Download as pptx, pdf, or txt

You might also like

- Value Added Tax (Vat) .PPT FinalDocument57 pagesValue Added Tax (Vat) .PPT FinalNick254No ratings yet

- Anup Paul CaseDocument2 pagesAnup Paul CaseHimesh ChawlaNo ratings yet

- Advance Tax Vat II Jj2024Document40 pagesAdvance Tax Vat II Jj2024cnarinNo ratings yet

- Unit 6: Value Added Tax (Proclamation 285/2002 Regulation 79/2002 Proclamation 609/2008)Document23 pagesUnit 6: Value Added Tax (Proclamation 285/2002 Regulation 79/2002 Proclamation 609/2008)Bizu AtnafuNo ratings yet

- 30 - Dinh Phuc UyenDocument6 pages30 - Dinh Phuc UyenĐinh Phúc UyênNo ratings yet

- Value Added TaxDocument9 pagesValue Added TaxĴõ ĔĺNo ratings yet

- SlideshowDocument37 pagesSlideshowBhavesh AgrawalNo ratings yet

- Tax Base For VAT: Import StageDocument2 pagesTax Base For VAT: Import StageS. M. Saz Lul HoqueNo ratings yet

- Main Features of VATDocument3 pagesMain Features of VATSiva Subramanian100% (2)

- Accounting For Indirect TaxesDocument40 pagesAccounting For Indirect TaxesSabaa if100% (1)

- Draft VAT FAQDocument17 pagesDraft VAT FAQreazvat786No ratings yet

- Value Added Tax - VatDocument37 pagesValue Added Tax - VatTimoth MbwiloNo ratings yet

- TAXATION - Value-Added TaxDocument10 pagesTAXATION - Value-Added TaxJohn Mahatma Agripa100% (2)

- Chapter 3. Corporate Income TaxDocument90 pagesChapter 3. Corporate Income TaxVu Thi ThuongNo ratings yet

- Vat Lecture ThreeDocument28 pagesVat Lecture ThreeAbdulkarim Hamisi KufakunogaNo ratings yet

- Value Added Tax (VAT)Document37 pagesValue Added Tax (VAT)Minh Hương TrầnNo ratings yet

- Value Added TaxDocument22 pagesValue Added TaxJ-Lem CachoNo ratings yet

- 2015 VAT in Cambodia Sesion II 22aug 2015Document27 pages2015 VAT in Cambodia Sesion II 22aug 2015Sovanna HangNo ratings yet

- Tax Session I - VATDocument32 pagesTax Session I - VATbrightkeysNo ratings yet

- HANDOUT FOR VAT-NewDocument25 pagesHANDOUT FOR VAT-NewCristian RenatusNo ratings yet

- Value Added Tax ActDocument18 pagesValue Added Tax ActStephen Amobi OkoronkwoNo ratings yet

- Vat IiDocument19 pagesVat IiPCNo ratings yet

- Vat Vs GST FinalDocument35 pagesVat Vs GST FinalJatin GoyalNo ratings yet

- Lecture VAT With ExercisesDocument82 pagesLecture VAT With ExercisesAko C JamzNo ratings yet

- 8VATDocument70 pages8VATNoelNo ratings yet

- Exam Gaci 9 y 10Document3 pagesExam Gaci 9 y 10aledobernal2No ratings yet

- Vat 220424091227Document16 pagesVat 220424091227vishal.patel250897No ratings yet

- (Return To Index) : DescriptionDocument13 pages(Return To Index) : DescriptionTara ManteNo ratings yet

- Bir - VatDocument24 pagesBir - Vatalfx216No ratings yet

- VatDocument37 pagesVatBảo BờmNo ratings yet

- LU1 - Value-Added TaxDocument24 pagesLU1 - Value-Added Taxmandisanomzamo72No ratings yet

- Part Two Value Added Tax VATDocument54 pagesPart Two Value Added Tax VATSawsan HatemNo ratings yet

- Tax UpdatesDocument19 pagesTax UpdatesYeoh MaeNo ratings yet

- Notes On Vat On Importation Feb 09 2023Document2 pagesNotes On Vat On Importation Feb 09 2023barneyaguilar8732No ratings yet

- Description: BIR Form 2550M BIR Form No. 2307Document17 pagesDescription: BIR Form 2550M BIR Form No. 2307Montessa GuelasNo ratings yet

- VAT Presentation To The General PublicDocument27 pagesVAT Presentation To The General PublicJoette PennNo ratings yet

- Valu E-Adde D TaxDocument18 pagesValu E-Adde D TaxXavier Hawkins Lopez ZamoraNo ratings yet

- Value Added Tax in Romania VAT TVADocument6 pagesValue Added Tax in Romania VAT TVAmondlyNo ratings yet

- Lecturer. 8.. Income Tax Article .22Document5 pagesLecturer. 8.. Income Tax Article .22AlisyaNo ratings yet

- UP Nepal Tax FeeDocument7 pagesUP Nepal Tax FeeAnil ShahNo ratings yet

- Value-Added Tax: DescriptionDocument26 pagesValue-Added Tax: DescriptionGIGI BODONo ratings yet

- Value Added Tax-PDocument20 pagesValue Added Tax-PMa. Corazon CaramalesNo ratings yet

- Module 1 & 2: at The End of This Topic, We Should Be Able To Learn The FollowingDocument33 pagesModule 1 & 2: at The End of This Topic, We Should Be Able To Learn The FollowingAlicia FelicianoNo ratings yet

- VAT Taxpayer Guide (Input Tax)Document54 pagesVAT Taxpayer Guide (Input Tax)NstrNo ratings yet

- Tax 5Document88 pagesTax 5Thái Minh ChâuNo ratings yet

- Calculation of Total Tax IncidenceDocument10 pagesCalculation of Total Tax Incidencesajjad147No ratings yet

- Case: Cir V PLDTDocument29 pagesCase: Cir V PLDTJaymee Andomang Os-agNo ratings yet

- 1 Understanding VAT For BusinessesDocument6 pages1 Understanding VAT For BusinessesBensonNo ratings yet

- Tax Equation & Short EssayDocument4 pagesTax Equation & Short EssayReva BellaNo ratings yet

- Consumption TaxDocument7 pagesConsumption Taxanyonghasayu30No ratings yet

- VAT Questions For Professional Stage Knowledge LevelDocument14 pagesVAT Questions For Professional Stage Knowledge LevelFahimaAkterNo ratings yet

- VATDocument11 pagesVATSaurav KumarNo ratings yet

- Corporate Income TaxDocument14 pagesCorporate Income Tax36. Lê Minh Phương 12A3No ratings yet

- Tax 2Document89 pagesTax 2Thái Minh ChâuNo ratings yet

- Value Added TaxDocument19 pagesValue Added TaxRenalyn GardeNo ratings yet

- Corporate - Income - Tax (CIT) 2022Document44 pagesCorporate - Income - Tax (CIT) 2022Thảo Nhi Đinh TrầnNo ratings yet

- Taxation EthiopiaDocument10 pagesTaxation EthiopiahailemichalefNo ratings yet

- Uganda Incentive Regime 2006-07Document20 pagesUganda Incentive Regime 2006-07Katamba JosephNo ratings yet

- 96 2015 TT BTCDocument41 pages96 2015 TT BTCKhánh Vy VũNo ratings yet

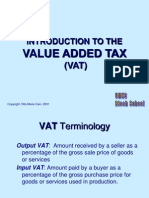

- Introduction To TheDocument11 pagesIntroduction To The9211420420No ratings yet

- MSDS Spectrum Underglaze 514Document2 pagesMSDS Spectrum Underglaze 514Anonymous EeTgKuNo ratings yet

- People v. Duca, October 9, 2009, G.R. No. 171175Document7 pagesPeople v. Duca, October 9, 2009, G.R. No. 171175brahmsNo ratings yet

- Authors' Manuscript Submission GuidelinesDocument3 pagesAuthors' Manuscript Submission GuidelinesAnamika ChoudharyNo ratings yet

- 6 Bromo Cresol GreenDocument7 pages6 Bromo Cresol GreenVincent KwofieNo ratings yet

- Common Problems in Practice and Procedure Before Registries of Deeds Incident To Subsequent RegistrationDocument11 pagesCommon Problems in Practice and Procedure Before Registries of Deeds Incident To Subsequent Registrationjuliepis_ewNo ratings yet

- What Man Cannot Not KnowDocument32 pagesWhat Man Cannot Not KnowDave100% (2)

- Report: Informal Dialogue Between CSO and ASEAN Secretary General, Between CSO and ASEAN CPR and The 1st Jakarta Human Rights Dialogue (JHRD) Final PDFDocument84 pagesReport: Informal Dialogue Between CSO and ASEAN Secretary General, Between CSO and ASEAN CPR and The 1st Jakarta Human Rights Dialogue (JHRD) Final PDFYuyun WahyuningrumNo ratings yet

- 8th February 2015Document1 page8th February 2015St Joseph's Parish, WarrnamboolNo ratings yet

- List of Registered ProjectsDocument214 pagesList of Registered ProjectsSunny SinghNo ratings yet

- STS Lesson 6Document34 pagesSTS Lesson 6Sharina Mhyca SamonteNo ratings yet

- Poly Medicure LTD.: Company Overview: DetailsDocument6 pagesPoly Medicure LTD.: Company Overview: DetailsRaghav BehaniNo ratings yet

- Virtues of TablighDocument26 pagesVirtues of TablighBooks for IslamNo ratings yet

- Commercial Dispatch Eedition 11-5-20Document12 pagesCommercial Dispatch Eedition 11-5-20The DispatchNo ratings yet

- Mathematics of Finance HandoutDocument10 pagesMathematics of Finance Handoutleandro2620010% (2)

- Answer Scheme TUTORIAL CHAPTER 4Document13 pagesAnswer Scheme TUTORIAL CHAPTER 4niklynNo ratings yet

- Notes On JudiciaryDocument3 pagesNotes On JudiciaryKhostwalNo ratings yet

- Unit 27 Issues in Factual ProgrammingDocument4 pagesUnit 27 Issues in Factual Programmingapi-268253755No ratings yet

- Maharashtra State PoliticsDocument2 pagesMaharashtra State Politicsvedanti shindeNo ratings yet

- LawsuitDocument2 pagesLawsuitasem adelNo ratings yet

- Notes For Semi Final Period 1Document27 pagesNotes For Semi Final Period 1arianne ayalaNo ratings yet

- Appalachia: High Intensity Drug Trafficking Area Drug Market AnalysisDocument12 pagesAppalachia: High Intensity Drug Trafficking Area Drug Market Analysislosangeles100% (3)

- EmkayDocument15 pagesEmkayCek IfaNo ratings yet

- AWS ArchitectureDocument24 pagesAWS Architecturefno investmentsNo ratings yet

- Once Upon A Greek Stage - SummaryDocument6 pagesOnce Upon A Greek Stage - SummaryRoshan P Nair88% (8)

- Ultrasonic Distance MeasurementDocument4 pagesUltrasonic Distance MeasurementDakhara PradipNo ratings yet

- RC186 Customer Letter en 1Document3 pagesRC186 Customer Letter en 1Thierry MoretNo ratings yet

- Spouses Toh Vs Solidbank. Surety. Is The Surety Discharge When The Bank Exended PaymentDocument2 pagesSpouses Toh Vs Solidbank. Surety. Is The Surety Discharge When The Bank Exended Paymenttimothymaderazo100% (1)

- Annual Report IndInfravit Trust 1Document183 pagesAnnual Report IndInfravit Trust 1Vikas VidhurNo ratings yet

- Firm of Pratapchand V. Firm of KotrikeDocument13 pagesFirm of Pratapchand V. Firm of Kotrikeatharva sanganeriaNo ratings yet