Download as ppt, pdf, or txt

You might also like

- Assessment 4 Tax 1Document3 pagesAssessment 4 Tax 1Judy Ann Gaceta0% (1)

- Chapter 17 - Financial ManagementDocument7 pagesChapter 17 - Financial ManagementArsalNo ratings yet

- MA-2018Document261 pagesMA-2018Dr Luis e Valdez rico0% (1)

- Proctoring Policy 5 12Document6 pagesProctoring Policy 5 12Dwi cahyaniNo ratings yet

- Subcontracting With Chargeable Components" and "Material LedgerDocument4 pagesSubcontracting With Chargeable Components" and "Material LedgerjoeindNo ratings yet

- Fin500 PPT CH17Document58 pagesFin500 PPT CH17Sarah SNo ratings yet

- Gitman Chapter 15 Working CapitalDocument67 pagesGitman Chapter 15 Working CapitalArif SharifNo ratings yet

- Working Capital and Current Assets Management: All Rights ReservedDocument58 pagesWorking Capital and Current Assets Management: All Rights ReservedAndrea RosalNo ratings yet

- Working Capital Management 15Document75 pagesWorking Capital Management 15Vany AprilianiNo ratings yet

- Working Capital ManagementDocument73 pagesWorking Capital ManagementThenappan GanesenNo ratings yet

- Class 14 Chapter 14 - Student - 2021Document41 pagesClass 14 Chapter 14 - Student - 2021BenNo ratings yet

- Working Capital ManagementDocument22 pagesWorking Capital Managementeaglefly7864696No ratings yet

- 2013 - UGent IR - Bain Lecture Financial Statements - Voor StudentenDocument23 pages2013 - UGent IR - Bain Lecture Financial Statements - Voor StudentenJanNo ratings yet

- Account Recievable ManagementDocument15 pagesAccount Recievable Managementeaglefly7864696No ratings yet

- Finance OverviewDocument38 pagesFinance OverviewGeethika NayanaprabhaNo ratings yet

- Short Term Financing Lecture NotesDocument15 pagesShort Term Financing Lecture Noteseaglefly7864696No ratings yet

- Topic 1 - Overview of Working Capital ManagementDocument80 pagesTopic 1 - Overview of Working Capital ManagementTâm ThuNo ratings yet

- Chapter 4 Financial ManagementDocument39 pagesChapter 4 Financial Managementmanthan212No ratings yet

- Announcements: Time: Friday, April 14, From 1:30 P.M. To 3:30 P.M. Location: ContentDocument81 pagesAnnouncements: Time: Friday, April 14, From 1:30 P.M. To 3:30 P.M. Location: ContentManav PatelNo ratings yet

- Business Finance - DocxnotesDocument70 pagesBusiness Finance - DocxnotesKimberly ReignsNo ratings yet

- Presentation On Working CapitalDocument86 pagesPresentation On Working Capitalstuddude88No ratings yet

- Working Capital and Cash ManagementDocument65 pagesWorking Capital and Cash Managementrey mark hamacNo ratings yet

- Module 4Document63 pagesModule 4Victor LeeNo ratings yet

- Fin500 PPT CH15Document55 pagesFin500 PPT CH15Sarah SNo ratings yet

- FM Cash ManagementDocument41 pagesFM Cash ManagementDimpol MagsalayNo ratings yet

- Cash and Cash Equivalents Topic 8Document46 pagesCash and Cash Equivalents Topic 8Abd AL Rahman Shah Bin Azlan ShahNo ratings yet

- Individual Assignment 5Document7 pagesIndividual Assignment 5211124022108No ratings yet

- 04-Aspek KeuanganDocument34 pages04-Aspek Keuanganmuhammad rifqirahmanNo ratings yet

- Cash Flow 13Document43 pagesCash Flow 13Khalil Al-QaderiNo ratings yet

- Financial Management Theories: Group 9 & 10Document5 pagesFinancial Management Theories: Group 9 & 10Aaron Dale VillanuevaNo ratings yet

- Objectives of Financial Reporting Objectives of Financial ReportingDocument30 pagesObjectives of Financial Reporting Objectives of Financial ReportingXuuuuuNo ratings yet

- Working Capital ManagementDocument81 pagesWorking Capital ManagementKelvin Tey Kai WenNo ratings yet

- Cash Flow and Financial PlanningDocument64 pagesCash Flow and Financial PlanningAmjad J AliNo ratings yet

- Chap 1Document24 pagesChap 1Bhavesh MahidaNo ratings yet

- Chap 017Document44 pagesChap 017coukslyneNo ratings yet

- Caiib Fmmodbacs Nov08Document91 pagesCaiib Fmmodbacs Nov08monirba48No ratings yet

- CAIIB-Financial Management-Module B Study of Financial StatementsDocument91 pagesCAIIB-Financial Management-Module B Study of Financial StatementsDeepak RathoreNo ratings yet

- Working Capital Management: A PerspectiveDocument21 pagesWorking Capital Management: A PerspectiveSanthosh Philip GeorgeNo ratings yet

- Chapter 18 Working Capital Management - CompressDocument27 pagesChapter 18 Working Capital Management - CompressAshiv MungurNo ratings yet

- Chapter 5 PPT (To Students)Document48 pagesChapter 5 PPT (To Students)Heidi ChanNo ratings yet

- The Scope of Corporate Finance: What Companies DoDocument8 pagesThe Scope of Corporate Finance: What Companies DoRony RahmanNo ratings yet

- 1 Corporate Finance IntroductionDocument21 pages1 Corporate Finance IntroductionNiharika AgarwalNo ratings yet

- CAIIB-Financial Management-Module B Study of Financial Statements C.S.Balakrishnan Faculty Member SPBT CollegeDocument39 pagesCAIIB-Financial Management-Module B Study of Financial Statements C.S.Balakrishnan Faculty Member SPBT CollegeNAGESH GUTTEDARNo ratings yet

- Financing Your New VentureDocument33 pagesFinancing Your New Venturetytry56565No ratings yet

- Statement of Cash Flow: Lecture-8Document11 pagesStatement of Cash Flow: Lecture-8Nirjon BhowmicNo ratings yet

- Ch5 DR - EzzDocument57 pagesCh5 DR - Ezzعمران تركيNo ratings yet

- Cash Management Cash ManagementDocument60 pagesCash Management Cash ManagementGlenn TaduranNo ratings yet

- Unit - 3 - Acma CMC 653Document192 pagesUnit - 3 - Acma CMC 653sakshiNo ratings yet

- WORKING CAPITAL MANAGEMENET BPFA BCD BSC PM DIPMDocument90 pagesWORKING CAPITAL MANAGEMENET BPFA BCD BSC PM DIPMOreratile KeorapetseNo ratings yet

- Gitman Chapter 14 Divident PolicyDocument59 pagesGitman Chapter 14 Divident PolicyArif SharifNo ratings yet

- Notes: Introduction To Working CapitalDocument5 pagesNotes: Introduction To Working CapitalanugpNo ratings yet

- 1 Corporate Finance IntroductionDocument41 pages1 Corporate Finance IntroductionPooja KaulNo ratings yet

- Study of Financial StatementsDocument39 pagesStudy of Financial Statementsagrawalrohit_228384No ratings yet

- Projecting Cash Flow and EarningsDocument46 pagesProjecting Cash Flow and EarningsNaeemNo ratings yet

- 10b. Pro Forma Financial StatementsDocument28 pages10b. Pro Forma Financial StatementsajenggNo ratings yet

- Working Capital ManagementDocument37 pagesWorking Capital ManagementgudunNo ratings yet

- Transaction Banking NotesDocument87 pagesTransaction Banking NotesAnand SrinivasanNo ratings yet

- Chapter 2 Financial Statement and Cash Flow AnalysisDocument26 pagesChapter 2 Financial Statement and Cash Flow AnalysisFarooqChaudharyNo ratings yet

- Finance Function: By: R. P. SharmaDocument24 pagesFinance Function: By: R. P. Sharmaalok_kumar_ca5122No ratings yet

- Working Capital and Current Assets ManagementDocument66 pagesWorking Capital and Current Assets ManagementElmer KennethNo ratings yet

- Chapter 01 Overview of Financial ManagementDocument42 pagesChapter 01 Overview of Financial Management叶文伟No ratings yet

- 1911061657MBA14309EA16working Capital Managementworking Capital Management - 025457 - 041141Document12 pages1911061657MBA14309EA16working Capital Managementworking Capital Management - 025457 - 041141sokit53704No ratings yet

- LN02 Keown33019306 08 LN02 GEDocument52 pagesLN02 Keown33019306 08 LN02 GEEnny HaryantiNo ratings yet

- LN10 Keown33019306 08 LN10 GEDocument68 pagesLN10 Keown33019306 08 LN10 GEEnny HaryantiNo ratings yet

- LN08 Keown33019306 08 LN08 GEDocument40 pagesLN08 Keown33019306 08 LN08 GEEnny HaryantiNo ratings yet

- LN06 Keown33019306 08 LN06 GEDocument70 pagesLN06 Keown33019306 08 LN06 GEEnny HaryantiNo ratings yet

- LN07 Keown33019306 08 LN07 GEDocument56 pagesLN07 Keown33019306 08 LN07 GEEnny HaryantiNo ratings yet

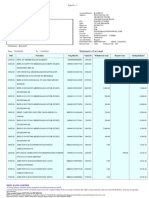

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument34 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceMehndi HasanNo ratings yet

- INKOLLU To Hyderabad: Vikram Srikrishna Travels Service # VSK - 07Document2 pagesINKOLLU To Hyderabad: Vikram Srikrishna Travels Service # VSK - 07Eswar RaoNo ratings yet

- Regd. With A.D. C-11 ESI Corporation, Ashram Road, Ahmedabad-380014Document2 pagesRegd. With A.D. C-11 ESI Corporation, Ashram Road, Ahmedabad-380014Rajput Mittu100% (1)

- Outline For Am Cri 090910Document18 pagesOutline For Am Cri 090910crimproNo ratings yet

- Open Letter To The World Intellectuals On My Repression in The United StatesDocument4 pagesOpen Letter To The World Intellectuals On My Repression in The United StatesKaveh L. AfrasiabiNo ratings yet

- Signs of Laylatul QadrDocument2 pagesSigns of Laylatul QadrMountainofknowledgeNo ratings yet

- Anti-Terrorism Act of 2020Document4 pagesAnti-Terrorism Act of 2020Kyla Ellen CalelaoNo ratings yet

- MCQ Midterms in Land Titles - 2020 - Answer KeyDocument21 pagesMCQ Midterms in Land Titles - 2020 - Answer KeyAr-Reb AquinoNo ratings yet

- (Name of The Association)Document4 pages(Name of The Association)ChanChi Domocmat LaresNo ratings yet

- Lao Gi V CA ESCRA Full Text CaseDocument11 pagesLao Gi V CA ESCRA Full Text CaseYaz CarlomanNo ratings yet

- 1 Assesment Chapter Three PDFDocument62 pages1 Assesment Chapter Three PDFbathsheba ratemoNo ratings yet

- Bautista, Maria Teresa SDocument4 pagesBautista, Maria Teresa SSarip Sharief SaripadaNo ratings yet

- DILG Strategic ThrustDocument22 pagesDILG Strategic ThrustErwin DopiawonNo ratings yet

- 1Document7 pages1JessaNo ratings yet

- HR Generalist Course ContentDocument5 pagesHR Generalist Course ContentswayamNo ratings yet

- Century v. PeopleDocument4 pagesCentury v. Peoplejdg jdgNo ratings yet

- PEARL & DEAN (PHIL.), INC. Vs SHOEMART, INC GR No. 148222Document2 pagesPEARL & DEAN (PHIL.), INC. Vs SHOEMART, INC GR No. 148222Cates Torres100% (1)

- Filinvest Credit Corporation Vs Court of AppealsDocument3 pagesFilinvest Credit Corporation Vs Court of Appealsdivine_carlosNo ratings yet

- Internship Report Based On InsuranceDocument26 pagesInternship Report Based On InsuranceTesnimNo ratings yet

- Take Another Look at Antony Flews Presumption of Atheism - 1995Document9 pagesTake Another Look at Antony Flews Presumption of Atheism - 1995Christopher Ullman100% (1)

- Account Transfer Form: Fax Cover SheetDocument6 pagesAccount Transfer Form: Fax Cover SheetJitendra SharmaNo ratings yet

- Thomas BushellDocument1 pageThomas Bushellapi-361779682No ratings yet

- International Law of Sea PDFDocument14 pagesInternational Law of Sea PDFJitendra RavalNo ratings yet

- CorruptionDocument1 pageCorruptionJohn Richmond RomeroNo ratings yet

- #75 - DUMAPIS, Et - Al. V. LEPANTODocument2 pages#75 - DUMAPIS, Et - Al. V. LEPANTOKê MilanNo ratings yet

- Civil Case FinalDocument14 pagesCivil Case FinalPulkit AgarwalNo ratings yet