Download as ppt, pdf, or txt

You might also like

- Certificate of Quality-TemplatesDocument1 pageCertificate of Quality-Templatesadnanbajwa141No ratings yet

- Introduction To Financial ManagementDocument9 pagesIntroduction To Financial ManagementRitesh ShreshthaNo ratings yet

- For Holders: Automated Income Tax CalculationDocument16 pagesFor Holders: Automated Income Tax Calculationmaruf048No ratings yet

- Assignment 3 SolDocument1 pageAssignment 3 Solhussain elahiNo ratings yet

- International Tax ComparisonsDocument23 pagesInternational Tax ComparisonsJahnavi BadlaniNo ratings yet

- The Government Sector: 2008 by The Mcgraw-Hill Companies, Inc. All Rights ReservedDocument57 pagesThe Government Sector: 2008 by The Mcgraw-Hill Companies, Inc. All Rights ReservedMDPGCNo ratings yet

- Econ Math ProjectDocument14 pagesEcon Math ProjectAndy ChiuNo ratings yet

- Ecu - 08606 Lecture 5Document23 pagesEcu - 08606 Lecture 5DanielNo ratings yet

- Income Tax Calculator FY 2020 2021Document8 pagesIncome Tax Calculator FY 2020 2021LalitNo ratings yet

- Emailing Inter Full Book DT - Youtube - Prof - Aagam Dalal-3Document126 pagesEmailing Inter Full Book DT - Youtube - Prof - Aagam Dalal-3chalu account100% (2)

- CalculationsDocument5 pagesCalculationsKhawaja HamzaNo ratings yet

- Chapter 1 SolutionsDocument3 pagesChapter 1 Solutionshassan.muradNo ratings yet

- TAXESDocument26 pagesTAXESPurchiaNo ratings yet

- Tax CalculatorDocument3 pagesTax CalculatorRohit KumarNo ratings yet

- Head Description: Income Tax Ratio Gross Income/Tax LiabilityDocument4 pagesHead Description: Income Tax Ratio Gross Income/Tax LiabilityGhodawatNo ratings yet

- Income Tax FY 2020-21-2Document25 pagesIncome Tax FY 2020-21-2umeshapkNo ratings yet

- Tax Slabs: Ca. Dipayan DasDocument4 pagesTax Slabs: Ca. Dipayan DasNoob GamerNo ratings yet

- Income Tax Calculator FY 2020 2021Document8 pagesIncome Tax Calculator FY 2020 2021bikofax543No ratings yet

- Income Tax Calculator FY 2020 2021Document8 pagesIncome Tax Calculator FY 2020 2021GhanshyamNo ratings yet

- Trần Hoài Anh Hs150639 Ib1602Document3 pagesTrần Hoài Anh Hs150639 Ib1602Vũ Nhi AnNo ratings yet

- Income Tax Calculator FY 2015-16 (AY 2016-17) : Particulars Details TypeDocument4 pagesIncome Tax Calculator FY 2015-16 (AY 2016-17) : Particulars Details TypeKamlesh ChauhanNo ratings yet

- Government Microeconomic Intervention Pt.4Document13 pagesGovernment Microeconomic Intervention Pt.4Yashjeet Gurung RCS KJNo ratings yet

- Provided Tax Tables: These Tax Tables Are Provided in The Exam Booklets For The March 2011 CFP Certification ExaminationDocument5 pagesProvided Tax Tables: These Tax Tables Are Provided in The Exam Booklets For The March 2011 CFP Certification ExaminationDebolina DasNo ratings yet

- UntitledDocument30 pagesUntitledRavi BanothNo ratings yet

- 1h DT Revision Short Notes Selected Chapters Cma Inter Dec 2023Document109 pages1h DT Revision Short Notes Selected Chapters Cma Inter Dec 2023Vaheed AliNo ratings yet

- Ques. Defered TaxDocument40 pagesQues. Defered TaxKALYANI JAYAKRISHNAN 2022155No ratings yet

- DT May 23 in 50 PagesDocument15 pagesDT May 23 in 50 PagesShivaji hariNo ratings yet

- Old Vs New Tax Regime Comparative AnalysisDocument11 pagesOld Vs New Tax Regime Comparative AnalysisAkchu KadNo ratings yet

- 1 3+part+2Document28 pages1 3+part+2jaspreet kaurNo ratings yet

- Complete C7Document15 pagesComplete C7tai nguyenNo ratings yet

- ExtraTaxProblem-TY2020 Student - SUSANDocument6 pagesExtraTaxProblem-TY2020 Student - SUSANhhunter530No ratings yet

- 19040400095- Nguyễn Hữu Phú- Lab03 Model Design 21092020Document5 pages19040400095- Nguyễn Hữu Phú- Lab03 Model Design 21092020Viem AnhNo ratings yet

- Only Fill Yellow Cells: WorkingsDocument2 pagesOnly Fill Yellow Cells: WorkingsvikrammoolchandaniNo ratings yet

- Topic-2-INTRODUCTION TO DIFFERENT TAXATION LAWS OF PAKISTANDocument18 pagesTopic-2-INTRODUCTION TO DIFFERENT TAXATION LAWS OF PAKISTANJaved AnwarNo ratings yet

- Materi - INCOME TAX ACCOUNTING - 26march2021Document18 pagesMateri - INCOME TAX ACCOUNTING - 26march2021Septian Dwi AnggoroNo ratings yet

- 12lpa Tax ComputationDocument1 page12lpa Tax ComputationSai KrishnaNo ratings yet

- Taxable - Income - Formula - Excel - TemplateDocument8 pagesTaxable - Income - Formula - Excel - TemplateFaizan AhmadNo ratings yet

- Exhibits 5.9 and 5.10Document2 pagesExhibits 5.9 and 5.10Oscar PinillosNo ratings yet

- Income Taxation: Under The Train LAWDocument9 pagesIncome Taxation: Under The Train LAWcerayNo ratings yet

- Solution Manual For Cfin 5Th Edition by Besley and Brigham Isbn 1305661656 9781305661653 Full Chapter PDFDocument36 pagesSolution Manual For Cfin 5Th Edition by Besley and Brigham Isbn 1305661656 9781305661653 Full Chapter PDFtiffany.kunst387100% (12)

- TAX LIABILITY PDF) OkDocument7 pagesTAX LIABILITY PDF) OksaeNo ratings yet

- Easy TaxDocument1 pageEasy TaxSiva GaneshNo ratings yet

- Acc501 GDB 1 Sol Fall 2022Document1 pageAcc501 GDB 1 Sol Fall 2022Sth. Bilal BashirNo ratings yet

- TaxationDocument12 pagesTaxationjanahh.omNo ratings yet

- Tax Credit Certificate - 2018 : PPS No: 1793106MADocument4 pagesTax Credit Certificate - 2018 : PPS No: 1793106MAAlexandru CiobanuNo ratings yet

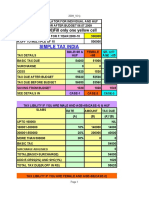

- Simple Tax India: (F.YEAR 2009-10) Fill Only One Yellow CellDocument4 pagesSimple Tax India: (F.YEAR 2009-10) Fill Only One Yellow CellRaj PatilNo ratings yet

- Tax Calculator AY 09-10Document4 pagesTax Calculator AY 09-10madhuamsNo ratings yet

- Simple Tax India: (F.YEAR 2009-10) Fill Only One Yellow CellDocument4 pagesSimple Tax India: (F.YEAR 2009-10) Fill Only One Yellow CellPradip ShawNo ratings yet

- Ecu - 08606 Lecture 6Document21 pagesEcu - 08606 Lecture 6DanielNo ratings yet

- Payroll AccoutingDocument7 pagesPayroll AccoutingGizaw BelayNo ratings yet

- NZ Resident Tax Refund CalculatorDocument3 pagesNZ Resident Tax Refund CalculatorkwqczxrdwnNo ratings yet

- Month Net Taxable Income Tax Slabs Tax RateDocument2 pagesMonth Net Taxable Income Tax Slabs Tax RateBhargav ChintalapatiNo ratings yet

- ACC 3013 Taxation RevisionDocument4 pagesACC 3013 Taxation Revisionfalnuaimi001No ratings yet

- Chapter 10 - Introduction To Government FinanceDocument26 pagesChapter 10 - Introduction To Government Financewatts175% (4)

- Taxation in EthiopiaDocument7 pagesTaxation in EthiopiaLeulNo ratings yet

- LeverageDocument6 pagesLeveragehussain hasniNo ratings yet

- Deferred Tax Assets: - Arise From Temporary Differences Where, Initially, Tax Rules RequireDocument14 pagesDeferred Tax Assets: - Arise From Temporary Differences Where, Initially, Tax Rules RequireSaddy ButtNo ratings yet

- F6SGP Dec2015q PDFDocument15 pagesF6SGP Dec2015q PDFDrift SirNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Difference Between The Balance of Payments CA and FADocument2 pagesDifference Between The Balance of Payments CA and FAIrfan AhmedNo ratings yet

- IrfanAhmed ECO315 TermPaperDocument10 pagesIrfanAhmed ECO315 TermPaperIrfan AhmedNo ratings yet

- January 2023 QP - Paper 2 Edexcel Economics IGCSE-2-20Document19 pagesJanuary 2023 QP - Paper 2 Edexcel Economics IGCSE-2-20Irfan AhmedNo ratings yet

- Paper 2 Edexcel Economics IGCSE Mock 03Document24 pagesPaper 2 Edexcel Economics IGCSE Mock 03Irfan AhmedNo ratings yet

- Thesis On Money LaunderingDocument278 pagesThesis On Money Launderingkananhajipara80% (5)

- Predatory Value: Economies of Dispossession and Disturbed RelationalitiesDocument18 pagesPredatory Value: Economies of Dispossession and Disturbed RelationalitiesJodi MelamedNo ratings yet

- Digital Business PPT CH - 4Document34 pagesDigital Business PPT CH - 4Chirag PatilNo ratings yet

- Corporate Social Performance Inter-Industry and International DifferencesDocument29 pagesCorporate Social Performance Inter-Industry and International DifferencesdessyNo ratings yet

- MBA Employment Report 2021: For The Mannheim Full-Time MBA Class of 2020Document5 pagesMBA Employment Report 2021: For The Mannheim Full-Time MBA Class of 2020SaikatNo ratings yet

- Antrix Kumar (102004056) Sehajpal Singh Badesha (102004040 Somnath Banerjee (102004049) Bakul Kwatra (102004041) Abhinav (102004045)Document18 pagesAntrix Kumar (102004056) Sehajpal Singh Badesha (102004040 Somnath Banerjee (102004049) Bakul Kwatra (102004041) Abhinav (102004045)Sehajpal BadeshaNo ratings yet

- FAR610 Consolidated Cashflow Past Semester FinalexamDocument18 pagesFAR610 Consolidated Cashflow Past Semester FinalexamANIS SYAKIRAH ADHWA MAHDILLAHNo ratings yet

- 3.2. Profit or Loss StatementDocument10 pages3.2. Profit or Loss StatementSayaNo ratings yet

- International Business Studies Final ExamDocument4 pagesInternational Business Studies Final ExamSatyendra Upreti100% (1)

- LPP AssignmentDocument3 pagesLPP AssignmentMohammed Marfatiya100% (1)

- A2 - Bs (U3) - Book-1Document256 pagesA2 - Bs (U3) - Book-1Fahad FarhanNo ratings yet

- Raushan RESUME1Document3 pagesRaushan RESUME1Israr AlamNo ratings yet

- FINAL - EXAM - ENG128 - 2021F: Tests & QuizzesDocument1 pageFINAL - EXAM - ENG128 - 2021F: Tests & QuizzesHoàng Tiến ĐạtNo ratings yet

- Power of Strategy MM3201 Draft QuestionnaireDocument4 pagesPower of Strategy MM3201 Draft QuestionnaireDaniela GetaladaNo ratings yet

- Lead Singapore and MalaysiaDocument30 pagesLead Singapore and Malaysiav6185666No ratings yet

- EagleRidge Development StatementDocument1 pageEagleRidge Development StatementRob PortNo ratings yet

- Bai Tap CF 2018 Solution PDFDocument11 pagesBai Tap CF 2018 Solution PDFXuân Huỳnh100% (2)

- Motel Business PlanDocument14 pagesMotel Business PlanDinkisaNo ratings yet

- Share Market Basics - Learn Stock Market Basics in India - Karvy OnlineDocument7 pagesShare Market Basics - Learn Stock Market Basics in India - Karvy Onlinevenki420No ratings yet

- Doctrine of MarshallingDocument6 pagesDoctrine of MarshallingKinshuk BaruaNo ratings yet

- The Wall Street Journal-231102Document32 pagesThe Wall Street Journal-231102Josué MachacaNo ratings yet

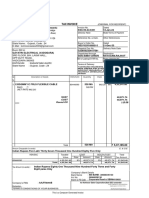

- 3351 InvoiceDocument1 page3351 InvoicepkNo ratings yet

- Chapter 5Document58 pagesChapter 5henryNo ratings yet

- Lecture 06 Basic Services 1Document49 pagesLecture 06 Basic Services 1ZHI YI SOONo ratings yet

- Financiamiento de La Circularidad: Desmitificar Las Finanzas para La Economía CircularDocument100 pagesFinanciamiento de La Circularidad: Desmitificar Las Finanzas para La Economía CircularComunicarSe-ArchivoNo ratings yet

- Chapter 8Document34 pagesChapter 8JP ONo ratings yet

- Module 3 - Activity 1 AnswersDocument5 pagesModule 3 - Activity 1 AnswersJoy Guevarra100% (1)

- ch01 Kieso IFRS4 PPTDocument55 pagesch01 Kieso IFRS4 PPTanna purwaningsih100% (1)

- Ron InvoiceDocument1 pageRon InvoiceJohn PoirierNo ratings yet