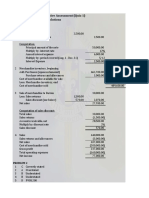

Mode Of: Dis Burs em en TS: Others

Mode Of: Dis Burs em en TS: Others

You might also like

- Budget Execution, Monitoring and Reporting of Government AccountingDocument13 pagesBudget Execution, Monitoring and Reporting of Government AccountingKathleenNo ratings yet

- Accounting For Disbursements and Related TransactionsDocument12 pagesAccounting For Disbursements and Related TransactionsVenn Bacus Rabadon100% (10)

- Diepenbrock BitcoinReport2011Document21 pagesDiepenbrock BitcoinReport2011tonydiepenbrockNo ratings yet

- Equity Markets in Transition PDFDocument612 pagesEquity Markets in Transition PDFkshitij kumar100% (1)

- Government AccountingDocument17 pagesGovernment AccountingJaniña Natividad100% (1)

- Note 5-Accounting For Budgetary AccountsDocument17 pagesNote 5-Accounting For Budgetary AccountsAngelica RubiosNo ratings yet

- Accounting For Disbursements and Related TransactionsDocument12 pagesAccounting For Disbursements and Related TransactionsJustine GuilingNo ratings yet

- Gov. Acc. Chapter 5Document38 pagesGov. Acc. Chapter 5Thea Marie GuiljonNo ratings yet

- Accounting For Government and Not-For-Profit OrganizationsDocument7 pagesAccounting For Government and Not-For-Profit OrganizationsAngela QuililanNo ratings yet

- Fundamental Principles For Revenue Collections and ReceiptsDocument3 pagesFundamental Principles For Revenue Collections and ReceiptsalliahnahNo ratings yet

- Duties & Responsibilities of DDOsDocument54 pagesDuties & Responsibilities of DDOsArshadMohdNo ratings yet

- Accounting For Disbursements and Related TransactionsDocument64 pagesAccounting For Disbursements and Related Transactionssayafront100% (1)

- Chapter 5Document9 pagesChapter 5tin2ndaccNo ratings yet

- Assignment 1Document2 pagesAssignment 1FRAULIEN GLINKA FANUGAONo ratings yet

- Basic Features of The New Government Accounting SystemDocument4 pagesBasic Features of The New Government Accounting SystemabbiecdefgNo ratings yet

- PH Gam - DisbursementsDocument6 pagesPH Gam - DisbursementsNabelah OdalNo ratings yet

- BudgetingDocument11 pagesBudgetingWinnie Ann Daquil LomosadNo ratings yet

- AA41023rdHand OutDocument7 pagesAA41023rdHand OutMana XDNo ratings yet

- Copy 7 ACP 313 QuickNotes On Government AccountingDocument10 pagesCopy 7 ACP 313 QuickNotes On Government AccountingRodken VallenteNo ratings yet

- Ngas & NposDocument7 pagesNgas & NposRenalyn MadeloNo ratings yet

- Disbursements MommyDocument61 pagesDisbursements MommyLyn CarlosNo ratings yet

- Part V Disbursement System 04122021Document19 pagesPart V Disbursement System 04122021Mana XD100% (1)

- Ngas Module Government AccountingDocument11 pagesNgas Module Government AccountingAnn Kristine Trinidad50% (2)

- CHAPTER 5 - DisbursementDocument25 pagesCHAPTER 5 - DisbursementMohammadNo ratings yet

- Submitted By: Mr. Malinao, Jeson SDocument3 pagesSubmitted By: Mr. Malinao, Jeson SJeson MalinaoNo ratings yet

- CHAPTER 5-RubyDocument3 pagesCHAPTER 5-RubyVenchNo ratings yet

- QUIZ in Government Accounting Disbursements: (Group 3)Document6 pagesQUIZ in Government Accounting Disbursements: (Group 3)TokkiNo ratings yet

- Part III - Accounting UnitDocument16 pagesPart III - Accounting Unitmoshi kpop cartNo ratings yet

- GAM 1 Chapter 6Document12 pagesGAM 1 Chapter 6Aldriel GabayanNo ratings yet

- AA 4102 4th Hand-OutDocument19 pagesAA 4102 4th Hand-OutGwen ClarinNo ratings yet

- Advacc ReportDocument29 pagesAdvacc ReportNHEMIA ELEVENCIONADONo ratings yet

- NGAS - NPOS - With AnswersDocument10 pagesNGAS - NPOS - With AnswersDardar Alcantara100% (1)

- Chapter 5 Accounting For Disbursements and Related TransactionsDocument8 pagesChapter 5 Accounting For Disbursements and Related TransactionsLeonard CanamoNo ratings yet

- R Pcpar Government AccountingDocument11 pagesR Pcpar Government Accountingdoora keys100% (1)

- Chapter 4 - Accounting For DisbursementsDocument12 pagesChapter 4 - Accounting For DisbursementsErika Villanueva Magallanes0% (1)

- ACC 312 Semestral OutputDocument11 pagesACC 312 Semestral Outputgelyncastromero25No ratings yet

- Budget Execution, Monitoring and Reporting Sec. 1. Scope. This Chapter Prescribes The Guidelines in Monitoring, Accounting, and Reporting ofDocument4 pagesBudget Execution, Monitoring and Reporting Sec. 1. Scope. This Chapter Prescribes The Guidelines in Monitoring, Accounting, and Reporting ofimsana minatozakiNo ratings yet

- Gov Acc 2019 JaaDocument9 pagesGov Acc 2019 JaaGlaiza Lerio100% (1)

- AGNPO Midterms ReviewerDocument79 pagesAGNPO Midterms ReviewerKurt Morin Cantor100% (2)

- Income Collection Deposit System With ConversionDocument5 pagesIncome Collection Deposit System With ConversionRichel ArmayanNo ratings yet

- New Government Accounting System & Non-Profit Organization #0005Document7 pagesNew Government Accounting System & Non-Profit Organization #0005Dardar AlcantaraNo ratings yet

- GAM Summary Group 4Document45 pagesGAM Summary Group 4Jake CasiñoNo ratings yet

- RCIDocument2 pagesRCIrussel1435100% (1)

- Accounting For Government and Non-Profit Organizations: 1. Notice of Cash Allocation (NCA)Document1 pageAccounting For Government and Non-Profit Organizations: 1. Notice of Cash Allocation (NCA)Randelle James FiestaNo ratings yet

- Government Accounting SummaryDocument9 pagesGovernment Accounting SummaryKenVictorino50% (2)

- ACCTG304 FinalDocument19 pagesACCTG304 FinalChristine Sondon100% (1)

- Accounting For Government and Not-For-Profit Organizations: ACCO 30033Document24 pagesAccounting For Government and Not-For-Profit Organizations: ACCO 30033hehehedontmind me100% (1)

- Module 5. DisbursementDocument4 pagesModule 5. DisbursementAbegail CadacioNo ratings yet

- Cash Advance For Petty Operating ExpensesDocument17 pagesCash Advance For Petty Operating ExpensesKristalyn MiguelNo ratings yet

- Accounting For Budgetary AccountsDocument51 pagesAccounting For Budgetary Accountsacctg2012No ratings yet

- Income Collection Deposit System With ConversionDocument6 pagesIncome Collection Deposit System With ConversionKaye Alyssa EnriquezNo ratings yet

- Accounting For Disbursement and Related TransactionsDocument16 pagesAccounting For Disbursement and Related TransactionsKattNo ratings yet

- Assignment 3Document2 pagesAssignment 3SandyNo ratings yet

- Revenue Memorandum Order No. 34-01Document8 pagesRevenue Memorandum Order No. 34-01johnnayelNo ratings yet

- Government Accounting Disbursements Definition of TermsDocument7 pagesGovernment Accounting Disbursements Definition of Termsralph macahiligNo ratings yet

- MRD 2015Document191 pagesMRD 2015Russel SarachoNo ratings yet

- Government Accounting Auditing & ProcurementDocument97 pagesGovernment Accounting Auditing & Procurementjamie c100% (1)

- Complete Accounting For Government DisbursementsDocument127 pagesComplete Accounting For Government DisbursementsMaketh.Man100% (1)

- Notes6 DisbursementsDocument15 pagesNotes6 DisbursementsRachel GellerNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- Investment PropertyDocument16 pagesInvestment PropertyDjunah ArellanoNo ratings yet

- Investment in Debt SecuritiesDocument29 pagesInvestment in Debt SecuritiesDjunah ArellanoNo ratings yet

- UntitledDocument4 pagesUntitledDjunah ArellanoNo ratings yet

- Module 11 Unit 2 Simple Linear RegressionDocument10 pagesModule 11 Unit 2 Simple Linear RegressionDjunah ArellanoNo ratings yet

- Ae314 - Task Guide (Final Project)Document1 pageAe314 - Task Guide (Final Project)Djunah ArellanoNo ratings yet

- Group 9-Educational InstitutionsDocument87 pagesGroup 9-Educational InstitutionsDjunah ArellanoNo ratings yet

- Chapter 7 The Balanced Scorecard A Tool To Implement Strategy SoftDocument20 pagesChapter 7 The Balanced Scorecard A Tool To Implement Strategy SoftDjunah ArellanoNo ratings yet

- AE 111 Midterm Formative Assessment 2Document3 pagesAE 111 Midterm Formative Assessment 2Djunah ArellanoNo ratings yet

- Ae314 - Task Guide (Summative 06)Document2 pagesAe314 - Task Guide (Summative 06)Djunah ArellanoNo ratings yet

- Module 9 Reports On Audited Financial StatementsDocument53 pagesModule 9 Reports On Audited Financial StatementsDjunah ArellanoNo ratings yet

- CMPC 311 Midterm ExaminationDocument13 pagesCMPC 311 Midterm ExaminationDjunah ArellanoNo ratings yet

- IA2 Prelim Quiz No. 2 Bio Assets 1Document6 pagesIA2 Prelim Quiz No. 2 Bio Assets 1Djunah ArellanoNo ratings yet

- AE 111 Midterm Departmental AssessmentDocument8 pagesAE 111 Midterm Departmental AssessmentDjunah ArellanoNo ratings yet

- AE 111 Midterm Summative Assessment 3Document4 pagesAE 111 Midterm Summative Assessment 3Djunah ArellanoNo ratings yet

- AE 111 Midterm Summative Assessment 2 SolutionsDocument6 pagesAE 111 Midterm Summative Assessment 2 SolutionsDjunah ArellanoNo ratings yet

- AE 111 Midterm Summative Assessment 3 SolutionsDocument12 pagesAE 111 Midterm Summative Assessment 3 SolutionsDjunah ArellanoNo ratings yet

- AE 111 Midterm Formative Assessment 3Document6 pagesAE 111 Midterm Formative Assessment 3Djunah ArellanoNo ratings yet

- AE 111 Final Summative Assessment 2Document3 pagesAE 111 Final Summative Assessment 2Djunah ArellanoNo ratings yet

- AE 111 Final Summative Assessment 1Document3 pagesAE 111 Final Summative Assessment 1Djunah ArellanoNo ratings yet

- BLR Midterm QuizDocument7 pagesBLR Midterm QuizDjunah ArellanoNo ratings yet

- AE 111 Midterm Formative Assessment 1Document4 pagesAE 111 Midterm Formative Assessment 1Djunah ArellanoNo ratings yet

- Final Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 1 Suggested Key AnswerDocument3 pagesFinal Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 1 Suggested Key AnswerDjunah ArellanoNo ratings yet

- Psa 2 Key AnswerDocument3 pagesPsa 2 Key AnswerDjunah ArellanoNo ratings yet

- BLR Prelims Quiz 1Document7 pagesBLR Prelims Quiz 1Djunah ArellanoNo ratings yet

- Final Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 2 Suggested Key AnswerDocument3 pagesFinal Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 2 Suggested Key AnswerDjunah ArellanoNo ratings yet

- AE 112 - Midterm Summative Assessment (Quiz 1) Suggested Answers and SolutionsDocument3 pagesAE 112 - Midterm Summative Assessment (Quiz 1) Suggested Answers and SolutionsDjunah ArellanoNo ratings yet

- BLR 211 - PdeDocument16 pagesBLR 211 - PdeDjunah ArellanoNo ratings yet

- BLR 211 - MdeDocument15 pagesBLR 211 - MdeDjunah ArellanoNo ratings yet

- BLR 211 - FdeDocument23 pagesBLR 211 - FdeDjunah Arellano100% (1)

- Arranz v. Manila Fidelity and Surety Co., Inc.Document2 pagesArranz v. Manila Fidelity and Surety Co., Inc.Ildefonso HernaezNo ratings yet

- PWC The Future of Financial ServicesDocument27 pagesPWC The Future of Financial ServicesPhương TrầnNo ratings yet

- LIC AAO 2016 Capsule by AffairscloudDocument84 pagesLIC AAO 2016 Capsule by AffairscloudRamesh RyNo ratings yet

- Rujukan: Jabatan Operasi Pelaburan Dan Pasaran Kewangan Bank Negara MalaysiaDocument1 pageRujukan: Jabatan Operasi Pelaburan Dan Pasaran Kewangan Bank Negara MalaysiaAry KurniaNo ratings yet

- RRB NTPC 4 Jan 2021 Answer Key With Question Paper (Released) : Check For Shift 1 and 2Document16 pagesRRB NTPC 4 Jan 2021 Answer Key With Question Paper (Released) : Check For Shift 1 and 2saranNo ratings yet

- TNJFU - Non-Teaching Positions - AdvertisementDocument2 pagesTNJFU - Non-Teaching Positions - AdvertisementGiridharan SubramaniamNo ratings yet

- Accounting For Crises: Nama MUHAMMAD DESTYAWAN (1500012328) Sri WahyuningsihDocument10 pagesAccounting For Crises: Nama MUHAMMAD DESTYAWAN (1500012328) Sri WahyuningsihMuhammad IwanNo ratings yet

- Bank of KhyberDocument63 pagesBank of KhyberSalman Khaliq BajwaNo ratings yet

- Form U Change of NameDocument2 pagesForm U Change of Namechief engineer CommercialNo ratings yet

- Finance Interview QuestionDocument41 pagesFinance Interview QuestionshuklashishNo ratings yet

- IRM Sessional Test Notes - Introduction To Risk and InsuranceDocument5 pagesIRM Sessional Test Notes - Introduction To Risk and InsuranceRupesh SharmaNo ratings yet

- Competative Profile Matrix Habib Bank Limited PakistanDocument4 pagesCompetative Profile Matrix Habib Bank Limited PakistanRaja Amir KhanNo ratings yet

- Interim Results June 2008Document12 pagesInterim Results June 2008Huseyin BozkinaNo ratings yet

- Ov QPR GIVBp at 5 Q8 MDocument15 pagesOv QPR GIVBp at 5 Q8 ManuranjankumarNo ratings yet

- Economics Mcqs For LecturerDocument8 pagesEconomics Mcqs For LecturerImran Khan Shar100% (1)

- Activity Based CostingDocument23 pagesActivity Based CostingLamhe Yasu0% (1)

- SVB Report 2022Document193 pagesSVB Report 2022iqbal maulanaNo ratings yet

- 7 Steps To Eliminate DebtDocument5 pages7 Steps To Eliminate DebtMirjana StefanovskiNo ratings yet

- Negotiable InstrumentsDocument60 pagesNegotiable InstrumentsTrem GallenteNo ratings yet

- Quiz 3Document5 pagesQuiz 3natashaNo ratings yet

- Questionnaire On Mutual FundsDocument5 pagesQuestionnaire On Mutual Fundsanushwarya80% (10)

- Tybcom Management AccoutingDocument6 pagesTybcom Management AccoutingavtaranNo ratings yet

- RCBC v. OdradaDocument28 pagesRCBC v. OdradaSabritoNo ratings yet

- Welcome To BRI Internet BankingDocument5 pagesWelcome To BRI Internet BankingLuru GratisanNo ratings yet

- Quotation of BMW 320d Luxury LineDocument2 pagesQuotation of BMW 320d Luxury Lineabhishek100% (1)

- Brand Development and Management Strategies in The Digital AgeDocument5 pagesBrand Development and Management Strategies in The Digital AgeRohanNo ratings yet

- Role of Merchant BanksDocument20 pagesRole of Merchant BanksSai Bhaskar Kannepalli100% (1)

- UCP Exam Review Consolidated Final (PDF) March 2023Document193 pagesUCP Exam Review Consolidated Final (PDF) March 2023enirhtacdiyezNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Budget Execution, Monitoring and Reporting of Government AccountingDocument13 pagesBudget Execution, Monitoring and Reporting of Government AccountingKathleenNo ratings yet

- Accounting For Disbursements and Related TransactionsDocument12 pagesAccounting For Disbursements and Related TransactionsVenn Bacus Rabadon100% (10)

- Diepenbrock BitcoinReport2011Document21 pagesDiepenbrock BitcoinReport2011tonydiepenbrockNo ratings yet

- Equity Markets in Transition PDFDocument612 pagesEquity Markets in Transition PDFkshitij kumar100% (1)

- Government AccountingDocument17 pagesGovernment AccountingJaniña Natividad100% (1)

- Note 5-Accounting For Budgetary AccountsDocument17 pagesNote 5-Accounting For Budgetary AccountsAngelica RubiosNo ratings yet

- Accounting For Disbursements and Related TransactionsDocument12 pagesAccounting For Disbursements and Related TransactionsJustine GuilingNo ratings yet

- Gov. Acc. Chapter 5Document38 pagesGov. Acc. Chapter 5Thea Marie GuiljonNo ratings yet

- Accounting For Government and Not-For-Profit OrganizationsDocument7 pagesAccounting For Government and Not-For-Profit OrganizationsAngela QuililanNo ratings yet

- Fundamental Principles For Revenue Collections and ReceiptsDocument3 pagesFundamental Principles For Revenue Collections and ReceiptsalliahnahNo ratings yet

- Duties & Responsibilities of DDOsDocument54 pagesDuties & Responsibilities of DDOsArshadMohdNo ratings yet

- Accounting For Disbursements and Related TransactionsDocument64 pagesAccounting For Disbursements and Related Transactionssayafront100% (1)

- Chapter 5Document9 pagesChapter 5tin2ndaccNo ratings yet

- Assignment 1Document2 pagesAssignment 1FRAULIEN GLINKA FANUGAONo ratings yet

- Basic Features of The New Government Accounting SystemDocument4 pagesBasic Features of The New Government Accounting SystemabbiecdefgNo ratings yet

- PH Gam - DisbursementsDocument6 pagesPH Gam - DisbursementsNabelah OdalNo ratings yet

- BudgetingDocument11 pagesBudgetingWinnie Ann Daquil LomosadNo ratings yet

- AA41023rdHand OutDocument7 pagesAA41023rdHand OutMana XDNo ratings yet

- Copy 7 ACP 313 QuickNotes On Government AccountingDocument10 pagesCopy 7 ACP 313 QuickNotes On Government AccountingRodken VallenteNo ratings yet

- Ngas & NposDocument7 pagesNgas & NposRenalyn MadeloNo ratings yet

- Disbursements MommyDocument61 pagesDisbursements MommyLyn CarlosNo ratings yet

- Part V Disbursement System 04122021Document19 pagesPart V Disbursement System 04122021Mana XD100% (1)

- Ngas Module Government AccountingDocument11 pagesNgas Module Government AccountingAnn Kristine Trinidad50% (2)

- CHAPTER 5 - DisbursementDocument25 pagesCHAPTER 5 - DisbursementMohammadNo ratings yet

- Submitted By: Mr. Malinao, Jeson SDocument3 pagesSubmitted By: Mr. Malinao, Jeson SJeson MalinaoNo ratings yet

- CHAPTER 5-RubyDocument3 pagesCHAPTER 5-RubyVenchNo ratings yet

- QUIZ in Government Accounting Disbursements: (Group 3)Document6 pagesQUIZ in Government Accounting Disbursements: (Group 3)TokkiNo ratings yet

- Part III - Accounting UnitDocument16 pagesPart III - Accounting Unitmoshi kpop cartNo ratings yet

- GAM 1 Chapter 6Document12 pagesGAM 1 Chapter 6Aldriel GabayanNo ratings yet

- AA 4102 4th Hand-OutDocument19 pagesAA 4102 4th Hand-OutGwen ClarinNo ratings yet

- Advacc ReportDocument29 pagesAdvacc ReportNHEMIA ELEVENCIONADONo ratings yet

- NGAS - NPOS - With AnswersDocument10 pagesNGAS - NPOS - With AnswersDardar Alcantara100% (1)

- Chapter 5 Accounting For Disbursements and Related TransactionsDocument8 pagesChapter 5 Accounting For Disbursements and Related TransactionsLeonard CanamoNo ratings yet

- R Pcpar Government AccountingDocument11 pagesR Pcpar Government Accountingdoora keys100% (1)

- Chapter 4 - Accounting For DisbursementsDocument12 pagesChapter 4 - Accounting For DisbursementsErika Villanueva Magallanes0% (1)

- ACC 312 Semestral OutputDocument11 pagesACC 312 Semestral Outputgelyncastromero25No ratings yet

- Budget Execution, Monitoring and Reporting Sec. 1. Scope. This Chapter Prescribes The Guidelines in Monitoring, Accounting, and Reporting ofDocument4 pagesBudget Execution, Monitoring and Reporting Sec. 1. Scope. This Chapter Prescribes The Guidelines in Monitoring, Accounting, and Reporting ofimsana minatozakiNo ratings yet

- Gov Acc 2019 JaaDocument9 pagesGov Acc 2019 JaaGlaiza Lerio100% (1)

- AGNPO Midterms ReviewerDocument79 pagesAGNPO Midterms ReviewerKurt Morin Cantor100% (2)

- Income Collection Deposit System With ConversionDocument5 pagesIncome Collection Deposit System With ConversionRichel ArmayanNo ratings yet

- New Government Accounting System & Non-Profit Organization #0005Document7 pagesNew Government Accounting System & Non-Profit Organization #0005Dardar AlcantaraNo ratings yet

- GAM Summary Group 4Document45 pagesGAM Summary Group 4Jake CasiñoNo ratings yet

- RCIDocument2 pagesRCIrussel1435100% (1)

- Accounting For Government and Non-Profit Organizations: 1. Notice of Cash Allocation (NCA)Document1 pageAccounting For Government and Non-Profit Organizations: 1. Notice of Cash Allocation (NCA)Randelle James FiestaNo ratings yet

- Government Accounting SummaryDocument9 pagesGovernment Accounting SummaryKenVictorino50% (2)

- ACCTG304 FinalDocument19 pagesACCTG304 FinalChristine Sondon100% (1)

- Accounting For Government and Not-For-Profit Organizations: ACCO 30033Document24 pagesAccounting For Government and Not-For-Profit Organizations: ACCO 30033hehehedontmind me100% (1)

- Module 5. DisbursementDocument4 pagesModule 5. DisbursementAbegail CadacioNo ratings yet

- Cash Advance For Petty Operating ExpensesDocument17 pagesCash Advance For Petty Operating ExpensesKristalyn MiguelNo ratings yet

- Accounting For Budgetary AccountsDocument51 pagesAccounting For Budgetary Accountsacctg2012No ratings yet

- Income Collection Deposit System With ConversionDocument6 pagesIncome Collection Deposit System With ConversionKaye Alyssa EnriquezNo ratings yet

- Accounting For Disbursement and Related TransactionsDocument16 pagesAccounting For Disbursement and Related TransactionsKattNo ratings yet

- Assignment 3Document2 pagesAssignment 3SandyNo ratings yet

- Revenue Memorandum Order No. 34-01Document8 pagesRevenue Memorandum Order No. 34-01johnnayelNo ratings yet

- Government Accounting Disbursements Definition of TermsDocument7 pagesGovernment Accounting Disbursements Definition of Termsralph macahiligNo ratings yet

- MRD 2015Document191 pagesMRD 2015Russel SarachoNo ratings yet

- Government Accounting Auditing & ProcurementDocument97 pagesGovernment Accounting Auditing & Procurementjamie c100% (1)

- Complete Accounting For Government DisbursementsDocument127 pagesComplete Accounting For Government DisbursementsMaketh.Man100% (1)

- Notes6 DisbursementsDocument15 pagesNotes6 DisbursementsRachel GellerNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- Investment PropertyDocument16 pagesInvestment PropertyDjunah ArellanoNo ratings yet

- Investment in Debt SecuritiesDocument29 pagesInvestment in Debt SecuritiesDjunah ArellanoNo ratings yet

- UntitledDocument4 pagesUntitledDjunah ArellanoNo ratings yet

- Module 11 Unit 2 Simple Linear RegressionDocument10 pagesModule 11 Unit 2 Simple Linear RegressionDjunah ArellanoNo ratings yet

- Ae314 - Task Guide (Final Project)Document1 pageAe314 - Task Guide (Final Project)Djunah ArellanoNo ratings yet

- Group 9-Educational InstitutionsDocument87 pagesGroup 9-Educational InstitutionsDjunah ArellanoNo ratings yet

- Chapter 7 The Balanced Scorecard A Tool To Implement Strategy SoftDocument20 pagesChapter 7 The Balanced Scorecard A Tool To Implement Strategy SoftDjunah ArellanoNo ratings yet

- AE 111 Midterm Formative Assessment 2Document3 pagesAE 111 Midterm Formative Assessment 2Djunah ArellanoNo ratings yet

- Ae314 - Task Guide (Summative 06)Document2 pagesAe314 - Task Guide (Summative 06)Djunah ArellanoNo ratings yet

- Module 9 Reports On Audited Financial StatementsDocument53 pagesModule 9 Reports On Audited Financial StatementsDjunah ArellanoNo ratings yet

- CMPC 311 Midterm ExaminationDocument13 pagesCMPC 311 Midterm ExaminationDjunah ArellanoNo ratings yet

- IA2 Prelim Quiz No. 2 Bio Assets 1Document6 pagesIA2 Prelim Quiz No. 2 Bio Assets 1Djunah ArellanoNo ratings yet

- AE 111 Midterm Departmental AssessmentDocument8 pagesAE 111 Midterm Departmental AssessmentDjunah ArellanoNo ratings yet

- AE 111 Midterm Summative Assessment 3Document4 pagesAE 111 Midterm Summative Assessment 3Djunah ArellanoNo ratings yet

- AE 111 Midterm Summative Assessment 2 SolutionsDocument6 pagesAE 111 Midterm Summative Assessment 2 SolutionsDjunah ArellanoNo ratings yet

- AE 111 Midterm Summative Assessment 3 SolutionsDocument12 pagesAE 111 Midterm Summative Assessment 3 SolutionsDjunah ArellanoNo ratings yet

- AE 111 Midterm Formative Assessment 3Document6 pagesAE 111 Midterm Formative Assessment 3Djunah ArellanoNo ratings yet

- AE 111 Final Summative Assessment 2Document3 pagesAE 111 Final Summative Assessment 2Djunah ArellanoNo ratings yet

- AE 111 Final Summative Assessment 1Document3 pagesAE 111 Final Summative Assessment 1Djunah ArellanoNo ratings yet

- BLR Midterm QuizDocument7 pagesBLR Midterm QuizDjunah ArellanoNo ratings yet

- AE 111 Midterm Formative Assessment 1Document4 pagesAE 111 Midterm Formative Assessment 1Djunah ArellanoNo ratings yet

- Final Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 1 Suggested Key AnswerDocument3 pagesFinal Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 1 Suggested Key AnswerDjunah ArellanoNo ratings yet

- Psa 2 Key AnswerDocument3 pagesPsa 2 Key AnswerDjunah ArellanoNo ratings yet

- BLR Prelims Quiz 1Document7 pagesBLR Prelims Quiz 1Djunah ArellanoNo ratings yet

- Final Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 2 Suggested Key AnswerDocument3 pagesFinal Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 2 Suggested Key AnswerDjunah ArellanoNo ratings yet

- AE 112 - Midterm Summative Assessment (Quiz 1) Suggested Answers and SolutionsDocument3 pagesAE 112 - Midterm Summative Assessment (Quiz 1) Suggested Answers and SolutionsDjunah ArellanoNo ratings yet

- BLR 211 - PdeDocument16 pagesBLR 211 - PdeDjunah ArellanoNo ratings yet

- BLR 211 - MdeDocument15 pagesBLR 211 - MdeDjunah ArellanoNo ratings yet

- BLR 211 - FdeDocument23 pagesBLR 211 - FdeDjunah Arellano100% (1)

- Arranz v. Manila Fidelity and Surety Co., Inc.Document2 pagesArranz v. Manila Fidelity and Surety Co., Inc.Ildefonso HernaezNo ratings yet

- PWC The Future of Financial ServicesDocument27 pagesPWC The Future of Financial ServicesPhương TrầnNo ratings yet

- LIC AAO 2016 Capsule by AffairscloudDocument84 pagesLIC AAO 2016 Capsule by AffairscloudRamesh RyNo ratings yet

- Rujukan: Jabatan Operasi Pelaburan Dan Pasaran Kewangan Bank Negara MalaysiaDocument1 pageRujukan: Jabatan Operasi Pelaburan Dan Pasaran Kewangan Bank Negara MalaysiaAry KurniaNo ratings yet

- RRB NTPC 4 Jan 2021 Answer Key With Question Paper (Released) : Check For Shift 1 and 2Document16 pagesRRB NTPC 4 Jan 2021 Answer Key With Question Paper (Released) : Check For Shift 1 and 2saranNo ratings yet

- TNJFU - Non-Teaching Positions - AdvertisementDocument2 pagesTNJFU - Non-Teaching Positions - AdvertisementGiridharan SubramaniamNo ratings yet

- Accounting For Crises: Nama MUHAMMAD DESTYAWAN (1500012328) Sri WahyuningsihDocument10 pagesAccounting For Crises: Nama MUHAMMAD DESTYAWAN (1500012328) Sri WahyuningsihMuhammad IwanNo ratings yet

- Bank of KhyberDocument63 pagesBank of KhyberSalman Khaliq BajwaNo ratings yet

- Form U Change of NameDocument2 pagesForm U Change of Namechief engineer CommercialNo ratings yet

- Finance Interview QuestionDocument41 pagesFinance Interview QuestionshuklashishNo ratings yet

- IRM Sessional Test Notes - Introduction To Risk and InsuranceDocument5 pagesIRM Sessional Test Notes - Introduction To Risk and InsuranceRupesh SharmaNo ratings yet

- Competative Profile Matrix Habib Bank Limited PakistanDocument4 pagesCompetative Profile Matrix Habib Bank Limited PakistanRaja Amir KhanNo ratings yet

- Interim Results June 2008Document12 pagesInterim Results June 2008Huseyin BozkinaNo ratings yet

- Ov QPR GIVBp at 5 Q8 MDocument15 pagesOv QPR GIVBp at 5 Q8 ManuranjankumarNo ratings yet

- Economics Mcqs For LecturerDocument8 pagesEconomics Mcqs For LecturerImran Khan Shar100% (1)

- Activity Based CostingDocument23 pagesActivity Based CostingLamhe Yasu0% (1)

- SVB Report 2022Document193 pagesSVB Report 2022iqbal maulanaNo ratings yet

- 7 Steps To Eliminate DebtDocument5 pages7 Steps To Eliminate DebtMirjana StefanovskiNo ratings yet

- Negotiable InstrumentsDocument60 pagesNegotiable InstrumentsTrem GallenteNo ratings yet

- Quiz 3Document5 pagesQuiz 3natashaNo ratings yet

- Questionnaire On Mutual FundsDocument5 pagesQuestionnaire On Mutual Fundsanushwarya80% (10)

- Tybcom Management AccoutingDocument6 pagesTybcom Management AccoutingavtaranNo ratings yet

- RCBC v. OdradaDocument28 pagesRCBC v. OdradaSabritoNo ratings yet

- Welcome To BRI Internet BankingDocument5 pagesWelcome To BRI Internet BankingLuru GratisanNo ratings yet

- Quotation of BMW 320d Luxury LineDocument2 pagesQuotation of BMW 320d Luxury Lineabhishek100% (1)

- Brand Development and Management Strategies in The Digital AgeDocument5 pagesBrand Development and Management Strategies in The Digital AgeRohanNo ratings yet

- Role of Merchant BanksDocument20 pagesRole of Merchant BanksSai Bhaskar Kannepalli100% (1)

- UCP Exam Review Consolidated Final (PDF) March 2023Document193 pagesUCP Exam Review Consolidated Final (PDF) March 2023enirhtacdiyezNo ratings yet