Download as pptx, pdf, or txt

You might also like

- The Ideal ExecutiveDocument39 pagesThe Ideal ExecutiveValery Moran50% (2)

- ACC 206 Incomplete Manufacturing Costs Expenses and Selling Data For Two Different Cases Are As FDocument3 pagesACC 206 Incomplete Manufacturing Costs Expenses and Selling Data For Two Different Cases Are As FebadbaddevNo ratings yet

- Chicago Real Estate AgentsDocument534 pagesChicago Real Estate AgentsBasit MushtaqNo ratings yet

- EDF Investor Guide On SEC Climate RuleDocument7 pagesEDF Investor Guide On SEC Climate RuleEren IleriNo ratings yet

- ING Think Why Us Secs Proposed Climate Disclosure Rules Are A Game ChangerDocument6 pagesING Think Why Us Secs Proposed Climate Disclosure Rules Are A Game ChangerOwm Close CorporationNo ratings yet

- SEC Rule Sierra Club AnalysisDocument18 pagesSEC Rule Sierra Club AnalysisEren IleriNo ratings yet

- SigreensDocument15 pagesSigreensksjzxg58bqNo ratings yet

- BCG Esg ComplianceDocument9 pagesBCG Esg Compliance15G.V.Pranav12-DNo ratings yet

- Insurance Amendmen Bill 2023 Insurance Alert HongkongDocument6 pagesInsurance Amendmen Bill 2023 Insurance Alert Hongkongho576464No ratings yet

- Ey tl21228 231us 04 04 2024Document14 pagesEy tl21228 231us 04 04 2024Imran KhanNo ratings yet

- AC - Annual Report 20Document168 pagesAC - Annual Report 20Hamadah HamadahNo ratings yet

- Climate - Map Stage 0Document8 pagesClimate - Map Stage 0Bob BertNo ratings yet

- Issb Exposure Draft 2022 2 Climate Related DisclosuresDocument60 pagesIssb Exposure Draft 2022 2 Climate Related DisclosuresRiny AgustinNo ratings yet

- Sustainability Reporting Frameworks 2023Document39 pagesSustainability Reporting Frameworks 2023Mohsin Khan100% (1)

- Csa 20211018 51-107 Disclosure-UpdateDocument74 pagesCsa 20211018 51-107 Disclosure-UpdateJESUS LAREZNo ratings yet

- Asia Response To The Finalised Issb Ifrs s1 and Ifrs s2 StandardsDocument20 pagesAsia Response To The Finalised Issb Ifrs s1 and Ifrs s2 StandardslukefernandezNo ratings yet

- CDP Credible Climate Transition Plans 1696512641Document27 pagesCDP Credible Climate Transition Plans 1696512641Hoa SuNo ratings yet

- Key Emerging Regulatory Issues Focus Areas Institutional Asset ManagersDocument7 pagesKey Emerging Regulatory Issues Focus Areas Institutional Asset ManagersSAI SUVEDHYA RNo ratings yet

- Measuring Climate-Related Risks in Investment PortfoliosDocument12 pagesMeasuring Climate-Related Risks in Investment PortfoliosJayv EwentryNo ratings yet

- A Framework and Principles For in Financing Operations: Climate Resilience MetricsDocument41 pagesA Framework and Principles For in Financing Operations: Climate Resilience MetricslaibaNo ratings yet

- What Audit Committees Should Prioritize in 2023Document27 pagesWhat Audit Committees Should Prioritize in 2023Yoddy PutraNo ratings yet

- The Climate-Related Financial Disclosure Regulations 2022: A Step in The Right Direction For ESG in The Private SectorDocument20 pagesThe Climate-Related Financial Disclosure Regulations 2022: A Step in The Right Direction For ESG in The Private SectorAdriana CarpiNo ratings yet

- Wind Assisted Ship Propulsion For Joint Industry Project - WiSPJIPDocument4 pagesWind Assisted Ship Propulsion For Joint Industry Project - WiSPJIPHua Hidari YangNo ratings yet

- Guide To Greenhouse Gas Emissions (Interim)Document11 pagesGuide To Greenhouse Gas Emissions (Interim)av1986362No ratings yet

- ESG Reporting: What Climate Risk Disclosures Mean For Federal ContractorsDocument21 pagesESG Reporting: What Climate Risk Disclosures Mean For Federal ContractorsKevin RamrattanNo ratings yet

- Criteria For High-Quality Carbon RemovalDocument58 pagesCriteria For High-Quality Carbon RemovalMark Sasongko100% (1)

- Business Responsibility and Sustainability Reporting by Listed EntitiesDocument10 pagesBusiness Responsibility and Sustainability Reporting by Listed EntitiesMohammad AamirNo ratings yet

- LCFS and CCS Protocol Digital Version 2Document24 pagesLCFS and CCS Protocol Digital Version 2vineetakaushik83No ratings yet

- CBI Transport Criteria Document - Apr2021Document24 pagesCBI Transport Criteria Document - Apr2021GamachuNo ratings yet

- Turning The Corner: Regulatory FrameworkDocument34 pagesTurning The Corner: Regulatory FrameworkANDI Agencia de Noticias do Direito da InfanciaNo ratings yet

- 联交所GSE咨詢文件 April 2023 (Eng)Document106 pages联交所GSE咨詢文件 April 2023 (Eng)rickychung.miniNo ratings yet

- The Big Ebook of Sustainability Reporting Frameworks - enDocument73 pagesThe Big Ebook of Sustainability Reporting Frameworks - enabdulraqeeb alareqiNo ratings yet

- Ey CBM What Auidt Committees Should Prioritize in 2023Document27 pagesEy CBM What Auidt Committees Should Prioritize in 2023TUREEN NABEEL MIZORYNo ratings yet

- Cap and Invest NYCI Pre-Proposal Outline FinalDocument33 pagesCap and Invest NYCI Pre-Proposal Outline FinalrkarlinNo ratings yet

- In The Spotlight How Software Accelerates Sustainability Reporting and Performance Management FINAL CompressedDocument18 pagesIn The Spotlight How Software Accelerates Sustainability Reporting and Performance Management FINAL CompressedDDNo ratings yet

- Consultation Paper On ESG by SEBIDocument27 pagesConsultation Paper On ESG by SEBISabSab MukNo ratings yet

- Transition Mapping - Climate Bonds - 6 Nov 2023Document47 pagesTransition Mapping - Climate Bonds - 6 Nov 2023abrahamkabranNo ratings yet

- Ey Ifrs Climate ChangeDocument4 pagesEy Ifrs Climate ChangeIke FinchNo ratings yet

- Pcaf-Standard-Part-C InsuranaceeDocument82 pagesPcaf-Standard-Part-C InsuranaceeNelson DiazNo ratings yet

- BMA Consultation PaperDocument72 pagesBMA Consultation PaperAnonymous UpWci5No ratings yet

- Climate Bonds - Standard - Version 3 - 0 - December 2017Document20 pagesClimate Bonds - Standard - Version 3 - 0 - December 2017Francesco CistarillNo ratings yet

- SBTi GuidelinesDocument14 pagesSBTi GuidelinesswathimblackrhinozNo ratings yet

- IiedDocument4 pagesIiedMallik ArjunNo ratings yet

- A Guide To ESG Standards and FrameworksDocument30 pagesA Guide To ESG Standards and Frameworksaleksandar_tudzarovNo ratings yet

- Jupiter Ebook TheUltimateGuidetoClimateRiskDisclosureRegulationspdfDocument20 pagesJupiter Ebook TheUltimateGuidetoClimateRiskDisclosureRegulationspdfRisk MavenNo ratings yet

- IFRS S1 and S2 Brief FinalDocument10 pagesIFRS S1 and S2 Brief FinalReza MuliaNo ratings yet

- Effects of Climate Related Matters On Financial StatementsDocument6 pagesEffects of Climate Related Matters On Financial StatementsSofiya BayraktarovaNo ratings yet

- Finance BillDocument52 pagesFinance BillAhmed EssalhiNo ratings yet

- IFRS S1 and S2 Brief FinalDocument11 pagesIFRS S1 and S2 Brief FinalKashilNo ratings yet

- WBCSD Climatefinancialimpactguide 2feb24Document47 pagesWBCSD Climatefinancialimpactguide 2feb24Emre GuneyNo ratings yet

- HidrogenoDocument99 pagesHidrogenoJOEDUMPMPNo ratings yet

- Fclim 04 1101525Document11 pagesFclim 04 1101525Muhammad Iqbal FirdausNo ratings yet

- KPMG Get Ready For ISSB Sustainability Disclosures - Understanding The ProposalsDocument17 pagesKPMG Get Ready For ISSB Sustainability Disclosures - Understanding The Proposalsjames jiangNo ratings yet

- Incorporating An Esg Lens in Business ValuationsDocument4 pagesIncorporating An Esg Lens in Business ValuationscheungNo ratings yet

- Ed46d 20 December 2022Document4 pagesEd46d 20 December 2022Shivendra pratap singhNo ratings yet

- Public Private Infrastructure Advisory FacilityDocument14 pagesPublic Private Infrastructure Advisory Facilitycynthia_gomez_agurto1745No ratings yet

- IFRS 4 Phase II and Solvency IIDocument8 pagesIFRS 4 Phase II and Solvency IIAidellediANo ratings yet

- TCFD Scenario Analysis Methodology Outcome - Borregaard GroupDocument20 pagesTCFD Scenario Analysis Methodology Outcome - Borregaard GroupThanh Thủy PhạmNo ratings yet

- Strategic Plan 2022-26Document68 pagesStrategic Plan 2022-26jeremytoh89No ratings yet

- 21 MegaTrends ReportDocument19 pages21 MegaTrends ReportAndhika Herdiawan100% (1)

- ESG Developments in The MENA and GCC Region - Look Back 2021 - Look Ahead 2022Document15 pagesESG Developments in The MENA and GCC Region - Look Back 2021 - Look Ahead 2022Mahmoud shawkyNo ratings yet

- MS GHG Ebook FinalDocument16 pagesMS GHG Ebook Finalkanna2327No ratings yet

- Policies and Investments to Address Climate Change and Air Quality in the Beijing–Tianjin–Hebei RegionFrom EverandPolicies and Investments to Address Climate Change and Air Quality in the Beijing–Tianjin–Hebei RegionNo ratings yet

- Final SCB Environment 2021 Q&ADocument88 pagesFinal SCB Environment 2021 Q&APreetham BharadwajNo ratings yet

- 7850 - Rev - 1 - Preetham Bharadwaj - Nimai Venture Corp. Pvt. LTD - Mysore - Karnataka - Hydraulic T-Model Lift - G+2 - Wheelchair - KrupaDocument8 pages7850 - Rev - 1 - Preetham Bharadwaj - Nimai Venture Corp. Pvt. LTD - Mysore - Karnataka - Hydraulic T-Model Lift - G+2 - Wheelchair - KrupaPreetham BharadwajNo ratings yet

- 7850 - Preetham Bharadwaj - Nimai Venture Corp. Pvt. LTD - Bengaluru - Karnataka - Hydraulic T-Model Lift - G+2 - Wheelchair - VarshaDocument8 pages7850 - Preetham Bharadwaj - Nimai Venture Corp. Pvt. LTD - Bengaluru - Karnataka - Hydraulic T-Model Lift - G+2 - Wheelchair - VarshaPreetham BharadwajNo ratings yet

- Corrected Emission Factor Based On Clinker OutputDocument3 pagesCorrected Emission Factor Based On Clinker OutputPreetham BharadwajNo ratings yet

- Socio Economic Caste Census 2011 PDFDocument5 pagesSocio Economic Caste Census 2011 PDFPreetham BharadwajNo ratings yet

- Compressed Biogas Project: Submitted by Submitted To Preetham Bharadwaj 1522 MER Coordinator (M.TECH REEM) REEM 2015-17Document9 pagesCompressed Biogas Project: Submitted by Submitted To Preetham Bharadwaj 1522 MER Coordinator (M.TECH REEM) REEM 2015-17Preetham BharadwajNo ratings yet

- Tuna Fish ThesisDocument35 pagesTuna Fish ThesisPreetham BharadwajNo ratings yet

- MASTER IRON LABOR UNION (MILU) vs. NATIONAL LABOR RELATIONS COMMISSIONDocument1 pageMASTER IRON LABOR UNION (MILU) vs. NATIONAL LABOR RELATIONS COMMISSIONAreeNo ratings yet

- Module 2Document101 pagesModule 2Sneha Giji SajiNo ratings yet

- Full Operations Management 6Th Edition Test Bank Nigel Slack PDF Docx Full Chapter ChapterDocument23 pagesFull Operations Management 6Th Edition Test Bank Nigel Slack PDF Docx Full Chapter Chaptersuavefiltermyr62100% (31)

- AC Installation Offer - Jan Till Mar 2024Document7 pagesAC Installation Offer - Jan Till Mar 2024SakthiRaj MuralidharanNo ratings yet

- Cad Cam TheoryDocument12 pagesCad Cam TheoryShashank VermaNo ratings yet

- 31jan2019 - PDs CompiledDocument108 pages31jan2019 - PDs CompiledharigroupphilippinesNo ratings yet

- Mandem Mandem: Outline Business Plan Outline Business PlanDocument15 pagesMandem Mandem: Outline Business Plan Outline Business PlanAndrew MwesigyeNo ratings yet

- (My) Insolvency Act 1967 Act 360Document113 pages(My) Insolvency Act 1967 Act 360Haikal AdninNo ratings yet

- Intellectual Property ProtectionDocument3 pagesIntellectual Property ProtectionUmair Raza KhanNo ratings yet

- Organizational Theories For Effective Business ManagementDocument30 pagesOrganizational Theories For Effective Business ManagementMark Reiven A. MendozaNo ratings yet

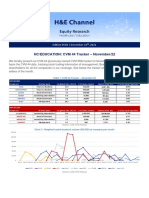

- HC/EDUCATION: CVM 44 Tracker - November/22: Edition #548 - December 16, 2022Document4 pagesHC/EDUCATION: CVM 44 Tracker - November/22: Edition #548 - December 16, 2022CAIO HENRIQUE FIORDELIZNo ratings yet

- Question & Answers Question No.1: How JIT Approach Can Help Dell Inc. To Meet Customer Demand On Time With Effective Inventory Management?Document2 pagesQuestion & Answers Question No.1: How JIT Approach Can Help Dell Inc. To Meet Customer Demand On Time With Effective Inventory Management?Arooj HectorNo ratings yet

- MAS Variable and Absorption CostingDocument11 pagesMAS Variable and Absorption CostingGwyneth TorrefloresNo ratings yet

- All Company and Its Brand and Product: Hindustan Unilever LimitedDocument73 pagesAll Company and Its Brand and Product: Hindustan Unilever Limitedpapa_didi700100% (8)

- Simple and Compound InterestDocument8 pagesSimple and Compound InterestMari Carreon TulioNo ratings yet

- Higher Nationals: Higher National Diploma in ComputingDocument2 pagesHigher Nationals: Higher National Diploma in ComputingDg PinzNo ratings yet

- Ouakouak 2017Document26 pagesOuakouak 2017Cristian RamosNo ratings yet

- Learning Outcome TaxDocument2 pagesLearning Outcome TaxNiño Mendoza MabatoNo ratings yet

- MCK Ceo Collection DemoDocument17 pagesMCK Ceo Collection DemoDiego AristizabalNo ratings yet

- RMC No. 43-2021 RevisedDocument4 pagesRMC No. 43-2021 RevisedPrimadonnaPrincess 03No ratings yet

- Case 4 Hrm520 GowinsDocument6 pagesCase 4 Hrm520 GowinsAliza PlacinoNo ratings yet

- Ey Regulatory Landscape of The Circular EconomyDocument7 pagesEy Regulatory Landscape of The Circular EconomyKoushik PonnuruNo ratings yet

- Timeshare Realty Corporation vs. Cesar Lao and Cynthia V. CortezDocument1 pageTimeshare Realty Corporation vs. Cesar Lao and Cynthia V. CortezCaroru ElNo ratings yet

- PT B2BDocument4 pagesPT B2Bjohni andreiNo ratings yet

- Mec-106 Public EconomicsDocument15 pagesMec-106 Public EconomicsMOHAMMAD NADEEMNo ratings yet

- Moriah Business Plan PDFDocument5 pagesMoriah Business Plan PDFally dereNo ratings yet

- Id-18241054 (B) PDFDocument2 pagesId-18241054 (B) PDFMd Abid RahamanNo ratings yet