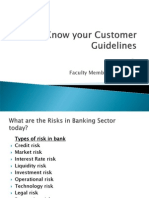

Kyc/Aml/Cft Policy: Presented by ROHIT KUMAR (PF 34282)

Kyc/Aml/Cft Policy: Presented by ROHIT KUMAR (PF 34282)

You might also like

- Certified AML - KYC Compliance OfficerDocument9 pagesCertified AML - KYC Compliance OfficerRicky MartinNo ratings yet

- Theories of Money SupplyDocument15 pagesTheories of Money SupplyAppan Kandala Vasudevachary100% (1)

- Kyc PPT CompleteDocument23 pagesKyc PPT CompleteNitin ChateNo ratings yet

- Zerodha PMLA PolicyDocument8 pagesZerodha PMLA PolicyAbhimanyu Yashwant AltekarNo ratings yet

- KYC HANDOUT 21 January 2021Document7 pagesKYC HANDOUT 21 January 2021RupamNo ratings yet

- Electronic Know-Your Customer (e-KYC)Document85 pagesElectronic Know-Your Customer (e-KYC)Chandrakanti SahooNo ratings yet

- Unit II Part 1 KYCDocument100 pagesUnit II Part 1 KYCramyaNo ratings yet

- What Is KYC PolicyDocument6 pagesWhat Is KYC Policyfariha khanamNo ratings yet

- 08L0767 Fy18-19 Kyc Aml CFT Fatca CRSDocument13 pages08L0767 Fy18-19 Kyc Aml CFT Fatca CRSabhi646son5124No ratings yet

- KYC NormsDocument38 pagesKYC Normsdranita@yahoo.com100% (2)

- Safeguards Balance Sheet MLDocument6 pagesSafeguards Balance Sheet MLRoshni 004No ratings yet

- Kyc Project ReportDocument12 pagesKyc Project Reportanam kazi100% (2)

- An Overview of Kyc NormsDocument5 pagesAn Overview of Kyc NormsArsh AhmedNo ratings yet

- Legal AspectsDocument38 pagesLegal AspectsAravind JayanNo ratings yet

- What Is KYC?Document12 pagesWhat Is KYC?dsdrddNo ratings yet

- 4 Banking Operations - AFB - Module DDocument44 pages4 Banking Operations - AFB - Module Dwaste mailNo ratings yet

- Kyc & AmlDocument149 pagesKyc & AmlKailash SharmaNo ratings yet

- KYCDocument82 pagesKYCDhruva Sareen100% (5)

- KYC, Internal Control and Preventive VigilanceDocument99 pagesKYC, Internal Control and Preventive VigilanceVivekSinghChand100% (2)

- CBMDocument30 pagesCBMPratik LawanaNo ratings yet

- What Is Know Your CustomerDocument9 pagesWhat Is Know Your CustomerAnaghaPuranikNo ratings yet

- KYCDocument2 pagesKYCNote10Pro ShiledarNo ratings yet

- AFB Short NotesDocument5 pagesAFB Short Notesstudy studyNo ratings yet

- KYC ProjectDocument40 pagesKYC Projectanon_292134566100% (2)

- Kyc & AmlDocument24 pagesKyc & AmlkallasanjayNo ratings yet

- Bim 3Document9 pagesBim 3Manas MohapatraNo ratings yet

- KYCDocument12 pagesKYCSiddhartha GhoshNo ratings yet

- AML Refresher COCDocument3 pagesAML Refresher COCakshay kasanaNo ratings yet

- AML and KYCDocument34 pagesAML and KYCKanika Dhingra0% (1)

- Kycamlpolicy 170116120359Document41 pagesKycamlpolicy 170116120359rahul.singh1No ratings yet

- Anti Money Laundering PolicyDocument45 pagesAnti Money Laundering PolicyAkash100% (1)

- KYC AML LatestDocument77 pagesKYC AML Latestbandari3943100% (1)

- Kyc FrameworkDocument4 pagesKyc FrameworkMary FergusonNo ratings yet

- Sound Mind Set Leads To Growth and ProsperityDocument87 pagesSound Mind Set Leads To Growth and ProsperityMahapatra MilonNo ratings yet

- Slide Set-3 KycDocument13 pagesSlide Set-3 Kycbipin kumarNo ratings yet

- Pathak Commitee ReportDocument2 pagesPathak Commitee ReportKunwarbir Singh lohatNo ratings yet

- Monetary AuthorityDocument13 pagesMonetary AuthoritySarthak Priyank VermaNo ratings yet

- Final PRJCTDocument27 pagesFinal PRJCTBilal AmjadNo ratings yet

- KycDocument47 pagesKycVinod TiwariNo ratings yet

- Master Key by AD PDFDocument76 pagesMaster Key by AD PDFpreeti.2405No ratings yet

- Ch5 PointsDocument22 pagesCh5 PointsHiruthik RajaNo ratings yet

- Kyc Aml and FatcaDocument42 pagesKyc Aml and Fatcajyos20201No ratings yet

- Anti Money LaunderingDocument4 pagesAnti Money LaunderingCHONG LI WENNo ratings yet

- Kyc - RbiDocument16 pagesKyc - RbiDebolina DasNo ratings yet

- Know Your Customer (Kyc) : Kyc-Aml-Cft Guidelines of RbiDocument5 pagesKnow Your Customer (Kyc) : Kyc-Aml-Cft Guidelines of RbiBhai ho to dodoNo ratings yet

- Module-2 Roll-49Document48 pagesModule-2 Roll-49SUBHECHHA MOHAPATRANo ratings yet

- FM 202 Finals3Document34 pagesFM 202 Finals3sudariodaisyre19No ratings yet

- Ombudsman, Universal Banking, KYCDocument3 pagesOmbudsman, Universal Banking, KYCseanmor111100% (2)

- Due DiligenceDocument7 pagesDue Diligenceanand guptaNo ratings yet

- Vijeta October 2022 - MDIDocument333 pagesVijeta October 2022 - MDIMihira SwarnaNo ratings yet

- Anti Money Laundering Policy: BackgroundDocument8 pagesAnti Money Laundering Policy: BackgroundalkasecuritiesNo ratings yet

- KYCDocument23 pagesKYCSunny GoelNo ratings yet

- Assurance and Attestation CheatsheetDocument4 pagesAssurance and Attestation CheatsheetrachmmmNo ratings yet

- Mastering Bookkeeping: Unveiling the Key to Financial SuccessFrom EverandMastering Bookkeeping: Unveiling the Key to Financial SuccessNo ratings yet

- Evaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersFrom EverandEvaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersNo ratings yet

- Evaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersFrom EverandEvaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersNo ratings yet

- Review of Some Online Banks and Visa/Master Cards IssuersFrom EverandReview of Some Online Banks and Visa/Master Cards IssuersNo ratings yet

- Textbook of Urgent Care Management: Chapter 13, Financial ManagementFrom EverandTextbook of Urgent Care Management: Chapter 13, Financial ManagementNo ratings yet

- Scss Closer Application Form-3Document1 pageScss Closer Application Form-3Rohit KumarNo ratings yet

- RB Chapter 3A-Savings Deposits - MITCDocument9 pagesRB Chapter 3A-Savings Deposits - MITCRohit KumarNo ratings yet

- Assignment - Group 3Document1 pageAssignment - Group 3Rohit KumarNo ratings yet

- Baltra Catalogues 2022-23 FinalDocument44 pagesBaltra Catalogues 2022-23 FinalRohit KumarNo ratings yet

- RB Chapter 1A - Lending PolicyDocument6 pagesRB Chapter 1A - Lending PolicyRohit KumarNo ratings yet

- RB Chapter 2A-Current Account-MITCDocument9 pagesRB Chapter 2A-Current Account-MITCRohit KumarNo ratings yet

- RB Chapter 2 - Current DepositsDocument3 pagesRB Chapter 2 - Current DepositsRohit KumarNo ratings yet

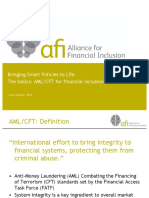

- Bringing Smart Policies To Life The Basics: AML/CFT For Financial InclusionDocument13 pagesBringing Smart Policies To Life The Basics: AML/CFT For Financial InclusionRohit KumarNo ratings yet

- 1bihar June English 52Document3 pages1bihar June English 52Rohit KumarNo ratings yet

- Scanned With CamscannerDocument7 pagesScanned With CamscannerRohit KumarNo ratings yet

- Reapp FinlDocument2 pagesReapp FinlRohit KumarNo ratings yet

- Buddhist Councils and Important TextsDocument3 pagesBuddhist Councils and Important TextsRohit KumarNo ratings yet

- Subhash Chandra BoseDocument3 pagesSubhash Chandra BoseRohit KumarNo ratings yet

- Home Rule Movement NCERT NotesDocument3 pagesHome Rule Movement NCERT NotesRohit KumarNo ratings yet

- Tipu SultanDocument3 pagesTipu SultanRohit KumarNo ratings yet

- Anglo Mysore War 431655090157974Document4 pagesAnglo Mysore War 431655090157974Rohit KumarNo ratings yet

- British Policy of Subsidiary Alliance Modern Indian History Notes For UPSCDocument2 pagesBritish Policy of Subsidiary Alliance Modern Indian History Notes For UPSCRohit KumarNo ratings yet

- Morley Minto Reforms Upsc Notes 921655090157974Document3 pagesMorley Minto Reforms Upsc Notes 921655090157974Rohit KumarNo ratings yet

- List of Viceroys in IndiaDocument3 pagesList of Viceroys in IndiaRohit KumarNo ratings yet

- Draft Invoice Botswana Rep OfficeDocument7 pagesDraft Invoice Botswana Rep OfficeVenkatramaniNo ratings yet

- Business Research ProposalDocument37 pagesBusiness Research Proposalobsinan dejeneNo ratings yet

- LBTRU00005805276 IT Certificate 2021-22Document2 pagesLBTRU00005805276 IT Certificate 2021-22siva kumar reddy kNo ratings yet

- MPay Solutions (2021) With Pricing and CommissionDocument44 pagesMPay Solutions (2021) With Pricing and CommissionMohammed NaflanNo ratings yet

- PNC Verification Form 0Document2 pagesPNC Verification Form 0Rabia Zafar100% (1)

- Schedule Yuran Sem 1 Sesi 20202021 MBADocument1 pageSchedule Yuran Sem 1 Sesi 20202021 MBAM NaszriNo ratings yet

- Brief History of Philippine MoneyDocument4 pagesBrief History of Philippine MoneyDanneth TabunoNo ratings yet

- SKCC 1Document1 pageSKCC 1barangaymaharlikawest017No ratings yet

- 0151xxxxxxxx6295 - 2023 12 01Document6 pages0151xxxxxxxx6295 - 2023 12 01George GeranisNo ratings yet

- Economics FinalDocument87 pagesEconomics FinalRavi Shankar VermaNo ratings yet

- Aggarwal 2018 - Sustainable Finance in Emerging Markets A Venture Capital Investment Decision DilemmaDocument13 pagesAggarwal 2018 - Sustainable Finance in Emerging Markets A Venture Capital Investment Decision DilemmaFaldi HarisNo ratings yet

- Fabm1 q3 Mod9 TrialbalanceDocument11 pagesFabm1 q3 Mod9 TrialbalanceXedric JuantaNo ratings yet

- What Is A Treasury BondDocument12 pagesWhat Is A Treasury Bondmorris yenenehNo ratings yet

- 03 Takaful MAYBANK EZYPAY Application Form V1.0 2018Document2 pages03 Takaful MAYBANK EZYPAY Application Form V1.0 2018UstazFaizalAriffinOriginalNo ratings yet

- Jayesh Gupta PDF 1Document12 pagesJayesh Gupta PDF 1Jayesh GuptaNo ratings yet

- Annual Information Statement (AIS) : ATLPK5075H XXXX XXXX 8789 Rajiv KarnDocument2 pagesAnnual Information Statement (AIS) : ATLPK5075H XXXX XXXX 8789 Rajiv Karndevesh mishraNo ratings yet

- L7796 Otm Workbook KenyaDocument80 pagesL7796 Otm Workbook Kenyaangela mwangiNo ratings yet

- Sonali Bank Term PaperDocument6 pagesSonali Bank Term Paperafmzvaeeowzqyv100% (1)

- CSEC POA January 2018 P1Document10 pagesCSEC POA January 2018 P1Boppy VevoNo ratings yet

- Study - Id116072 - Digital Payments in Vietnam PDFDocument44 pagesStudy - Id116072 - Digital Payments in Vietnam PDFhà thànhNo ratings yet

- FINMAN Finals Reviewer by Diamla Foronda GanDocument35 pagesFINMAN Finals Reviewer by Diamla Foronda Ganmarcgabriel.cortez.acctNo ratings yet

- Group TaskDocument5 pagesGroup TaskNiraj MantriNo ratings yet

- FA Lesson 1 Checking AccountDocument5 pagesFA Lesson 1 Checking Accountludy louisNo ratings yet

- Community Initiatives in The Charlotte MSA and North CarolinaDocument5 pagesCommunity Initiatives in The Charlotte MSA and North CarolinaWCNC DigitalNo ratings yet

- HS 2nd Year Finance Project 2023Document7 pagesHS 2nd Year Finance Project 2023jnsz7t5bpqNo ratings yet

- Accenture Banking New Digital Opportunities Unsecured LendingDocument12 pagesAccenture Banking New Digital Opportunities Unsecured LendingFUDANI MANISHANo ratings yet

- GEC Elect 2 Module 4Document10 pagesGEC Elect 2 Module 4Aira Mae Quinones OrendainNo ratings yet

- BÀI TẬP BỔ SUNG - CHƯƠNG 1-5Document46 pagesBÀI TẬP BỔ SUNG - CHƯƠNG 1-5Lâm Thị Như ÝNo ratings yet

- HLB Receipt-2023-03-08 2Document2 pagesHLB Receipt-2023-03-08 2zu hairyNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Certified AML - KYC Compliance OfficerDocument9 pagesCertified AML - KYC Compliance OfficerRicky MartinNo ratings yet

- Theories of Money SupplyDocument15 pagesTheories of Money SupplyAppan Kandala Vasudevachary100% (1)

- Kyc PPT CompleteDocument23 pagesKyc PPT CompleteNitin ChateNo ratings yet

- Zerodha PMLA PolicyDocument8 pagesZerodha PMLA PolicyAbhimanyu Yashwant AltekarNo ratings yet

- KYC HANDOUT 21 January 2021Document7 pagesKYC HANDOUT 21 January 2021RupamNo ratings yet

- Electronic Know-Your Customer (e-KYC)Document85 pagesElectronic Know-Your Customer (e-KYC)Chandrakanti SahooNo ratings yet

- Unit II Part 1 KYCDocument100 pagesUnit II Part 1 KYCramyaNo ratings yet

- What Is KYC PolicyDocument6 pagesWhat Is KYC Policyfariha khanamNo ratings yet

- 08L0767 Fy18-19 Kyc Aml CFT Fatca CRSDocument13 pages08L0767 Fy18-19 Kyc Aml CFT Fatca CRSabhi646son5124No ratings yet

- KYC NormsDocument38 pagesKYC Normsdranita@yahoo.com100% (2)

- Safeguards Balance Sheet MLDocument6 pagesSafeguards Balance Sheet MLRoshni 004No ratings yet

- Kyc Project ReportDocument12 pagesKyc Project Reportanam kazi100% (2)

- An Overview of Kyc NormsDocument5 pagesAn Overview of Kyc NormsArsh AhmedNo ratings yet

- Legal AspectsDocument38 pagesLegal AspectsAravind JayanNo ratings yet

- What Is KYC?Document12 pagesWhat Is KYC?dsdrddNo ratings yet

- 4 Banking Operations - AFB - Module DDocument44 pages4 Banking Operations - AFB - Module Dwaste mailNo ratings yet

- Kyc & AmlDocument149 pagesKyc & AmlKailash SharmaNo ratings yet

- KYCDocument82 pagesKYCDhruva Sareen100% (5)

- KYC, Internal Control and Preventive VigilanceDocument99 pagesKYC, Internal Control and Preventive VigilanceVivekSinghChand100% (2)

- CBMDocument30 pagesCBMPratik LawanaNo ratings yet

- What Is Know Your CustomerDocument9 pagesWhat Is Know Your CustomerAnaghaPuranikNo ratings yet

- KYCDocument2 pagesKYCNote10Pro ShiledarNo ratings yet

- AFB Short NotesDocument5 pagesAFB Short Notesstudy studyNo ratings yet

- KYC ProjectDocument40 pagesKYC Projectanon_292134566100% (2)

- Kyc & AmlDocument24 pagesKyc & AmlkallasanjayNo ratings yet

- Bim 3Document9 pagesBim 3Manas MohapatraNo ratings yet

- KYCDocument12 pagesKYCSiddhartha GhoshNo ratings yet

- AML Refresher COCDocument3 pagesAML Refresher COCakshay kasanaNo ratings yet

- AML and KYCDocument34 pagesAML and KYCKanika Dhingra0% (1)

- Kycamlpolicy 170116120359Document41 pagesKycamlpolicy 170116120359rahul.singh1No ratings yet

- Anti Money Laundering PolicyDocument45 pagesAnti Money Laundering PolicyAkash100% (1)

- KYC AML LatestDocument77 pagesKYC AML Latestbandari3943100% (1)

- Kyc FrameworkDocument4 pagesKyc FrameworkMary FergusonNo ratings yet

- Sound Mind Set Leads To Growth and ProsperityDocument87 pagesSound Mind Set Leads To Growth and ProsperityMahapatra MilonNo ratings yet

- Slide Set-3 KycDocument13 pagesSlide Set-3 Kycbipin kumarNo ratings yet

- Pathak Commitee ReportDocument2 pagesPathak Commitee ReportKunwarbir Singh lohatNo ratings yet

- Monetary AuthorityDocument13 pagesMonetary AuthoritySarthak Priyank VermaNo ratings yet

- Final PRJCTDocument27 pagesFinal PRJCTBilal AmjadNo ratings yet

- KycDocument47 pagesKycVinod TiwariNo ratings yet

- Master Key by AD PDFDocument76 pagesMaster Key by AD PDFpreeti.2405No ratings yet

- Ch5 PointsDocument22 pagesCh5 PointsHiruthik RajaNo ratings yet

- Kyc Aml and FatcaDocument42 pagesKyc Aml and Fatcajyos20201No ratings yet

- Anti Money LaunderingDocument4 pagesAnti Money LaunderingCHONG LI WENNo ratings yet

- Kyc - RbiDocument16 pagesKyc - RbiDebolina DasNo ratings yet

- Know Your Customer (Kyc) : Kyc-Aml-Cft Guidelines of RbiDocument5 pagesKnow Your Customer (Kyc) : Kyc-Aml-Cft Guidelines of RbiBhai ho to dodoNo ratings yet

- Module-2 Roll-49Document48 pagesModule-2 Roll-49SUBHECHHA MOHAPATRANo ratings yet

- FM 202 Finals3Document34 pagesFM 202 Finals3sudariodaisyre19No ratings yet

- Ombudsman, Universal Banking, KYCDocument3 pagesOmbudsman, Universal Banking, KYCseanmor111100% (2)

- Due DiligenceDocument7 pagesDue Diligenceanand guptaNo ratings yet

- Vijeta October 2022 - MDIDocument333 pagesVijeta October 2022 - MDIMihira SwarnaNo ratings yet

- Anti Money Laundering Policy: BackgroundDocument8 pagesAnti Money Laundering Policy: BackgroundalkasecuritiesNo ratings yet

- KYCDocument23 pagesKYCSunny GoelNo ratings yet

- Assurance and Attestation CheatsheetDocument4 pagesAssurance and Attestation CheatsheetrachmmmNo ratings yet

- Mastering Bookkeeping: Unveiling the Key to Financial SuccessFrom EverandMastering Bookkeeping: Unveiling the Key to Financial SuccessNo ratings yet

- Evaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersFrom EverandEvaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersNo ratings yet

- Evaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersFrom EverandEvaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersNo ratings yet

- Review of Some Online Banks and Visa/Master Cards IssuersFrom EverandReview of Some Online Banks and Visa/Master Cards IssuersNo ratings yet

- Textbook of Urgent Care Management: Chapter 13, Financial ManagementFrom EverandTextbook of Urgent Care Management: Chapter 13, Financial ManagementNo ratings yet

- Scss Closer Application Form-3Document1 pageScss Closer Application Form-3Rohit KumarNo ratings yet

- RB Chapter 3A-Savings Deposits - MITCDocument9 pagesRB Chapter 3A-Savings Deposits - MITCRohit KumarNo ratings yet

- Assignment - Group 3Document1 pageAssignment - Group 3Rohit KumarNo ratings yet

- Baltra Catalogues 2022-23 FinalDocument44 pagesBaltra Catalogues 2022-23 FinalRohit KumarNo ratings yet

- RB Chapter 1A - Lending PolicyDocument6 pagesRB Chapter 1A - Lending PolicyRohit KumarNo ratings yet

- RB Chapter 2A-Current Account-MITCDocument9 pagesRB Chapter 2A-Current Account-MITCRohit KumarNo ratings yet

- RB Chapter 2 - Current DepositsDocument3 pagesRB Chapter 2 - Current DepositsRohit KumarNo ratings yet

- Bringing Smart Policies To Life The Basics: AML/CFT For Financial InclusionDocument13 pagesBringing Smart Policies To Life The Basics: AML/CFT For Financial InclusionRohit KumarNo ratings yet

- 1bihar June English 52Document3 pages1bihar June English 52Rohit KumarNo ratings yet

- Scanned With CamscannerDocument7 pagesScanned With CamscannerRohit KumarNo ratings yet

- Reapp FinlDocument2 pagesReapp FinlRohit KumarNo ratings yet

- Buddhist Councils and Important TextsDocument3 pagesBuddhist Councils and Important TextsRohit KumarNo ratings yet

- Subhash Chandra BoseDocument3 pagesSubhash Chandra BoseRohit KumarNo ratings yet

- Home Rule Movement NCERT NotesDocument3 pagesHome Rule Movement NCERT NotesRohit KumarNo ratings yet

- Tipu SultanDocument3 pagesTipu SultanRohit KumarNo ratings yet

- Anglo Mysore War 431655090157974Document4 pagesAnglo Mysore War 431655090157974Rohit KumarNo ratings yet

- British Policy of Subsidiary Alliance Modern Indian History Notes For UPSCDocument2 pagesBritish Policy of Subsidiary Alliance Modern Indian History Notes For UPSCRohit KumarNo ratings yet

- Morley Minto Reforms Upsc Notes 921655090157974Document3 pagesMorley Minto Reforms Upsc Notes 921655090157974Rohit KumarNo ratings yet

- List of Viceroys in IndiaDocument3 pagesList of Viceroys in IndiaRohit KumarNo ratings yet

- Draft Invoice Botswana Rep OfficeDocument7 pagesDraft Invoice Botswana Rep OfficeVenkatramaniNo ratings yet

- Business Research ProposalDocument37 pagesBusiness Research Proposalobsinan dejeneNo ratings yet

- LBTRU00005805276 IT Certificate 2021-22Document2 pagesLBTRU00005805276 IT Certificate 2021-22siva kumar reddy kNo ratings yet

- MPay Solutions (2021) With Pricing and CommissionDocument44 pagesMPay Solutions (2021) With Pricing and CommissionMohammed NaflanNo ratings yet

- PNC Verification Form 0Document2 pagesPNC Verification Form 0Rabia Zafar100% (1)

- Schedule Yuran Sem 1 Sesi 20202021 MBADocument1 pageSchedule Yuran Sem 1 Sesi 20202021 MBAM NaszriNo ratings yet

- Brief History of Philippine MoneyDocument4 pagesBrief History of Philippine MoneyDanneth TabunoNo ratings yet

- SKCC 1Document1 pageSKCC 1barangaymaharlikawest017No ratings yet

- 0151xxxxxxxx6295 - 2023 12 01Document6 pages0151xxxxxxxx6295 - 2023 12 01George GeranisNo ratings yet

- Economics FinalDocument87 pagesEconomics FinalRavi Shankar VermaNo ratings yet

- Aggarwal 2018 - Sustainable Finance in Emerging Markets A Venture Capital Investment Decision DilemmaDocument13 pagesAggarwal 2018 - Sustainable Finance in Emerging Markets A Venture Capital Investment Decision DilemmaFaldi HarisNo ratings yet

- Fabm1 q3 Mod9 TrialbalanceDocument11 pagesFabm1 q3 Mod9 TrialbalanceXedric JuantaNo ratings yet

- What Is A Treasury BondDocument12 pagesWhat Is A Treasury Bondmorris yenenehNo ratings yet

- 03 Takaful MAYBANK EZYPAY Application Form V1.0 2018Document2 pages03 Takaful MAYBANK EZYPAY Application Form V1.0 2018UstazFaizalAriffinOriginalNo ratings yet

- Jayesh Gupta PDF 1Document12 pagesJayesh Gupta PDF 1Jayesh GuptaNo ratings yet

- Annual Information Statement (AIS) : ATLPK5075H XXXX XXXX 8789 Rajiv KarnDocument2 pagesAnnual Information Statement (AIS) : ATLPK5075H XXXX XXXX 8789 Rajiv Karndevesh mishraNo ratings yet

- L7796 Otm Workbook KenyaDocument80 pagesL7796 Otm Workbook Kenyaangela mwangiNo ratings yet

- Sonali Bank Term PaperDocument6 pagesSonali Bank Term Paperafmzvaeeowzqyv100% (1)

- CSEC POA January 2018 P1Document10 pagesCSEC POA January 2018 P1Boppy VevoNo ratings yet

- Study - Id116072 - Digital Payments in Vietnam PDFDocument44 pagesStudy - Id116072 - Digital Payments in Vietnam PDFhà thànhNo ratings yet

- FINMAN Finals Reviewer by Diamla Foronda GanDocument35 pagesFINMAN Finals Reviewer by Diamla Foronda Ganmarcgabriel.cortez.acctNo ratings yet

- Group TaskDocument5 pagesGroup TaskNiraj MantriNo ratings yet

- FA Lesson 1 Checking AccountDocument5 pagesFA Lesson 1 Checking Accountludy louisNo ratings yet

- Community Initiatives in The Charlotte MSA and North CarolinaDocument5 pagesCommunity Initiatives in The Charlotte MSA and North CarolinaWCNC DigitalNo ratings yet

- HS 2nd Year Finance Project 2023Document7 pagesHS 2nd Year Finance Project 2023jnsz7t5bpqNo ratings yet

- Accenture Banking New Digital Opportunities Unsecured LendingDocument12 pagesAccenture Banking New Digital Opportunities Unsecured LendingFUDANI MANISHANo ratings yet

- GEC Elect 2 Module 4Document10 pagesGEC Elect 2 Module 4Aira Mae Quinones OrendainNo ratings yet

- BÀI TẬP BỔ SUNG - CHƯƠNG 1-5Document46 pagesBÀI TẬP BỔ SUNG - CHƯƠNG 1-5Lâm Thị Như ÝNo ratings yet

- HLB Receipt-2023-03-08 2Document2 pagesHLB Receipt-2023-03-08 2zu hairyNo ratings yet