Ias 16

Ias 16

You might also like

- Daikin VRV Handbook - OHUS08-1FCU-bDocument72 pagesDaikin VRV Handbook - OHUS08-1FCU-bthanhthuan100% (1)

- IAS-16 (Property, Plant & Equipment)Document20 pagesIAS-16 (Property, Plant & Equipment)Nazmul HaqueNo ratings yet

- PP (A) - Lect 2 - Ias 16 PpeDocument19 pagesPP (A) - Lect 2 - Ias 16 Ppekevin digumberNo ratings yet

- IAS 16 Property, Plant and EquipmentDocument4 pagesIAS 16 Property, Plant and EquipmentSelva Bavani SelwaduraiNo ratings yet

- Unit 1 - IAS 16: Property, Plant and Equipment Objective: Advanced Financial ReportingDocument18 pagesUnit 1 - IAS 16: Property, Plant and Equipment Objective: Advanced Financial ReportingRobin G'koolNo ratings yet

- IAS#16Document17 pagesIAS#16Shah KamalNo ratings yet

- ClassNotes IAS 16 PPEDocument2 pagesClassNotes IAS 16 PPEKhadejai LairdNo ratings yet

- IAS16 Defines Property, Plant and Equipment As "Tangible Items ThatDocument35 pagesIAS16 Defines Property, Plant and Equipment As "Tangible Items ThatMo HachimNo ratings yet

- Property, Plant and EquipmentDocument6 pagesProperty, Plant and EquipmenthemantbaidNo ratings yet

- Property, Plant and EquipmentDocument8 pagesProperty, Plant and EquipmentMark John Malazo RiveraNo ratings yet

- Theory of Accounting - SUMMARY of PPEDocument15 pagesTheory of Accounting - SUMMARY of PPESteven Chou100% (2)

- IAS 16 SummaryDocument7 pagesIAS 16 SummaryCharmaine LogaNo ratings yet

- These Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoDocument8 pagesThese Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoEki OmallaoNo ratings yet

- Property, Plant and EquipmentDocument35 pagesProperty, Plant and EquipmentNimona BeyeneNo ratings yet

- 12 PPE Part 1 With AnswersDocument13 pages12 PPE Part 1 With AnswersZatsumono YamamotoNo ratings yet

- Property, Plant and Equipment: By:-Yohannes Negatu (Acca, Dipifr)Document37 pagesProperty, Plant and Equipment: By:-Yohannes Negatu (Acca, Dipifr)Eshetie Mekonene AmareNo ratings yet

- TA07b - Current AssetsDocument11 pagesTA07b - Current AssetsMarsha Sabrina LillahNo ratings yet

- Week 10 - 02 - Module 23 - Property, Plant & Equipment (Part 2)Document10 pagesWeek 10 - 02 - Module 23 - Property, Plant & Equipment (Part 2)지마리No ratings yet

- Ias 16 PropertyDocument11 pagesIas 16 PropertyFolarin EmmanuelNo ratings yet

- Ias 16 Property, Plant & Equipment: Adeel SaleemDocument20 pagesIas 16 Property, Plant & Equipment: Adeel SaleemAtif RehmanNo ratings yet

- IAS16Document2 pagesIAS16Atif RehmanNo ratings yet

- Discontinued Operations: Property, Plant and Equipment 2020-SPN PART 1Document13 pagesDiscontinued Operations: Property, Plant and Equipment 2020-SPN PART 1Mich ClementeNo ratings yet

- Summary of IAS 16Document5 pagesSummary of IAS 16Laskar REAZNo ratings yet

- Accounting For PPEDocument4 pagesAccounting For PPEMaureen Derial PantaNo ratings yet

- Ias 16Document3 pagesIas 16CandyNo ratings yet

- Summary of Pas 16 NDocument5 pagesSummary of Pas 16 NJenny Hermosado100% (1)

- Ias 16 - PpeDocument4 pagesIas 16 - Ppecar itselfNo ratings yet

- Ias16, 23, 36, 38, 40 and Ifrs 3Document71 pagesIas16, 23, 36, 38, 40 and Ifrs 3mulualemNo ratings yet

- Ias 16Document26 pagesIas 16Niharika MishraNo ratings yet

- Technical SummaryDocument2 pagesTechnical Summarysza_13100% (2)

- IAS 16: Property Plant and Equipment Objective of IAS 16Document5 pagesIAS 16: Property Plant and Equipment Objective of IAS 16Joseph Gerald M. ArcegaNo ratings yet

- Pas 16 - PpeDocument24 pagesPas 16 - PpeNikki Ysabel RedNo ratings yet

- Pas 16 Property, Plant and EquipmentDocument2 pagesPas 16 Property, Plant and Equipmentamber_harthartNo ratings yet

- Ias 16Document7 pagesIas 16Baqar BaigNo ratings yet

- Indian Accounting Standard 16 Property, Plant & Equipment: By: Rahul DabralDocument9 pagesIndian Accounting Standard 16 Property, Plant & Equipment: By: Rahul DabralMangala BorkarNo ratings yet

- Nepal Accounting Standards On Property, Plant and Equipment: Initial Cost 11 Subsequent Cost 12-14Document24 pagesNepal Accounting Standards On Property, Plant and Equipment: Initial Cost 11 Subsequent Cost 12-14Gemini_0804No ratings yet

- Property, Plant and Equipment (IAS 16) : Haroon Arshad Butt IcmapDocument16 pagesProperty, Plant and Equipment (IAS 16) : Haroon Arshad Butt IcmapHaroon A ButtNo ratings yet

- Ias 16Document9 pagesIas 16ADEYANJU AKEEMNo ratings yet

- Ias 38Document43 pagesIas 38khan_ssNo ratings yet

- Ias 16 & Ias 40Document47 pagesIas 16 & Ias 40Etiel Films / ኢትኤል ፊልሞች100% (1)

- Ias 16Document5 pagesIas 16thenikkitrNo ratings yet

- Pas 16Document30 pagesPas 16Hannah Mae D. LozanoNo ratings yet

- Summary PpeDocument8 pagesSummary PpeJenilyn CalaraNo ratings yet

- Property, Plant and Equipment Are Tangible Items ThatDocument2 pagesProperty, Plant and Equipment Are Tangible Items ThatnasirNo ratings yet

- IAS 16 PropertyDocument6 pagesIAS 16 PropertyMuhammad Salman RasheedNo ratings yet

- Ques. 1. Peterlee (A) - Purpose and Authoritative Status of The FrameworkDocument7 pagesQues. 1. Peterlee (A) - Purpose and Authoritative Status of The FrameworkJulet Harris-TopeyNo ratings yet

- Ias 16 PropertyDocument6 pagesIas 16 PropertyAnjas A. M. TyasNo ratings yet

- Fair ValueDocument3 pagesFair ValueHisham MalikNo ratings yet

- Property Plant and EquipmentsDocument9 pagesProperty Plant and EquipmentsWize TreelerNo ratings yet

- Ias 16 Property Plant Equipment v1 080713Document7 pagesIas 16 Property Plant Equipment v1 080713Phebieon MukwenhaNo ratings yet

- Unit 1 and 2Document7 pagesUnit 1 and 2missyemylia27novNo ratings yet

- PPE Theory-DepDocument5 pagesPPE Theory-DepDibyansu KumarNo ratings yet

- Accounting For Property Plant and EquipmentDocument6 pagesAccounting For Property Plant and EquipmentmostafaNo ratings yet

- Historical Cost of Property, Plant and EquipmentDocument9 pagesHistorical Cost of Property, Plant and EquipmentChinchin Ilagan DatayloNo ratings yet

- IND AS-16 Property, Plant and Equipment: Measurement of PpeDocument3 pagesIND AS-16 Property, Plant and Equipment: Measurement of PpeHimank SinglaNo ratings yet

- International Accounting Standard 16 Property, Plant and EquipmentDocument29 pagesInternational Accounting Standard 16 Property, Plant and EquipmentAbdullah Shaker TahaNo ratings yet

- BA 114.1 Handout On PPEDocument5 pagesBA 114.1 Handout On PPEHuarde SophiaNo ratings yet

- Pas 16 - Property Plant and EquipmentDocument4 pagesPas 16 - Property Plant and EquipmentJessie ForpublicuseNo ratings yet

- IAS 41 - AgricultureDocument17 pagesIAS 41 - AgricultureArshad BhuttaNo ratings yet

- IAS 38 - Intangible AssetsDocument27 pagesIAS 38 - Intangible AssetsArshad BhuttaNo ratings yet

- IFRS 5 - Non - Current Assets Held For Sale and Discontinued OperationsDocument16 pagesIFRS 5 - Non - Current Assets Held For Sale and Discontinued OperationsArshad BhuttaNo ratings yet

- IAS 40 - Investment PropertyDocument19 pagesIAS 40 - Investment PropertyArshad BhuttaNo ratings yet

- Route 22 23 September 2023Document3 pagesRoute 22 23 September 2023api-523195650No ratings yet

- Kluster Kimpalan Julai 2018Document6 pagesKluster Kimpalan Julai 2018Ajie Fikri FahamiNo ratings yet

- Earth Sci Module 8Document10 pagesEarth Sci Module 8Tom AngNo ratings yet

- CAPITALGAINS 3rdsep PDFDocument202 pagesCAPITALGAINS 3rdsep PDFPhani Kumar SomarajupalliNo ratings yet

- Future of EA - 269850Document14 pagesFuture of EA - 269850Renato Cardoso BottoNo ratings yet

- Ignition System: Engine Control (ECM)Document1 pageIgnition System: Engine Control (ECM)Rafael Alejandro ReyesNo ratings yet

- Activity Proposal-Stakeholders Forum 2Document6 pagesActivity Proposal-Stakeholders Forum 2Rob MachiavelliNo ratings yet

- Download: Setting Goals and ObjectivesDocument4 pagesDownload: Setting Goals and ObjectivesJacques VisserNo ratings yet

- FP75E eDocument4 pagesFP75E estar990No ratings yet

- Z VF-S15 PIDcontrol-InstrMan Neutral e E6581879Document23 pagesZ VF-S15 PIDcontrol-InstrMan Neutral e E6581879mdtabanioNo ratings yet

- 13 Electrical Pole's TrasverseDocument7 pages13 Electrical Pole's TrasverseReza PahlepiNo ratings yet

- Peralatan KantorDocument47 pagesPeralatan KantorEva SiswantiNo ratings yet

- MDP43887 Mileage Warranty Flyer Quick GuideDocument2 pagesMDP43887 Mileage Warranty Flyer Quick GuideScenic777No ratings yet

- 2017 Winter Model Answer PaperDocument21 pages2017 Winter Model Answer PaperjohnNo ratings yet

- Manila Prince Hotel vs. GSISDocument5 pagesManila Prince Hotel vs. GSISFenina ReyesNo ratings yet

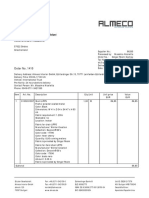

- B 1410 - B&N Contract Furniture S.A. - Almeco Interior GMBHDocument2 pagesB 1410 - B&N Contract Furniture S.A. - Almeco Interior GMBHmaxNo ratings yet

- Application For Electronic Clearance Service (Ecs)Document2 pagesApplication For Electronic Clearance Service (Ecs)vijayindia87No ratings yet

- Human Resource Management 14th Edition Mondy Solutions Manual 1Document17 pagesHuman Resource Management 14th Edition Mondy Solutions Manual 1freida100% (44)

- GC TodayDocument31 pagesGC TodayBrayan GuzmanNo ratings yet

- New Microsoft Office Excel WorksheetDocument12 pagesNew Microsoft Office Excel WorksheetRam Krishna AdhikariNo ratings yet

- Secdocument 5193Document89 pagesSecdocument 5193keith.fairley123No ratings yet

- UPSE Discussion Paper On Maharlika FundDocument28 pagesUPSE Discussion Paper On Maharlika FundjosnixNo ratings yet

- C3h - 14 MERALCO v. QuisumbingDocument2 pagesC3h - 14 MERALCO v. QuisumbingAaron AristonNo ratings yet

- Japanese Depreciable Assets Tax Summary Report: No Data FoundDocument1 pageJapanese Depreciable Assets Tax Summary Report: No Data FoundrpillzNo ratings yet

- Petitioner Respondent: Ivq Land Holdings, Inc.Document15 pagesPetitioner Respondent: Ivq Land Holdings, Inc.Em-em DomingoNo ratings yet

- Hashimoto'S: ProtocolDocument13 pagesHashimoto'S: ProtocolNatasa EricNo ratings yet

- 372A Inter-Corporate Loans & InvestmentsDocument2 pages372A Inter-Corporate Loans & Investmentslegendstillalive4826No ratings yet

- 1 PDFDocument53 pages1 PDFChelle BelenzoNo ratings yet

- Unit Ii Inheritance and Interfaces: CS8392 /object Oriented ProgrammingDocument30 pagesUnit Ii Inheritance and Interfaces: CS8392 /object Oriented ProgrammingJhonNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Daikin VRV Handbook - OHUS08-1FCU-bDocument72 pagesDaikin VRV Handbook - OHUS08-1FCU-bthanhthuan100% (1)

- IAS-16 (Property, Plant & Equipment)Document20 pagesIAS-16 (Property, Plant & Equipment)Nazmul HaqueNo ratings yet

- PP (A) - Lect 2 - Ias 16 PpeDocument19 pagesPP (A) - Lect 2 - Ias 16 Ppekevin digumberNo ratings yet

- IAS 16 Property, Plant and EquipmentDocument4 pagesIAS 16 Property, Plant and EquipmentSelva Bavani SelwaduraiNo ratings yet

- Unit 1 - IAS 16: Property, Plant and Equipment Objective: Advanced Financial ReportingDocument18 pagesUnit 1 - IAS 16: Property, Plant and Equipment Objective: Advanced Financial ReportingRobin G'koolNo ratings yet

- IAS#16Document17 pagesIAS#16Shah KamalNo ratings yet

- ClassNotes IAS 16 PPEDocument2 pagesClassNotes IAS 16 PPEKhadejai LairdNo ratings yet

- IAS16 Defines Property, Plant and Equipment As "Tangible Items ThatDocument35 pagesIAS16 Defines Property, Plant and Equipment As "Tangible Items ThatMo HachimNo ratings yet

- Property, Plant and EquipmentDocument6 pagesProperty, Plant and EquipmenthemantbaidNo ratings yet

- Property, Plant and EquipmentDocument8 pagesProperty, Plant and EquipmentMark John Malazo RiveraNo ratings yet

- Theory of Accounting - SUMMARY of PPEDocument15 pagesTheory of Accounting - SUMMARY of PPESteven Chou100% (2)

- IAS 16 SummaryDocument7 pagesIAS 16 SummaryCharmaine LogaNo ratings yet

- These Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoDocument8 pagesThese Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoEki OmallaoNo ratings yet

- Property, Plant and EquipmentDocument35 pagesProperty, Plant and EquipmentNimona BeyeneNo ratings yet

- 12 PPE Part 1 With AnswersDocument13 pages12 PPE Part 1 With AnswersZatsumono YamamotoNo ratings yet

- Property, Plant and Equipment: By:-Yohannes Negatu (Acca, Dipifr)Document37 pagesProperty, Plant and Equipment: By:-Yohannes Negatu (Acca, Dipifr)Eshetie Mekonene AmareNo ratings yet

- TA07b - Current AssetsDocument11 pagesTA07b - Current AssetsMarsha Sabrina LillahNo ratings yet

- Week 10 - 02 - Module 23 - Property, Plant & Equipment (Part 2)Document10 pagesWeek 10 - 02 - Module 23 - Property, Plant & Equipment (Part 2)지마리No ratings yet

- Ias 16 PropertyDocument11 pagesIas 16 PropertyFolarin EmmanuelNo ratings yet

- Ias 16 Property, Plant & Equipment: Adeel SaleemDocument20 pagesIas 16 Property, Plant & Equipment: Adeel SaleemAtif RehmanNo ratings yet

- IAS16Document2 pagesIAS16Atif RehmanNo ratings yet

- Discontinued Operations: Property, Plant and Equipment 2020-SPN PART 1Document13 pagesDiscontinued Operations: Property, Plant and Equipment 2020-SPN PART 1Mich ClementeNo ratings yet

- Summary of IAS 16Document5 pagesSummary of IAS 16Laskar REAZNo ratings yet

- Accounting For PPEDocument4 pagesAccounting For PPEMaureen Derial PantaNo ratings yet

- Ias 16Document3 pagesIas 16CandyNo ratings yet

- Summary of Pas 16 NDocument5 pagesSummary of Pas 16 NJenny Hermosado100% (1)

- Ias 16 - PpeDocument4 pagesIas 16 - Ppecar itselfNo ratings yet

- Ias16, 23, 36, 38, 40 and Ifrs 3Document71 pagesIas16, 23, 36, 38, 40 and Ifrs 3mulualemNo ratings yet

- Ias 16Document26 pagesIas 16Niharika MishraNo ratings yet

- Technical SummaryDocument2 pagesTechnical Summarysza_13100% (2)

- IAS 16: Property Plant and Equipment Objective of IAS 16Document5 pagesIAS 16: Property Plant and Equipment Objective of IAS 16Joseph Gerald M. ArcegaNo ratings yet

- Pas 16 - PpeDocument24 pagesPas 16 - PpeNikki Ysabel RedNo ratings yet

- Pas 16 Property, Plant and EquipmentDocument2 pagesPas 16 Property, Plant and Equipmentamber_harthartNo ratings yet

- Ias 16Document7 pagesIas 16Baqar BaigNo ratings yet

- Indian Accounting Standard 16 Property, Plant & Equipment: By: Rahul DabralDocument9 pagesIndian Accounting Standard 16 Property, Plant & Equipment: By: Rahul DabralMangala BorkarNo ratings yet

- Nepal Accounting Standards On Property, Plant and Equipment: Initial Cost 11 Subsequent Cost 12-14Document24 pagesNepal Accounting Standards On Property, Plant and Equipment: Initial Cost 11 Subsequent Cost 12-14Gemini_0804No ratings yet

- Property, Plant and Equipment (IAS 16) : Haroon Arshad Butt IcmapDocument16 pagesProperty, Plant and Equipment (IAS 16) : Haroon Arshad Butt IcmapHaroon A ButtNo ratings yet

- Ias 16Document9 pagesIas 16ADEYANJU AKEEMNo ratings yet

- Ias 38Document43 pagesIas 38khan_ssNo ratings yet

- Ias 16 & Ias 40Document47 pagesIas 16 & Ias 40Etiel Films / ኢትኤል ፊልሞች100% (1)

- Ias 16Document5 pagesIas 16thenikkitrNo ratings yet

- Pas 16Document30 pagesPas 16Hannah Mae D. LozanoNo ratings yet

- Summary PpeDocument8 pagesSummary PpeJenilyn CalaraNo ratings yet

- Property, Plant and Equipment Are Tangible Items ThatDocument2 pagesProperty, Plant and Equipment Are Tangible Items ThatnasirNo ratings yet

- IAS 16 PropertyDocument6 pagesIAS 16 PropertyMuhammad Salman RasheedNo ratings yet

- Ques. 1. Peterlee (A) - Purpose and Authoritative Status of The FrameworkDocument7 pagesQues. 1. Peterlee (A) - Purpose and Authoritative Status of The FrameworkJulet Harris-TopeyNo ratings yet

- Ias 16 PropertyDocument6 pagesIas 16 PropertyAnjas A. M. TyasNo ratings yet

- Fair ValueDocument3 pagesFair ValueHisham MalikNo ratings yet

- Property Plant and EquipmentsDocument9 pagesProperty Plant and EquipmentsWize TreelerNo ratings yet

- Ias 16 Property Plant Equipment v1 080713Document7 pagesIas 16 Property Plant Equipment v1 080713Phebieon MukwenhaNo ratings yet

- Unit 1 and 2Document7 pagesUnit 1 and 2missyemylia27novNo ratings yet

- PPE Theory-DepDocument5 pagesPPE Theory-DepDibyansu KumarNo ratings yet

- Accounting For Property Plant and EquipmentDocument6 pagesAccounting For Property Plant and EquipmentmostafaNo ratings yet

- Historical Cost of Property, Plant and EquipmentDocument9 pagesHistorical Cost of Property, Plant and EquipmentChinchin Ilagan DatayloNo ratings yet

- IND AS-16 Property, Plant and Equipment: Measurement of PpeDocument3 pagesIND AS-16 Property, Plant and Equipment: Measurement of PpeHimank SinglaNo ratings yet

- International Accounting Standard 16 Property, Plant and EquipmentDocument29 pagesInternational Accounting Standard 16 Property, Plant and EquipmentAbdullah Shaker TahaNo ratings yet

- BA 114.1 Handout On PPEDocument5 pagesBA 114.1 Handout On PPEHuarde SophiaNo ratings yet

- Pas 16 - Property Plant and EquipmentDocument4 pagesPas 16 - Property Plant and EquipmentJessie ForpublicuseNo ratings yet

- IAS 41 - AgricultureDocument17 pagesIAS 41 - AgricultureArshad BhuttaNo ratings yet

- IAS 38 - Intangible AssetsDocument27 pagesIAS 38 - Intangible AssetsArshad BhuttaNo ratings yet

- IFRS 5 - Non - Current Assets Held For Sale and Discontinued OperationsDocument16 pagesIFRS 5 - Non - Current Assets Held For Sale and Discontinued OperationsArshad BhuttaNo ratings yet

- IAS 40 - Investment PropertyDocument19 pagesIAS 40 - Investment PropertyArshad BhuttaNo ratings yet

- Route 22 23 September 2023Document3 pagesRoute 22 23 September 2023api-523195650No ratings yet

- Kluster Kimpalan Julai 2018Document6 pagesKluster Kimpalan Julai 2018Ajie Fikri FahamiNo ratings yet

- Earth Sci Module 8Document10 pagesEarth Sci Module 8Tom AngNo ratings yet

- CAPITALGAINS 3rdsep PDFDocument202 pagesCAPITALGAINS 3rdsep PDFPhani Kumar SomarajupalliNo ratings yet

- Future of EA - 269850Document14 pagesFuture of EA - 269850Renato Cardoso BottoNo ratings yet

- Ignition System: Engine Control (ECM)Document1 pageIgnition System: Engine Control (ECM)Rafael Alejandro ReyesNo ratings yet

- Activity Proposal-Stakeholders Forum 2Document6 pagesActivity Proposal-Stakeholders Forum 2Rob MachiavelliNo ratings yet

- Download: Setting Goals and ObjectivesDocument4 pagesDownload: Setting Goals and ObjectivesJacques VisserNo ratings yet

- FP75E eDocument4 pagesFP75E estar990No ratings yet

- Z VF-S15 PIDcontrol-InstrMan Neutral e E6581879Document23 pagesZ VF-S15 PIDcontrol-InstrMan Neutral e E6581879mdtabanioNo ratings yet

- 13 Electrical Pole's TrasverseDocument7 pages13 Electrical Pole's TrasverseReza PahlepiNo ratings yet

- Peralatan KantorDocument47 pagesPeralatan KantorEva SiswantiNo ratings yet

- MDP43887 Mileage Warranty Flyer Quick GuideDocument2 pagesMDP43887 Mileage Warranty Flyer Quick GuideScenic777No ratings yet

- 2017 Winter Model Answer PaperDocument21 pages2017 Winter Model Answer PaperjohnNo ratings yet

- Manila Prince Hotel vs. GSISDocument5 pagesManila Prince Hotel vs. GSISFenina ReyesNo ratings yet

- B 1410 - B&N Contract Furniture S.A. - Almeco Interior GMBHDocument2 pagesB 1410 - B&N Contract Furniture S.A. - Almeco Interior GMBHmaxNo ratings yet

- Application For Electronic Clearance Service (Ecs)Document2 pagesApplication For Electronic Clearance Service (Ecs)vijayindia87No ratings yet

- Human Resource Management 14th Edition Mondy Solutions Manual 1Document17 pagesHuman Resource Management 14th Edition Mondy Solutions Manual 1freida100% (44)

- GC TodayDocument31 pagesGC TodayBrayan GuzmanNo ratings yet

- New Microsoft Office Excel WorksheetDocument12 pagesNew Microsoft Office Excel WorksheetRam Krishna AdhikariNo ratings yet

- Secdocument 5193Document89 pagesSecdocument 5193keith.fairley123No ratings yet

- UPSE Discussion Paper On Maharlika FundDocument28 pagesUPSE Discussion Paper On Maharlika FundjosnixNo ratings yet

- C3h - 14 MERALCO v. QuisumbingDocument2 pagesC3h - 14 MERALCO v. QuisumbingAaron AristonNo ratings yet

- Japanese Depreciable Assets Tax Summary Report: No Data FoundDocument1 pageJapanese Depreciable Assets Tax Summary Report: No Data FoundrpillzNo ratings yet

- Petitioner Respondent: Ivq Land Holdings, Inc.Document15 pagesPetitioner Respondent: Ivq Land Holdings, Inc.Em-em DomingoNo ratings yet

- Hashimoto'S: ProtocolDocument13 pagesHashimoto'S: ProtocolNatasa EricNo ratings yet

- 372A Inter-Corporate Loans & InvestmentsDocument2 pages372A Inter-Corporate Loans & Investmentslegendstillalive4826No ratings yet

- 1 PDFDocument53 pages1 PDFChelle BelenzoNo ratings yet

- Unit Ii Inheritance and Interfaces: CS8392 /object Oriented ProgrammingDocument30 pagesUnit Ii Inheritance and Interfaces: CS8392 /object Oriented ProgrammingJhonNo ratings yet