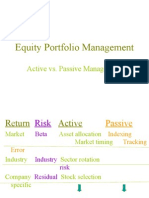

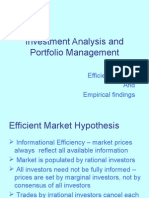

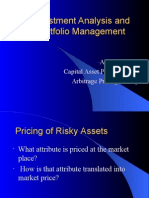

6560 Lecture

6560 Lecture

You might also like

- The ICT London Close KillzoneDocument3 pagesThe ICT London Close Killzonehuda EcharkaouiNo ratings yet

- Black Book PDFDocument62 pagesBlack Book PDFfaik100% (1)

- The Art of Japanese Candlestick Charting Summary PDFDocument24 pagesThe Art of Japanese Candlestick Charting Summary PDFelbronNo ratings yet

- Acegazettepriceaction Supplyanddemand 140117194309 Phpapp01Document41 pagesAcegazettepriceaction Supplyanddemand 140117194309 Phpapp01Panneer Selvam Easwaran100% (1)

- Audited P&L TrendsDocument1 pageAudited P&L Trendsapi-3699305No ratings yet

- Day 5 Task (Bop Cad FD)Document11 pagesDay 5 Task (Bop Cad FD)ashish sunnyNo ratings yet

- EU: Articles of Stationery - Market Report. Analysis and Forecast To 2020Document9 pagesEU: Articles of Stationery - Market Report. Analysis and Forecast To 2020IndexBox MarketingNo ratings yet

- Technical ResearchDocument30 pagesTechnical Researchamit_idea1No ratings yet

- 19 - 7-PDF - Wiley CandleStick and Pivot Point Trading TriggersDocument1 page19 - 7-PDF - Wiley CandleStick and Pivot Point Trading TriggersPranayNo ratings yet

- Technical Analysis: Power Tools For Active Investors: Click HereDocument5 pagesTechnical Analysis: Power Tools For Active Investors: Click HereMashahir AhmedNo ratings yet

- Moving Average Convergence DivergenceDocument3 pagesMoving Average Convergence DivergenceNikita DubeyNo ratings yet

- Ichimoku Kinko Hyo Trading PDF .DownloadDocument13 pagesIchimoku Kinko Hyo Trading PDF .DownloadMuraliNo ratings yet

- Chart Nexus ManualDocument161 pagesChart Nexus Manualsriharsha777No ratings yet

- Pattern Recognition and Candlesticks by WagnerDocument11 pagesPattern Recognition and Candlesticks by WagnerMohammadkhodaeiNo ratings yet

- TechAnalysis InvestopediaDocument14 pagesTechAnalysis InvestopediaCristian FilipNo ratings yet

- Support Gap Up: Bullish ConfirmationDocument6 pagesSupport Gap Up: Bullish ConfirmationScott LuNo ratings yet

- Logical Profits ManualDocument11 pagesLogical Profits ManualCapitanu IulianNo ratings yet

- ReversalCandlestickVietnam Updated PDFDocument7 pagesReversalCandlestickVietnam Updated PDFdanielNo ratings yet

- Freescalpingindicator PDFDocument7 pagesFreescalpingindicator PDFhandi supraNo ratings yet

- The Dow Powers Above Its 200-Day Simple Moving Average at 10,321Document5 pagesThe Dow Powers Above Its 200-Day Simple Moving Average at 10,321ValuEngine.comNo ratings yet

- Technical Analysis EngineeringDocument8 pagesTechnical Analysis EngineeringAbhinav AroraNo ratings yet

- Stochastic Oscillator: WhereDocument3 pagesStochastic Oscillator: WhereNAYIB MNo ratings yet

- Savvy MACD IndicatorDocument10 pagesSavvy MACD IndicatorCapitanu IulianNo ratings yet

- The 5 Most Powerful Candlestick Patterns (NUAN, GMCR) - InvestopediaDocument6 pagesThe 5 Most Powerful Candlestick Patterns (NUAN, GMCR) - InvestopediaMax Rene Velazquez GarciaNo ratings yet

- SDRC2 ORpostsDocument133 pagesSDRC2 ORpostsNg Tiong YewNo ratings yet

- Trading Systems IndicatorsDocument3 pagesTrading Systems IndicatorsKam MusNo ratings yet

- Heikin AshiDocument3 pagesHeikin AshiYudha Wijaya50% (4)

- Bulls Eye Trading Academy - Basic Course1Document15 pagesBulls Eye Trading Academy - Basic Course1Sanjay DubeyNo ratings yet

- Trading Logic Technical Indicators v1Document26 pagesTrading Logic Technical Indicators v1myturtle gameNo ratings yet

- Support & ResistanceDocument8 pagesSupport & Resistanceanalyst_anil14No ratings yet

- Jacko Trading StyleDocument25 pagesJacko Trading StyleMohammed NizamNo ratings yet

- The Next Apple ChecklistDocument7 pagesThe Next Apple ChecklistShubham siddhpuriaNo ratings yet

- Moda Trendus ManualDocument9 pagesModa Trendus ManualCapitanu IulianNo ratings yet

- Moving Average Trading Rules For NASDAQ Composite PDFDocument13 pagesMoving Average Trading Rules For NASDAQ Composite PDFKatlego MalulekaNo ratings yet

- Technical Analysis: Dr. Pankaj K AgarwalDocument58 pagesTechnical Analysis: Dr. Pankaj K AgarwalAnshul GuptaNo ratings yet

- Consolidation Patterns: by Melanie F. Bowman and Thom HartleDocument7 pagesConsolidation Patterns: by Melanie F. Bowman and Thom HartleFetogNo ratings yet

- The Disciplined Trader ScheduleDocument11 pagesThe Disciplined Trader Schedulemara saleNo ratings yet

- Bollinger Bands: Bollinger Bands and The Related Indicators %B and Bandwidth AreDocument4 pagesBollinger Bands: Bollinger Bands and The Related Indicators %B and Bandwidth AresrikanthpoonaNo ratings yet

- What The MACD Indicator Is and How It WorksDocument6 pagesWhat The MACD Indicator Is and How It WorksAkingbemi MorakinyoNo ratings yet

- The Most Enlightening Technical Analysis Seminar, Advanced Market Timing Experts Workshop 2011Document8 pagesThe Most Enlightening Technical Analysis Seminar, Advanced Market Timing Experts Workshop 2011Golden NetworkingNo ratings yet

- Technical Analysis of Usdcad CurrencyDocument58 pagesTechnical Analysis of Usdcad CurrencyDhanalakshmi SelvarajNo ratings yet

- Calculating Retracement and Projection LevelsDocument9 pagesCalculating Retracement and Projection LevelsAndre SetiawanNo ratings yet

- An Introduction To Japanese Candlestick ChartingDocument14 pagesAn Introduction To Japanese Candlestick ChartingRomelu MartialNo ratings yet

- 7 EntryDocument87 pages7 EntryAlfis OzilNo ratings yet

- Ultimate Charting ManualDocument114 pagesUltimate Charting ManualChaudaryWaqasIsrar100% (1)

- Rotational Trading Using The %B Oscillator: February 2007Document16 pagesRotational Trading Using The %B Oscillator: February 2007eduardoNo ratings yet

- 5 6165764460687393021 PDFDocument13 pages5 6165764460687393021 PDFmannimanojNo ratings yet

- Plan 415Document20 pagesPlan 415Eduardo Dutra100% (1)

- IntroductiontoTechnicalAnalysisandChartingwww - Nooreshtech.co .In 2 PDFDocument28 pagesIntroductiontoTechnicalAnalysisandChartingwww - Nooreshtech.co .In 2 PDFrohitNo ratings yet

- How To Dominate in The FX MarketDocument147 pagesHow To Dominate in The FX MarketGeorgeNo ratings yet

- Lifespan Investing: Building the Best Portfolio for Every Stage of Your LifeFrom EverandLifespan Investing: Building the Best Portfolio for Every Stage of Your LifeNo ratings yet

- Hikkake Set UpDocument5 pagesHikkake Set UpGed WardNo ratings yet

- FibnocciDocument30 pagesFibnoccipraveenrajNo ratings yet

- Technical AnalyyysisDocument95 pagesTechnical AnalyyysisSoumya Ranjan PandaNo ratings yet

- Active Trading Online Manual 2012Document42 pagesActive Trading Online Manual 2012artus14No ratings yet

- Computer Analysis of The Futures MarketDocument34 pagesComputer Analysis of The Futures Marketteclas71No ratings yet

- Time Tested Classic Trading RulesDocument2 pagesTime Tested Classic Trading RulesMichael Mario100% (1)

- Swing Trading PivotDocument16 pagesSwing Trading Pivotshafiul azam shahinNo ratings yet

- Strength of The TrendDocument14 pagesStrength of The TrendDavid VenancioNo ratings yet

- 6123 TitlesDocument1 page6123 Titlesapi-3699305No ratings yet

- 6766 Merger Course06 BriefDocument2 pages6766 Merger Course06 Briefapi-3699305100% (1)

- 5850 Ec225 06 Class ScheduleDocument1 page5850 Ec225 06 Class Scheduleapi-3699305No ratings yet

- 5691 EC225CourseOutline06-07Document2 pages5691 EC225CourseOutline06-07api-3699305No ratings yet

- 6769 - Merger Lect 3Document21 pages6769 - Merger Lect 3api-3699305No ratings yet

- 6769 - Merger Lect 3Document21 pages6769 - Merger Lect 3api-3699305No ratings yet

- 6886 Valuation 2Document25 pages6886 Valuation 2api-3699305100% (1)

- 5691 EC225CourseOutline06-07Document2 pages5691 EC225CourseOutline06-07api-3699305No ratings yet

- 6772 - Lecture 5 IIMC M & ADocument23 pages6772 - Lecture 5 IIMC M & Aapi-3699305No ratings yet

- 6516 TechnicalDocument33 pages6516 Technicalapi-3699305No ratings yet

- A Smarter Computer To Pick Stocks: Microsoft Nasdaq Bill GatesDocument5 pagesA Smarter Computer To Pick Stocks: Microsoft Nasdaq Bill Gatesapi-3699305No ratings yet

- 6312 LectureDocument8 pages6312 Lectureapi-3699305No ratings yet

- IAPMDocument4 pagesIAPMapi-3699305No ratings yet

- 6242 LectureDocument10 pages6242 Lectureapi-3699305No ratings yet

- 6473 LectureDocument13 pages6473 Lectureapi-3699305No ratings yet

- 6205 LectureDocument27 pages6205 Lectureapi-3699305No ratings yet

- 6209 PagesDocument4 pages6209 Pagesapi-3699305No ratings yet

- 6058 Many2Document6 pages6058 Many2api-3699305No ratings yet

- 6124 LectureDocument8 pages6124 Lectureapi-3699305No ratings yet

- 6055 TwoDocument2 pages6055 Twoapi-3699305No ratings yet

- 6057 TwoDocument2 pages6057 Twoapi-3699305No ratings yet

- 6054 LecturesDocument13 pages6054 Lecturesapi-3699305No ratings yet

- D S P Merrill Lynch LTD.: 1. Net WorthDocument2 pagesD S P Merrill Lynch LTD.: 1. Net Worthapi-3699305No ratings yet

- DSP Merrill Lynch LTD Industry:Securities/Commodities Trading ServicesDocument8 pagesDSP Merrill Lynch LTD Industry:Securities/Commodities Trading Servicesapi-3699305No ratings yet

- 6053 LecturesDocument17 pages6053 Lecturesapi-3699305No ratings yet

- Macro Essay PlansDocument9 pagesMacro Essay PlansLucas JonasNo ratings yet

- PIF IFC PresentationDocument9 pagesPIF IFC PresentationFarhan A KhanNo ratings yet

- SS en 934-6-2008 (2015)Document16 pagesSS en 934-6-2008 (2015)Heyson JayNo ratings yet

- StatisticalSummary1952 1957 PDFDocument388 pagesStatisticalSummary1952 1957 PDFTHE FORUMNo ratings yet

- ASUD Philippines Planned City Extension - Silay CityDocument4 pagesASUD Philippines Planned City Extension - Silay CityUNHabitatPhilippinesNo ratings yet

- Hpas Solved Paper v1.2 PDFDocument297 pagesHpas Solved Paper v1.2 PDFSpartanRana0% (1)

- Zee Power SolutionDocument7 pagesZee Power SolutionMuhammad ZahidNo ratings yet

- Tech Lesson Gala RadinovicDocument14 pagesTech Lesson Gala Radinovicapi-316211811No ratings yet

- 2.7 - Hunt, Geoffrey - Gramsci, Civil Society and Bureaucracy (En)Document15 pages2.7 - Hunt, Geoffrey - Gramsci, Civil Society and Bureaucracy (En)Johann Vessant RoigNo ratings yet

- Unwto Tourism Highlights: 2018 EditionDocument20 pagesUnwto Tourism Highlights: 2018 Editionкристина раджабоваNo ratings yet

- July 2023 Lets Talk Avon HyperlinkDocument52 pagesJuly 2023 Lets Talk Avon HyperlinkLeonNo ratings yet

- Alphaex Capital Candlestick Pattern Cheat Sheet InfographDocument1 pageAlphaex Capital Candlestick Pattern Cheat Sheet InfographAlfian Amin100% (1)

- Statement For Aug 18, 2023Document1 pageStatement For Aug 18, 2023Hawa KabiaNo ratings yet

- Energy Stability and SustainabilityDocument614 pagesEnergy Stability and SustainabilityΆσου ΝάνταNo ratings yet

- BOP and XMasTreeDocument1 pageBOP and XMasTreeo_tostaNo ratings yet

- Poverty and UnemploymentDocument10 pagesPoverty and UnemploymentJOSEPH HERBERT MABELNo ratings yet

- Macarena Gomezbarris The Extractive Zone Social Ecologies and Decolonial PerspectivesDocument209 pagesMacarena Gomezbarris The Extractive Zone Social Ecologies and Decolonial PerspectivesNina Hoechtl100% (2)

- Empirical Study of Indian Stock MarketDocument85 pagesEmpirical Study of Indian Stock Marketlokesh_045100% (1)

- Brooks and WohlforthDocument15 pagesBrooks and WohlforthjaserificNo ratings yet

- 11 ECO 08 Introduction To Index NumberDocument4 pages11 ECO 08 Introduction To Index NumberFebin Kurian FrancisNo ratings yet

- IFPRI Research PaperDocument36 pagesIFPRI Research Paperrajaji63No ratings yet

- Four Weapons of The RBI-1Document14 pagesFour Weapons of The RBI-1yashjadhav08No ratings yet

- TSF External Apr 2022 Junior Engineer TSF ENGDocument2 pagesTSF External Apr 2022 Junior Engineer TSF ENGMuhammad DandyNo ratings yet

- Continuation PatternDocument17 pagesContinuation Patternswetha reddy100% (1)

- Introduction and Ideas and Theories of Economic DevelopmentDocument61 pagesIntroduction and Ideas and Theories of Economic DevelopmentDenice Benzene SampangNo ratings yet

- 2013 Defeasance AnalysisDocument1 page2013 Defeasance AnalysisPennLiveNo ratings yet

- On Banking Sector For PresentationDocument23 pagesOn Banking Sector For Presentationvaishali haritNo ratings yet

Download as ppt, pdf, or txt

You might also like

- The ICT London Close KillzoneDocument3 pagesThe ICT London Close Killzonehuda EcharkaouiNo ratings yet

- Black Book PDFDocument62 pagesBlack Book PDFfaik100% (1)

- The Art of Japanese Candlestick Charting Summary PDFDocument24 pagesThe Art of Japanese Candlestick Charting Summary PDFelbronNo ratings yet

- Acegazettepriceaction Supplyanddemand 140117194309 Phpapp01Document41 pagesAcegazettepriceaction Supplyanddemand 140117194309 Phpapp01Panneer Selvam Easwaran100% (1)

- Audited P&L TrendsDocument1 pageAudited P&L Trendsapi-3699305No ratings yet

- Day 5 Task (Bop Cad FD)Document11 pagesDay 5 Task (Bop Cad FD)ashish sunnyNo ratings yet

- EU: Articles of Stationery - Market Report. Analysis and Forecast To 2020Document9 pagesEU: Articles of Stationery - Market Report. Analysis and Forecast To 2020IndexBox MarketingNo ratings yet

- Technical ResearchDocument30 pagesTechnical Researchamit_idea1No ratings yet

- 19 - 7-PDF - Wiley CandleStick and Pivot Point Trading TriggersDocument1 page19 - 7-PDF - Wiley CandleStick and Pivot Point Trading TriggersPranayNo ratings yet

- Technical Analysis: Power Tools For Active Investors: Click HereDocument5 pagesTechnical Analysis: Power Tools For Active Investors: Click HereMashahir AhmedNo ratings yet

- Moving Average Convergence DivergenceDocument3 pagesMoving Average Convergence DivergenceNikita DubeyNo ratings yet

- Ichimoku Kinko Hyo Trading PDF .DownloadDocument13 pagesIchimoku Kinko Hyo Trading PDF .DownloadMuraliNo ratings yet

- Chart Nexus ManualDocument161 pagesChart Nexus Manualsriharsha777No ratings yet

- Pattern Recognition and Candlesticks by WagnerDocument11 pagesPattern Recognition and Candlesticks by WagnerMohammadkhodaeiNo ratings yet

- TechAnalysis InvestopediaDocument14 pagesTechAnalysis InvestopediaCristian FilipNo ratings yet

- Support Gap Up: Bullish ConfirmationDocument6 pagesSupport Gap Up: Bullish ConfirmationScott LuNo ratings yet

- Logical Profits ManualDocument11 pagesLogical Profits ManualCapitanu IulianNo ratings yet

- ReversalCandlestickVietnam Updated PDFDocument7 pagesReversalCandlestickVietnam Updated PDFdanielNo ratings yet

- Freescalpingindicator PDFDocument7 pagesFreescalpingindicator PDFhandi supraNo ratings yet

- The Dow Powers Above Its 200-Day Simple Moving Average at 10,321Document5 pagesThe Dow Powers Above Its 200-Day Simple Moving Average at 10,321ValuEngine.comNo ratings yet

- Technical Analysis EngineeringDocument8 pagesTechnical Analysis EngineeringAbhinav AroraNo ratings yet

- Stochastic Oscillator: WhereDocument3 pagesStochastic Oscillator: WhereNAYIB MNo ratings yet

- Savvy MACD IndicatorDocument10 pagesSavvy MACD IndicatorCapitanu IulianNo ratings yet

- The 5 Most Powerful Candlestick Patterns (NUAN, GMCR) - InvestopediaDocument6 pagesThe 5 Most Powerful Candlestick Patterns (NUAN, GMCR) - InvestopediaMax Rene Velazquez GarciaNo ratings yet

- SDRC2 ORpostsDocument133 pagesSDRC2 ORpostsNg Tiong YewNo ratings yet

- Trading Systems IndicatorsDocument3 pagesTrading Systems IndicatorsKam MusNo ratings yet

- Heikin AshiDocument3 pagesHeikin AshiYudha Wijaya50% (4)

- Bulls Eye Trading Academy - Basic Course1Document15 pagesBulls Eye Trading Academy - Basic Course1Sanjay DubeyNo ratings yet

- Trading Logic Technical Indicators v1Document26 pagesTrading Logic Technical Indicators v1myturtle gameNo ratings yet

- Support & ResistanceDocument8 pagesSupport & Resistanceanalyst_anil14No ratings yet

- Jacko Trading StyleDocument25 pagesJacko Trading StyleMohammed NizamNo ratings yet

- The Next Apple ChecklistDocument7 pagesThe Next Apple ChecklistShubham siddhpuriaNo ratings yet

- Moda Trendus ManualDocument9 pagesModa Trendus ManualCapitanu IulianNo ratings yet

- Moving Average Trading Rules For NASDAQ Composite PDFDocument13 pagesMoving Average Trading Rules For NASDAQ Composite PDFKatlego MalulekaNo ratings yet

- Technical Analysis: Dr. Pankaj K AgarwalDocument58 pagesTechnical Analysis: Dr. Pankaj K AgarwalAnshul GuptaNo ratings yet

- Consolidation Patterns: by Melanie F. Bowman and Thom HartleDocument7 pagesConsolidation Patterns: by Melanie F. Bowman and Thom HartleFetogNo ratings yet

- The Disciplined Trader ScheduleDocument11 pagesThe Disciplined Trader Schedulemara saleNo ratings yet

- Bollinger Bands: Bollinger Bands and The Related Indicators %B and Bandwidth AreDocument4 pagesBollinger Bands: Bollinger Bands and The Related Indicators %B and Bandwidth AresrikanthpoonaNo ratings yet

- What The MACD Indicator Is and How It WorksDocument6 pagesWhat The MACD Indicator Is and How It WorksAkingbemi MorakinyoNo ratings yet

- The Most Enlightening Technical Analysis Seminar, Advanced Market Timing Experts Workshop 2011Document8 pagesThe Most Enlightening Technical Analysis Seminar, Advanced Market Timing Experts Workshop 2011Golden NetworkingNo ratings yet

- Technical Analysis of Usdcad CurrencyDocument58 pagesTechnical Analysis of Usdcad CurrencyDhanalakshmi SelvarajNo ratings yet

- Calculating Retracement and Projection LevelsDocument9 pagesCalculating Retracement and Projection LevelsAndre SetiawanNo ratings yet

- An Introduction To Japanese Candlestick ChartingDocument14 pagesAn Introduction To Japanese Candlestick ChartingRomelu MartialNo ratings yet

- 7 EntryDocument87 pages7 EntryAlfis OzilNo ratings yet

- Ultimate Charting ManualDocument114 pagesUltimate Charting ManualChaudaryWaqasIsrar100% (1)

- Rotational Trading Using The %B Oscillator: February 2007Document16 pagesRotational Trading Using The %B Oscillator: February 2007eduardoNo ratings yet

- 5 6165764460687393021 PDFDocument13 pages5 6165764460687393021 PDFmannimanojNo ratings yet

- Plan 415Document20 pagesPlan 415Eduardo Dutra100% (1)

- IntroductiontoTechnicalAnalysisandChartingwww - Nooreshtech.co .In 2 PDFDocument28 pagesIntroductiontoTechnicalAnalysisandChartingwww - Nooreshtech.co .In 2 PDFrohitNo ratings yet

- How To Dominate in The FX MarketDocument147 pagesHow To Dominate in The FX MarketGeorgeNo ratings yet

- Lifespan Investing: Building the Best Portfolio for Every Stage of Your LifeFrom EverandLifespan Investing: Building the Best Portfolio for Every Stage of Your LifeNo ratings yet

- Hikkake Set UpDocument5 pagesHikkake Set UpGed WardNo ratings yet

- FibnocciDocument30 pagesFibnoccipraveenrajNo ratings yet

- Technical AnalyyysisDocument95 pagesTechnical AnalyyysisSoumya Ranjan PandaNo ratings yet

- Active Trading Online Manual 2012Document42 pagesActive Trading Online Manual 2012artus14No ratings yet

- Computer Analysis of The Futures MarketDocument34 pagesComputer Analysis of The Futures Marketteclas71No ratings yet

- Time Tested Classic Trading RulesDocument2 pagesTime Tested Classic Trading RulesMichael Mario100% (1)

- Swing Trading PivotDocument16 pagesSwing Trading Pivotshafiul azam shahinNo ratings yet

- Strength of The TrendDocument14 pagesStrength of The TrendDavid VenancioNo ratings yet

- 6123 TitlesDocument1 page6123 Titlesapi-3699305No ratings yet

- 6766 Merger Course06 BriefDocument2 pages6766 Merger Course06 Briefapi-3699305100% (1)

- 5850 Ec225 06 Class ScheduleDocument1 page5850 Ec225 06 Class Scheduleapi-3699305No ratings yet

- 5691 EC225CourseOutline06-07Document2 pages5691 EC225CourseOutline06-07api-3699305No ratings yet

- 6769 - Merger Lect 3Document21 pages6769 - Merger Lect 3api-3699305No ratings yet

- 6769 - Merger Lect 3Document21 pages6769 - Merger Lect 3api-3699305No ratings yet

- 6886 Valuation 2Document25 pages6886 Valuation 2api-3699305100% (1)

- 5691 EC225CourseOutline06-07Document2 pages5691 EC225CourseOutline06-07api-3699305No ratings yet

- 6772 - Lecture 5 IIMC M & ADocument23 pages6772 - Lecture 5 IIMC M & Aapi-3699305No ratings yet

- 6516 TechnicalDocument33 pages6516 Technicalapi-3699305No ratings yet

- A Smarter Computer To Pick Stocks: Microsoft Nasdaq Bill GatesDocument5 pagesA Smarter Computer To Pick Stocks: Microsoft Nasdaq Bill Gatesapi-3699305No ratings yet

- 6312 LectureDocument8 pages6312 Lectureapi-3699305No ratings yet

- IAPMDocument4 pagesIAPMapi-3699305No ratings yet

- 6242 LectureDocument10 pages6242 Lectureapi-3699305No ratings yet

- 6473 LectureDocument13 pages6473 Lectureapi-3699305No ratings yet

- 6205 LectureDocument27 pages6205 Lectureapi-3699305No ratings yet

- 6209 PagesDocument4 pages6209 Pagesapi-3699305No ratings yet

- 6058 Many2Document6 pages6058 Many2api-3699305No ratings yet

- 6124 LectureDocument8 pages6124 Lectureapi-3699305No ratings yet

- 6055 TwoDocument2 pages6055 Twoapi-3699305No ratings yet

- 6057 TwoDocument2 pages6057 Twoapi-3699305No ratings yet

- 6054 LecturesDocument13 pages6054 Lecturesapi-3699305No ratings yet

- D S P Merrill Lynch LTD.: 1. Net WorthDocument2 pagesD S P Merrill Lynch LTD.: 1. Net Worthapi-3699305No ratings yet

- DSP Merrill Lynch LTD Industry:Securities/Commodities Trading ServicesDocument8 pagesDSP Merrill Lynch LTD Industry:Securities/Commodities Trading Servicesapi-3699305No ratings yet

- 6053 LecturesDocument17 pages6053 Lecturesapi-3699305No ratings yet

- Macro Essay PlansDocument9 pagesMacro Essay PlansLucas JonasNo ratings yet

- PIF IFC PresentationDocument9 pagesPIF IFC PresentationFarhan A KhanNo ratings yet

- SS en 934-6-2008 (2015)Document16 pagesSS en 934-6-2008 (2015)Heyson JayNo ratings yet

- StatisticalSummary1952 1957 PDFDocument388 pagesStatisticalSummary1952 1957 PDFTHE FORUMNo ratings yet

- ASUD Philippines Planned City Extension - Silay CityDocument4 pagesASUD Philippines Planned City Extension - Silay CityUNHabitatPhilippinesNo ratings yet

- Hpas Solved Paper v1.2 PDFDocument297 pagesHpas Solved Paper v1.2 PDFSpartanRana0% (1)

- Zee Power SolutionDocument7 pagesZee Power SolutionMuhammad ZahidNo ratings yet

- Tech Lesson Gala RadinovicDocument14 pagesTech Lesson Gala Radinovicapi-316211811No ratings yet

- 2.7 - Hunt, Geoffrey - Gramsci, Civil Society and Bureaucracy (En)Document15 pages2.7 - Hunt, Geoffrey - Gramsci, Civil Society and Bureaucracy (En)Johann Vessant RoigNo ratings yet

- Unwto Tourism Highlights: 2018 EditionDocument20 pagesUnwto Tourism Highlights: 2018 Editionкристина раджабоваNo ratings yet

- July 2023 Lets Talk Avon HyperlinkDocument52 pagesJuly 2023 Lets Talk Avon HyperlinkLeonNo ratings yet

- Alphaex Capital Candlestick Pattern Cheat Sheet InfographDocument1 pageAlphaex Capital Candlestick Pattern Cheat Sheet InfographAlfian Amin100% (1)

- Statement For Aug 18, 2023Document1 pageStatement For Aug 18, 2023Hawa KabiaNo ratings yet

- Energy Stability and SustainabilityDocument614 pagesEnergy Stability and SustainabilityΆσου ΝάνταNo ratings yet

- BOP and XMasTreeDocument1 pageBOP and XMasTreeo_tostaNo ratings yet

- Poverty and UnemploymentDocument10 pagesPoverty and UnemploymentJOSEPH HERBERT MABELNo ratings yet

- Macarena Gomezbarris The Extractive Zone Social Ecologies and Decolonial PerspectivesDocument209 pagesMacarena Gomezbarris The Extractive Zone Social Ecologies and Decolonial PerspectivesNina Hoechtl100% (2)

- Empirical Study of Indian Stock MarketDocument85 pagesEmpirical Study of Indian Stock Marketlokesh_045100% (1)

- Brooks and WohlforthDocument15 pagesBrooks and WohlforthjaserificNo ratings yet

- 11 ECO 08 Introduction To Index NumberDocument4 pages11 ECO 08 Introduction To Index NumberFebin Kurian FrancisNo ratings yet

- IFPRI Research PaperDocument36 pagesIFPRI Research Paperrajaji63No ratings yet

- Four Weapons of The RBI-1Document14 pagesFour Weapons of The RBI-1yashjadhav08No ratings yet

- TSF External Apr 2022 Junior Engineer TSF ENGDocument2 pagesTSF External Apr 2022 Junior Engineer TSF ENGMuhammad DandyNo ratings yet

- Continuation PatternDocument17 pagesContinuation Patternswetha reddy100% (1)

- Introduction and Ideas and Theories of Economic DevelopmentDocument61 pagesIntroduction and Ideas and Theories of Economic DevelopmentDenice Benzene SampangNo ratings yet

- 2013 Defeasance AnalysisDocument1 page2013 Defeasance AnalysisPennLiveNo ratings yet

- On Banking Sector For PresentationDocument23 pagesOn Banking Sector For Presentationvaishali haritNo ratings yet