Download as ppt, pdf, or txt

You might also like

- MathDocument42 pagesMathMamun RashidNo ratings yet

- Problem Sets Present ValueDocument16 pagesProblem Sets Present ValueJoaquín Norambuena EscalonaNo ratings yet

- RM Quiz 4 Chappa ContentDocument66 pagesRM Quiz 4 Chappa ContentMurad Ahmed Niazi100% (1)

- Exercises - Corporate Finance 1Document12 pagesExercises - Corporate Finance 1Hông HoaNo ratings yet

- Quiz 4 SolutionDocument5 pagesQuiz 4 SolutionSam LindersonNo ratings yet

- Solutions For End-of-Chapter Questions and Problems: Chapter TenDocument27 pagesSolutions For End-of-Chapter Questions and Problems: Chapter TenSam MNo ratings yet

- Week 3 TuteDocument4 pagesWeek 3 TuteSam KellyNo ratings yet

- Tutorial 1 - Time Value of Money 2018 PDFDocument4 pagesTutorial 1 - Time Value of Money 2018 PDFKhouja TeyssirNo ratings yet

- EPC Contract Tool For Project FinanceDocument29 pagesEPC Contract Tool For Project Financeshalw100% (2)

- Solutions To Questions - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications Question 6-1Document16 pagesSolutions To Questions - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications Question 6-1--bolabolaNo ratings yet

- Real Estate Finance and Investments 15th Edition Brueggeman Solutions ManualDocument19 pagesReal Estate Finance and Investments 15th Edition Brueggeman Solutions Manualwilliamvanrqg100% (26)

- Loan ScenariosDocument3 pagesLoan Scenariostroyblood405986No ratings yet

- Mortgage Markets 2 1Document9 pagesMortgage Markets 2 1Janine Bad-angNo ratings yet

- M Finance 3Rd Edition Cornett Test Bank Full Chapter PDFDocument27 pagesM Finance 3Rd Edition Cornett Test Bank Full Chapter PDFcordie.borda532100% (11)

- FIN 438 - Chapter 15 QuestionsDocument6 pagesFIN 438 - Chapter 15 QuestionsTrần Dương Mai PhươngNo ratings yet

- Solutions For End-of-Chapter Questions and Problems: Chapter TenDocument27 pagesSolutions For End-of-Chapter Questions and Problems: Chapter TenYasser AlmishalNo ratings yet

- Fixed Income SecuritiesDocument1 pageFixed Income SecuritiesRaghuveer ChandraNo ratings yet

- Financial Institutions Management - Chap011Document21 pagesFinancial Institutions Management - Chap011sk625218No ratings yet

- Problem SetsDocument69 pagesProblem SetsAnnagrazia Argentieri100% (1)

- Topic 4 - Current Liabilities Sample ProblemsDocument8 pagesTopic 4 - Current Liabilities Sample ProblemsHazel Jane EsclamadaNo ratings yet

- Real Chapter 6Document6 pagesReal Chapter 6mahidafsanaNo ratings yet

- 21 Problems For CB NewDocument5 pages21 Problems For CB NewLinh LinhNo ratings yet

- Current Liabilities Management SOLUTIONSDocument9 pagesCurrent Liabilities Management SOLUTIONSJack Herer100% (1)

- HWCH 8Document3 pagesHWCH 8Victoria G. CrosswellNo ratings yet

- CMA B4.7 Bank LoansDocument13 pagesCMA B4.7 Bank LoansZeinabNo ratings yet

- Week 7 Consumer Credit 2024Document45 pagesWeek 7 Consumer Credit 2024Atika HassanNo ratings yet

- Problem Sets 15 - 401 08Document72 pagesProblem Sets 15 - 401 08Muhammad GhazzianNo ratings yet

- Practice Set - Alternative InvestmentsDocument5 pagesPractice Set - Alternative Investmentsint.saggaNo ratings yet

- Fin 4 WC FinancingDocument2 pagesFin 4 WC FinancingHumphrey OdchigueNo ratings yet

- Solutions For End-of-Chapter Questions and Problems: Chapter TenDocument29 pagesSolutions For End-of-Chapter Questions and Problems: Chapter Tenester jofreyNo ratings yet

- Exercises MortgagesDocument2 pagesExercises MortgagesNicu BotnariNo ratings yet

- Finance Applications and Theory 3rd Edition Cornett Test Bank 1Document120 pagesFinance Applications and Theory 3rd Edition Cornett Test Bank 1kyle100% (49)

- Introduction To Personal Finance SEPT 2015 REVISION PACKDocument27 pagesIntroduction To Personal Finance SEPT 2015 REVISION PACKAnonymous p65I0YZVCNo ratings yet

- Chapter Four Credit Risk: Individual Loan RiskDocument22 pagesChapter Four Credit Risk: Individual Loan RiskMd NaeemNo ratings yet

- Assignment 1Document31 pagesAssignment 1saad bin sadaqatNo ratings yet

- SwapDocument25 pagesSwapBhakti Bhushan MishraNo ratings yet

- Concept Check Quiz: First SessionDocument27 pagesConcept Check Quiz: First SessionMichael MillerNo ratings yet

- Chapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONSDocument9 pagesChapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONSSolutionz Manual67% (3)

- FM Tutorial TVM 2023.24Document5 pagesFM Tutorial TVM 2023.24Đức ThọNo ratings yet

- Time Value of MoneyDocument43 pagesTime Value of MoneyEdwin OctorizaNo ratings yet

- Solutions To Questions - Chapter 4 Fixed Rate Mortgage Loans Question 4-1Document16 pagesSolutions To Questions - Chapter 4 Fixed Rate Mortgage Loans Question 4-1DeliaNo ratings yet

- Chapter 2 Time Value of Money ANSWERS TO END OF CHAPTER QUESTIONSDocument9 pagesChapter 2 Time Value of Money ANSWERS TO END OF CHAPTER QUESTIONSMariem JabberiNo ratings yet

- Sources of Short Term FinancingDocument74 pagesSources of Short Term FinancingKim TaengoossNo ratings yet

- AFCP810 Finance PrinciplesDocument3 pagesAFCP810 Finance PrinciplesbustitoutNo ratings yet

- 10 Short Term Bank Loans and Other S-T FinancingDocument33 pages10 Short Term Bank Loans and Other S-T FinancingMohammad DwidarNo ratings yet

- FIRE Case 1Document2 pagesFIRE Case 1prajwal jNo ratings yet

- Concept Questions: Compound Interest: Future Value and Present ValueDocument4 pagesConcept Questions: Compound Interest: Future Value and Present ValuelinhNo ratings yet

- DS Chapter 7 (p203-213) Mortgage ModificationDocument11 pagesDS Chapter 7 (p203-213) Mortgage ModificationsandeepdevathiNo ratings yet

- U2 BayeDocument9 pagesU2 Bayeishitasaini0852No ratings yet

- AsdDocument18 pagesAsdJenever Leo SerranoNo ratings yet

- Sample/practice Exam 15 November, Answers Sample/practice Exam 15 November, AnswersDocument9 pagesSample/practice Exam 15 November, Answers Sample/practice Exam 15 November, AnswersTuyết NhiNo ratings yet

- TUTORIALDocument10 pagesTUTORIALViễn QuyênNo ratings yet

- R06 The Time Value of Money Q BankDocument19 pagesR06 The Time Value of Money Q BankTeddy JainNo ratings yet

- FD Swap 2Document6 pagesFD Swap 2Gayu RkNo ratings yet

- HEHEHEHEDocument4 pagesHEHEHEHEJemelyn YapNo ratings yet

- 236224" de Meest Innovatieve Dingen Gebeuren Met Lening Duurzame Energie"Document2 pages236224" de Meest Innovatieve Dingen Gebeuren Met Lening Duurzame Energie"angelm2jrvNo ratings yet

- From Bad to Good Credit: A Practical Guide for Individuals with Charge-Offs and CollectionsFrom EverandFrom Bad to Good Credit: A Practical Guide for Individuals with Charge-Offs and CollectionsNo ratings yet

- Make Money Magazine #1 - Alex Forex Millionaire and Playboy!Document19 pagesMake Money Magazine #1 - Alex Forex Millionaire and Playboy!ForexAlex71% (7)

- FLIP (Q & A) - Updated 28Document6 pagesFLIP (Q & A) - Updated 28atul gawaliNo ratings yet

- PTBA Presentation 9M2015Document24 pagesPTBA Presentation 9M2015apurnomoNo ratings yet

- 3) Business Structure (D)Document10 pages3) Business Structure (D)CRAZYBLOBY 99No ratings yet

- Important Features of IAS 1 PDFDocument6 pagesImportant Features of IAS 1 PDFJayedNo ratings yet

- Inventory 2Document8 pagesInventory 2Nonso OsakweNo ratings yet

- TRM Report ViettinbankDocument22 pagesTRM Report ViettinbankNinh Thị Ánh NgọcNo ratings yet

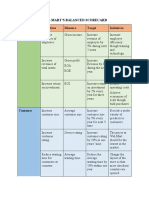

- Wal-Mart's Balanced ScorecardDocument3 pagesWal-Mart's Balanced ScorecardCấn Thu HuyềnNo ratings yet

- Role of Ecommerce in 21st CenturyDocument9 pagesRole of Ecommerce in 21st CenturychaturvediprateekNo ratings yet

- Nutresa Nov 3Document13 pagesNutresa Nov 3SemanaNo ratings yet

- Chapter 24 Finance, Saving, and InvestmentDocument32 pagesChapter 24 Finance, Saving, and InvestmentkimkimberlyNo ratings yet

- BNCM - JM L UhlnygkfDocument28 pagesBNCM - JM L UhlnygkfReckon IndepthNo ratings yet

- BJMPMBAI 2019 Annual ReportDocument24 pagesBJMPMBAI 2019 Annual ReportKrystal Claire Dioso MarimonNo ratings yet

- Reform of Retirement Benefits in Sindh, PakistanDocument19 pagesReform of Retirement Benefits in Sindh, PakistanAsian Development BankNo ratings yet

- ReportDocument22 pagesReportTrinh LyNo ratings yet

- Hi-Vogue's Business Proposal PDFDocument24 pagesHi-Vogue's Business Proposal PDFShahRukh KhalidNo ratings yet

- Capital Budgeting Decisions: DR R.S. Aurora, Faculty in FinanceDocument31 pagesCapital Budgeting Decisions: DR R.S. Aurora, Faculty in FinanceAmit KumarNo ratings yet

- Presentation On Institutional Investors Roadshow (Company Update)Document30 pagesPresentation On Institutional Investors Roadshow (Company Update)Shyam SunderNo ratings yet

- Eastspring Investments Dinasti Equity Fund Product HighlightsDocument8 pagesEastspring Investments Dinasti Equity Fund Product HighlightsGrab Hakim RazakNo ratings yet

- Midterm Exam Answer Sheet Course 8110Document8 pagesMidterm Exam Answer Sheet Course 8110kajalNo ratings yet

- The Encyclopedia Americana 1997Document78 pagesThe Encyclopedia Americana 1997Lichelle SeeNo ratings yet

- Q1) Define The Meaning of Agency Theory?Document8 pagesQ1) Define The Meaning of Agency Theory?vivek1119No ratings yet

- Garbles Cellular PhonesDocument32 pagesGarbles Cellular PhonesAbu AliNo ratings yet

- Chap 04 Answerkey Test Bank Answer KeyDocument59 pagesChap 04 Answerkey Test Bank Answer KeyQuỳnh Giao TôNo ratings yet

- Impact of Liberalization & Privatization On Indian EconomyDocument13 pagesImpact of Liberalization & Privatization On Indian EconomyNitesh SinghalNo ratings yet

- BPDocument26 pagesBPDeyeck VergaNo ratings yet

- Assess Macroeconomic Policies Which Might Be Used To Respond To Rising Commodity Prices During A Period of Slow Economic GrowthDocument2 pagesAssess Macroeconomic Policies Which Might Be Used To Respond To Rising Commodity Prices During A Period of Slow Economic GrowthJamie HaywoodNo ratings yet

- Hindustan Unilever: Brand ValuationDocument19 pagesHindustan Unilever: Brand ValuationSultan MahmudNo ratings yet