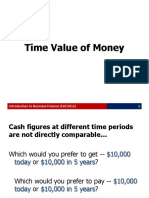

Time Value of Money Chapter 3

Time Value of Money Chapter 3

You might also like

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2024 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2024 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- Financial Management For Public Health and Not-For-Profit Organizations 4th Edition Finkler Solutions Manual DownloadDocument10 pagesFinancial Management For Public Health and Not-For-Profit Organizations 4th Edition Finkler Solutions Manual DownloadPeter Baker100% (25)

- CH 3 SolutionsDocument12 pagesCH 3 SolutionsLucia100% (3)

- AGC Guide To Construction Financing 2nd EditionDocument26 pagesAGC Guide To Construction Financing 2nd EditionCitizen Kwadwo Ansong100% (1)

- EBS (Electronic Bank Statement) - Not Clearing Automatically in FIDocument7 pagesEBS (Electronic Bank Statement) - Not Clearing Automatically in FIKiran KumarNo ratings yet

- Annuity 1Document36 pagesAnnuity 1Mahnoor ZainabNo ratings yet

- Time Value of MoneyDocument46 pagesTime Value of Moneyanum iftikha100% (1)

- REAL 4000 Ch3 HW SolutionsDocument6 pagesREAL 4000 Ch3 HW SolutionsnunyabiznessNo ratings yet

- Time Value of Money Using Excel Time Value of Money Using TI BA II PlusDocument21 pagesTime Value of Money Using Excel Time Value of Money Using TI BA II Plusautocrats 207No ratings yet

- Future Value: FV PV (1 + R) N PV FV / (1 +R) NDocument64 pagesFuture Value: FV PV (1 + R) N PV FV / (1 +R) NShlokNo ratings yet

- FM Lecture 2 Time Value of Money S2 2020.21Document75 pagesFM Lecture 2 Time Value of Money S2 2020.21Quỳnh NguyễnNo ratings yet

- MSL 708 Financial Management Topic 1a: Time Value of Money: Topics (Tentative) : Pre-Readings (BM Chapters)Document15 pagesMSL 708 Financial Management Topic 1a: Time Value of Money: Topics (Tentative) : Pre-Readings (BM Chapters)sasidhar naidu SiripurapuNo ratings yet

- Adobe Scan 23 Nov 2023Document12 pagesAdobe Scan 23 Nov 2023mahakc1110No ratings yet

- Time - Value - of - Money SampleDocument8 pagesTime - Value - of - Money SampleHassleBustNo ratings yet

- Chap 004Document46 pagesChap 004NazifahNo ratings yet

- 2 Time Value of MoneyDocument46 pages2 Time Value of MoneyABHINAV AGRAWALNo ratings yet

- Time Value of Money: DR. Mohamed SamehDocument22 pagesTime Value of Money: DR. Mohamed SamehRamadan IbrahemNo ratings yet

- TVM (FM)Document77 pagesTVM (FM)24 kunal bhojankarNo ratings yet

- 3b Accounting and the Time Value of Money (1)Document37 pages3b Accounting and the Time Value of Money (1)Yandi AriefNo ratings yet

- MAF759: Analytical MethodsDocument42 pagesMAF759: Analytical MethodshieuduyNo ratings yet

- Chapter 2 - How To Calculate Present ValuesDocument21 pagesChapter 2 - How To Calculate Present ValuesTrọng PhạmNo ratings yet

- Time Value of MoneyDocument74 pagesTime Value of MoneybusebeeNo ratings yet

- Time Value of MoneyDocument95 pagesTime Value of MoneyKalkayeNo ratings yet

- Fin 2200 Sum 07 MTDocument12 pagesFin 2200 Sum 07 MTSims LauNo ratings yet

- Financial Managment Chapter 02 PART 1Document41 pagesFinancial Managment Chapter 02 PART 1MISRA MUHUDINNo ratings yet

- Exam Practice QuestionsDocument6 pagesExam Practice Questionssir bookkeeperNo ratings yet

- Net Present Value: Corporate FinanceDocument38 pagesNet Present Value: Corporate FinanceNguyễn Thùy LinhNo ratings yet

- CHPT 4Document41 pagesCHPT 4ferahNo ratings yet

- IAChap 006 PPTDocument39 pagesIAChap 006 PPTلين صبحNo ratings yet

- LM01 Time Value of MoneyDocument48 pagesLM01 Time Value of Moneymenexe9137No ratings yet

- PresTheme2-Eng-Time Value of MoneyDocument39 pagesPresTheme2-Eng-Time Value of MoneyKristina PekovaNo ratings yet

- Kewirausahaan Konsep-Konsep Keuangan: Dteti 2021Document27 pagesKewirausahaan Konsep-Konsep Keuangan: Dteti 2021PANDHU ARDI PRASETYONo ratings yet

- M4 TVMDocument87 pagesM4 TVMAnonymousWriter348No ratings yet

- Time Value of Money Time Value of MoneyDocument29 pagesTime Value of Money Time Value of MoneyEunice Dimple CaliwagNo ratings yet

- 07 Time Value of Money - BE ExercisesDocument26 pages07 Time Value of Money - BE ExercisesMUNDADA VENKATESH SURESH PGP 2019-21 BatchNo ratings yet

- SDFFDocument10 pagesSDFFNidhi AshokNo ratings yet

- Tutorial 2 Solutions S22019Document6 pagesTutorial 2 Solutions S22019Pingan LiNo ratings yet

- 02 - TVMDocument18 pages02 - TVMYOGINDRE V PAINo ratings yet

- Chapter 4Document40 pagesChapter 4SyedAunRazaRizviNo ratings yet

- Chapter 4Document40 pagesChapter 4SyedAunRazaRizviNo ratings yet

- Time Value of Money: Instructor: Ajab Khan BurkiDocument86 pagesTime Value of Money: Instructor: Ajab Khan BurkiGaurav KarkiNo ratings yet

- Personal Financial Planning 2nd Edition Altfest Solution ManualDocument71 pagesPersonal Financial Planning 2nd Edition Altfest Solution Manualcynthia100% (36)

- Enter Your Campus LocationDocument28 pagesEnter Your Campus LocationRidwaan JaffooNo ratings yet

- AnnuitiesDocument39 pagesAnnuitiesRaymart BulagsacNo ratings yet

- Time Value of MoneyDocument14 pagesTime Value of MoneyYasir AyazNo ratings yet

- Lec 4 FM NumlDocument17 pagesLec 4 FM Numlpal 8311No ratings yet

- Lecture6 Time Value of MoneyDocument18 pagesLecture6 Time Value of MoneyAbdurehman FaisalNo ratings yet

- Problems of FinanceDocument67 pagesProblems of FinanceTariqul IslamNo ratings yet

- ch4 IM 1EDocument21 pagesch4 IM 1EReginoSaynoValenzuelaNo ratings yet

- Lecture 2Document10 pagesLecture 2Na ViNo ratings yet

- FM - Lecture 2 - Time Value of Money PDFDocument82 pagesFM - Lecture 2 - Time Value of Money PDFMi ThưNo ratings yet

- Financial Managmen Van Horne 13th Edition Chapter 3 Time Value of MoneyDocument57 pagesFinancial Managmen Van Horne 13th Edition Chapter 3 Time Value of MoneyMirza4200% (1)

- MB - Group Assignent 1Document32 pagesMB - Group Assignent 1Doan BùiNo ratings yet

- Topic 2 SupplementaryDocument26 pagesTopic 2 SupplementaryManton YeungNo ratings yet

- Chapter 2 - Time Value of Money - ch02Document21 pagesChapter 2 - Time Value of Money - ch02ThuyDuong BuiNo ratings yet

- TVMDocument28 pagesTVMJay AnneNo ratings yet

- General Mathematics Q2 Week 4 1Document11 pagesGeneral Mathematics Q2 Week 4 1Santos, Mart Czendric Y.No ratings yet

- Final Exam Practice Papers SolutionsDocument31 pagesFinal Exam Practice Papers Solutionssamuel ngNo ratings yet

- Time Value of MoneyDocument87 pagesTime Value of Moneysaad azamNo ratings yet

- Exercises - Lecture 7 (A)Document7 pagesExercises - Lecture 7 (A)Samuel ChunNo ratings yet

- Personal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyFrom EverandPersonal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyNo ratings yet

- Valuation Chapter 4 FinManDocument40 pagesValuation Chapter 4 FinManSteven Kyle PeregrinoNo ratings yet

- Aircraft MaterialsDocument2 pagesAircraft MaterialsSteven Kyle PeregrinoNo ratings yet

- Risk and Return Chapter 5 FinManDocument51 pagesRisk and Return Chapter 5 FinManSteven Kyle PeregrinoNo ratings yet

- Limited Partnership - Grp. 4Document29 pagesLimited Partnership - Grp. 4Steven Kyle PeregrinoNo ratings yet

- INCOTERMSDocument2 pagesINCOTERMSSteven Kyle PeregrinoNo ratings yet

- Natural Hazard-WPS OfficeDocument3 pagesNatural Hazard-WPS OfficeSteven Kyle PeregrinoNo ratings yet

- Balance of Payment Adjustment - Akila WeerapanaDocument4 pagesBalance of Payment Adjustment - Akila WeerapanacitadNo ratings yet

- Exercises Short ProblemsDocument6 pagesExercises Short ProblemsKlaire SwswswsNo ratings yet

- General Ordinary AnnuitiesDocument3 pagesGeneral Ordinary Annuitiesstudent.devyankgosainNo ratings yet

- Present Worth Method of Comparison Lecture 7&8Document20 pagesPresent Worth Method of Comparison Lecture 7&8Hammad SattiNo ratings yet

- @@bond &bond Valuation-4!24!21Document37 pages@@bond &bond Valuation-4!24!21Mark LesterNo ratings yet

- Digital PaymentsDocument57 pagesDigital PaymentsArjun VkNo ratings yet

- FRM Final ProjectDocument5 pagesFRM Final ProjectOkasha AliNo ratings yet

- E-Handout On Audit of Cash and Cash EquivalentsDocument12 pagesE-Handout On Audit of Cash and Cash EquivalentsAsnifah AlinorNo ratings yet

- CFP Introduction To Financial Planning Practice Book SampleDocument35 pagesCFP Introduction To Financial Planning Practice Book SampleMeenakshi100% (1)

- BARBED WIRe DPRDocument22 pagesBARBED WIRe DPRGateway ComputersNo ratings yet

- Blockchain and Crypto in PaymentsDocument16 pagesBlockchain and Crypto in PaymentsforcetenNo ratings yet

- Export-Import: Module - 5 RiskDocument18 pagesExport-Import: Module - 5 RiskabhanidharaNo ratings yet

- Bonds PayableDocument2 pagesBonds PayableanonymousjoeyNo ratings yet

- 20MEV3CA Venture FinancingDocument107 pages20MEV3CA Venture FinancingsrinivasanscribdNo ratings yet

- Pdic-Example ComputationDocument9 pagesPdic-Example ComputationAndrei Nicole RiveraNo ratings yet

- Live Trading Session With Rishikesh SirDocument6 pagesLive Trading Session With Rishikesh SirYash GangwalNo ratings yet

- Unit 3-Time Value of MoneyDocument12 pagesUnit 3-Time Value of MoneyGizaw BelayNo ratings yet

- Summary of Accounts: Contacting UsDocument3 pagesSummary of Accounts: Contacting Ussiva AwaraNo ratings yet

- Apr 2023 SouthlandDocument2 pagesApr 2023 Southlandsufyan meerNo ratings yet

- Monetary Policy and Central Banking - Finance 7 SyllabusDocument9 pagesMonetary Policy and Central Banking - Finance 7 SyllabusMarjon DimafilisNo ratings yet

- Credit Management of JBL Final PDFDocument39 pagesCredit Management of JBL Final PDFmili dattaNo ratings yet

- SynopsisDocument20 pagesSynopsisJeetu VermaNo ratings yet

- Zimbabwe School Examinations Council Principles of Accounting 4051/2Document12 pagesZimbabwe School Examinations Council Principles of Accounting 4051/2Ryan HowesNo ratings yet

- SILIVERU SHIVAKUMAR A Study On Rural Banking - SBIDocument19 pagesSILIVERU SHIVAKUMAR A Study On Rural Banking - SBIkizieNo ratings yet

- InvoiceDocument1 pageInvoiceNikhil SinghNo ratings yet

- 18 007004 PDFDocument206 pages18 007004 PDFBrenda HerringNo ratings yet

- 13 (D) Ericsson Telecommunications, Inc. vs. City of PasigDocument2 pages13 (D) Ericsson Telecommunications, Inc. vs. City of PasigGoodyNo ratings yet

- The Philippine Financial System ReportDocument28 pagesThe Philippine Financial System Reportvalerie joy camemoNo ratings yet

Download as pptx, pdf, or txt

You might also like

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2024 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2024 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- Financial Management For Public Health and Not-For-Profit Organizations 4th Edition Finkler Solutions Manual DownloadDocument10 pagesFinancial Management For Public Health and Not-For-Profit Organizations 4th Edition Finkler Solutions Manual DownloadPeter Baker100% (25)

- CH 3 SolutionsDocument12 pagesCH 3 SolutionsLucia100% (3)

- AGC Guide To Construction Financing 2nd EditionDocument26 pagesAGC Guide To Construction Financing 2nd EditionCitizen Kwadwo Ansong100% (1)

- EBS (Electronic Bank Statement) - Not Clearing Automatically in FIDocument7 pagesEBS (Electronic Bank Statement) - Not Clearing Automatically in FIKiran KumarNo ratings yet

- Annuity 1Document36 pagesAnnuity 1Mahnoor ZainabNo ratings yet

- Time Value of MoneyDocument46 pagesTime Value of Moneyanum iftikha100% (1)

- REAL 4000 Ch3 HW SolutionsDocument6 pagesREAL 4000 Ch3 HW SolutionsnunyabiznessNo ratings yet

- Time Value of Money Using Excel Time Value of Money Using TI BA II PlusDocument21 pagesTime Value of Money Using Excel Time Value of Money Using TI BA II Plusautocrats 207No ratings yet

- Future Value: FV PV (1 + R) N PV FV / (1 +R) NDocument64 pagesFuture Value: FV PV (1 + R) N PV FV / (1 +R) NShlokNo ratings yet

- FM Lecture 2 Time Value of Money S2 2020.21Document75 pagesFM Lecture 2 Time Value of Money S2 2020.21Quỳnh NguyễnNo ratings yet

- MSL 708 Financial Management Topic 1a: Time Value of Money: Topics (Tentative) : Pre-Readings (BM Chapters)Document15 pagesMSL 708 Financial Management Topic 1a: Time Value of Money: Topics (Tentative) : Pre-Readings (BM Chapters)sasidhar naidu SiripurapuNo ratings yet

- Adobe Scan 23 Nov 2023Document12 pagesAdobe Scan 23 Nov 2023mahakc1110No ratings yet

- Time - Value - of - Money SampleDocument8 pagesTime - Value - of - Money SampleHassleBustNo ratings yet

- Chap 004Document46 pagesChap 004NazifahNo ratings yet

- 2 Time Value of MoneyDocument46 pages2 Time Value of MoneyABHINAV AGRAWALNo ratings yet

- Time Value of Money: DR. Mohamed SamehDocument22 pagesTime Value of Money: DR. Mohamed SamehRamadan IbrahemNo ratings yet

- TVM (FM)Document77 pagesTVM (FM)24 kunal bhojankarNo ratings yet

- 3b Accounting and the Time Value of Money (1)Document37 pages3b Accounting and the Time Value of Money (1)Yandi AriefNo ratings yet

- MAF759: Analytical MethodsDocument42 pagesMAF759: Analytical MethodshieuduyNo ratings yet

- Chapter 2 - How To Calculate Present ValuesDocument21 pagesChapter 2 - How To Calculate Present ValuesTrọng PhạmNo ratings yet

- Time Value of MoneyDocument74 pagesTime Value of MoneybusebeeNo ratings yet

- Time Value of MoneyDocument95 pagesTime Value of MoneyKalkayeNo ratings yet

- Fin 2200 Sum 07 MTDocument12 pagesFin 2200 Sum 07 MTSims LauNo ratings yet

- Financial Managment Chapter 02 PART 1Document41 pagesFinancial Managment Chapter 02 PART 1MISRA MUHUDINNo ratings yet

- Exam Practice QuestionsDocument6 pagesExam Practice Questionssir bookkeeperNo ratings yet

- Net Present Value: Corporate FinanceDocument38 pagesNet Present Value: Corporate FinanceNguyễn Thùy LinhNo ratings yet

- CHPT 4Document41 pagesCHPT 4ferahNo ratings yet

- IAChap 006 PPTDocument39 pagesIAChap 006 PPTلين صبحNo ratings yet

- LM01 Time Value of MoneyDocument48 pagesLM01 Time Value of Moneymenexe9137No ratings yet

- PresTheme2-Eng-Time Value of MoneyDocument39 pagesPresTheme2-Eng-Time Value of MoneyKristina PekovaNo ratings yet

- Kewirausahaan Konsep-Konsep Keuangan: Dteti 2021Document27 pagesKewirausahaan Konsep-Konsep Keuangan: Dteti 2021PANDHU ARDI PRASETYONo ratings yet

- M4 TVMDocument87 pagesM4 TVMAnonymousWriter348No ratings yet

- Time Value of Money Time Value of MoneyDocument29 pagesTime Value of Money Time Value of MoneyEunice Dimple CaliwagNo ratings yet

- 07 Time Value of Money - BE ExercisesDocument26 pages07 Time Value of Money - BE ExercisesMUNDADA VENKATESH SURESH PGP 2019-21 BatchNo ratings yet

- SDFFDocument10 pagesSDFFNidhi AshokNo ratings yet

- Tutorial 2 Solutions S22019Document6 pagesTutorial 2 Solutions S22019Pingan LiNo ratings yet

- 02 - TVMDocument18 pages02 - TVMYOGINDRE V PAINo ratings yet

- Chapter 4Document40 pagesChapter 4SyedAunRazaRizviNo ratings yet

- Chapter 4Document40 pagesChapter 4SyedAunRazaRizviNo ratings yet

- Time Value of Money: Instructor: Ajab Khan BurkiDocument86 pagesTime Value of Money: Instructor: Ajab Khan BurkiGaurav KarkiNo ratings yet

- Personal Financial Planning 2nd Edition Altfest Solution ManualDocument71 pagesPersonal Financial Planning 2nd Edition Altfest Solution Manualcynthia100% (36)

- Enter Your Campus LocationDocument28 pagesEnter Your Campus LocationRidwaan JaffooNo ratings yet

- AnnuitiesDocument39 pagesAnnuitiesRaymart BulagsacNo ratings yet

- Time Value of MoneyDocument14 pagesTime Value of MoneyYasir AyazNo ratings yet

- Lec 4 FM NumlDocument17 pagesLec 4 FM Numlpal 8311No ratings yet

- Lecture6 Time Value of MoneyDocument18 pagesLecture6 Time Value of MoneyAbdurehman FaisalNo ratings yet

- Problems of FinanceDocument67 pagesProblems of FinanceTariqul IslamNo ratings yet

- ch4 IM 1EDocument21 pagesch4 IM 1EReginoSaynoValenzuelaNo ratings yet

- Lecture 2Document10 pagesLecture 2Na ViNo ratings yet

- FM - Lecture 2 - Time Value of Money PDFDocument82 pagesFM - Lecture 2 - Time Value of Money PDFMi ThưNo ratings yet

- Financial Managmen Van Horne 13th Edition Chapter 3 Time Value of MoneyDocument57 pagesFinancial Managmen Van Horne 13th Edition Chapter 3 Time Value of MoneyMirza4200% (1)

- MB - Group Assignent 1Document32 pagesMB - Group Assignent 1Doan BùiNo ratings yet

- Topic 2 SupplementaryDocument26 pagesTopic 2 SupplementaryManton YeungNo ratings yet

- Chapter 2 - Time Value of Money - ch02Document21 pagesChapter 2 - Time Value of Money - ch02ThuyDuong BuiNo ratings yet

- TVMDocument28 pagesTVMJay AnneNo ratings yet

- General Mathematics Q2 Week 4 1Document11 pagesGeneral Mathematics Q2 Week 4 1Santos, Mart Czendric Y.No ratings yet

- Final Exam Practice Papers SolutionsDocument31 pagesFinal Exam Practice Papers Solutionssamuel ngNo ratings yet

- Time Value of MoneyDocument87 pagesTime Value of Moneysaad azamNo ratings yet

- Exercises - Lecture 7 (A)Document7 pagesExercises - Lecture 7 (A)Samuel ChunNo ratings yet

- Personal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyFrom EverandPersonal Money Management Made Simple with MS Excel: How to save, invest and borrow wiselyNo ratings yet

- Valuation Chapter 4 FinManDocument40 pagesValuation Chapter 4 FinManSteven Kyle PeregrinoNo ratings yet

- Aircraft MaterialsDocument2 pagesAircraft MaterialsSteven Kyle PeregrinoNo ratings yet

- Risk and Return Chapter 5 FinManDocument51 pagesRisk and Return Chapter 5 FinManSteven Kyle PeregrinoNo ratings yet

- Limited Partnership - Grp. 4Document29 pagesLimited Partnership - Grp. 4Steven Kyle PeregrinoNo ratings yet

- INCOTERMSDocument2 pagesINCOTERMSSteven Kyle PeregrinoNo ratings yet

- Natural Hazard-WPS OfficeDocument3 pagesNatural Hazard-WPS OfficeSteven Kyle PeregrinoNo ratings yet

- Balance of Payment Adjustment - Akila WeerapanaDocument4 pagesBalance of Payment Adjustment - Akila WeerapanacitadNo ratings yet

- Exercises Short ProblemsDocument6 pagesExercises Short ProblemsKlaire SwswswsNo ratings yet

- General Ordinary AnnuitiesDocument3 pagesGeneral Ordinary Annuitiesstudent.devyankgosainNo ratings yet

- Present Worth Method of Comparison Lecture 7&8Document20 pagesPresent Worth Method of Comparison Lecture 7&8Hammad SattiNo ratings yet

- @@bond &bond Valuation-4!24!21Document37 pages@@bond &bond Valuation-4!24!21Mark LesterNo ratings yet

- Digital PaymentsDocument57 pagesDigital PaymentsArjun VkNo ratings yet

- FRM Final ProjectDocument5 pagesFRM Final ProjectOkasha AliNo ratings yet

- E-Handout On Audit of Cash and Cash EquivalentsDocument12 pagesE-Handout On Audit of Cash and Cash EquivalentsAsnifah AlinorNo ratings yet

- CFP Introduction To Financial Planning Practice Book SampleDocument35 pagesCFP Introduction To Financial Planning Practice Book SampleMeenakshi100% (1)

- BARBED WIRe DPRDocument22 pagesBARBED WIRe DPRGateway ComputersNo ratings yet

- Blockchain and Crypto in PaymentsDocument16 pagesBlockchain and Crypto in PaymentsforcetenNo ratings yet

- Export-Import: Module - 5 RiskDocument18 pagesExport-Import: Module - 5 RiskabhanidharaNo ratings yet

- Bonds PayableDocument2 pagesBonds PayableanonymousjoeyNo ratings yet

- 20MEV3CA Venture FinancingDocument107 pages20MEV3CA Venture FinancingsrinivasanscribdNo ratings yet

- Pdic-Example ComputationDocument9 pagesPdic-Example ComputationAndrei Nicole RiveraNo ratings yet

- Live Trading Session With Rishikesh SirDocument6 pagesLive Trading Session With Rishikesh SirYash GangwalNo ratings yet

- Unit 3-Time Value of MoneyDocument12 pagesUnit 3-Time Value of MoneyGizaw BelayNo ratings yet

- Summary of Accounts: Contacting UsDocument3 pagesSummary of Accounts: Contacting Ussiva AwaraNo ratings yet

- Apr 2023 SouthlandDocument2 pagesApr 2023 Southlandsufyan meerNo ratings yet

- Monetary Policy and Central Banking - Finance 7 SyllabusDocument9 pagesMonetary Policy and Central Banking - Finance 7 SyllabusMarjon DimafilisNo ratings yet

- Credit Management of JBL Final PDFDocument39 pagesCredit Management of JBL Final PDFmili dattaNo ratings yet

- SynopsisDocument20 pagesSynopsisJeetu VermaNo ratings yet

- Zimbabwe School Examinations Council Principles of Accounting 4051/2Document12 pagesZimbabwe School Examinations Council Principles of Accounting 4051/2Ryan HowesNo ratings yet

- SILIVERU SHIVAKUMAR A Study On Rural Banking - SBIDocument19 pagesSILIVERU SHIVAKUMAR A Study On Rural Banking - SBIkizieNo ratings yet

- InvoiceDocument1 pageInvoiceNikhil SinghNo ratings yet

- 18 007004 PDFDocument206 pages18 007004 PDFBrenda HerringNo ratings yet

- 13 (D) Ericsson Telecommunications, Inc. vs. City of PasigDocument2 pages13 (D) Ericsson Telecommunications, Inc. vs. City of PasigGoodyNo ratings yet

- The Philippine Financial System ReportDocument28 pagesThe Philippine Financial System Reportvalerie joy camemoNo ratings yet