Download as pptx, pdf, or txt

You might also like

- ACCA Financial Management Dec Mock - Questions PDFDocument18 pagesACCA Financial Management Dec Mock - Questions PDFAmilah Fadhlin100% (1)

- Story Telling Script Robin HoodDocument2 pagesStory Telling Script Robin HoodEdwin Gumay100% (2)

- Criminal Law - Arts 1-20Document73 pagesCriminal Law - Arts 1-20KrisLarr100% (5)

- Production ForecastDocument210 pagesProduction ForecastLuciano FucelloNo ratings yet

- Table 210-06101Document28 pagesTable 210-06101Benito Santana RiosNo ratings yet

- Biostats ReviewerDocument8 pagesBiostats ReviewerDIVINA DAILISANNo ratings yet

- Chapter 5 - Forecasting Chapter 5 BEDocument26 pagesChapter 5 - Forecasting Chapter 5 BEFadhila Nurfida HanifNo ratings yet

- ACCA F9 Financial Management Mock Exam Questions 2017Document20 pagesACCA F9 Financial Management Mock Exam Questions 2017Vaishali BhargavNo ratings yet

- M12 - Set 4Document86 pagesM12 - Set 4Coffeebean LittleNo ratings yet

- QuanticoDocument6 pagesQuantico19EBKCS082 PIYUSHLATTANo ratings yet

- Selected Macroeconomic Indicatorsfor MPCDec 2008Document1 pageSelected Macroeconomic Indicatorsfor MPCDec 2008dl09vcNo ratings yet

- Q (X) e DT Q (X) : Complementary Error FunctionDocument2 pagesQ (X) e DT Q (X) : Complementary Error FunctionMohamed DakheelNo ratings yet

- Tabel Student TDocument3 pagesTabel Student TLhEiya RochmaNo ratings yet

- MA Mock - Questions S20-A21Document15 pagesMA Mock - Questions S20-A21Abdinasir HassanNo ratings yet

- Faculty of Science FRM 9649: Time Series Analysis & ForecastingDocument5 pagesFaculty of Science FRM 9649: Time Series Analysis & ForecastingHafeni tulongeni HamukotoNo ratings yet

- BlanchingDocument22 pagesBlanchingAdrianna MichelleNo ratings yet

- F9 - BPP - MOCK EXAM - QnsDocument10 pagesF9 - BPP - MOCK EXAM - QnsRaluca PanaitNo ratings yet

- Texas Roadhouse Published DataDocument2 pagesTexas Roadhouse Published DataKnagarNo ratings yet

- Nissin Corporation (A) PerciDocument44 pagesNissin Corporation (A) PerciScribdTranslationsNo ratings yet

- T-Distribution TableDocument1 pageT-Distribution Tablemaolin.zahrianiNo ratings yet

- US Corporate Bond Issuance: All Data Are Subject To RevisionDocument5 pagesUS Corporate Bond Issuance: All Data Are Subject To RevisionÂn TrầnNo ratings yet

- Table 248: Wholesale Price Index (Monthly Average) - ANNUAL VARIATIONDocument6 pagesTable 248: Wholesale Price Index (Monthly Average) - ANNUAL VARIATIONmaratageriNo ratings yet

- Critical ValueDocument12 pagesCritical ValueZAIRUL AMIN BIN RABIDIN (FRIM)No ratings yet

- Value Guide April 2011Document63 pagesValue Guide April 2011Siddharth KumarNo ratings yet

- TABLA T STUDENTDocument1 pageTABLA T STUDENTDaniel López100% (1)

- Metric Thread - Extended Thread Size Range PDFDocument20 pagesMetric Thread - Extended Thread Size Range PDFDu Shan100% (2)

- Annuities K. RaghunandanDocument18 pagesAnnuities K. RaghunandanShubhankar ShuklaNo ratings yet

- Height and Weight Conversion Charts No BMIDocument2 pagesHeight and Weight Conversion Charts No BMIdaenbiNo ratings yet

- C&W U.S. Lodging Overview 2017Document18 pagesC&W U.S. Lodging Overview 2017crticoticoNo ratings yet

- Intrinsic Viscosity Table PDFDocument3 pagesIntrinsic Viscosity Table PDFYunistya Dwi Cahyani100% (1)

- Time Value Money TableDocument5 pagesTime Value Money TableHien NguyenNo ratings yet

- Atb - Uv6154 XLS Eng 1Document5 pagesAtb - Uv6154 XLS Eng 1DevNo ratings yet

- Chương 3 - Financial ModelingDocument6 pagesChương 3 - Financial ModelingHUONG NGUYEN THINo ratings yet

- F3 Tables and FormulasDocument12 pagesF3 Tables and FormulastutorbritzNo ratings yet

- Financial Management Tables - PV & FVDocument4 pagesFinancial Management Tables - PV & FVsamantha119No ratings yet

- April Bullet InogureyDocument14 pagesApril Bullet InogureySoumiyaraj MahesanNo ratings yet

- SL Annual Stat Report-2011Document2 pagesSL Annual Stat Report-2011Wind RsNo ratings yet

- BYU Stat 121 Statistical TablesDocument1 pageBYU Stat 121 Statistical TablesGreg KnappNo ratings yet

- Tugas Besar PBA PerhitunganDocument145 pagesTugas Besar PBA Perhitungansyamsul anwarNo ratings yet

- Tugas Besar Perhitungan Curah HujanDocument59 pagesTugas Besar Perhitungan Curah Hujansyamsul anwar100% (1)

- Azhaan Day1Document31 pagesAzhaan Day1Azhaan AkhtarNo ratings yet

- Metric Thread - Extended Thread Size RangeDocument20 pagesMetric Thread - Extended Thread Size Rangerickscribd33100% (1)

- Metric Thread - Extended Thread Size RangeDocument19 pagesMetric Thread - Extended Thread Size RangeNatashaAggarwalNo ratings yet

- BLS Job Statistics Nonfarm Employment Jan 2001 To Aug 2010Document53 pagesBLS Job Statistics Nonfarm Employment Jan 2001 To Aug 2010liberalbillNo ratings yet

- Distribusi Nilai Durbin WatsonDocument1 pageDistribusi Nilai Durbin WatsonRIDWAN TORONo ratings yet

- OECD DataDocument9 pagesOECD DataArturitoNo ratings yet

- Tablas EstadisticasDocument5 pagesTablas EstadisticasCsar Calla MendozaNo ratings yet

- Databases: Consumer Price Index - Average Price DataDocument2 pagesDatabases: Consumer Price Index - Average Price Dataapi-18816456No ratings yet

- Macroeconomía País Hungría Practica 4Document33 pagesMacroeconomía País Hungría Practica 4magdalenoNo ratings yet

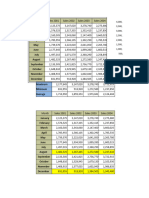

- Expense Trends Title: Ns e 1 Xpe Ns e 2 Xpe Ns e 3 Xpe Ns e 4 Xpe Ns e 5Document3 pagesExpense Trends Title: Ns e 1 Xpe Ns e 2 Xpe Ns e 3 Xpe Ns e 4 Xpe Ns e 5Ranjith KaruturiNo ratings yet

- V.9. Posisi Cadangan Devisa (Juta USD)Document2 pagesV.9. Posisi Cadangan Devisa (Juta USD)Izzuddin AbdurrahmanNo ratings yet

- AFM Class Notes PDFDocument154 pagesAFM Class Notes PDFSiddharth NarayananNo ratings yet

- TABLOLARDocument5 pagesTABLOLARordeklerimNo ratings yet

- Split 20240228 0105Document2 pagesSplit 20240228 0105Rip IhtishamNo ratings yet

- Critical values of Student's t distribution with ν degrees of freedomDocument11 pagesCritical values of Student's t distribution with ν degrees of freedomveronica lodgeNo ratings yet

- Statistical Constants FileDocument12 pagesStatistical Constants FileAnandhi ChidambaramNo ratings yet

- ACCA F9 - Financia Management - LSBF Class Notes 2011 (Free)Document185 pagesACCA F9 - Financia Management - LSBF Class Notes 2011 (Free)Rahib Jaskani100% (1)

- 2021-2024 (4 Year) Planner (Printable Version)From Everand2021-2024 (4 Year) Planner (Printable Version)Rating: 5 out of 5 stars5/5 (1)

- Profitability of simple fixed strategies in sport betting: NHL, 2009-2019From EverandProfitability of simple fixed strategies in sport betting: NHL, 2009-2019No ratings yet

- Profitability of simple fixed strategies in sport betting: Soccer, Belgium Jupiter League, 2009-2019From EverandProfitability of simple fixed strategies in sport betting: Soccer, Belgium Jupiter League, 2009-2019No ratings yet

- Doris Chase DoaneDocument16 pagesDoris Chase DoaneTTamara2950% (2)

- Managing Markets Strategically: Professor Noel CaponDocument53 pagesManaging Markets Strategically: Professor Noel CaponMoidin AfsanNo ratings yet

- INDIVIDUALSDocument6 pagesINDIVIDUALSAnne KimNo ratings yet

- PLD 1990 SC 28Document8 pagesPLD 1990 SC 28Ali HussainNo ratings yet

- The Disaster Crunch Model: Guidelines For A Gendered ApproachDocument16 pagesThe Disaster Crunch Model: Guidelines For A Gendered ApproachOxfamNo ratings yet

- Clubbing Sign and CyanosisDocument26 pagesClubbing Sign and CyanosisKhushboo IkramNo ratings yet

- Chapter 5 SolutionDocument7 pagesChapter 5 SolutionAli M AntthoNo ratings yet

- (PC) Porras v. Woodward - Document No. 3Document2 pages(PC) Porras v. Woodward - Document No. 3Justia.comNo ratings yet

- International Marketing Chapter 6Document3 pagesInternational Marketing Chapter 6Abviel Yumul50% (2)

- Allergic Bronchopulmonary Aspergillosis Clinical Care Guidelines - CF FoundationDocument8 pagesAllergic Bronchopulmonary Aspergillosis Clinical Care Guidelines - CF FoundationOxana TurcuNo ratings yet

- Federico Kauffmann Doig - The Chachapoyas CultureDocument320 pagesFederico Kauffmann Doig - The Chachapoyas CultureChachapoyaNo ratings yet

- (Extended) Roll Me A Deity - by Assassin NPCDocument35 pages(Extended) Roll Me A Deity - by Assassin NPCRunic PinesNo ratings yet

- ADE 420 Spring 2015 Assignment #1 GuidelinesDocument2 pagesADE 420 Spring 2015 Assignment #1 Guidelinesapi-20975547No ratings yet

- Lecture Notes: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument5 pagesLecture Notes: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDenny June CraususNo ratings yet

- What Is Financial Forecasting?: Basis For Comparison Forecasting PlanningDocument7 pagesWhat Is Financial Forecasting?: Basis For Comparison Forecasting PlanningB112NITESH KUMAR SAHUNo ratings yet

- Part-II Poem Article and Report For College Magazine-2015-16 Dr.M.Q. KhanDocument4 pagesPart-II Poem Article and Report For College Magazine-2015-16 Dr.M.Q. KhanTechi Son taraNo ratings yet

- 5c928989ac4f9 TSICanadaManualS PDFDocument144 pages5c928989ac4f9 TSICanadaManualS PDFAnggi SujiwoNo ratings yet

- F (X) X F: Second Quarter Examination in Mathematics Grade 10Document5 pagesF (X) X F: Second Quarter Examination in Mathematics Grade 10Aiza Abd0% (1)

- Rmullinsresume 2019Document2 pagesRmullinsresume 2019api-448247344No ratings yet

- Eastern Shipping LinesDocument3 pagesEastern Shipping LinessophiaNo ratings yet

- Sociology As A Branch of KnowledgeDocument19 pagesSociology As A Branch of KnowledgeRaju AhmmedNo ratings yet

- Job Description For Hse AdvisorDocument2 pagesJob Description For Hse AdvisorSam JoseNo ratings yet

- Assignment On Allegories in Fairie QueeneDocument5 pagesAssignment On Allegories in Fairie QueeneAltaf Sheikh100% (1)

- Angle Sum Property of A QuadrilateralDocument3 pagesAngle Sum Property of A Quadrilateralapi-174391216No ratings yet

- Collins - Expertise 2Document3 pagesCollins - Expertise 2Fernando SilvaNo ratings yet

- Welfare of Subjects, Experimenters and EnvironmentDocument15 pagesWelfare of Subjects, Experimenters and EnvironmentPaul BryanNo ratings yet

- Arthanaya Capital - WriteupDocument1 pageArthanaya Capital - WriteupAryan GargNo ratings yet

- SM CDR InterfaceDocument13 pagesSM CDR InterfaceLakshmi NarayanaNo ratings yet