1 pageMauritius Negative Income Taxsr moosunNo ratings yet

- Personnel Services in GovernmentDocument25 pagesPersonnel Services in GovernmentDarwin D. BrilloNo ratings yet

- Taxation of SalaryDocument27 pagesTaxation of SalaryAshish RanjanNo ratings yet

- Gen Math Q2 - Week1 - Simple and Compound InterestDocument27 pagesGen Math Q2 - Week1 - Simple and Compound InterestJohn Nicholas TabadaNo ratings yet

- GST AssignmentDocument6 pagesGST Assignment13664No ratings yet

- Solve The Following Problems. Show Your SolutionDocument2 pagesSolve The Following Problems. Show Your SolutionPSHNo ratings yet

- Multi Financial YearDocument6 pagesMulti Financial YearA KumarNo ratings yet

- Learn More Salaries - August 2020Document5 pagesLearn More Salaries - August 2020Adarsh PandeyNo ratings yet

- Know Difference Between Assessment Year (AY) and Financial Year (FY)Document4 pagesKnow Difference Between Assessment Year (AY) and Financial Year (FY)vthreefriendsNo ratings yet

- EPFO Circular - Calculation of Higher P - 240214 - 214241Document3 pagesEPFO Circular - Calculation of Higher P - 240214 - 214241dineshp28300No ratings yet

- Basics of Income TaxDocument8 pagesBasics of Income Taxpajowah498No ratings yet

- Session 27-28 Advance TaxDocument5 pagesSession 27-28 Advance Taxomar zohorianNo ratings yet

- Extra Proplem CHP 4Document2 pagesExtra Proplem CHP 4Ali Al AjamiNo ratings yet

- C.H.A.P.P.S.: CLOCKABLE HOURS APPLICATION PROCESS AND PAY SYSTEMFrom EverandC.H.A.P.P.S.: CLOCKABLE HOURS APPLICATION PROCESS AND PAY SYSTEMNo ratings yet

- Goods and Services Tax-Dispute Settelement Authority - Article 279BDocument6 pagesGoods and Services Tax-Dispute Settelement Authority - Article 279Bsuyash dugarNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- Registration Under GSTDocument13 pagesRegistration Under GSTsuyash dugarNo ratings yet

- Basic Principles of Income-Tax: BY Bommaraju Ramakotaiah. M SC, LLB, IrsDocument75 pagesBasic Principles of Income-Tax: BY Bommaraju Ramakotaiah. M SC, LLB, Irssuyash dugarNo ratings yet

- UntitledDocument14 pagesUntitledsuyash dugarNo ratings yet

- UntitledDocument9 pagesUntitledsuyash dugarNo ratings yet

- Transaction Value, Which Is The Price Actually Paid or PayableDocument10 pagesTransaction Value, Which Is The Price Actually Paid or Payablesuyash dugarNo ratings yet

- Connotation of Receipt of Income and Accrual of IncomeDocument8 pagesConnotation of Receipt of Income and Accrual of Incomesuyash dugarNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- UntitledDocument26 pagesUntitledsuyash dugarNo ratings yet

- Historical Development of The Customs Act and Customs DutyDocument47 pagesHistorical Development of The Customs Act and Customs Dutysuyash dugarNo ratings yet

- UntitledDocument14 pagesUntitledsuyash dugarNo ratings yet

- Clubbing of Income-PrintDocument5 pagesClubbing of Income-Printsuyash dugarNo ratings yet

- Goods and Services Tax Council Article-279ADocument5 pagesGoods and Services Tax Council Article-279Asuyash dugarNo ratings yet

- Than Money and Securities But Includes Actionable Claim, Growing CropsDocument8 pagesThan Money and Securities But Includes Actionable Claim, Growing Cropssuyash dugarNo ratings yet

- Customs ValuationDocument6 pagesCustoms Valuationsuyash dugarNo ratings yet

- International TaxationDocument10 pagesInternational Taxationsuyash dugarNo ratings yet

- Income Tax Slabs Tax RateDocument7 pagesIncome Tax Slabs Tax Ratesuyash dugarNo ratings yet

- UntitledDocument7 pagesUntitledsuyash dugarNo ratings yet

- Adv & Dis Adv.Document6 pagesAdv & Dis Adv.suyash dugarNo ratings yet

- UntitledDocument17 pagesUntitledsuyash dugarNo ratings yet

- Constitutional Amendments and Provisions of GST in IndiaDocument20 pagesConstitutional Amendments and Provisions of GST in Indiasuyash dugarNo ratings yet

- International TaxationDocument6 pagesInternational Taxationsuyash dugarNo ratings yet

- UntitledDocument12 pagesUntitledsuyash dugarNo ratings yet

- PrintDocument6 pagesPrintsuyash dugarNo ratings yet

- Taxable EventDocument2 pagesTaxable Eventsuyash dugarNo ratings yet

- A Partnership Firm With A, B and C Partners.: IllustrationsDocument4 pagesA Partnership Firm With A, B and C Partners.: Illustrationssuyash dugarNo ratings yet

- UntitledDocument8 pagesUntitledsuyash dugarNo ratings yet

- Tax FeeDocument1 pageTax Feesuyash dugarNo ratings yet

- Agricultural IncomeDocument16 pagesAgricultural Incomesuyash dugarNo ratings yet

- Straddle StrategyDocument11 pagesStraddle StrategyРуслан СалаватовNo ratings yet

- A Study On The Performance of Valparai Urban Cooperative Bank in Coimabtor District-with-cover-page-V2Document267 pagesA Study On The Performance of Valparai Urban Cooperative Bank in Coimabtor District-with-cover-page-V2Pragathi MittalNo ratings yet

- Transfer Pricing: Impact of Transfer Price On Each Segment and The Company As A WholeDocument3 pagesTransfer Pricing: Impact of Transfer Price On Each Segment and The Company As A Wholezein lopezNo ratings yet

- Exam 3 Practice ProblemsDocument8 pagesExam 3 Practice ProblemsAn KouNo ratings yet

- Mortgage and Pivot Table-RepuelaDocument2 pagesMortgage and Pivot Table-RepuelaFrancis Loie RepuelaNo ratings yet

- Vitting - Format.Document12 pagesVitting - Format.rbn_7225No ratings yet

- Law Institute VictoriaDocument3 pagesLaw Institute VictoriaKaynat KatariaNo ratings yet

- Directors Loan and Tax ImplicationsDocument2 pagesDirectors Loan and Tax ImplicationsMary SmithNo ratings yet

- DBB1104-Unit 06 Product Related DecisionsDocument19 pagesDBB1104-Unit 06 Product Related DecisionsJust SaaNo ratings yet

- Premises MOU NewDocument2 pagesPremises MOU NewRehanNo ratings yet

- COVID-19 and Impact On Export Sector in Sri Lanka: Janaka WijayasiriDocument14 pagesCOVID-19 and Impact On Export Sector in Sri Lanka: Janaka WijayasiriShehan AnuradaNo ratings yet

- HDFC Life Smart Pension Plan BrochureDocument17 pagesHDFC Life Smart Pension Plan BrochureSatyajeet AnandNo ratings yet

- The Two-Gap Model of Economic Growth in Nigeria: Vector Autoregression (Var) ApproachDocument27 pagesThe Two-Gap Model of Economic Growth in Nigeria: Vector Autoregression (Var) ApproachyaredNo ratings yet

- Declercq (1992) : Crafts, 1995Document25 pagesDeclercq (1992) : Crafts, 1995Susovon JanaNo ratings yet

- Disney PestelDocument9 pagesDisney PestelShruti JhunjhunwalaNo ratings yet

- Medhanit Tadesse Thesis Final Doc-1Document76 pagesMedhanit Tadesse Thesis Final Doc-1Tatekia DanielNo ratings yet

- Process Costing TheoryDocument2 pagesProcess Costing TheoryNicoleNo ratings yet

- Executive-Legislative Agenda For Davao City: City Director Vicky P. Sarcena DILG Davao City OfficeDocument33 pagesExecutive-Legislative Agenda For Davao City: City Director Vicky P. Sarcena DILG Davao City OfficeHannah Cris Azcona Echavez100% (1)

- Mid Assignment - ACT 202Document4 pagesMid Assignment - ACT 202ramisa tasrimNo ratings yet

- Audit of Receivables - Notes & ReviewerDocument3 pagesAudit of Receivables - Notes & ReviewerJoshua LisingNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Anusha NairNo ratings yet

- UEF BE Unit 6 Logistics Chau Nguyen Full LectureDocument38 pagesUEF BE Unit 6 Logistics Chau Nguyen Full LectureDuongNo ratings yet

- Excel Bav Vinamilk C A 3 Chúng TaDocument47 pagesExcel Bav Vinamilk C A 3 Chúng TaThu ThuNo ratings yet

- DLP ElementsofstoryDocument33 pagesDLP ElementsofstoryKathlen Aiyanna Salvan BuhatNo ratings yet

- Cash Flow Template From Xlteq LimitedDocument12 pagesCash Flow Template From Xlteq LimitedmuhammadhideyosiNo ratings yet

- Cause and Effect EssayDocument2 pagesCause and Effect EssayAhmad AfiqNo ratings yet

- For Official Use Only: GMP Audit ReportDocument21 pagesFor Official Use Only: GMP Audit ReportserayemaydaNo ratings yet

- Make in IndiaDocument6 pagesMake in Indiasridharvchinni_21769No ratings yet

- Title Defense (SNDH)Document34 pagesTitle Defense (SNDH)sunandar HlaingNo ratings yet

- ECC2Document2 pagesECC2Dana IsabelleNo ratings yet