Download as pptx, pdf, or txt

You might also like

- Taxation Income MCQDocument59 pagesTaxation Income MCQMary Therese Gabrielle Estioko33% (3)

- Course Syllabus International Business and TradeDocument11 pagesCourse Syllabus International Business and TradeCharmaine ShaninaNo ratings yet

- Course Syllabus Business FinanceDocument11 pagesCourse Syllabus Business FinanceCharmaine Shanina100% (1)

- Slide 1Document8 pagesSlide 1Sk Abul Salam100% (1)

- Income and Business TaxationDocument6 pagesIncome and Business Taxationomega shtNo ratings yet

- Income Taxation Lecture Notes.5.Classifications of Individual TaxpayersDocument5 pagesIncome Taxation Lecture Notes.5.Classifications of Individual Taxpayerseinel dc100% (1)

- Income Tax: Chapter 2: Income Taxes For IndividualDocument87 pagesIncome Tax: Chapter 2: Income Taxes For IndividualMaria Maganda MalditaNo ratings yet

- Corporate Social Responsibility of TESCODocument22 pagesCorporate Social Responsibility of TESCOPanigrahi AbhaNo ratings yet

- Personal and Additional ExemptionsDocument2 pagesPersonal and Additional ExemptionsRey AlegriaNo ratings yet

- Taxation-IT For Individuals Part3Document5 pagesTaxation-IT For Individuals Part3EmperiumNo ratings yet

- IndividualsDocument12 pagesIndividualsdarlene floresNo ratings yet

- Module 2 Tax On IndividualsDocument12 pagesModule 2 Tax On Individualscha11No ratings yet

- Income Taxation IndividualsDocument19 pagesIncome Taxation IndividualsJenniNo ratings yet

- Up Barops Income Tax ReviewerDocument37 pagesUp Barops Income Tax Reviewerliboanino100% (1)

- Income Taxation-IndividualDocument118 pagesIncome Taxation-Individualjovelyn labordoNo ratings yet

- Tax On Individuals Part 1Document9 pagesTax On Individuals Part 1Tet AleraNo ratings yet

- An Exemption Provided by Law To Take Care of PersonalDocument5 pagesAn Exemption Provided by Law To Take Care of PersonalQueen ValleNo ratings yet

- Individual TaxationDocument113 pagesIndividual TaxationGemmalyn Julaton100% (7)

- Summary Lesson 4Document6 pagesSummary Lesson 4Janien MedestomasNo ratings yet

- TAX - 601 - Individuals - Abapo, Mary Jhudiel G.Document53 pagesTAX - 601 - Individuals - Abapo, Mary Jhudiel G.Mohammad100% (1)

- Individual Income TaxationDocument4 pagesIndividual Income TaxationRoi RimasNo ratings yet

- Income Tax RegulationsDocument163 pagesIncome Tax RegulationsMark OyalesNo ratings yet

- TaxationDocument26 pagesTaxationReynamae Garcia AbalesNo ratings yet

- Exercises On Individual Income Taxation 3BDocument11 pagesExercises On Individual Income Taxation 3BSean San AntonioNo ratings yet

- 20240313T061944584 Att 908654264076627Document113 pages20240313T061944584 Att 908654264076627klee042697No ratings yet

- 3PO1 U1L2 PreTest Q5 - General Principles of Taxation - Tax LawsDocument1 page3PO1 U1L2 PreTest Q5 - General Principles of Taxation - Tax LawsKimberly MartinezNo ratings yet

- Fundamental Concepts of Individual Income TaxationDocument43 pagesFundamental Concepts of Individual Income TaxationLawrence Ting100% (1)

- Taxation - Individual - QuizzerDocument12 pagesTaxation - Individual - QuizzerKenneth Bryan Tegerero TegioNo ratings yet

- Chapter 2Document9 pagesChapter 2Sheilamae Sernadilla GregorioNo ratings yet

- Lesson 2 Taxation of IndividualsDocument40 pagesLesson 2 Taxation of IndividualsQuenie De la CruzNo ratings yet

- Revenue Regulations No 02-40Document19 pagesRevenue Regulations No 02-40corky01No ratings yet

- Introduction To Income TaxDocument28 pagesIntroduction To Income TaxGeena Chavez GabrielNo ratings yet

- Template Taxation Unit IIDocument29 pagesTemplate Taxation Unit IINacion, Jaime G.No ratings yet

- Tax ReviewerDocument103 pagesTax ReviewerOscar Ryan SantillanNo ratings yet

- Sample Question and Answer in TaxationDocument3 pagesSample Question and Answer in TaxationKJ Vecino Bontuyan100% (1)

- Tax 1007-16Document67 pagesTax 1007-16jaseyNo ratings yet

- Ast TX 501 Individual, Estate and Trust Taxation (Batch 22)Document7 pagesAst TX 501 Individual, Estate and Trust Taxation (Batch 22)Herald Gangcuangco100% (1)

- CH 3 Intro To Income TaxDocument16 pagesCH 3 Intro To Income TaxGabriel Trinidad SonielNo ratings yet

- 13 - About Filing Income Tax ReturnsDocument3 pages13 - About Filing Income Tax ReturnsAllan SantosNo ratings yet

- Rev. Regs. No. 2 (Income Tax Regs.)Document141 pagesRev. Regs. No. 2 (Income Tax Regs.)Iriz BelenoNo ratings yet

- Reviewer in Income Taxation Old TaxationDocument1 pageReviewer in Income Taxation Old TaxationJanRalphBulanonNo ratings yet

- Introduction To Income TaxationDocument3 pagesIntroduction To Income TaxationescrowNo ratings yet

- RR 2 (1940)Document41 pagesRR 2 (1940)Mariano Rentomes100% (1)

- Taxation FinalsDocument48 pagesTaxation Finalsaerosmith_julio6627No ratings yet

- Report in Taxation Group 3Document25 pagesReport in Taxation Group 3Patricia BacatanoNo ratings yet

- Introduction To Taxation What Is Taxation?Document5 pagesIntroduction To Taxation What Is Taxation?Monica MonicaNo ratings yet

- Income Taxation 1Document54 pagesIncome Taxation 1dffaurilloNo ratings yet

- Republic Act 8424: "Tax Reform Act of 1997": (Due To Mental/physical Defect Regardless of Age)Document2 pagesRepublic Act 8424: "Tax Reform Act of 1997": (Due To Mental/physical Defect Regardless of Age)Ellese SayNo ratings yet

- Home Development Mutual Fund Law ReportDocument8 pagesHome Development Mutual Fund Law ReportAmado Vallejo IIINo ratings yet

- TAX Reviewer FINALSDocument9 pagesTAX Reviewer FINALSLalaine SantiagoNo ratings yet

- DeductionsDocument10 pagesDeductionsSjaneyNo ratings yet

- Types of TaxpayerDocument23 pagesTypes of TaxpayerReina Rose LebrillaNo ratings yet

- Module 2 - Income Taxes For Individuals - Lecture NotesDocument52 pagesModule 2 - Income Taxes For Individuals - Lecture NotesRina Bico Advincula100% (1)

- Tax 601Document11 pagesTax 601C.J. Clarisse FranciscoNo ratings yet

- Taxation of IndividualsDocument49 pagesTaxation of IndividualsAnastasha Grey100% (1)

- Lesson Income TaxDocument8 pagesLesson Income TaxEfren Lester ReyesNo ratings yet

- Tax - Income Tax Individuals (Easy)Document28 pagesTax - Income Tax Individuals (Easy)Kristine Lirose BordeosNo ratings yet

- Introduction To Individual Income Taxation Chapter Overview and ObjectivesDocument25 pagesIntroduction To Individual Income Taxation Chapter Overview and ObjectivesMatta, Jherrie MaeNo ratings yet

- What Are The Kinds of TaxpayersDocument4 pagesWhat Are The Kinds of TaxpayersALee Bud100% (1)

- MixDocument32 pagesMixUnnecessary BuyingNo ratings yet

- Train Individual INCOME TAXDocument48 pagesTrain Individual INCOME TAXMeireen Ann100% (2)

- Sponsorship: Who's Eligible & How to ApplyFrom EverandSponsorship: Who's Eligible & How to ApplyNo ratings yet

- Course Syllabus Managerial AccountingDocument10 pagesCourse Syllabus Managerial AccountingCharmaine Shanina100% (1)

- Practicum Deployment Matrix of BSBA OJT StudentsDocument7 pagesPracticum Deployment Matrix of BSBA OJT StudentsCharmaine ShaninaNo ratings yet

- By Laws BSE OrganizationDocument6 pagesBy Laws BSE OrganizationCharmaine ShaninaNo ratings yet

- Sample Intent LetterDocument1 pageSample Intent LetterCharmaine ShaninaNo ratings yet

- OJT PointersDocument2 pagesOJT PointersCharmaine ShaninaNo ratings yet

- Pointers-Comprehensive Examination Marketing ManagementDocument1 pagePointers-Comprehensive Examination Marketing ManagementCharmaine ShaninaNo ratings yet

- Research Proposal 1Document46 pagesResearch Proposal 1Charmaine Shanina100% (1)

- Long Quiz in Income Taxation FM 3Document2 pagesLong Quiz in Income Taxation FM 3Charmaine Shanina100% (1)

- Research Proposal 3Document36 pagesResearch Proposal 3Charmaine ShaninaNo ratings yet

- Long Quiz in Financial Management - 12122022Document1 pageLong Quiz in Financial Management - 12122022Charmaine ShaninaNo ratings yet

- Thesis Rubrics Criteria For GradingDocument6 pagesThesis Rubrics Criteria For GradingCharmaine ShaninaNo ratings yet

- 4BKP Hilltribe (01 Nov 2019 - 30 April 2020) - USDDocument3 pages4BKP Hilltribe (01 Nov 2019 - 30 April 2020) - USDCharmaine ShaninaNo ratings yet

- Long Quiz in Financial Management 2Document1 pageLong Quiz in Financial Management 2Charmaine ShaninaNo ratings yet

- Accessibility Porto Et Al 2018Document18 pagesAccessibility Porto Et Al 2018Charmaine ShaninaNo ratings yet

- Research Proposal 2Document8 pagesResearch Proposal 2Charmaine ShaninaNo ratings yet

- Cmf-006 Agency Application FormDocument2 pagesCmf-006 Agency Application FormCharmaine ShaninaNo ratings yet

- Business Research - Module 3Document6 pagesBusiness Research - Module 3Charmaine ShaninaNo ratings yet

- Micali 0410Document1 pageMicali 0410Charmaine ShaninaNo ratings yet

- How To Do Regular Class Memo and Count Class NumberDocument4 pagesHow To Do Regular Class Memo and Count Class NumberCharmaine ShaninaNo ratings yet

- RP Activities Voucher - DunvarDocument2 pagesRP Activities Voucher - DunvarCharmaine ShaninaNo ratings yet

- Class Materials: Your Name: Charmaine Shanina B. DeminDocument2 pagesClass Materials: Your Name: Charmaine Shanina B. DeminCharmaine ShaninaNo ratings yet

- 11 Rules in GrammarDocument4 pages11 Rules in GrammarCharmaine ShaninaNo ratings yet

- Characteristics of The TourismDocument4 pagesCharacteristics of The TourismRay KNo ratings yet

- SAMPLE Assignment Madoff Ponzi Scheme 2010Document2 pagesSAMPLE Assignment Madoff Ponzi Scheme 2010scholarsassistNo ratings yet

- HP Blueprint - PsDocument87 pagesHP Blueprint - PsRangabashyam100% (2)

- 5s Methodology Implementation in The Laboratories of University Srivastava, K.R., Gupta, R.K., Khare, M.Document5 pages5s Methodology Implementation in The Laboratories of University Srivastava, K.R., Gupta, R.K., Khare, M.Pablo Fernández SaavedraNo ratings yet

- Principles of Management Set 1Document6 pagesPrinciples of Management Set 1prolay80No ratings yet

- Nucleon, Inc.: June 28th, 2019 - Group 5 - Bishwadeep - Gulshan - Mitali - RaghaviDocument12 pagesNucleon, Inc.: June 28th, 2019 - Group 5 - Bishwadeep - Gulshan - Mitali - RaghaviGulshan DhananiNo ratings yet

- In-House Cpa Review Taxation Donor'S Tax - Notes: E.A.Dg - MateoDocument2 pagesIn-House Cpa Review Taxation Donor'S Tax - Notes: E.A.Dg - MateoMina ValenciaNo ratings yet

- Ti TechDocument4 pagesTi Techmadddy_hyd100% (3)

- Pengajian Perniagaan Semester 1 Bab 3Document18 pagesPengajian Perniagaan Semester 1 Bab 3EagelNo ratings yet

- Operating Segment: Pfrs 8Document28 pagesOperating Segment: Pfrs 8Giellay OyaoNo ratings yet

- Abebaw Shimelis 2003Document164 pagesAbebaw Shimelis 2003Rafez JoneNo ratings yet

- Tybfm Sem 6 Venture Capital Unit II & IIIDocument19 pagesTybfm Sem 6 Venture Capital Unit II & IIIElamathiNo ratings yet

- Lesson 6 Theory of Cost and Profit: Cueto, Ivan Macayan, Jhon Alexis Bangcuyo, Andrei Nicole Betsaida, Angelika (Group 6)Document38 pagesLesson 6 Theory of Cost and Profit: Cueto, Ivan Macayan, Jhon Alexis Bangcuyo, Andrei Nicole Betsaida, Angelika (Group 6)Ally 19No ratings yet

- Cfo AgendaDocument7 pagesCfo AgendaMOORTHY.KENo ratings yet

- (Exercise) WaccDocument3 pages(Exercise) Waccclary frayNo ratings yet

- MM ProjectDocument11 pagesMM ProjectSonal GanganiNo ratings yet

- M Acc Spring 2017Document383 pagesM Acc Spring 2017Awais MehmoodNo ratings yet

- Services Marketing Midterm ExamDocument7 pagesServices Marketing Midterm ExamNH PrinceNo ratings yet

- Agriclinics and Agribusiness CentersDocument47 pagesAgriclinics and Agribusiness CentersMadhavilathaNo ratings yet

- My Player Aid Version 1.2Document1 pageMy Player Aid Version 1.2Armand GuerreNo ratings yet

- Tax Case Digest 5Document11 pagesTax Case Digest 5Tammy YahNo ratings yet

- Ismt LTD (2019-2020)Document150 pagesIsmt LTD (2019-2020)Nimit BhimjiyaniNo ratings yet

- Detour Gold Dec 2009 PresentationDocument38 pagesDetour Gold Dec 2009 PresentationAla BasterNo ratings yet

- APGLIDocument7 pagesAPGLIskssahul59No ratings yet

- Chapter 3Document47 pagesChapter 3zeid100% (1)

- Zeeman's Family ExpansionDocument16 pagesZeeman's Family ExpansionColinNo ratings yet

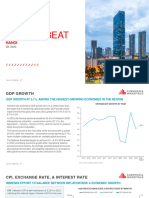

- Vietnam 2023q4 CW Market Beat Hanoi - en CombinedDocument36 pagesVietnam 2023q4 CW Market Beat Hanoi - en CombinedVu Ha NguyenNo ratings yet

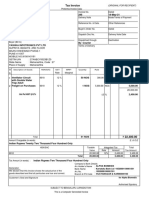

- Tax Invoice: Alpha Biomedix 295 14-May-21Document3 pagesTax Invoice: Alpha Biomedix 295 14-May-21Neha UkaleNo ratings yet