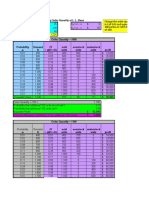

Date Cost Model Revaluation Model Fair Value Model

Date Cost Model Revaluation Model Fair Value Model

You might also like

- Ipsas 17 ExampleDocument4 pagesIpsas 17 Examplesenbetotilahun8No ratings yet

- Chapter 12 Ia1Document9 pagesChapter 12 Ia1Bella FlairNo ratings yet

- A01 - Assignment 4Document3 pagesA01 - Assignment 4MalykaNo ratings yet

- Ap 1-4 IsDocument1 pageAp 1-4 Isapi-334420312No ratings yet

- Modi Method UnbalancedDocument4 pagesModi Method UnbalancedRowillyn OrsalNo ratings yet

- Ap 1-4 IsDocument1 pageAp 1-4 Isapi-335646206No ratings yet

- 11 Solutions PDFDocument9 pages11 Solutions PDFKenneth KibataNo ratings yet

- Chapter 13-ExamplesDocument18 pagesChapter 13-Examplesaaha10No ratings yet

- 2 - Breakeven Analysis & Decision Trees PDFDocument35 pages2 - Breakeven Analysis & Decision Trees PDFRajat AgrawalNo ratings yet

- HW2-5 (PDF) - CliffsNotesDocument4 pagesHW2-5 (PDF) - CliffsNotesSylvester WasongaNo ratings yet

- pROBLEM 12Document2 pagespROBLEM 12Nepal Bishal ShresthaNo ratings yet

- Excel Discussion in Define Benefit PlanDocument5 pagesExcel Discussion in Define Benefit PlanElaine Joyce GarciaNo ratings yet

- Joint VentureDocument2 pagesJoint Venturexokittyxo987No ratings yet

- Management Accounting Set 5Document6 pagesManagement Accounting Set 5Julia ŚwierczyńskaNo ratings yet

- A 2021MBA030 YuddhaveerSingh CaseScenariosRBCDocument7 pagesA 2021MBA030 YuddhaveerSingh CaseScenariosRBCmohammedsuhaim abdul gafoorNo ratings yet

- Process Sol For StudentsDocument9 pagesProcess Sol For Studentsfernandesjervis8No ratings yet

- Journal Transactions: Dwyer Delivery ServiceDocument10 pagesJournal Transactions: Dwyer Delivery ServiceClara Saty M LambaNo ratings yet

- BØK260Document41 pagesBØK260gintare.ginkaiteNo ratings yet

- Structural Analysis - IDocument13 pagesStructural Analysis - INitendra TomarNo ratings yet

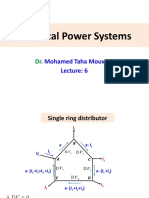

- Lecture 6Document16 pagesLecture 6Amr MohamedNo ratings yet

- CSEC Jan 2020 Paper 1 AnswersDocument13 pagesCSEC Jan 2020 Paper 1 Answersricardogibbs9o9No ratings yet

- C - 2021MBA160 - Case ScenariosRBCDocument7 pagesC - 2021MBA160 - Case ScenariosRBCmohammedsuhaim abdul gafoorNo ratings yet

- Practice 2 (Answer)Document8 pagesPractice 2 (Answer)PRITIKA GUNASEGARANNo ratings yet

- Tugas 3 Ekonomi MakroDocument2 pagesTugas 3 Ekonomi MakroMuhammad IrsyadNo ratings yet

- Addresing Modjgvve QuestionDocument1 pageAddresing Modjgvve Questionnielabh GireyNo ratings yet

- WK 4 Solutions To Thread Practice ProblemsDocument3 pagesWK 4 Solutions To Thread Practice Problemsmasta4ulskilzNo ratings yet

- Oper&Scm SupaDocument58 pagesOper&Scm Supa장현우No ratings yet

- Cost Accounting 87Document1 pageCost Accounting 87alfredrunz7No ratings yet

- W Gas ExpenditureDocument8 pagesW Gas ExpenditureLime Hexa StudiosNo ratings yet

- Chapter 12 Standard Costing Nov 2020 2Document112 pagesChapter 12 Standard Costing Nov 2020 2Kunal KuvadiaNo ratings yet

- LiquidationDocument20 pagesLiquidationReham DarweshNo ratings yet

- X Y Objective 12 4 20 Constraint 1 2 4 20 Constraint 2 5 2 10 X y Solution 0 5Document26 pagesX Y Objective 12 4 20 Constraint 1 2 4 20 Constraint 2 5 2 10 X y Solution 0 5Mavie MolinoNo ratings yet

- ACCA107 MIDTERMS OCT 06 2021 PROBLEMS SOLUTION - Sheet3Document12 pagesACCA107 MIDTERMS OCT 06 2021 PROBLEMS SOLUTION - Sheet3Mary Kate OrobiaNo ratings yet

- Gabuya, Christine EDocument4 pagesGabuya, Christine Echristine gabuyaNo ratings yet

- Eval Balance Cairan - B2 - 1911604082 - Wahyu Putri NurjannahDocument4 pagesEval Balance Cairan - B2 - 1911604082 - Wahyu Putri NurjannahAprimansahNo ratings yet

- Cost AnswerDocument8 pagesCost AnswerSsel Gamboa GayaresNo ratings yet

- Week 2 - LPDocument16 pagesWeek 2 - LPVieri SuhermanNo ratings yet

- Application Problem 1-4 Student's Name: (Your Name) You Have 2 Item(s) Remaining To Answer CorrectlyDocument1 pageApplication Problem 1-4 Student's Name: (Your Name) You Have 2 Item(s) Remaining To Answer CorrectlyDaran RungwattanasophonNo ratings yet

- Assignment - CEE 300Document3 pagesAssignment - CEE 300Edwin OtienoNo ratings yet

- Cost Accounting 1Document4 pagesCost Accounting 1Rohan RalliNo ratings yet

- Pea Company Soup Company Debit Credit Debit Credit: Income StatementDocument2 pagesPea Company Soup Company Debit Credit Debit Credit: Income StatementSARA ALKHODAIRNo ratings yet

- State of Nature Alternatives 1 2 3Document10 pagesState of Nature Alternatives 1 2 3Michael Allen RodrigoNo ratings yet

- Green Mills - Level & Chase WorkedDocument11 pagesGreen Mills - Level & Chase WorkedJagan JCNo ratings yet

- Contoh Soal Flexibel Budget PDFDocument3 pagesContoh Soal Flexibel Budget PDFJaihut NainggolanNo ratings yet

- Bci Ex (S) 00024129Document1 pageBci Ex (S) 00024129planetamundo2017No ratings yet

- Intermediate Accounting Chapter 12 Lower of Cost and Net Realizable ValueDocument11 pagesIntermediate Accounting Chapter 12 Lower of Cost and Net Realizable ValueBlue SkyNo ratings yet

- National Income DeterminationDocument8 pagesNational Income DeterminationredNo ratings yet

- Financial ManagementDocument35 pagesFinancial ManagementNipuna WijeruwanNo ratings yet

- Problem 2 Table IDocument3 pagesProblem 2 Table IIsabelle CandelariaNo ratings yet

- Problem 2 Table IDocument3 pagesProblem 2 Table IKristelle Mae Dela Peña DugayNo ratings yet

- ISSUE: Z Correct But Why Is DEC VAR Is Not Matching. PG 166Document2 pagesISSUE: Z Correct But Why Is DEC VAR Is Not Matching. PG 166Rithesh KNo ratings yet

- Account Title Debit Credit Debit Credit Debit Credit Debit CreditDocument1 pageAccount Title Debit Credit Debit Credit Debit Credit Debit CreditMike MikeNo ratings yet

- Solver Aggregate Planning Example inDocument5 pagesSolver Aggregate Planning Example inGopichand AthukuriNo ratings yet

- Book 1Document2 pagesBook 1Laika DuradaNo ratings yet

- Actual Based Costing vs. Traditional ApproachDocument4 pagesActual Based Costing vs. Traditional ApproachSHARMAINE JOY FULGARNo ratings yet

- Módulo 3 Métodos de Costos Sesión 3Document4 pagesMódulo 3 Métodos de Costos Sesión 3FerNo ratings yet

- Supplement 7: Capacity Planning - Suggested Solutions To Selected QuestionsDocument4 pagesSupplement 7: Capacity Planning - Suggested Solutions To Selected QuestionsAriajiPrichiGamayudaNo ratings yet

- Break Even ExercisesDocument4 pagesBreak Even ExercisesErjonaNo ratings yet

- IM - Chapter 2 AnswersDocument4 pagesIM - Chapter 2 AnswersEileen WongNo ratings yet

- Chapter - Three Budgets and Budgetary ControlDocument83 pagesChapter - Three Budgets and Budgetary ControlHace AdisNo ratings yet

- Ipsas 21: Impairment of Non-Cash-Generating AssetsDocument25 pagesIpsas 21: Impairment of Non-Cash-Generating AssetsHace AdisNo ratings yet

- Ipsas 23: Revenue From Non Exchange TransactionsDocument11 pagesIpsas 23: Revenue From Non Exchange TransactionsHace AdisNo ratings yet

- Ipsas 16: Investment PropertyDocument25 pagesIpsas 16: Investment PropertyHace AdisNo ratings yet

- Ifrs 15: Revenue From Contracts With CustomersDocument46 pagesIfrs 15: Revenue From Contracts With CustomersHace AdisNo ratings yet

- CHAPTER Four NewDocument16 pagesCHAPTER Four NewHace AdisNo ratings yet

- FM II - Chapter 03, Financial Planning & ForecastingDocument28 pagesFM II - Chapter 03, Financial Planning & ForecastingHace Adis100% (1)

- Article Review FinalDocument5 pagesArticle Review FinalHace AdisNo ratings yet

- Finance AttachementDocument21 pagesFinance AttachementHace AdisNo ratings yet

- Financial Hand Out 22-2Document13 pagesFinancial Hand Out 22-2Hace AdisNo ratings yet

- FM II - Chapter 03, Financial Planning & ForecastingDocument14 pagesFM II - Chapter 03, Financial Planning & ForecastingHace AdisNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Ipsas 17 ExampleDocument4 pagesIpsas 17 Examplesenbetotilahun8No ratings yet

- Chapter 12 Ia1Document9 pagesChapter 12 Ia1Bella FlairNo ratings yet

- A01 - Assignment 4Document3 pagesA01 - Assignment 4MalykaNo ratings yet

- Ap 1-4 IsDocument1 pageAp 1-4 Isapi-334420312No ratings yet

- Modi Method UnbalancedDocument4 pagesModi Method UnbalancedRowillyn OrsalNo ratings yet

- Ap 1-4 IsDocument1 pageAp 1-4 Isapi-335646206No ratings yet

- 11 Solutions PDFDocument9 pages11 Solutions PDFKenneth KibataNo ratings yet

- Chapter 13-ExamplesDocument18 pagesChapter 13-Examplesaaha10No ratings yet

- 2 - Breakeven Analysis & Decision Trees PDFDocument35 pages2 - Breakeven Analysis & Decision Trees PDFRajat AgrawalNo ratings yet

- HW2-5 (PDF) - CliffsNotesDocument4 pagesHW2-5 (PDF) - CliffsNotesSylvester WasongaNo ratings yet

- pROBLEM 12Document2 pagespROBLEM 12Nepal Bishal ShresthaNo ratings yet

- Excel Discussion in Define Benefit PlanDocument5 pagesExcel Discussion in Define Benefit PlanElaine Joyce GarciaNo ratings yet

- Joint VentureDocument2 pagesJoint Venturexokittyxo987No ratings yet

- Management Accounting Set 5Document6 pagesManagement Accounting Set 5Julia ŚwierczyńskaNo ratings yet

- A 2021MBA030 YuddhaveerSingh CaseScenariosRBCDocument7 pagesA 2021MBA030 YuddhaveerSingh CaseScenariosRBCmohammedsuhaim abdul gafoorNo ratings yet

- Process Sol For StudentsDocument9 pagesProcess Sol For Studentsfernandesjervis8No ratings yet

- Journal Transactions: Dwyer Delivery ServiceDocument10 pagesJournal Transactions: Dwyer Delivery ServiceClara Saty M LambaNo ratings yet

- BØK260Document41 pagesBØK260gintare.ginkaiteNo ratings yet

- Structural Analysis - IDocument13 pagesStructural Analysis - INitendra TomarNo ratings yet

- Lecture 6Document16 pagesLecture 6Amr MohamedNo ratings yet

- CSEC Jan 2020 Paper 1 AnswersDocument13 pagesCSEC Jan 2020 Paper 1 Answersricardogibbs9o9No ratings yet

- C - 2021MBA160 - Case ScenariosRBCDocument7 pagesC - 2021MBA160 - Case ScenariosRBCmohammedsuhaim abdul gafoorNo ratings yet

- Practice 2 (Answer)Document8 pagesPractice 2 (Answer)PRITIKA GUNASEGARANNo ratings yet

- Tugas 3 Ekonomi MakroDocument2 pagesTugas 3 Ekonomi MakroMuhammad IrsyadNo ratings yet

- Addresing Modjgvve QuestionDocument1 pageAddresing Modjgvve Questionnielabh GireyNo ratings yet

- WK 4 Solutions To Thread Practice ProblemsDocument3 pagesWK 4 Solutions To Thread Practice Problemsmasta4ulskilzNo ratings yet

- Oper&Scm SupaDocument58 pagesOper&Scm Supa장현우No ratings yet

- Cost Accounting 87Document1 pageCost Accounting 87alfredrunz7No ratings yet

- W Gas ExpenditureDocument8 pagesW Gas ExpenditureLime Hexa StudiosNo ratings yet

- Chapter 12 Standard Costing Nov 2020 2Document112 pagesChapter 12 Standard Costing Nov 2020 2Kunal KuvadiaNo ratings yet

- LiquidationDocument20 pagesLiquidationReham DarweshNo ratings yet

- X Y Objective 12 4 20 Constraint 1 2 4 20 Constraint 2 5 2 10 X y Solution 0 5Document26 pagesX Y Objective 12 4 20 Constraint 1 2 4 20 Constraint 2 5 2 10 X y Solution 0 5Mavie MolinoNo ratings yet

- ACCA107 MIDTERMS OCT 06 2021 PROBLEMS SOLUTION - Sheet3Document12 pagesACCA107 MIDTERMS OCT 06 2021 PROBLEMS SOLUTION - Sheet3Mary Kate OrobiaNo ratings yet

- Gabuya, Christine EDocument4 pagesGabuya, Christine Echristine gabuyaNo ratings yet

- Eval Balance Cairan - B2 - 1911604082 - Wahyu Putri NurjannahDocument4 pagesEval Balance Cairan - B2 - 1911604082 - Wahyu Putri NurjannahAprimansahNo ratings yet

- Cost AnswerDocument8 pagesCost AnswerSsel Gamboa GayaresNo ratings yet

- Week 2 - LPDocument16 pagesWeek 2 - LPVieri SuhermanNo ratings yet

- Application Problem 1-4 Student's Name: (Your Name) You Have 2 Item(s) Remaining To Answer CorrectlyDocument1 pageApplication Problem 1-4 Student's Name: (Your Name) You Have 2 Item(s) Remaining To Answer CorrectlyDaran RungwattanasophonNo ratings yet

- Assignment - CEE 300Document3 pagesAssignment - CEE 300Edwin OtienoNo ratings yet

- Cost Accounting 1Document4 pagesCost Accounting 1Rohan RalliNo ratings yet

- Pea Company Soup Company Debit Credit Debit Credit: Income StatementDocument2 pagesPea Company Soup Company Debit Credit Debit Credit: Income StatementSARA ALKHODAIRNo ratings yet

- State of Nature Alternatives 1 2 3Document10 pagesState of Nature Alternatives 1 2 3Michael Allen RodrigoNo ratings yet

- Green Mills - Level & Chase WorkedDocument11 pagesGreen Mills - Level & Chase WorkedJagan JCNo ratings yet

- Contoh Soal Flexibel Budget PDFDocument3 pagesContoh Soal Flexibel Budget PDFJaihut NainggolanNo ratings yet

- Bci Ex (S) 00024129Document1 pageBci Ex (S) 00024129planetamundo2017No ratings yet

- Intermediate Accounting Chapter 12 Lower of Cost and Net Realizable ValueDocument11 pagesIntermediate Accounting Chapter 12 Lower of Cost and Net Realizable ValueBlue SkyNo ratings yet

- National Income DeterminationDocument8 pagesNational Income DeterminationredNo ratings yet

- Financial ManagementDocument35 pagesFinancial ManagementNipuna WijeruwanNo ratings yet

- Problem 2 Table IDocument3 pagesProblem 2 Table IIsabelle CandelariaNo ratings yet

- Problem 2 Table IDocument3 pagesProblem 2 Table IKristelle Mae Dela Peña DugayNo ratings yet

- ISSUE: Z Correct But Why Is DEC VAR Is Not Matching. PG 166Document2 pagesISSUE: Z Correct But Why Is DEC VAR Is Not Matching. PG 166Rithesh KNo ratings yet

- Account Title Debit Credit Debit Credit Debit Credit Debit CreditDocument1 pageAccount Title Debit Credit Debit Credit Debit Credit Debit CreditMike MikeNo ratings yet

- Solver Aggregate Planning Example inDocument5 pagesSolver Aggregate Planning Example inGopichand AthukuriNo ratings yet

- Book 1Document2 pagesBook 1Laika DuradaNo ratings yet

- Actual Based Costing vs. Traditional ApproachDocument4 pagesActual Based Costing vs. Traditional ApproachSHARMAINE JOY FULGARNo ratings yet

- Módulo 3 Métodos de Costos Sesión 3Document4 pagesMódulo 3 Métodos de Costos Sesión 3FerNo ratings yet

- Supplement 7: Capacity Planning - Suggested Solutions To Selected QuestionsDocument4 pagesSupplement 7: Capacity Planning - Suggested Solutions To Selected QuestionsAriajiPrichiGamayudaNo ratings yet

- Break Even ExercisesDocument4 pagesBreak Even ExercisesErjonaNo ratings yet

- IM - Chapter 2 AnswersDocument4 pagesIM - Chapter 2 AnswersEileen WongNo ratings yet

- Chapter - Three Budgets and Budgetary ControlDocument83 pagesChapter - Three Budgets and Budgetary ControlHace AdisNo ratings yet

- Ipsas 21: Impairment of Non-Cash-Generating AssetsDocument25 pagesIpsas 21: Impairment of Non-Cash-Generating AssetsHace AdisNo ratings yet

- Ipsas 23: Revenue From Non Exchange TransactionsDocument11 pagesIpsas 23: Revenue From Non Exchange TransactionsHace AdisNo ratings yet

- Ipsas 16: Investment PropertyDocument25 pagesIpsas 16: Investment PropertyHace AdisNo ratings yet

- Ifrs 15: Revenue From Contracts With CustomersDocument46 pagesIfrs 15: Revenue From Contracts With CustomersHace AdisNo ratings yet

- CHAPTER Four NewDocument16 pagesCHAPTER Four NewHace AdisNo ratings yet

- FM II - Chapter 03, Financial Planning & ForecastingDocument28 pagesFM II - Chapter 03, Financial Planning & ForecastingHace Adis100% (1)

- Article Review FinalDocument5 pagesArticle Review FinalHace AdisNo ratings yet

- Finance AttachementDocument21 pagesFinance AttachementHace AdisNo ratings yet

- Financial Hand Out 22-2Document13 pagesFinancial Hand Out 22-2Hace AdisNo ratings yet

- FM II - Chapter 03, Financial Planning & ForecastingDocument14 pagesFM II - Chapter 03, Financial Planning & ForecastingHace AdisNo ratings yet