Download as pptx, pdf, or txt

You might also like

- Full Solution Manual Accounting 8th Edition by John Hoggett SLW1014Document68 pagesFull Solution Manual Accounting 8th Edition by John Hoggett SLW1014Sm Help80% (5)

- Chapter 2 The Accounting Equation and The Double-Entry SystemDocument24 pagesChapter 2 The Accounting Equation and The Double-Entry SystemMarriel Fate Cullano0% (1)

- 2021 August StatementDocument7 pages2021 August StatementJawad AhmedNo ratings yet

- Svo PP 2016 PDFDocument344 pagesSvo PP 2016 PDFkcchan7No ratings yet

- Replacement TheoryDocument27 pagesReplacement TheorymanishasainNo ratings yet

- ACT201 Chap001 NBNDocument18 pagesACT201 Chap001 NBNAudity PaulNo ratings yet

- Accounting..... All Questions & Answer.Document13 pagesAccounting..... All Questions & Answer.MehediNo ratings yet

- Part Two: Financial Accounting: An IntroductionDocument139 pagesPart Two: Financial Accounting: An IntroductionRobel Habtamu100% (1)

- Accounting For Business: Asso. Prof. Dr. Nguyen Thi Phuong HoaDocument37 pagesAccounting For Business: Asso. Prof. Dr. Nguyen Thi Phuong HoaTam DoNo ratings yet

- Session 1 - Introduction To Accounting and Balance SheetDocument32 pagesSession 1 - Introduction To Accounting and Balance Sheethieucaiminh155No ratings yet

- Acctg 101 SG 5Document4 pagesAcctg 101 SG 5justinnamoro8No ratings yet

- Far QeDocument55 pagesFar QeMaica A.No ratings yet

- Balance SheetDocument28 pagesBalance SheetrimaNo ratings yet

- Power Point Presentation 2Document39 pagesPower Point Presentation 2268gunnaNo ratings yet

- Final SummaryDocument6 pagesFinal SummaryAkanksha singhNo ratings yet

- CFAB Accounting Chap02 Accounting EquationDocument38 pagesCFAB Accounting Chap02 Accounting EquationHoa NguyễnNo ratings yet

- Week 3-4 Financial Statements - TopicDocument5 pagesWeek 3-4 Financial Statements - TopicApril Raylin RodeoNo ratings yet

- NIOS Class 12 ACC Most Important QuestionDocument8 pagesNIOS Class 12 ACC Most Important QuestionKaushil SolankiNo ratings yet

- Accounting in ActionDocument42 pagesAccounting in ActionMuhammad TausiqueNo ratings yet

- 01 Accounting StatementsDocument4 pages01 Accounting StatementsTijana DoberšekNo ratings yet

- Fundamentals of Accounting, Business and Management 2: Quarter 1-Module 1: Statement of Financial Position (SFP)Document20 pagesFundamentals of Accounting, Business and Management 2: Quarter 1-Module 1: Statement of Financial Position (SFP)Arvin Salazar Llaneta100% (1)

- Lesson 3: Accounting EquationDocument3 pagesLesson 3: Accounting EquationDante SausaNo ratings yet

- Chapters 1 and 2Document36 pagesChapters 1 and 2Qing ShiNo ratings yet

- AD1101 AY15 - 16 Sem 1 Lecture 1Document21 pagesAD1101 AY15 - 16 Sem 1 Lecture 1weeeeeshNo ratings yet

- Accounting C2 Lesson 1 PDFDocument5 pagesAccounting C2 Lesson 1 PDFJake ShimNo ratings yet

- LAS ABM - FABM12 Ia B 1 Week 1Document9 pagesLAS ABM - FABM12 Ia B 1 Week 1ROMMEL RABONo ratings yet

- 2Q - Fabm 2Document7 pages2Q - Fabm 2Alexandra Norin RodriguezNo ratings yet

- Finance & Investment Appraisal - v2Document28 pagesFinance & Investment Appraisal - v2nurhasanarko1No ratings yet

- Basic Accounting-Made EasyDocument20 pagesBasic Accounting-Made EasyRoy Kenneth Lingat100% (1)

- Lesson 2Document7 pagesLesson 2AdrianIlaganNo ratings yet

- 1accounting Equation RevisedDocument4 pages1accounting Equation RevisedReniel MillarNo ratings yet

- MBA Pre-Term - Ch4 - ISDocument58 pagesMBA Pre-Term - Ch4 - ISJoe YunNo ratings yet

- Topic 2 The Statement of Financial PositionDocument38 pagesTopic 2 The Statement of Financial PositionTanmay Sharma100% (1)

- Financial Instruments FINALDocument40 pagesFinancial Instruments FINALShaina DwightNo ratings yet

- Financial ReportsDocument36 pagesFinancial ReportsbehanzinlufrancheNo ratings yet

- 3 The Accounting EquationDocument26 pages3 The Accounting EquationJohn Alfred CastinoNo ratings yet

- Financial Statement AnalysisDocument31 pagesFinancial Statement AnalysisAbinash MishraNo ratings yet

- 2 Financial Statements ArticulationDocument31 pages2 Financial Statements Articulationchirag100% (1)

- Unit 2 MADocument28 pagesUnit 2 MATheresa BrownNo ratings yet

- Financial Management - ResumosDocument10 pagesFinancial Management - ResumosBeatriz BastosNo ratings yet

- Supplementary 1 - Financial StatementsDocument21 pagesSupplementary 1 - Financial StatementsQuốc Khánh100% (1)

- SAS#4-ACC104 With AnswerDocument5 pagesSAS#4-ACC104 With AnswerartificerrrrNo ratings yet

- Understanding Balance SheetsDocument26 pagesUnderstanding Balance SheetsAli AhmedNo ratings yet

- Group Reporting II: Application of The Acquisition Method Under IFRS 3Document77 pagesGroup Reporting II: Application of The Acquisition Method Under IFRS 3فهد التويجريNo ratings yet

- Topic 3 - Accounting Classification and Accounting Equation LatestDocument28 pagesTopic 3 - Accounting Classification and Accounting Equation LatestKhairul AkmalNo ratings yet

- Finance+Webinar 13.12.2022++updatedDocument42 pagesFinance+Webinar 13.12.2022++updatedJasmine ChoudharyNo ratings yet

- FABM2Document32 pagesFABM2Ylena AllejeNo ratings yet

- Investing and Financing Decisions and The Balance SheetDocument35 pagesInvesting and Financing Decisions and The Balance Sheetfmj6687No ratings yet

- 1st Quarter DiscussionDocument10 pages1st Quarter DiscussionCHARVIE KYLE RAMIREZNo ratings yet

- Basic Accounting Concepts and Principles Readings - 182930250Document6 pagesBasic Accounting Concepts and Principles Readings - 182930250braveweb136No ratings yet

- Iam Notes - I - StudentsDocument16 pagesIam Notes - I - StudentsNic BrownNo ratings yet

- Chapter 1 Introduction To FSADocument11 pagesChapter 1 Introduction To FSALuu Nhat MinhNo ratings yet

- Chapter 3 Cash Flows and Financial AnalysisDocument6 pagesChapter 3 Cash Flows and Financial AnalysisHannah Pauleen G. LabasaNo ratings yet

- Wey AP 8e Ch01 RevisedDocument25 pagesWey AP 8e Ch01 RevisedRahat Morshed NabilNo ratings yet

- Accounting 0452 Revision Notes For The y PDFDocument48 pagesAccounting 0452 Revision Notes For The y PDFSiddarthNo ratings yet

- Simplified Notes Unit 1 and 2Document4 pagesSimplified Notes Unit 1 and 2John Paul Gaylan100% (1)

- ACCOUNTANCY (Code No. 055) : RationaleDocument10 pagesACCOUNTANCY (Code No. 055) : RationaleAshish GangwalNo ratings yet

- FMA NotesDocument19 pagesFMA NotesLAXIANo ratings yet

- Review On Basic AccountingDocument19 pagesReview On Basic AccountingRegina BengadoNo ratings yet

- Accounting Concepts and Priciples: Fundamentals of Accountancy, Business and Management 1Document10 pagesAccounting Concepts and Priciples: Fundamentals of Accountancy, Business and Management 1Marilyn Nelmida TamayoNo ratings yet

- Chap 1 PowerpointDocument31 pagesChap 1 PowerpointKalkayeNo ratings yet

- Energy Efficient Manet ProtocplsDocument7 pagesEnergy Efficient Manet ProtocplsSuhas KapseNo ratings yet

- 1 Jurnal KosongDocument15 pages1 Jurnal KosongFadila HasifaNo ratings yet

- Working Capital Management 1Document48 pagesWorking Capital Management 1Nayan MaldeNo ratings yet

- 12th Accountancy EM Important Questions English Medium PDF DownloadDocument4 pages12th Accountancy EM Important Questions English Medium PDF Downloadqueensmiling495No ratings yet

- Bognot V RRI Lending CorpDocument2 pagesBognot V RRI Lending CorpRoy Angelo NepomucenoNo ratings yet

- PM Mock1Document40 pagesPM Mock1anuNo ratings yet

- MR Sivapragasam Sri Skanda 4 Farm Road Sutton Surrey Sm2 5huDocument2 pagesMR Sivapragasam Sri Skanda 4 Farm Road Sutton Surrey Sm2 5huSriskanda SivapragasamNo ratings yet

- KMA Sacco Loan Application FormDocument4 pagesKMA Sacco Loan Application FormDr. philemon mwongeraNo ratings yet

- Tax Ch02Document10 pagesTax Ch02GabriellaNo ratings yet

- Chapter 4 (Compatibility Mode)Document26 pagesChapter 4 (Compatibility Mode)AndualemEndrisNo ratings yet

- Fee Info Template EuroDocument13 pagesFee Info Template EuroMIRO GroupNo ratings yet

- Analysis Horizontal - SFPDocument18 pagesAnalysis Horizontal - SFPAnnalyn SamaniegoNo ratings yet

- Exposure To Currency Risk, Definition and MeasurementDocument12 pagesExposure To Currency Risk, Definition and MeasurementGustavo Adolfo Leyva LópezNo ratings yet

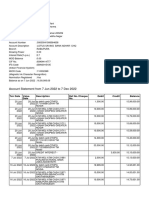

- Account Statement From 7 Jun 2022 To 7 Dec 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument3 pagesAccount Statement From 7 Jun 2022 To 7 Dec 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRdb TalkNo ratings yet

- Breakout On Gold Future (GC) or Gold Spot (XAUUSD) : Trading Risk DisclosureDocument2 pagesBreakout On Gold Future (GC) or Gold Spot (XAUUSD) : Trading Risk Disclosurehenry prabowoNo ratings yet

- Sample Cir BSPDocument1 pageSample Cir BSPAngelo SandovalNo ratings yet

- Karnataka II PUC Accountancy Sample Question Paper 18Document6 pagesKarnataka II PUC Accountancy Sample Question Paper 18Kishu KishoreNo ratings yet

- A Turnaround Story: Group 8: Yash, Ritu, Bhartesh, Smriti, Rahul, Piyush & JastejDocument17 pagesA Turnaround Story: Group 8: Yash, Ritu, Bhartesh, Smriti, Rahul, Piyush & JastejPratyush BaruaNo ratings yet

- Module 6 Is - LM ModelDocument50 pagesModule 6 Is - LM ModelHetvi JasaniNo ratings yet

- Business Research MethodDocument6 pagesBusiness Research MethodMehwish SiddiquiNo ratings yet

- Capital Budgeting and Cost AnalysisDocument26 pagesCapital Budgeting and Cost Analysissiti fatimatuzzahraNo ratings yet

- Credit Collection Module 2Document9 pagesCredit Collection Module 2Crystal Jade Apolinario RefilNo ratings yet

- 3.vol 01 Issue 05 Lenin Kumar Cluster Analysis of Mutual FundsDocument24 pages3.vol 01 Issue 05 Lenin Kumar Cluster Analysis of Mutual FundsRaaj SinghNo ratings yet

- Swot Analysis of MCBDocument4 pagesSwot Analysis of MCBAbdulMoeedMalik100% (1)

- The Legend of Situ BagenditDocument3 pagesThe Legend of Situ BagenditVisby NNo ratings yet

- Highlights of Proposed Ability-To-Repay RulesDocument3 pagesHighlights of Proposed Ability-To-Repay RulesForeclosure FraudNo ratings yet

- Investment SettingDocument34 pagesInvestment SettingRafia NaveedNo ratings yet