Download as pptx, pdf, or txt

You might also like

- Transfer Pricing EssayDocument8 pagesTransfer Pricing EssayFernando Montoro SánchezNo ratings yet

- International Accounting: Learning ObjectivesDocument13 pagesInternational Accounting: Learning ObjectivesNorhan NabilNo ratings yet

- Management Accounting: MBA First Year CR23Document14 pagesManagement Accounting: MBA First Year CR23Ajinkya NaikNo ratings yet

- Chapter 7 - PricingDocument19 pagesChapter 7 - PricingMaria JosefaNo ratings yet

- GM CH 6 Pricing DecisionsDocument48 pagesGM CH 6 Pricing DecisionsgeremewNo ratings yet

- Doupnik ch11Document33 pagesDoupnik ch11Catalina Oriani0% (1)

- Introduction To Transfer PricingDocument8 pagesIntroduction To Transfer PricinglinapramajayaNo ratings yet

- SM Finalnew Vol2 Cp7 CHAPTER 7Document51 pagesSM Finalnew Vol2 Cp7 CHAPTER 7Prin PrinksNo ratings yet

- Transfer PricingDocument26 pagesTransfer PricingPrince McGershonNo ratings yet

- Transfer PricingDocument16 pagesTransfer PricingAbokingsNo ratings yet

- IFM Transfer PricingDocument9 pagesIFM Transfer PricingPooja Ujjwal JainNo ratings yet

- Chapter 1 Thomas 13eDocument27 pagesChapter 1 Thomas 13erc0952No ratings yet

- Dividend Policy in Multinationals and Transfer PricingDocument11 pagesDividend Policy in Multinationals and Transfer PricingKaren Diane Chua RiveraNo ratings yet

- Chapter 5Document22 pagesChapter 5JUNAINAH AHMADNo ratings yet

- Thom23e Ch07 FinalDocument38 pagesThom23e Ch07 FinalNguyễn Quỳnh HươngNo ratings yet

- Alternative Methods of Transfer PricingDocument4 pagesAlternative Methods of Transfer PricingRyan FranklinNo ratings yet

- Thom23e Ch07 FinalDocument39 pagesThom23e Ch07 FinalLeleNo ratings yet

- Typical Pricing PracticesDocument3 pagesTypical Pricing PracticesDullah AllyNo ratings yet

- C.2. Transfer Pricing EssayDocument7 pagesC.2. Transfer Pricing EssayKondreddi SakuNo ratings yet

- Im 6Document17 pagesIm 6Awal AhmadNo ratings yet

- Transfer PricingDocument26 pagesTransfer Pricingsudhir_hankar100% (1)

- CH 12Document32 pagesCH 12Deepanshu SaraswatNo ratings yet

- Transfer Pricing: Department of AccountingDocument27 pagesTransfer Pricing: Department of AccountingFahmida AkhterNo ratings yet

- Transfer Pricing: Karan Wadhawan 19A Rohit Verma 39A Tapan Sharma 50ADocument10 pagesTransfer Pricing: Karan Wadhawan 19A Rohit Verma 39A Tapan Sharma 50ARachna khuranaNo ratings yet

- International Pricing DecisionsDocument32 pagesInternational Pricing DecisionsSaumya JaiswalNo ratings yet

- PricingDocument26 pagesPricingRucha TandulwadkarNo ratings yet

- Transfer PricingDocument29 pagesTransfer PricingRina MartinaNo ratings yet

- Chapter 6 - Managing PriceDocument56 pagesChapter 6 - Managing PriceShafayet JamilNo ratings yet

- IMChap 012Document18 pagesIMChap 012Aaron Hamilton100% (2)

- Chapter Six Nternational Marketing For Ug StudentsDocument52 pagesChapter Six Nternational Marketing For Ug StudentsEyob ZekariyasNo ratings yet

- Transfer Pricing FinalDocument29 pagesTransfer Pricing FinalVineet RanjanNo ratings yet

- Lecture 8 - Forms of RegulationDocument20 pagesLecture 8 - Forms of RegulationsolachristoNo ratings yet

- Management Control Systems, Transfer Pricing, and Multinational ConsiderationsDocument70 pagesManagement Control Systems, Transfer Pricing, and Multinational Considerationsjuang philiaNo ratings yet

- Transfer Pricing and Multinational Management Control SystemsDocument10 pagesTransfer Pricing and Multinational Management Control Systemslucas silvaNo ratings yet

- Bhavya N L Divya L Divya S Sathwik SandeepDocument44 pagesBhavya N L Divya L Divya S Sathwik SandeepVipin K HariNo ratings yet

- Integration Is A Crucial Part of Any Successful AcquisitionDocument10 pagesIntegration Is A Crucial Part of Any Successful AcquisitionPooja Chander DudejaNo ratings yet

- Geelec10-M2 01Document17 pagesGeelec10-M2 01dan.nics19No ratings yet

- Vietnam Product/Pricing Diagnostic Executive Overview: December, 2016Document24 pagesVietnam Product/Pricing Diagnostic Executive Overview: December, 2016deepak cityNo ratings yet

- Lecture 23 - Advanced Cost and Management AccountingDocument16 pagesLecture 23 - Advanced Cost and Management AccountingawaisjinnahNo ratings yet

- Pricing Strategies - Part1 PDFDocument52 pagesPricing Strategies - Part1 PDFJaisal SinghNo ratings yet

- ECON 350 - October 20th 2022 (F22)Document15 pagesECON 350 - October 20th 2022 (F22)Dat NguyenNo ratings yet

- Chap 9 Current Issues in Tax TP APADocument31 pagesChap 9 Current Issues in Tax TP APA2022452932No ratings yet

- Managerial Economics and Business Strategy - Ch. 6 - The Organization of The FirmDocument22 pagesManagerial Economics and Business Strategy - Ch. 6 - The Organization of The FirmRayhanNo ratings yet

- WK 6 Aa Lesson 6 Transfer Pricing Lec NotesDocument3 pagesWK 6 Aa Lesson 6 Transfer Pricing Lec Notesnot funny didn't laughNo ratings yet

- Strategic Pricing Techniques: Pacheco, Ivan Venturayo, Haven Well Ginggo, Marilyn (BSA1C)Document41 pagesStrategic Pricing Techniques: Pacheco, Ivan Venturayo, Haven Well Ginggo, Marilyn (BSA1C)Ivan PachecoNo ratings yet

- Unit-Iv ImDocument62 pagesUnit-Iv ImAVADHESH KUMARNo ratings yet

- Cartels in The Cement IndustryDocument29 pagesCartels in The Cement IndustryrashmiNo ratings yet

- Case 15-5 Xerox Corporation RecommendationsDocument6 pagesCase 15-5 Xerox Corporation RecommendationsgabrielyangNo ratings yet

- OligopolyDocument21 pagesOligopolyJuli SitohangNo ratings yet

- International MarketingDocument19 pagesInternational MarketingHimanshu BansalNo ratings yet

- Managerial Economics and Gap Between Theory and PracticeDocument6 pagesManagerial Economics and Gap Between Theory and Practicesamuel debebeNo ratings yet

- International Marketing Module 3Document60 pagesInternational Marketing Module 3VyshnavNo ratings yet

- CM13e Basic PPT Ch18Document18 pagesCM13e Basic PPT Ch18Eisya SwiftNo ratings yet

- International PricingDocument22 pagesInternational PricingAnonymous d3CGBMzNo ratings yet

- Valuation of Distressed Firms in India: Venkatesh PanchapagesanDocument15 pagesValuation of Distressed Firms in India: Venkatesh PanchapagesanJobin JohnNo ratings yet

- Exposure Management Internal TechniquesDocument8 pagesExposure Management Internal TechniquesArockia Shiny SNo ratings yet

- Mas Research PaperDocument7 pagesMas Research Paperdiane camansagNo ratings yet

- 3 Strategy - External AnalysisDocument37 pages3 Strategy - External AnalysismahammedNo ratings yet

- The Key to Higher Profits: Pricing PowerFrom EverandThe Key to Higher Profits: Pricing PowerRating: 5 out of 5 stars5/5 (1)

- The Outsourcing Revolution (Review and Analysis of Corbett's Book)From EverandThe Outsourcing Revolution (Review and Analysis of Corbett's Book)No ratings yet

- Doupnik 6e Chap006 PPT Accessible GM OutputDocument65 pagesDoupnik 6e Chap006 PPT Accessible GM Outputhasan jabrNo ratings yet

- Doupnik 6e Chap005 PPT Accessible GM OutputDocument56 pagesDoupnik 6e Chap005 PPT Accessible GM Outputhasan jabrNo ratings yet

- Doupnik 6e Chap004 PPT Accessible GM OutputDocument41 pagesDoupnik 6e Chap004 PPT Accessible GM Outputhasan jabrNo ratings yet

- Doupnik 6e Chap011 PPT Accessible GM OutputDocument55 pagesDoupnik 6e Chap011 PPT Accessible GM Outputhasan jabrNo ratings yet

- pp03Document51 pagespp03hasan jabrNo ratings yet

- Doupnik 6e Chap010 PPT Accessible GM OutputDocument41 pagesDoupnik 6e Chap010 PPT Accessible GM Outputhasan jabrNo ratings yet

- Ngos1 2Document35 pagesNgos1 2hasan jabrNo ratings yet

- Chapter 9 Accounting For Musharaka FinancingDocument28 pagesChapter 9 Accounting For Musharaka Financinghasan jabrNo ratings yet

- ch12 SM RankinDocument10 pagesch12 SM Rankinhasan jabrNo ratings yet

- Chapter FiveDocument58 pagesChapter Fivehasan jabrNo ratings yet

- Chapter 8BDocument17 pagesChapter 8Bhasan jabrNo ratings yet

- ch01 SM RankinDocument14 pagesch01 SM Rankinhasan jabrNo ratings yet

- Fifth ChapDocument22 pagesFifth Chaphasan jabrNo ratings yet

- Chapter TwoDocument42 pagesChapter Twohasan jabrNo ratings yet

- Third ChapDocument32 pagesThird Chaphasan jabrNo ratings yet

- Second ChapDocument39 pagesSecond Chaphasan jabrNo ratings yet

- Chapter 8Document23 pagesChapter 8hasan jabrNo ratings yet

- Chapter OneDocument31 pagesChapter Onehasan jabrNo ratings yet

- Ais CH 6Document35 pagesAis CH 6hasan jabrNo ratings yet

- Chapter 10.accounting For IjarahDocument46 pagesChapter 10.accounting For Ijarahhasan jabrNo ratings yet

- Accounting Theory Ch01Document23 pagesAccounting Theory Ch01hasan jabrNo ratings yet

- Chap010-Financial AnalysisDocument40 pagesChap010-Financial Analysishasan jabrNo ratings yet

- Financial Statement Analysis: K.R. SubramanyamDocument42 pagesFinancial Statement Analysis: K.R. Subramanyamhasan jabrNo ratings yet

- Globalization: Prepared By: Fernando Quijano and Yvonn QuijanoDocument42 pagesGlobalization: Prepared By: Fernando Quijano and Yvonn Quijanohasan jabrNo ratings yet

- Long-Run Growth: Prepared By: Fernando Quijano and Yvonn QuijanoDocument40 pagesLong-Run Growth: Prepared By: Fernando Quijano and Yvonn Quijanohasan jabrNo ratings yet

- Accounting Theory-Ch05 - Income ConceptDocument28 pagesAccounting Theory-Ch05 - Income Concepthasan jabrNo ratings yet

- Household and Firm Behavior in The Macroeconomy: A Further LookDocument64 pagesHousehold and Firm Behavior in The Macroeconomy: A Further Lookhasan jabrNo ratings yet

- Debates in Macroeconomics: Monetarism, New Classical Theory, and Supply-Side EconomicsDocument38 pagesDebates in Macroeconomics: Monetarism, New Classical Theory, and Supply-Side Economicshasan jabrNo ratings yet

- DFI 224 Assignment March 2024Document16 pagesDFI 224 Assignment March 2024Tiana TillaNo ratings yet

- LabidabdabDocument4 pagesLabidabdabJusteen ChamNo ratings yet

- Goel Institute of Technology and Management Lucknow PDFDocument87 pagesGoel Institute of Technology and Management Lucknow PDFRohan SrivastavaNo ratings yet

- FAMS PPM Configuration Workbook v0.4Document267 pagesFAMS PPM Configuration Workbook v0.4murliramNo ratings yet

- Trade Life CycleDocument1 pageTrade Life CycleVishnuNo ratings yet

- Class NotesDocument63 pagesClass NotesVikram SinghNo ratings yet

- MSRPT PDFDocument1 pageMSRPT PDFHasanur RahamanNo ratings yet

- Best SMS or IM ServDocument3 pagesBest SMS or IM Servirfanabdullahal9No ratings yet

- 2022 Annual Report Final - Dizon MinesDocument112 pages2022 Annual Report Final - Dizon MinesJun BelenNo ratings yet

- Ys%, XLD M Dka S%L Iudcjd Ckrcfha .Eiü M %H: The Gazette of The Democratic Socialist Republic of Sri LankaDocument5 pagesYs%, XLD M Dka S%L Iudcjd Ckrcfha .Eiü M %H: The Gazette of The Democratic Socialist Republic of Sri LankaKajarathan SubramaniamNo ratings yet

- Corporate Risk Management2Document101 pagesCorporate Risk Management2ANo ratings yet

- Chapter 4 - Time Value of MoneyDocument28 pagesChapter 4 - Time Value of MoneyIm HerinNo ratings yet

- RatioanalyasisDocument20 pagesRatioanalyasiscknowledge10No ratings yet

- The Gartley PatternDocument1 pageThe Gartley PatternBiantoroKunartoNo ratings yet

- Central Bank of Nigeria Communiqué No. 146 of The Monetary Policy Committee Meeting Held On Monday 23 and Tuesday 24 JANUARY 2023Document70 pagesCentral Bank of Nigeria Communiqué No. 146 of The Monetary Policy Committee Meeting Held On Monday 23 and Tuesday 24 JANUARY 2023QS OH OladosuNo ratings yet

- ForexDoc Ebook PreviewDocument17 pagesForexDoc Ebook Previewjoe337992No ratings yet

- BofA Merrill - QuestionsDocument2 pagesBofA Merrill - QuestionsShubham KumarNo ratings yet

- FM Chapter 2Document16 pagesFM Chapter 2mearghaile4No ratings yet

- International Financial Management 8th Edition Ebook PDFDocument41 pagesInternational Financial Management 8th Edition Ebook PDFlarry.pacheco182No ratings yet

- 6 - Advanced Cryptocurrency Analysis & Trading - v2Document13 pages6 - Advanced Cryptocurrency Analysis & Trading - v2Rey CiaNo ratings yet

- ACCA FA1 Practice Question 1Document5 pagesACCA FA1 Practice Question 1arslan.ahmed8179No ratings yet

- T8 Financial Strategy III (Suggested Answers)Document3 pagesT8 Financial Strategy III (Suggested Answers)xinghe666No ratings yet

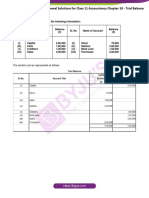

- Ts Grewal Solutions For Class 11 Accountancy Chapter 10 TrialDocument22 pagesTs Grewal Solutions For Class 11 Accountancy Chapter 10 TrialMantejNo ratings yet

- Chapter 17 18 Exam Partnership Formation and Operations Sept. 15 2021 - Attempt ReviewDocument24 pagesChapter 17 18 Exam Partnership Formation and Operations Sept. 15 2021 - Attempt ReviewGio BurburanNo ratings yet

- IC-38 Crash CourseDocument18 pagesIC-38 Crash CourseÅdârsh DûßêyNo ratings yet

- Compare Funds 02 Apr 2023 1954Document2 pagesCompare Funds 02 Apr 2023 1954c22manasNo ratings yet

- The Story of Village PalampurDocument5 pagesThe Story of Village PalampurSAHIL SharmaNo ratings yet

- Ae11 Chapter 6 ReviewerDocument4 pagesAe11 Chapter 6 ReviewerJustine ReyesNo ratings yet

- MAC2602 - Capital Budgeting SlidesDocument35 pagesMAC2602 - Capital Budgeting SlidesShaina-Leigh KoenNo ratings yet

- Sample Practice Exam 10 May Questions - CompressDocument16 pagesSample Practice Exam 10 May Questions - CompressKaycee StylesNo ratings yet