Download as pptx, pdf, or txt

You might also like

- Compensation & Benefits of Airline IndustryDocument20 pagesCompensation & Benefits of Airline Industryjason_bourne_900No ratings yet

- TexasTech Adams Contract 4-1-22Document13 pagesTexasTech Adams Contract 4-1-22Carlos Silva, Jr.No ratings yet

- Workday Human Capital Management DatasheetDocument4 pagesWorkday Human Capital Management DatasheetWorkdayNo ratings yet

- Chapter 5 HRMDocument47 pagesChapter 5 HRMJennalynNo ratings yet

- Creative CompensationDocument7 pagesCreative Compensationdua khanNo ratings yet

- Compensation and Benefits Compensation and BenefitsDocument34 pagesCompensation and Benefits Compensation and BenefitsKirti ShivakumarNo ratings yet

- Chapter 6 HBO 1Document10 pagesChapter 6 HBO 1Mars MandigmaNo ratings yet

- Obhrm Unit-5-1Document17 pagesObhrm Unit-5-1Abhishek KunchalaNo ratings yet

- Unit-IV HRMDocument10 pagesUnit-IV HRMSaini Lakhvindar singhNo ratings yet

- Compensation MGT 260214Document224 pagesCompensation MGT 260214Thiru VenkatNo ratings yet

- HRM Unit 4Document44 pagesHRM Unit 4Manigandan .RNo ratings yet

- BobbDocument3 pagesBobbJustine angelesNo ratings yet

- Compensation Administration - August 30, 2022Document20 pagesCompensation Administration - August 30, 2022Gabrielle IbascoNo ratings yet

- HRM Exam ModsDocument51 pagesHRM Exam ModsAlthea Joy PauleNo ratings yet

- Compensation and Managing Human ResourcesDocument21 pagesCompensation and Managing Human ResourcesKath ViloraNo ratings yet

- Compensation ManagementDocument19 pagesCompensation ManagementDesh Bandhu KaitNo ratings yet

- Kompensasi Dan Manfaat InternasionalDocument9 pagesKompensasi Dan Manfaat Internasional20. Komang Ayu Sukma GinantiNo ratings yet

- Comp MGT Mba IV Sem Unit 1 NotesDocument15 pagesComp MGT Mba IV Sem Unit 1 NotesMehak BhargavNo ratings yet

- CH 7Document5 pagesCH 7hailu mekonenNo ratings yet

- Human Resource Management: Employee Compensation GuideDocument4 pagesHuman Resource Management: Employee Compensation Guideaqsa goharNo ratings yet

- HRM8 Compensating HRDocument12 pagesHRM8 Compensating HRarantonizhaNo ratings yet

- ESOPDocument40 pagesESOPsimonebandrawala9No ratings yet

- Submitted To: Amita Sharma Submitted By: Aditya Kumar Section-A Enrollment No. - 16flicddno1006Document14 pagesSubmitted To: Amita Sharma Submitted By: Aditya Kumar Section-A Enrollment No. - 16flicddno1006Aditya PandeyNo ratings yet

- (Unit 4-) Human Resource Management - Kmbn-202Document14 pages(Unit 4-) Human Resource Management - Kmbn-202Tanya MalviyaNo ratings yet

- Lesson-4 CONTEMPORARY WORLDDocument19 pagesLesson-4 CONTEMPORARY WORLDMicaella JanNo ratings yet

- Lesson 4 (HRM Reporting)Document79 pagesLesson 4 (HRM Reporting)Eldeen EscuadroNo ratings yet

- Compensation 8th Module NotesDocument45 pagesCompensation 8th Module NotesSreejith C S SreeNo ratings yet

- Session 3Document44 pagesSession 3Marielle Ace Gole CruzNo ratings yet

- Compensation ManagementDocument27 pagesCompensation ManagementsachinmanjuNo ratings yet

- CPM Unit - IDocument11 pagesCPM Unit - Imba departmentNo ratings yet

- HRM Chap 8Document11 pagesHRM Chap 8Yosef KetemaNo ratings yet

- Compensation ManagementDocument5 pagesCompensation Managementjagannadha raoNo ratings yet

- Unit-9 Compensation ManagementDocument5 pagesUnit-9 Compensation Managementjagannadha raoNo ratings yet

- Introduction To Pay SystemDocument25 pagesIntroduction To Pay SystemSubhashNo ratings yet

- Employee CompensationDocument9 pagesEmployee CompensationHemant AgarwalNo ratings yet

- Compensation MGT 260214Document224 pagesCompensation MGT 260214Vivek KadamNo ratings yet

- Compensation and BenefitsDocument7 pagesCompensation and BenefitsMaiaDeepNo ratings yet

- WageDocument137 pagesWagebavantika29No ratings yet

- Incentives and BenefitsDocument14 pagesIncentives and BenefitsAditya PandeyNo ratings yet

- Compensation and Benefits AssignmentDocument10 pagesCompensation and Benefits AssignmentManinder KaurNo ratings yet

- Compensation AdministrationDocument8 pagesCompensation AdministrationABM 12-1 EMERALD ATTENDANCENo ratings yet

- Human Resource Management 14 Edition Chapter 9 & 10 CompensationDocument43 pagesHuman Resource Management 14 Edition Chapter 9 & 10 CompensationTanvir AhmedNo ratings yet

- Oam Module 4 - Q2Document22 pagesOam Module 4 - Q2Sherilyn InsonNo ratings yet

- Human Resource ManagementDocument13 pagesHuman Resource ManagementNk MehtaNo ratings yet

- COMPENSATION MGT Topic No 1Document7 pagesCOMPENSATION MGT Topic No 1Ashish Khadakhade100% (1)

- Meaning: Types of CompensationDocument5 pagesMeaning: Types of CompensationShyam MaariNo ratings yet

- Io Psych Chap7 Report - 20240320 - 154527 - 0000Document19 pagesIo Psych Chap7 Report - 20240320 - 154527 - 0000claire001024No ratings yet

- Pondicherry University: Compensation ManagementDocument228 pagesPondicherry University: Compensation Managementprathamesh suralkarNo ratings yet

- Unit 6Document34 pagesUnit 6Anwesha KarmakarNo ratings yet

- Compensation DefinitionDocument6 pagesCompensation DefinitionshorifmrhNo ratings yet

- Vaishnavi 1Document7 pagesVaishnavi 1Ritesh SinghNo ratings yet

- Compensation Management and Incentives: Mr. Kumar Satyam Amity University Jharkhand, RanchiDocument23 pagesCompensation Management and Incentives: Mr. Kumar Satyam Amity University Jharkhand, RanchiRaviNo ratings yet

- Synopsis of CompensationDocument15 pagesSynopsis of CompensationShipra Jain0% (2)

- CompensationDocument8 pagesCompensationJustine angelesNo ratings yet

- Compensation HRM 3Document5 pagesCompensation HRM 3Alamin tahaminNo ratings yet

- C&B Module 2 Compensation PlanningDocument18 pagesC&B Module 2 Compensation PlanningkedarambikarNo ratings yet

- 4 th unitHRMDocument5 pages4 th unitHRMFitha FathimaNo ratings yet

- Unit - 4 HRMDocument10 pagesUnit - 4 HRMAatif AatifNo ratings yet

- Compensation HRMDocument7 pagesCompensation HRMMica Abanador100% (1)

- Compensation Systems, Job Performance, and How to Ask for a Pay RaiseFrom EverandCompensation Systems, Job Performance, and How to Ask for a Pay RaiseNo ratings yet

- Model Answer: Literature review on Employee motivation, rewards and performanceFrom EverandModel Answer: Literature review on Employee motivation, rewards and performanceNo ratings yet

- Test Report 2Document32 pagesTest Report 2Artik JainNo ratings yet

- Section C Compensation Strategy For ZenithDocument12 pagesSection C Compensation Strategy For Zenithadeol5012No ratings yet

- Debtors Motion for Interim and Final Orders Pursuant to Bankruptcy Code Sections 105, 363(b), 507(a), 541, 1107(a) and 1108, Authorizing, But Not Directing, the Debtor, Inter Alia, to Pay Prepetition Wages, Compensation, and Employee Benefits filed by Scott Eric Ratner on behalf of Dewey & LeBoeuf LLP. (Attachments: # (1) Exhibit A - Proposed Interim Order# (2) Exhibit B - Proposed Final Order)Document22 pagesDebtors Motion for Interim and Final Orders Pursuant to Bankruptcy Code Sections 105, 363(b), 507(a), 541, 1107(a) and 1108, Authorizing, But Not Directing, the Debtor, Inter Alia, to Pay Prepetition Wages, Compensation, and Employee Benefits filed by Scott Eric Ratner on behalf of Dewey & LeBoeuf LLP. (Attachments: # (1) Exhibit A - Proposed Interim Order# (2) Exhibit B - Proposed Final Order)Chapter 11 DocketsNo ratings yet

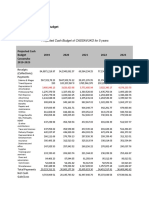

- Sample Financial StatementDocument8 pagesSample Financial StatementMax Sedric L LaylayNo ratings yet

- Ideal Company:bossDocument1 pageIdeal Company:bossSkoro EducationNo ratings yet

- FO PPT Employees As PromotersDocument13 pagesFO PPT Employees As PromotersYash TokarNo ratings yet

- Taxation Part 2Document101 pagesTaxation Part 2Akeefah BrockNo ratings yet

- Caf 06 Principles of Taxation QBDocument115 pagesCaf 06 Principles of Taxation QBSajid Ali100% (2)

- Chapter 6 Motivation - NotesDocument6 pagesChapter 6 Motivation - NotesAli NehanNo ratings yet

- Productivity of Cement Industry of PakistanDocument37 pagesProductivity of Cement Industry of Pakistansyed usman wazir100% (9)

- 2015 Competition Forum Issue 2Document197 pages2015 Competition Forum Issue 2maheraldamatiNo ratings yet

- Project On Fringe BenefitsDocument60 pagesProject On Fringe BenefitsSunakshiRattan33% (3)

- Employee EngagementDocument37 pagesEmployee EngagementBhavya KapoorNo ratings yet

- Revenue Memorandum Circular No. 50-2018: Quezon CityDocument18 pagesRevenue Memorandum Circular No. 50-2018: Quezon CityKyleZapanta100% (1)

- Business Studies P1 Grade 12 June 2024 - MG Modera - 240605 - 153016Document30 pagesBusiness Studies P1 Grade 12 June 2024 - MG Modera - 240605 - 153016malebomokwena07No ratings yet

- Sample Budget and Justification (No Match Required)Document7 pagesSample Budget and Justification (No Match Required)joy margaNo ratings yet

- NTCCDocument19 pagesNTCCPreeti AnandNo ratings yet

- Module 8 - Inclusion of Gross IncomeDocument4 pagesModule 8 - Inclusion of Gross IncomeReicaNo ratings yet

- Form e 2022 Bi 16012023Document7 pagesForm e 2022 Bi 16012023Fatimah IsmailNo ratings yet

- Fast Track Quick Revision AY 16-17 PDFDocument49 pagesFast Track Quick Revision AY 16-17 PDFJyoti Sankar Bairagi67% (3)

- Britannia IndustriesDocument27 pagesBritannia Industriesdiksha chauhanNo ratings yet

- Business Registration and LicensingDocument30 pagesBusiness Registration and LicensingRheneir MoraNo ratings yet

- Qs N AnsDocument7 pagesQs N AnsUzair Fareed100% (2)

- AssignmentDocument5 pagesAssignmentSuyash PrakashNo ratings yet

- FTE-PF Nominee FormDocument3 pagesFTE-PF Nominee FormgangadharNo ratings yet

- Lopez Sugar Corporation vs. Federation of Free WorkersDocument19 pagesLopez Sugar Corporation vs. Federation of Free Workersdos2reqjNo ratings yet

- TDS Ready ReckonerDocument29 pagesTDS Ready ReckonerShivani Singh ChandelNo ratings yet

- Taxation Law 1 Final Examination Part I: Multiple Choice QuestionsDocument8 pagesTaxation Law 1 Final Examination Part I: Multiple Choice Questionsfrance marie annNo ratings yet