Download as ppt, pdf, or txt

You might also like

- Electrical - J1175 - Troubleshooting - v1 (Read-Only)Document42 pagesElectrical - J1175 - Troubleshooting - v1 (Read-Only)Simon C Mulgrew100% (7)

- Ultimate Guide To Debt & Leveraged Finance - Wall Street PrepDocument18 pagesUltimate Guide To Debt & Leveraged Finance - Wall Street PrepPearson SunigaNo ratings yet

- The Private Equity Analyst: Guide To The Secondary MarketDocument54 pagesThe Private Equity Analyst: Guide To The Secondary Marketscidmark123No ratings yet

- 1MRB520176 Ben RIO580Document20 pages1MRB520176 Ben RIO580alimaghamiNo ratings yet

- SubprimeDocument31 pagesSubprimeapi-3712367No ratings yet

- Sub Prime Overview For Samir 1 Final 97-2003 FormatDocument10 pagesSub Prime Overview For Samir 1 Final 97-2003 FormatAliasgar SuratwalaNo ratings yet

- Risk Management Failures During The Financial Crisis: November 2011Document27 pagesRisk Management Failures During The Financial Crisis: November 2011Khushi ShahNo ratings yet

- Subprime Crisis: Sandipan Nandi Shamik Roy Uttiya DasDocument61 pagesSubprime Crisis: Sandipan Nandi Shamik Roy Uttiya DasUttiya DasNo ratings yet

- Securitization CDO CDS Subprime CrisesDocument81 pagesSecuritization CDO CDS Subprime Crisesshwetata986No ratings yet

- Assignment No.2 Inside JobDocument6 pagesAssignment No.2 Inside JobJill SanghrajkaNo ratings yet

- SecuritizationDocument34 pagesSecuritizationsanil mehtaNo ratings yet

- Krassimir Petrov - Intto To Credit Default SwapsDocument13 pagesKrassimir Petrov - Intto To Credit Default SwapsAntonio Luis SantosNo ratings yet

- Submission Number: 1 Group Number: 34 Group Members: Non-Contributing Member (X)Document5 pagesSubmission Number: 1 Group Number: 34 Group Members: Non-Contributing Member (X)Darshna JhaNo ratings yet

- Finance Assignment 2: Financial Crisis of 2008: Housing Market in USADocument2 pagesFinance Assignment 2: Financial Crisis of 2008: Housing Market in USADipankar BasumataryNo ratings yet

- How Destruction Happened?: FICO Score S of Below 620. Because TheseDocument5 pagesHow Destruction Happened?: FICO Score S of Below 620. Because ThesePramod KhandelwalNo ratings yet

- ProjectDocument7 pagesProjectmalik waseemNo ratings yet

- Mortgage Credit CrisisDocument5 pagesMortgage Credit Crisisasfand yar waliNo ratings yet

- Crisis FinancieraDocument4 pagesCrisis Financierahawk91No ratings yet

- Financial Crises: Past, Present and Future: James J. Angel, PHD, Cfa Georgetown University Mcdonough School of BusinessDocument39 pagesFinancial Crises: Past, Present and Future: James J. Angel, PHD, Cfa Georgetown University Mcdonough School of BusinessnitikanNo ratings yet

- FRM Part 1 R7Document2 pagesFRM Part 1 R7Tony NasrNo ratings yet

- Assignment# 1: Name: Muhammad Ali Adil Malik REG #: SP16-BAF-015 Instructor: Dr. Sabeen KhanDocument5 pagesAssignment# 1: Name: Muhammad Ali Adil Malik REG #: SP16-BAF-015 Instructor: Dr. Sabeen KhanAli MalikNo ratings yet

- Sub-Prime Crisis and Its AftermathDocument24 pagesSub-Prime Crisis and Its AftermathasifanisNo ratings yet

- The Makng of A Bank FailureDocument5 pagesThe Makng of A Bank FailureFayçal SinaceurNo ratings yet

- Economics PresentationsDocument2 pagesEconomics PresentationsMunny Akter KhanNo ratings yet

- The Role of CDOs in Subprime CrisisDocument6 pagesThe Role of CDOs in Subprime CrisisKunal BhodiaNo ratings yet

- Sub PrimeDocument16 pagesSub PrimeDavneet KaurNo ratings yet

- The Great Recession: The burst of the property bubble and the excesses of speculationFrom EverandThe Great Recession: The burst of the property bubble and the excesses of speculationNo ratings yet

- SAMPLE Assignment Sub Prime Financial Crisis 2008Document4 pagesSAMPLE Assignment Sub Prime Financial Crisis 2008scholarsassistNo ratings yet

- Bruce Carruthers - Sociology of Bubbles (2009)Document5 pagesBruce Carruthers - Sociology of Bubbles (2009)NagelNo ratings yet

- 2008 Financial CrisisDocument34 pages2008 Financial CrisisJakeNo ratings yet

- Sub PrimeDocument7 pagesSub PrimeAtul SuranaNo ratings yet

- Bonds: (Pakistan) (00923013791119)Document31 pagesBonds: (Pakistan) (00923013791119)chelsea1989No ratings yet

- Notes On Basel IIIDocument11 pagesNotes On Basel IIIprat05No ratings yet

- Macro - Chapter 9Document9 pagesMacro - Chapter 9ljayoungNo ratings yet

- Financial Shock: by Mark Zandi, FT Press, 2009Document6 pagesFinancial Shock: by Mark Zandi, FT Press, 2009amitprakash1985No ratings yet

- Reason: Financial Crises in Advanced EconomiesDocument6 pagesReason: Financial Crises in Advanced EconomiesSorah YoriNo ratings yet

- Financial InstituitionsDocument2 pagesFinancial InstituitionsSidra NadeemNo ratings yet

- Different Types of DepositsDocument25 pagesDifferent Types of DepositsRAMALAKSHMI SUDALAIKANNANNo ratings yet

- DiamondDocument15 pagesDiamondMaxim FilippovNo ratings yet

- International Finance FinalDocument27 pagesInternational Finance FinalRishabh RaiNo ratings yet

- U. S. Loan Syndications: Chris Droussiotis Spring 2010Document37 pagesU. S. Loan Syndications: Chris Droussiotis Spring 2010Ash_ish_vNo ratings yet

- Depository Institutions: Activities and Characteristics: Instructor: Mahwish KhokharDocument36 pagesDepository Institutions: Activities and Characteristics: Instructor: Mahwish KhokharAbdur RehmanNo ratings yet

- Eco PresentationDocument2 pagesEco PresentationMunny Akter KhanNo ratings yet

- What Is A Subprime Mortgage?Document5 pagesWhat Is A Subprime Mortgage?Chigo RamosNo ratings yet

- Financial Crisis - Group 6Document8 pagesFinancial Crisis - Group 6Anonymous ZCvBMCO9No ratings yet

- Q: - "Why Is British Banking in Crisis?" Provide Reasons and Suggest Possible Solutions?Document6 pagesQ: - "Why Is British Banking in Crisis?" Provide Reasons and Suggest Possible Solutions?scorpio786No ratings yet

- Assignment No. 4 Roll No. L-1184 Financial Institution Topic: Bond Market, Stock Market and Mortgage Market Submitted To: Sir Abdul Qadeer Submitted By: Zainab Shabbir Dated: 21 June, 2020Document16 pagesAssignment No. 4 Roll No. L-1184 Financial Institution Topic: Bond Market, Stock Market and Mortgage Market Submitted To: Sir Abdul Qadeer Submitted By: Zainab Shabbir Dated: 21 June, 2020Faisal NaqviNo ratings yet

- What Is The Main Function of Financial Markets?: Tutorial 1 Overview of Financial System Part 1. Questions For ReviewDocument16 pagesWhat Is The Main Function of Financial Markets?: Tutorial 1 Overview of Financial System Part 1. Questions For ReviewViem AnhNo ratings yet

- Ch13: Commercial Bank Operations: Major Sources of Bank FundsDocument6 pagesCh13: Commercial Bank Operations: Major Sources of Bank FundsBruno U. YabutaNo ratings yet

- Financial Imst &mark Unit - 2Document57 pagesFinancial Imst &mark Unit - 2KalkayeNo ratings yet

- Tutorial 1 QuestionsDocument8 pagesTutorial 1 QuestionsHuế HoàngNo ratings yet

- PART 1: How We Got Here?Document5 pagesPART 1: How We Got Here?Abdul Wahab ShahidNo ratings yet

- Case BackgroundDocument7 pagesCase Backgroundabhilash191No ratings yet

- The Sub-Prime Mortgage Crisis & DerivativesDocument10 pagesThe Sub-Prime Mortgage Crisis & DerivativesChen XinNo ratings yet

- Master of Business Administration: Cover / Title PageDocument39 pagesMaster of Business Administration: Cover / Title PageDevi monishaNo ratings yet

- 01 07 08 NYC JMC UpdateDocument10 pages01 07 08 NYC JMC Updateapi-27426110No ratings yet

- History: Loans Market Interest Rates Credit History Primary MarketDocument8 pagesHistory: Loans Market Interest Rates Credit History Primary Marketkishorepatil8887No ratings yet

- MortgagepptDocument28 pagesMortgagepptJocelynNo ratings yet

- UssamaDocument12 pagesUssamaRizwan RizzuNo ratings yet

- FinTech Rising: Navigating the maze of US & EU regulationsFrom EverandFinTech Rising: Navigating the maze of US & EU regulationsRating: 5 out of 5 stars5/5 (1)

- Investing in Fixed Income Securities: Understanding the Bond MarketFrom EverandInvesting in Fixed Income Securities: Understanding the Bond MarketNo ratings yet

- WEight Training ScheduleDocument2 pagesWEight Training Scheduleapi-3712367100% (1)

- FFRChange HistoryDocument1 pageFFRChange Historyapi-3712367No ratings yet

- Anti-Inflationary Policy in IndiaDocument14 pagesAnti-Inflationary Policy in Indiaapi-3712367No ratings yet

- Policybrief Nov05Document6 pagesPolicybrief Nov05api-3712367No ratings yet

- Macroeconomics AssignmentsDocument15 pagesMacroeconomics Assignmentsapi-3712367No ratings yet

- Fema CDocument5 pagesFema Capi-3712367No ratings yet

- Foreign Exchange Management Policy in IndiaDocument6 pagesForeign Exchange Management Policy in Indiaapi-371236767% (3)

- Report OnDocument9 pagesReport Onapi-3712367No ratings yet

- Subprime Toxic Debt - Bloomberg July07Document10 pagesSubprime Toxic Debt - Bloomberg July07api-3712367No ratings yet

- SubprimeDocument31 pagesSubprimeapi-3712367No ratings yet

- SubPrime Mortgage MarketDocument6 pagesSubPrime Mortgage Marketapi-3712367No ratings yet

- BSC & Knowledge ManagementDocument3 pagesBSC & Knowledge Managementapi-3712367100% (1)

- Sebi TocDocument33 pagesSebi Tocapi-3712367No ratings yet

- Global Economics - IndiaDocument2 pagesGlobal Economics - Indiaapi-3712367No ratings yet

- Balanced ScorecardDocument13 pagesBalanced Scorecardapi-3712367No ratings yet

- Amortization Calculator - Wikipedia, The Free EncyclopediaDocument3 pagesAmortization Calculator - Wikipedia, The Free Encyclopediaapi-3712367No ratings yet

- Balanced ScorecardDocument67 pagesBalanced Scorecardapi-3712367100% (4)

- MacroEconomics - Lecture 4 SKM MultiplierDocument7 pagesMacroEconomics - Lecture 4 SKM Multiplierapi-3712367No ratings yet

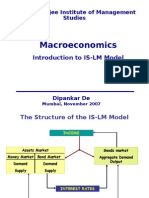

- MacroEconomics - Lecture 5 Introduction To ISLMDocument21 pagesMacroEconomics - Lecture 5 Introduction To ISLMapi-3712367100% (1)

- Micro Economics PresentationDocument18 pagesMicro Economics Presentationapi-3712367No ratings yet

- Smart Monitoring of Food SpoilageDocument31 pagesSmart Monitoring of Food Spoilagehimani dewanganNo ratings yet

- Product Classification: SL110 Series Modular Jack, RJ45, Category 6, T568A/T568B, Unshielded, Without Dust Cover, BlackDocument2 pagesProduct Classification: SL110 Series Modular Jack, RJ45, Category 6, T568A/T568B, Unshielded, Without Dust Cover, BlackDWVIZCARRANo ratings yet

- Guidelines - In-Hospital ResuscitationDocument18 pagesGuidelines - In-Hospital ResuscitationparuNo ratings yet

- Ruwanpura Expressway Design ProjectDocument5 pagesRuwanpura Expressway Design ProjectMuhammadh MANo ratings yet

- The 2020 Lithium-Ion Battery Guide - The Easy DIY Guide To Building Your Own Battery Packs (Lithium Ion Battery Book Book 1)Document101 pagesThe 2020 Lithium-Ion Battery Guide - The Easy DIY Guide To Building Your Own Battery Packs (Lithium Ion Battery Book Book 1)Hangar Graus75% (4)

- Presentation of A Golden FIBC Made From PET Bottle Flakes enDocument2 pagesPresentation of A Golden FIBC Made From PET Bottle Flakes enMILADNo ratings yet

- Kirch GroupDocument13 pagesKirch GroupStacy ChackoNo ratings yet

- Carbon Dioxide Portable Storage UnitsDocument2 pagesCarbon Dioxide Portable Storage UnitsDiego AnayaNo ratings yet

- BP 2009 Metro Availability PDFDocument66 pagesBP 2009 Metro Availability PDFEduardo LoureiroNo ratings yet

- Study On Vehicle Loan Disbursement ProceDocument11 pagesStudy On Vehicle Loan Disbursement ProceRuby PrajapatiNo ratings yet

- Basement and Retaining WallsDocument42 pagesBasement and Retaining WallsSamata Mahajan0% (1)

- Decision Utah LighthouseDocument28 pagesDecision Utah LighthousemschwimmerNo ratings yet

- UMAM Fee Structure EditedVer2Document1 pageUMAM Fee Structure EditedVer2AKMA SAUPINo ratings yet

- Code of Practice For Power System ProtectionDocument3 pagesCode of Practice For Power System ProtectionVinit JhingronNo ratings yet

- Biobase GoupDocument11 pagesBiobase Goupfrancheska bacaNo ratings yet

- Homeland Security Thesis StatementDocument8 pagesHomeland Security Thesis Statementdwtcn1jq100% (2)

- Funda ExamDocument115 pagesFunda ExamKate Onniel RimandoNo ratings yet

- A Framework For Improving Advertising Creative Using Digital MeasurementDocument15 pagesA Framework For Improving Advertising Creative Using Digital MeasurementMs Mariia MykhailenkoNo ratings yet

- Ace3 Unit8 TestDocument3 pagesAce3 Unit8 Testnatacha100% (3)

- PM - Equipment Task ListDocument26 pagesPM - Equipment Task Listsiva prasadNo ratings yet

- Investment Property - DQDocument3 pagesInvestment Property - DQKryztal TalaveraNo ratings yet

- 3 If D⋅∇=∈∇.Eand∇.J = σ∇.Ein a given material, the material is said to beDocument3 pages3 If D⋅∇=∈∇.Eand∇.J = σ∇.Ein a given material, the material is said to besai kumar vemparalaNo ratings yet

- Digital Electronics MCQDocument10 pagesDigital Electronics MCQDr.D.PradeepkannanNo ratings yet

- FreemanWhite Hybrid Operating Room Design GuideDocument11 pagesFreemanWhite Hybrid Operating Room Design GuideFaisal KhanNo ratings yet

- D D D D D D D D D: DescriptionDocument34 pagesD D D D D D D D D: DescriptionSukandar TeaNo ratings yet

- Pemanfaatan Media Sosial Dan Ecommerce Sebagai Media Pemasaran Dalam Mendukung Peluang Usaha Mandiri Pada Masa Pandemi Covid 19Document12 pagesPemanfaatan Media Sosial Dan Ecommerce Sebagai Media Pemasaran Dalam Mendukung Peluang Usaha Mandiri Pada Masa Pandemi Covid 19Min HwagiNo ratings yet

- Indian Bank Vs Maharashtra State Cooperative Marke0827s980450COM441873Document4 pagesIndian Bank Vs Maharashtra State Cooperative Marke0827s980450COM441873Bhuvneshwari RathoreNo ratings yet

- Iac Advanced Financial Accounting and ReDocument4 pagesIac Advanced Financial Accounting and ReIshi AbainzaNo ratings yet