Download as ppt, pdf, or txt

You might also like

- Original PDF Criminal Procedure From First Contact To Appeal 6th EditionDocument62 pagesOriginal PDF Criminal Procedure From First Contact To Appeal 6th Editionbetty.barabas349100% (50)

- In Class ProblemsDocument5 pagesIn Class Problemsishu0% (1)

- Midwest Ice Cream CompanyDocument13 pagesMidwest Ice Cream CompanyArijit Das0% (1)

- AcknowledgementDocument1 pageAcknowledgementapi-382116079% (19)

- Colorscope 1Document6 pagesColorscope 1Andrew NeuberNo ratings yet

- The Wind Egg. Haseeb AhmedDocument211 pagesThe Wind Egg. Haseeb Ahmedhwace40No ratings yet

- Speedking-World Versi Bhsa EnglishDocument10 pagesSpeedking-World Versi Bhsa EnglishBobby KurniawanNo ratings yet

- Class Activities (Chapter 6-Financial Modeling)Document18 pagesClass Activities (Chapter 6-Financial Modeling)JOHN MITCHELL GALLARDONo ratings yet

- Chapter 4. Mini Case: SituationDocument8 pagesChapter 4. Mini Case: SituationCool MomNo ratings yet

- Act Grupal 102003 9Document16 pagesAct Grupal 102003 9davidNo ratings yet

- Casino MathDocument43 pagesCasino MathferroalNo ratings yet

- Mafia Wars Expense Guide - Properties SheetDocument8 pagesMafia Wars Expense Guide - Properties SheetZababa100% (1)

- Marketing Directions December Edition 2016 PDFDocument10 pagesMarketing Directions December Edition 2016 PDFAseem SinghalNo ratings yet

- Regent CoinDocument38 pagesRegent Coindhananjay chaudharyNo ratings yet

- Airline Management AnalysisDocument17 pagesAirline Management AnalysisJerry John Ayayi AyiteyNo ratings yet

- The Global Cost of FraudDocument2 pagesThe Global Cost of FraudSefvinur PutriNo ratings yet

- Control de Lectura 1 - 2do ParcialDocument5 pagesControl de Lectura 1 - 2do ParcialPaulaNo ratings yet

- Blue Ridge Spain ExcelDocument5 pagesBlue Ridge Spain Excelsanchi virmaniNo ratings yet

- APF2Document1 pageAPF2chuckepsteinNo ratings yet

- Risk Man. & Comp. SheetDocument10 pagesRisk Man. & Comp. Sheetaarmcourse1No ratings yet

- Casino Visitation, Revenue, and Impact Assessment (11!19!19)Document87 pagesCasino Visitation, Revenue, and Impact Assessment (11!19!19)WSETNo ratings yet

- Hedging Foreign Exchange Rate Risk With Cme FX Futures Cad Vs UsdDocument8 pagesHedging Foreign Exchange Rate Risk With Cme FX Futures Cad Vs UsdThục LinhNo ratings yet

- Summit - 04-05-06-07-08-09 Oct. 09Document1 pageSummit - 04-05-06-07-08-09 Oct. 09Breckenridge Grand Real EstateNo ratings yet

- Assigment 3Document9 pagesAssigment 3Felipe PinedaNo ratings yet

- UntitledDocument26 pagesUntitledDhapaDanNo ratings yet

- Nominex Presentation Bop 25 Jun 2022 - PublicDocument46 pagesNominex Presentation Bop 25 Jun 2022 - PublicAsni Nor Rizwan Abdul RaniNo ratings yet

- Imperfect Competition: Pure MonopolyDocument15 pagesImperfect Competition: Pure MonopolyMarcus WellsNo ratings yet

- Pure MonopolyDocument26 pagesPure MonopolyRifat al haque DhruboNo ratings yet

- Riggs Group September 2012Document7 pagesRiggs Group September 2012nspectah1No ratings yet

- Issues of Housing Affordability in Montgomery County, MD: Slide 1Document87 pagesIssues of Housing Affordability in Montgomery County, MD: Slide 1M-NCPPCNo ratings yet

- FinMan Assign. No. 3 - ToyWorldDocument6 pagesFinMan Assign. No. 3 - ToyWorldKristine Nitzkie SalazarNo ratings yet

- MKM704 - Finance For Marketers - Lab 4 Solution: MKM704 - DR Page 1 of 3 02/18/2022 at 22:03:08Document3 pagesMKM704 - Finance For Marketers - Lab 4 Solution: MKM704 - DR Page 1 of 3 02/18/2022 at 22:03:08VarunNo ratings yet

- MSFT Valuation 28 Sept 2019Document51 pagesMSFT Valuation 28 Sept 2019ket careNo ratings yet

- 2 IF Function Vlookup ExerciseDocument10 pages2 IF Function Vlookup Exercisekeith tambaNo ratings yet

- Ex1 Sensitivity AnalysisDocument21 pagesEx1 Sensitivity AnalysisP MarpaungNo ratings yet

- Case 13Document7 pagesCase 13Nguyễn Quốc TháiNo ratings yet

- ACCT 10001 Accounting Reports & Analysis Review Questions - Topic 9 Chapter 9: BudgetingDocument8 pagesACCT 10001 Accounting Reports & Analysis Review Questions - Topic 9 Chapter 9: BudgetingBáchHợpNo ratings yet

- Equipment Purchase Costs V2 07112014Document81 pagesEquipment Purchase Costs V2 07112014Tom GoodladNo ratings yet

- Agger Company - AssignmentDocument7 pagesAgger Company - AssignmentWolfManNo ratings yet

- Quarterly Review: The Housing Boom: 2002-2005Document4 pagesQuarterly Review: The Housing Boom: 2002-2005Nicholas FrenchNo ratings yet

- Stock Portfolio SubscribersDocument16 pagesStock Portfolio SubscribersNguyenNo ratings yet

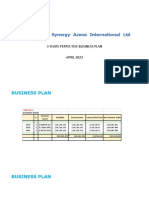

- Synergy Arena International LTD: 3 Years Perpective Business Plan APRIL 2023Document10 pagesSynergy Arena International LTD: 3 Years Perpective Business Plan APRIL 2023brook emenikeNo ratings yet

- Plus CDSE Performance Bonuses:: Diplomat - Ambassador - Regional Ambassador - National Ambassador - Global AmbassadorDocument2 pagesPlus CDSE Performance Bonuses:: Diplomat - Ambassador - Regional Ambassador - National Ambassador - Global AmbassadorsogunmolaNo ratings yet

- Report 5e0631ed0Document1 pageReport 5e0631ed0Teresa Dallman KeenanNo ratings yet

- Dramatic Rebound Characterizes Canada's Luxury Home Segment in 2010Document3 pagesDramatic Rebound Characterizes Canada's Luxury Home Segment in 2010api-26009134No ratings yet

- 1.1 - Forwards and Futures, IntroductionDocument37 pages1.1 - Forwards and Futures, IntroductioncutehibouxNo ratings yet

- ADIB Current Spending LimitsDocument1 pageADIB Current Spending LimitsMohamed AhmedNo ratings yet

- Loan Options For Idaho Store Purchase: Rates Versus Months: Projected Income Statement ModelDocument9 pagesLoan Options For Idaho Store Purchase: Rates Versus Months: Projected Income Statement ModeltinoNo ratings yet

- Ford Fact Sheet - Economic FootprintDocument6 pagesFord Fact Sheet - Economic FootprintFord Motor Company100% (30)

- Montos de Los Créditos Hipotecarios 2017: IssfamDocument1 pageMontos de Los Créditos Hipotecarios 2017: IssfamOmar Utrera RodriguezNo ratings yet

- Excel 8G Income ModelDocument6 pagesExcel 8G Income Modelsayfsalah2016No ratings yet

- MFF Challenge PropDocument19 pagesMFF Challenge PropSamuelNo ratings yet

- Assigment 4 SolutionDocument2 pagesAssigment 4 SolutionRamy ShabanaNo ratings yet

- Systemetic Investment Plan Empowering BeginnerDocument33 pagesSystemetic Investment Plan Empowering BeginnerKshitiz Rastogi0% (1)

- Managing Customer ProfitabilityDocument6 pagesManaging Customer ProfitabilitySafira UlfaNo ratings yet

- The Money Markets: Quantitative ProblemsDocument4 pagesThe Money Markets: Quantitative ProblemsMai AnhNo ratings yet

- Exc Rate As On Nov 08, 2022Document1 pageExc Rate As On Nov 08, 2022iftihaj HossainNo ratings yet

- Astra: AstrazionDocument17 pagesAstra: AstrazionRomeo Arceo Jr100% (2)

- whatIfAnalysis Classwork 2024Document12 pageswhatIfAnalysis Classwork 2024ishika18bhargavaNo ratings yet

- Book Sale Via Earn Out - SampleDocument5 pagesBook Sale Via Earn Out - SamplesaonNo ratings yet

- RiskGrade Your Investments: Measure Your Risk and Create WealthFrom EverandRiskGrade Your Investments: Measure Your Risk and Create WealthNo ratings yet

- Buy Now: The Ultimate Guide to Owning and Investing in PropertyFrom EverandBuy Now: The Ultimate Guide to Owning and Investing in PropertyRating: 5 out of 5 stars5/5 (1)

- Presentation Sussex Conference (1st Year PHD Student)Document9 pagesPresentation Sussex Conference (1st Year PHD Student)vsavvidouNo ratings yet

- JohnsonEvinrude ElectricalDocument5 pagesJohnsonEvinrude Electricalwguenon100% (1)

- Power Industry IN INDIADocument21 pagesPower Industry IN INDIAbb2No ratings yet

- Persuasive Essay: English Proficiency For The Empowered ProfessionalsDocument2 pagesPersuasive Essay: English Proficiency For The Empowered ProfessionalsKyle Sanchez (Kylie)No ratings yet

- Hyperemesis GravidarumDocument13 pagesHyperemesis GravidarumBang JuntakNo ratings yet

- 01 Drillmec Company Profile E78913cf d70c 465b 911a Ab1b009160baDocument13 pages01 Drillmec Company Profile E78913cf d70c 465b 911a Ab1b009160baDaniel Marulituah SinagaNo ratings yet

- Take Aim Spring 2008Document16 pagesTake Aim Spring 2008Felix GrosseNo ratings yet

- Discurso de Obama - Obamas Victory SpeechDocument3 pagesDiscurso de Obama - Obamas Victory SpeechccalderoNo ratings yet

- Clarence-Smith, W. G., African and European Cocoa Producers On Fernando Poo, 1880s To 1910s', The Journal of African History, 35 (1994), 179-199Document22 pagesClarence-Smith, W. G., African and European Cocoa Producers On Fernando Poo, 1880s To 1910s', The Journal of African History, 35 (1994), 179-199OSGuineaNo ratings yet

- 3.11.1 Packet Tracer Network Security Exploration Physical ModeDocument7 pages3.11.1 Packet Tracer Network Security Exploration Physical ModeirfanNo ratings yet

- CLONINGDocument5 pagesCLONINGAfrin IbrahimNo ratings yet

- WHAP AP Review Session 6 - 1900-PresentDocument46 pagesWHAP AP Review Session 6 - 1900-PresentNajlae HommanNo ratings yet

- Micro Focus Cobol Survey Itl 2015 Report PTDocument22 pagesMicro Focus Cobol Survey Itl 2015 Report PTprojrev2No ratings yet

- Constellation Program BrochureDocument2 pagesConstellation Program BrochureBob Andrepont100% (1)

- ARTS 725-734, 748-749 Donation REVIEW23Document11 pagesARTS 725-734, 748-749 Donation REVIEW23Vikki AmorioNo ratings yet

- XKCD Dissertation DefenseDocument6 pagesXKCD Dissertation DefenseWebsitesToTypePapersUK100% (1)

- Hoang Huy HoangDocument12 pagesHoang Huy Hoanghoang hoangNo ratings yet

- Chapter 7 Strong and Weak FormsDocument28 pagesChapter 7 Strong and Weak Formsaligamil9100% (1)

- Pulmo Viewboxes BLOCK 8Document251 pagesPulmo Viewboxes BLOCK 8U.P. College of Medicine Class 2014100% (2)

- Conectores y DiagramasDocument6 pagesConectores y Diagramasrodrigo michelNo ratings yet

- CO4CRT12 - Quantitative Techniques For Business - II (T)Document4 pagesCO4CRT12 - Quantitative Techniques For Business - II (T)Ann Maria GeorgeNo ratings yet

- Online Resources For ESL TeachersDocument12 pagesOnline Resources For ESL TeachersmehindmeNo ratings yet

- MOTORTECH SalesFlyer Spark Plug Extensions For WAUKESHA Gas Engines 01.15.051 en 2017 04Document4 pagesMOTORTECH SalesFlyer Spark Plug Extensions For WAUKESHA Gas Engines 01.15.051 en 2017 04RobertNo ratings yet

- Membres Consell CSDocument2 pagesMembres Consell CSpersepNo ratings yet

- Magic Cards - ShadowDocument2 pagesMagic Cards - ShadowLuis RodriguezNo ratings yet

- Led LightssDocument23 pagesLed LightssBhavin GhoniyaNo ratings yet

- Fortaleza vs. LapitanDocument15 pagesFortaleza vs. LapitanAji AmanNo ratings yet