Pertemuan+2 the+Financial+Market+Environment

Pertemuan+2 the+Financial+Market+Environment

You might also like

- Financial Accounting - Rev Partner-2Document168 pagesFinancial Accounting - Rev Partner-2JOHN KAMANDA100% (1)

- MODULE 1 Lecture Notes (Jeff Madura)Document4 pagesMODULE 1 Lecture Notes (Jeff Madura)Romen CenizaNo ratings yet

- Debt InstrumentsDocument53 pagesDebt Instrumentskinjalkapadia087118100% (6)

- FM 03 Financial IntermediationDocument8 pagesFM 03 Financial IntermediationIvy ObligadoNo ratings yet

- Financial Markets LowDocument17 pagesFinancial Markets LowNelsonMoseMNo ratings yet

- Questions Chapter TwoDocument5 pagesQuestions Chapter TwoRose Sánchez0% (1)

- Investment Bankers and Scope FinalDocument48 pagesInvestment Bankers and Scope FinalAkash Gupta0% (1)

- STUDENT Capital and Bond Market UNITDocument24 pagesSTUDENT Capital and Bond Market UNITTetiana VozniukNo ratings yet

- Examples of Financial MarketsDocument3 pagesExamples of Financial Marketskate trishaNo ratings yet

- Capital Markets.Document32 pagesCapital Markets.api-3727090No ratings yet

- Capital Market - A BriefDocument7 pagesCapital Market - A BriefasfaarsafiNo ratings yet

- Credit MarketsDocument12 pagesCredit MarketsDarlyn CarelNo ratings yet

- An Overview of The Financial SystemDocument15 pagesAn Overview of The Financial SystemBerk YAZARNo ratings yet

- Gen Math Stocks and BondsDocument41 pagesGen Math Stocks and BondsDaniel VillahermosaNo ratings yet

- A Financial MarketDocument5 pagesA Financial MarketSalvador SantosNo ratings yet

- Background On Mortgages: Mortgage MarketsDocument7 pagesBackground On Mortgages: Mortgage MarketsPaw VerdilloNo ratings yet

- Chapter 5 FIMDocument13 pagesChapter 5 FIMMintayto TebekaNo ratings yet

- Solution Manual For Principles of Managerial Finance Brief 8th Edition ZutterDocument24 pagesSolution Manual For Principles of Managerial Finance Brief 8th Edition Zuttermichellelewismqdacbxijt100% (53)

- Business Breif U06-2 PDFDocument1 pageBusiness Breif U06-2 PDFAdam MichałekNo ratings yet

- FINAL-fm Project of Group No-13Document29 pagesFINAL-fm Project of Group No-13Prashant PatelNo ratings yet

- Operario, Gabrielle Mae - MODULE3 - ASSIGNMENT - BOND MARKET SECURITIESDocument5 pagesOperario, Gabrielle Mae - MODULE3 - ASSIGNMENT - BOND MARKET SECURITIESGabby OperarioNo ratings yet

- BFM NotesDocument10 pagesBFM Notesravitejaraviteja11111No ratings yet

- M&B Lesson 4 The Financial SystemDocument12 pagesM&B Lesson 4 The Financial SystemAnthony BandaNo ratings yet

- Islamic Vs Modern BONDDocument18 pagesIslamic Vs Modern BONDPakassignmentNo ratings yet

- Report in MTH of IntDocument6 pagesReport in MTH of Intangie valenzuelaNo ratings yet

- Module Code: Umed8S-30-1 MODULE TITLE: Financial Institutions and Markets STUDENT NUMBER: 20055737 Online Exam Section ADocument3 pagesModule Code: Umed8S-30-1 MODULE TITLE: Financial Institutions and Markets STUDENT NUMBER: 20055737 Online Exam Section ALinh Nguyễn Hoàng PhươngNo ratings yet

- Derivatives CaseDocument10 pagesDerivatives CaseLương Thế CườngNo ratings yet

- Finance TestDocument6 pagesFinance Testqylimstephy100% (1)

- Types of Financial InstitutionsDocument9 pagesTypes of Financial InstitutionsfathimabindmohdNo ratings yet

- Savings, Investment and The Financial System CH 26Document29 pagesSavings, Investment and The Financial System CH 26Md. Mehedi HasanNo ratings yet

- FIM Group Assignmen FinalDocument9 pagesFIM Group Assignmen FinalEndeg KelkayNo ratings yet

- Definition of 'Stock Market'Document3 pagesDefinition of 'Stock Market'Karla BordonesNo ratings yet

- Contemporary Financial Management 14th Edition Moyer Solutions ManualDocument35 pagesContemporary Financial Management 14th Edition Moyer Solutions Manualexedentzigzag.96ewc96% (27)

- Financial MarketDocument8 pagesFinancial MarkettiloooNo ratings yet

- Saint Mary'S University: Faculty of Accounting and FinanceDocument10 pagesSaint Mary'S University: Faculty of Accounting and FinanceruhamaNo ratings yet

- Saint Mary'S University: Faculty of Accounting and FinanceDocument10 pagesSaint Mary'S University: Faculty of Accounting and FinanceruhamaNo ratings yet

- T4-4.4. The Financial SectorDocument6 pagesT4-4.4. The Financial SectorBlu BostockNo ratings yet

- Financial System and MarketsDocument17 pagesFinancial System and MarketsDipesh GautamNo ratings yet

- Ilovepdf MergedDocument582 pagesIlovepdf MergedSahil SawantNo ratings yet

- 1 The Investment Industry A Top Down ViewDocument24 pages1 The Investment Industry A Top Down Viewakash jainNo ratings yet

- Specialty CorporationDocument171 pagesSpecialty CorporationAdrian Steven Claude CosicoNo ratings yet

- Financial M R AsiignmentDocument12 pagesFinancial M R AsiignmentDHARAM DEEPAK VISHWASHNo ratings yet

- Financial Markets and Institutions 1Document29 pagesFinancial Markets and Institutions 1Hamza Iqbal100% (1)

- Fin Market and InstitutionDocument3 pagesFin Market and Institutionzeus manNo ratings yet

- Securities Market - CLCDocument7 pagesSecurities Market - CLChoangngothanhtrangNo ratings yet

- Benavidez, Ramcie A. Bsba FM TF-7:00-8:30pm 4FM6Document3 pagesBenavidez, Ramcie A. Bsba FM TF-7:00-8:30pm 4FM6Ramcie Aguilar BenavidezNo ratings yet

- Ict2 ST Agnes Bulaon Jun 7pmquizDocument18 pagesIct2 ST Agnes Bulaon Jun 7pmquizArjeune Victoria BulaonNo ratings yet

- 02 - Handout - 1 (FINANCIAL MARKETS AND INSTITUTIONS)Document6 pages02 - Handout - 1 (FINANCIAL MARKETS AND INSTITUTIONS)Janrey RomanNo ratings yet

- Question 1) Briefly Explain Capital Allocation Process With The Help of Diagram?Document7 pagesQuestion 1) Briefly Explain Capital Allocation Process With The Help of Diagram?Usama KhanNo ratings yet

- Hedge ProfileDocument37 pagesHedge ProfilePramod PNo ratings yet

- Specialized Financial Institutions.: by MKDocument47 pagesSpecialized Financial Institutions.: by MKSarwan GulNo ratings yet

- Financial IntermediationDocument14 pagesFinancial IntermediationKimberly BastesNo ratings yet

- Securitization CitedDocument13 pagesSecuritization CitedBrighton NabiswaNo ratings yet

- Assignment No. 4 Roll No. L-1184 Financial Institution Topic: Bond Market, Stock Market and Mortgage Market Submitted To: Sir Abdul Qadeer Submitted By: Zainab Shabbir Dated: 21 June, 2020Document16 pagesAssignment No. 4 Roll No. L-1184 Financial Institution Topic: Bond Market, Stock Market and Mortgage Market Submitted To: Sir Abdul Qadeer Submitted By: Zainab Shabbir Dated: 21 June, 2020Faisal NaqviNo ratings yet

- ABIYDocument9 pagesABIYEyob HaylemariamNo ratings yet

- 1 I 1.1 O F S: Ntroduction Verview OF THE Inancial YstemDocument8 pages1 I 1.1 O F S: Ntroduction Verview OF THE Inancial YstemAyanda Yan'Dee DimphoNo ratings yet

- Chapter Two-The Financial Environment: Markets, Institutions and Investment BanksDocument4 pagesChapter Two-The Financial Environment: Markets, Institutions and Investment Banksmaquesurat ferdousNo ratings yet

- FM - 3Document4 pagesFM - 3Qani SalvaNo ratings yet

- Financial Environment - Lecture2Document20 pagesFinancial Environment - Lecture2mehnaz kNo ratings yet

- Purple Gradient 3D Bold Modern Investing Tips PresentationDocument47 pagesPurple Gradient 3D Bold Modern Investing Tips PresentationJana Beni Carolyn R. SabadoNo ratings yet

- The Great Recession: The burst of the property bubble and the excesses of speculationFrom EverandThe Great Recession: The burst of the property bubble and the excesses of speculationNo ratings yet

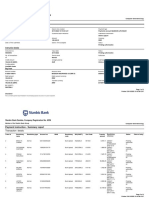

- Payment Instruction - Summary Report: Stanbic Bank Zambia, Company Registration No. 6559Document4 pagesPayment Instruction - Summary Report: Stanbic Bank Zambia, Company Registration No. 6559Daniel KaundaNo ratings yet

- Ce MasDocument97 pagesCe MasrylNo ratings yet

- Chapter 4Document8 pagesChapter 4Fekadegeta AdibibNo ratings yet

- Financial Market Final QuestionsDocument6 pagesFinancial Market Final Questionsnewaybeyene5No ratings yet

- FIXED INCOME SECURITIES AND DEBT MARKETS Chapter 5 ANSWERSDocument14 pagesFIXED INCOME SECURITIES AND DEBT MARKETS Chapter 5 ANSWERSShilpika ShettyNo ratings yet

- General Banking Functions of Al-Arafah Islami Bank Limited.: Internship ReportDocument58 pagesGeneral Banking Functions of Al-Arafah Islami Bank Limited.: Internship ReportAmazing SongNo ratings yet

- Cir 210485133300Document2 pagesCir 210485133300Bea LouiseNo ratings yet

- Abu Bakkar Sani Askkari ExpDocument234 pagesAbu Bakkar Sani Askkari Expmalik omerNo ratings yet

- Account Statement As of 08-06-2020 15:04:32 GMT +0530Document16 pagesAccount Statement As of 08-06-2020 15:04:32 GMT +0530sunojNo ratings yet

- Final Project of Home LoanDocument63 pagesFinal Project of Home Loansheetalvaviya6439No ratings yet

- EDE Practicals PDFDocument34 pagesEDE Practicals PDFTanmay BhatewaraNo ratings yet

- Wolaita Sodo Unversity College of Business and Economics Department of Accounting and FinanceDocument6 pagesWolaita Sodo Unversity College of Business and Economics Department of Accounting and FinanceEndrias EyanoNo ratings yet

- Abhishek Singh: Education SkillsDocument1 pageAbhishek Singh: Education SkillsHarsh ShekharNo ratings yet

- LibroDocument212 pagesLibromiguelchp02No ratings yet

- Covered Bond LLP ListDocument18 pagesCovered Bond LLP Listsriram1901yeleswarapuNo ratings yet

- Ha Andhra Bank: Cdamo Dhay PeddDocument5 pagesHa Andhra Bank: Cdamo Dhay PeddMahesh NidumoluNo ratings yet

- Bank Management SystemDocument5 pagesBank Management SystemMohd ShahramNo ratings yet

- MCQ FA1 TenDocument12 pagesMCQ FA1 TenZeeshan BakaliNo ratings yet

- 03 - FM-II - Week 4 - Sessions 9-11 - Application AssignmentDocument2 pages03 - FM-II - Week 4 - Sessions 9-11 - Application Assignmentsparshithrs2No ratings yet

- G1 (Sanket Awate) Pem PFSDocument5 pagesG1 (Sanket Awate) Pem PFSNirank JadhavNo ratings yet

- Substantive Tests 1 Copy - CompressDocument11 pagesSubstantive Tests 1 Copy - Compressmariakate LeeNo ratings yet

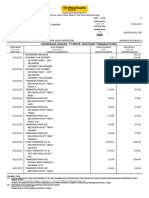

- Histori Transaksi 1712227606648Document4 pagesHistori Transaksi 1712227606648yuribekariNo ratings yet

- Banking Services and Habits ProjectDocument90 pagesBanking Services and Habits Projectgnanesh addepalliNo ratings yet

- Debt Restructuring Theories QuestionsDocument10 pagesDebt Restructuring Theories QuestionsPushTheStart GamingNo ratings yet

- Ibs Pandan Jaya 1 31/12/23Document17 pagesIbs Pandan Jaya 1 31/12/23nor.atikahNo ratings yet

- Role of Micro Finance Institutions MfisDocument8 pagesRole of Micro Finance Institutions MfisMohammad Adnan RummanNo ratings yet

- Accounts Paper 1 November 2007Document7 pagesAccounts Paper 1 November 2007WayneNo ratings yet

- Sunshine ContractDocument13 pagesSunshine Contractnick wilkinsonNo ratings yet

- Date Particulars Withdrawals Deposits BalanceDocument2 pagesDate Particulars Withdrawals Deposits BalanceUrooj AhmedNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Financial Accounting - Rev Partner-2Document168 pagesFinancial Accounting - Rev Partner-2JOHN KAMANDA100% (1)

- MODULE 1 Lecture Notes (Jeff Madura)Document4 pagesMODULE 1 Lecture Notes (Jeff Madura)Romen CenizaNo ratings yet

- Debt InstrumentsDocument53 pagesDebt Instrumentskinjalkapadia087118100% (6)

- FM 03 Financial IntermediationDocument8 pagesFM 03 Financial IntermediationIvy ObligadoNo ratings yet

- Financial Markets LowDocument17 pagesFinancial Markets LowNelsonMoseMNo ratings yet

- Questions Chapter TwoDocument5 pagesQuestions Chapter TwoRose Sánchez0% (1)

- Investment Bankers and Scope FinalDocument48 pagesInvestment Bankers and Scope FinalAkash Gupta0% (1)

- STUDENT Capital and Bond Market UNITDocument24 pagesSTUDENT Capital and Bond Market UNITTetiana VozniukNo ratings yet

- Examples of Financial MarketsDocument3 pagesExamples of Financial Marketskate trishaNo ratings yet

- Capital Markets.Document32 pagesCapital Markets.api-3727090No ratings yet

- Capital Market - A BriefDocument7 pagesCapital Market - A BriefasfaarsafiNo ratings yet

- Credit MarketsDocument12 pagesCredit MarketsDarlyn CarelNo ratings yet

- An Overview of The Financial SystemDocument15 pagesAn Overview of The Financial SystemBerk YAZARNo ratings yet

- Gen Math Stocks and BondsDocument41 pagesGen Math Stocks and BondsDaniel VillahermosaNo ratings yet

- A Financial MarketDocument5 pagesA Financial MarketSalvador SantosNo ratings yet

- Background On Mortgages: Mortgage MarketsDocument7 pagesBackground On Mortgages: Mortgage MarketsPaw VerdilloNo ratings yet

- Chapter 5 FIMDocument13 pagesChapter 5 FIMMintayto TebekaNo ratings yet

- Solution Manual For Principles of Managerial Finance Brief 8th Edition ZutterDocument24 pagesSolution Manual For Principles of Managerial Finance Brief 8th Edition Zuttermichellelewismqdacbxijt100% (53)

- Business Breif U06-2 PDFDocument1 pageBusiness Breif U06-2 PDFAdam MichałekNo ratings yet

- FINAL-fm Project of Group No-13Document29 pagesFINAL-fm Project of Group No-13Prashant PatelNo ratings yet

- Operario, Gabrielle Mae - MODULE3 - ASSIGNMENT - BOND MARKET SECURITIESDocument5 pagesOperario, Gabrielle Mae - MODULE3 - ASSIGNMENT - BOND MARKET SECURITIESGabby OperarioNo ratings yet

- BFM NotesDocument10 pagesBFM Notesravitejaraviteja11111No ratings yet

- M&B Lesson 4 The Financial SystemDocument12 pagesM&B Lesson 4 The Financial SystemAnthony BandaNo ratings yet

- Islamic Vs Modern BONDDocument18 pagesIslamic Vs Modern BONDPakassignmentNo ratings yet

- Report in MTH of IntDocument6 pagesReport in MTH of Intangie valenzuelaNo ratings yet

- Module Code: Umed8S-30-1 MODULE TITLE: Financial Institutions and Markets STUDENT NUMBER: 20055737 Online Exam Section ADocument3 pagesModule Code: Umed8S-30-1 MODULE TITLE: Financial Institutions and Markets STUDENT NUMBER: 20055737 Online Exam Section ALinh Nguyễn Hoàng PhươngNo ratings yet

- Derivatives CaseDocument10 pagesDerivatives CaseLương Thế CườngNo ratings yet

- Finance TestDocument6 pagesFinance Testqylimstephy100% (1)

- Types of Financial InstitutionsDocument9 pagesTypes of Financial InstitutionsfathimabindmohdNo ratings yet

- Savings, Investment and The Financial System CH 26Document29 pagesSavings, Investment and The Financial System CH 26Md. Mehedi HasanNo ratings yet

- FIM Group Assignmen FinalDocument9 pagesFIM Group Assignmen FinalEndeg KelkayNo ratings yet

- Definition of 'Stock Market'Document3 pagesDefinition of 'Stock Market'Karla BordonesNo ratings yet

- Contemporary Financial Management 14th Edition Moyer Solutions ManualDocument35 pagesContemporary Financial Management 14th Edition Moyer Solutions Manualexedentzigzag.96ewc96% (27)

- Financial MarketDocument8 pagesFinancial MarkettiloooNo ratings yet

- Saint Mary'S University: Faculty of Accounting and FinanceDocument10 pagesSaint Mary'S University: Faculty of Accounting and FinanceruhamaNo ratings yet

- Saint Mary'S University: Faculty of Accounting and FinanceDocument10 pagesSaint Mary'S University: Faculty of Accounting and FinanceruhamaNo ratings yet

- T4-4.4. The Financial SectorDocument6 pagesT4-4.4. The Financial SectorBlu BostockNo ratings yet

- Financial System and MarketsDocument17 pagesFinancial System and MarketsDipesh GautamNo ratings yet

- Ilovepdf MergedDocument582 pagesIlovepdf MergedSahil SawantNo ratings yet

- 1 The Investment Industry A Top Down ViewDocument24 pages1 The Investment Industry A Top Down Viewakash jainNo ratings yet

- Specialty CorporationDocument171 pagesSpecialty CorporationAdrian Steven Claude CosicoNo ratings yet

- Financial M R AsiignmentDocument12 pagesFinancial M R AsiignmentDHARAM DEEPAK VISHWASHNo ratings yet

- Financial Markets and Institutions 1Document29 pagesFinancial Markets and Institutions 1Hamza Iqbal100% (1)

- Fin Market and InstitutionDocument3 pagesFin Market and Institutionzeus manNo ratings yet

- Securities Market - CLCDocument7 pagesSecurities Market - CLChoangngothanhtrangNo ratings yet

- Benavidez, Ramcie A. Bsba FM TF-7:00-8:30pm 4FM6Document3 pagesBenavidez, Ramcie A. Bsba FM TF-7:00-8:30pm 4FM6Ramcie Aguilar BenavidezNo ratings yet

- Ict2 ST Agnes Bulaon Jun 7pmquizDocument18 pagesIct2 ST Agnes Bulaon Jun 7pmquizArjeune Victoria BulaonNo ratings yet

- 02 - Handout - 1 (FINANCIAL MARKETS AND INSTITUTIONS)Document6 pages02 - Handout - 1 (FINANCIAL MARKETS AND INSTITUTIONS)Janrey RomanNo ratings yet

- Question 1) Briefly Explain Capital Allocation Process With The Help of Diagram?Document7 pagesQuestion 1) Briefly Explain Capital Allocation Process With The Help of Diagram?Usama KhanNo ratings yet

- Hedge ProfileDocument37 pagesHedge ProfilePramod PNo ratings yet

- Specialized Financial Institutions.: by MKDocument47 pagesSpecialized Financial Institutions.: by MKSarwan GulNo ratings yet

- Financial IntermediationDocument14 pagesFinancial IntermediationKimberly BastesNo ratings yet

- Securitization CitedDocument13 pagesSecuritization CitedBrighton NabiswaNo ratings yet

- Assignment No. 4 Roll No. L-1184 Financial Institution Topic: Bond Market, Stock Market and Mortgage Market Submitted To: Sir Abdul Qadeer Submitted By: Zainab Shabbir Dated: 21 June, 2020Document16 pagesAssignment No. 4 Roll No. L-1184 Financial Institution Topic: Bond Market, Stock Market and Mortgage Market Submitted To: Sir Abdul Qadeer Submitted By: Zainab Shabbir Dated: 21 June, 2020Faisal NaqviNo ratings yet

- ABIYDocument9 pagesABIYEyob HaylemariamNo ratings yet

- 1 I 1.1 O F S: Ntroduction Verview OF THE Inancial YstemDocument8 pages1 I 1.1 O F S: Ntroduction Verview OF THE Inancial YstemAyanda Yan'Dee DimphoNo ratings yet

- Chapter Two-The Financial Environment: Markets, Institutions and Investment BanksDocument4 pagesChapter Two-The Financial Environment: Markets, Institutions and Investment Banksmaquesurat ferdousNo ratings yet

- FM - 3Document4 pagesFM - 3Qani SalvaNo ratings yet

- Financial Environment - Lecture2Document20 pagesFinancial Environment - Lecture2mehnaz kNo ratings yet

- Purple Gradient 3D Bold Modern Investing Tips PresentationDocument47 pagesPurple Gradient 3D Bold Modern Investing Tips PresentationJana Beni Carolyn R. SabadoNo ratings yet

- The Great Recession: The burst of the property bubble and the excesses of speculationFrom EverandThe Great Recession: The burst of the property bubble and the excesses of speculationNo ratings yet

- Payment Instruction - Summary Report: Stanbic Bank Zambia, Company Registration No. 6559Document4 pagesPayment Instruction - Summary Report: Stanbic Bank Zambia, Company Registration No. 6559Daniel KaundaNo ratings yet

- Ce MasDocument97 pagesCe MasrylNo ratings yet

- Chapter 4Document8 pagesChapter 4Fekadegeta AdibibNo ratings yet

- Financial Market Final QuestionsDocument6 pagesFinancial Market Final Questionsnewaybeyene5No ratings yet

- FIXED INCOME SECURITIES AND DEBT MARKETS Chapter 5 ANSWERSDocument14 pagesFIXED INCOME SECURITIES AND DEBT MARKETS Chapter 5 ANSWERSShilpika ShettyNo ratings yet

- General Banking Functions of Al-Arafah Islami Bank Limited.: Internship ReportDocument58 pagesGeneral Banking Functions of Al-Arafah Islami Bank Limited.: Internship ReportAmazing SongNo ratings yet

- Cir 210485133300Document2 pagesCir 210485133300Bea LouiseNo ratings yet

- Abu Bakkar Sani Askkari ExpDocument234 pagesAbu Bakkar Sani Askkari Expmalik omerNo ratings yet

- Account Statement As of 08-06-2020 15:04:32 GMT +0530Document16 pagesAccount Statement As of 08-06-2020 15:04:32 GMT +0530sunojNo ratings yet

- Final Project of Home LoanDocument63 pagesFinal Project of Home Loansheetalvaviya6439No ratings yet

- EDE Practicals PDFDocument34 pagesEDE Practicals PDFTanmay BhatewaraNo ratings yet

- Wolaita Sodo Unversity College of Business and Economics Department of Accounting and FinanceDocument6 pagesWolaita Sodo Unversity College of Business and Economics Department of Accounting and FinanceEndrias EyanoNo ratings yet

- Abhishek Singh: Education SkillsDocument1 pageAbhishek Singh: Education SkillsHarsh ShekharNo ratings yet

- LibroDocument212 pagesLibromiguelchp02No ratings yet

- Covered Bond LLP ListDocument18 pagesCovered Bond LLP Listsriram1901yeleswarapuNo ratings yet

- Ha Andhra Bank: Cdamo Dhay PeddDocument5 pagesHa Andhra Bank: Cdamo Dhay PeddMahesh NidumoluNo ratings yet

- Bank Management SystemDocument5 pagesBank Management SystemMohd ShahramNo ratings yet

- MCQ FA1 TenDocument12 pagesMCQ FA1 TenZeeshan BakaliNo ratings yet

- 03 - FM-II - Week 4 - Sessions 9-11 - Application AssignmentDocument2 pages03 - FM-II - Week 4 - Sessions 9-11 - Application Assignmentsparshithrs2No ratings yet

- G1 (Sanket Awate) Pem PFSDocument5 pagesG1 (Sanket Awate) Pem PFSNirank JadhavNo ratings yet

- Substantive Tests 1 Copy - CompressDocument11 pagesSubstantive Tests 1 Copy - Compressmariakate LeeNo ratings yet

- Histori Transaksi 1712227606648Document4 pagesHistori Transaksi 1712227606648yuribekariNo ratings yet

- Banking Services and Habits ProjectDocument90 pagesBanking Services and Habits Projectgnanesh addepalliNo ratings yet

- Debt Restructuring Theories QuestionsDocument10 pagesDebt Restructuring Theories QuestionsPushTheStart GamingNo ratings yet

- Ibs Pandan Jaya 1 31/12/23Document17 pagesIbs Pandan Jaya 1 31/12/23nor.atikahNo ratings yet

- Role of Micro Finance Institutions MfisDocument8 pagesRole of Micro Finance Institutions MfisMohammad Adnan RummanNo ratings yet

- Accounts Paper 1 November 2007Document7 pagesAccounts Paper 1 November 2007WayneNo ratings yet

- Sunshine ContractDocument13 pagesSunshine Contractnick wilkinsonNo ratings yet

- Date Particulars Withdrawals Deposits BalanceDocument2 pagesDate Particulars Withdrawals Deposits BalanceUrooj AhmedNo ratings yet