Download as pptx, pdf, or txt

You might also like

- Ebook Ebook PDF Purchasing Supply Chain Management 7th Edition PDFDocument41 pagesEbook Ebook PDF Purchasing Supply Chain Management 7th Edition PDFiona.curnutte249100% (45)

- Filipino Brand of Service ExcellenceDocument23 pagesFilipino Brand of Service Excellence2197378No ratings yet

- Creating Value Through Corporate Restructuring - 2012 - GilsonDocument827 pagesCreating Value Through Corporate Restructuring - 2012 - GilsondavidNo ratings yet

- ISL League RulesDocument43 pagesISL League RulesManoj Kashyap100% (2)

- Project Report ON Comparative Analysis of Financial Performance of Zomato: A Ratio Analysis ApproachDocument49 pagesProject Report ON Comparative Analysis of Financial Performance of Zomato: A Ratio Analysis Approachsudhanshu jeevtani100% (5)

- The UAE's Free Zones: UAE Business Setup GuidesDocument8 pagesThe UAE's Free Zones: UAE Business Setup GuidesGracia MayaNo ratings yet

- FINA2010 Financial Management: Lecture 3: Time Value of MoneyDocument65 pagesFINA2010 Financial Management: Lecture 3: Time Value of MoneyWai Lam HsuNo ratings yet

- Session 2 Time Value of MoneyDocument34 pagesSession 2 Time Value of MoneyRoshanNo ratings yet

- Introduction To Valuation: The Time Value of Money Chapter OutlineDocument10 pagesIntroduction To Valuation: The Time Value of Money Chapter OutlineEman SamirNo ratings yet

- FINA2010 Financial Management: Lecture 3: Time Value of MoneyDocument62 pagesFINA2010 Financial Management: Lecture 3: Time Value of MoneymoonNo ratings yet

- Teknologi Keuangan: Manajemen Rekayasa Fakultas Teknologi Industri IT DelDocument35 pagesTeknologi Keuangan: Manajemen Rekayasa Fakultas Teknologi Industri IT DelNatasya Romauli SilitongaNo ratings yet

- Lecture 2Document21 pagesLecture 2Samantha YuNo ratings yet

- Lesson 3. TVM 2020Document25 pagesLesson 3. TVM 2020Vĩ NguyễnNo ratings yet

- Reading: Capital BudgetingDocument32 pagesReading: Capital BudgetingKhánh VyNo ratings yet

- Time Value of Money Chapter 5Document78 pagesTime Value of Money Chapter 5herculesNo ratings yet

- Lectures 7,8,9,10 - POFDocument115 pagesLectures 7,8,9,10 - POFThảo Nhi LêNo ratings yet

- Fundamentals of Managerial EconomicsDocument32 pagesFundamentals of Managerial Economicsosama haseebNo ratings yet

- Discounted Cash Flow ValuationDocument31 pagesDiscounted Cash Flow ValuationJay Prakash MandalNo ratings yet

- Introduction To Valuation: The Time Value of MoneyDocument61 pagesIntroduction To Valuation: The Time Value of MoneyNimra RehmanNo ratings yet

- Time Value of MoneyDocument73 pagesTime Value of MoneyZeenat NoorNo ratings yet

- Time Value of Money: Present and Future ValueDocument29 pagesTime Value of Money: Present and Future ValuekateNo ratings yet

- Chapter 3 - FIN3004 - 2024Document99 pagesChapter 3 - FIN3004 - 2024luuthuydiem63No ratings yet

- Chapter 3 - FIN3004 - 2022Document109 pagesChapter 3 - FIN3004 - 2022Phương ThảoNo ratings yet

- Introduction To Valuation: The Time Value of Money: Rights Reserved Mcgraw-Hill/IrwinDocument12 pagesIntroduction To Valuation: The Time Value of Money: Rights Reserved Mcgraw-Hill/IrwinYasser MaamounNo ratings yet

- 02 The Meaning of Interest RatesDocument62 pages02 The Meaning of Interest RatesCatherine ChouNo ratings yet

- Time Value of Money: ObjectiveDocument9 pagesTime Value of Money: ObjectiveThuyển ThuyểnNo ratings yet

- Introduction To Valuation: The Time Value of MoneyDocument32 pagesIntroduction To Valuation: The Time Value of MoneyYannah HidalgoNo ratings yet

- Time Value of Money: All Rights ReservedDocument79 pagesTime Value of Money: All Rights ReservedBilal SahuNo ratings yet

- 2023 Time Value of MoneyDocument81 pages2023 Time Value of Moneylynthehunkyapple205No ratings yet

- 1 Time Value of MoneyDocument24 pages1 Time Value of MoneyGeckoNo ratings yet

- The Time Value of Money: Mike Shaffer April 15, 2005Document23 pagesThe Time Value of Money: Mike Shaffer April 15, 2005Ritika SinghNo ratings yet

- Chapter Four: Future Value, Present Value, and Interest RatesDocument40 pagesChapter Four: Future Value, Present Value, and Interest RatesStive BrackNo ratings yet

- Session 10: Unit II: Time Value of MoneyDocument49 pagesSession 10: Unit II: Time Value of MoneySamia ElsayedNo ratings yet

- Chapter 4. Time Value of MoneyDocument49 pagesChapter 4. Time Value of MoneySơn Đặng TháiNo ratings yet

- Introduction To Valuation: The Time Value of MoneyDocument48 pagesIntroduction To Valuation: The Time Value of MoneyNurul SafrinaNo ratings yet

- Chapter 4. Time Value of MoneyDocument49 pagesChapter 4. Time Value of MoneyThu PhươngNo ratings yet

- Time Value of Money Lecture NotesDocument51 pagesTime Value of Money Lecture NotesOhene Asare PogastyNo ratings yet

- BFW2140 Lecture Week 2: Corporate Financial Mathematics IDocument33 pagesBFW2140 Lecture Week 2: Corporate Financial Mathematics Iaa TANNo ratings yet

- Feedback and Warm-Up Review: - Feedback of Your Requests - Cash Flow - Cash Flow Diagrams - Economic EquivalenceDocument30 pagesFeedback and Warm-Up Review: - Feedback of Your Requests - Cash Flow - Cash Flow Diagrams - Economic EquivalenceSajid IqbalNo ratings yet

- Chapter 5 Time Value of MoneyDocument25 pagesChapter 5 Time Value of MoneyAhmed FathelbabNo ratings yet

- TVM Part 1Document18 pagesTVM Part 1Hoai ThuongNo ratings yet

- EEE 452: Engineering Economics and Management: - Lec 9: Time Value of MoneyDocument28 pagesEEE 452: Engineering Economics and Management: - Lec 9: Time Value of MoneyTomas KhanNo ratings yet

- The Two Key Concepts in FinanceDocument63 pagesThe Two Key Concepts in FinanceJai SharmaNo ratings yet

- Lecture 02dm Time Value of MoneyDocument42 pagesLecture 02dm Time Value of Moneylja92No ratings yet

- Time Value2023Document68 pagesTime Value2023Geethika NayanaprabhaNo ratings yet

- Time Value of MoneyDocument25 pagesTime Value of MoneyRuchaNo ratings yet

- Chapter 5 & 6Document13 pagesChapter 5 & 6sandi ibrahimNo ratings yet

- Issues in Corporate Finance: ValuationDocument52 pagesIssues in Corporate Finance: ValuationMD Hafizul Islam HafizNo ratings yet

- Introduction To Valuation: The Time Value of MoneyDocument34 pagesIntroduction To Valuation: The Time Value of MoneyAlfina AfiiNo ratings yet

- Principles of Managerial Finance: Time Value of MoneyDocument45 pagesPrinciples of Managerial Finance: Time Value of MoneyJoshNo ratings yet

- Time Value of Money - TVMDocument21 pagesTime Value of Money - TVMTh'bo Muzorewa ChizyukaNo ratings yet

- Parrino 2e PowerPoint Review Ch05Document42 pagesParrino 2e PowerPoint Review Ch05Khadija AlkebsiNo ratings yet

- Mata Kuliah: Manajemen Keuangan 1 Kode Mata Kuliah/Sks: Mn5003 / 3 Sks Kurikulum: 2012 Versi: 0.1Document52 pagesMata Kuliah: Manajemen Keuangan 1 Kode Mata Kuliah/Sks: Mn5003 / 3 Sks Kurikulum: 2012 Versi: 0.1Faishal Alghi FariNo ratings yet

- Topic 4 Valuation of Future Cashflows - Time Value For MoneyDocument39 pagesTopic 4 Valuation of Future Cashflows - Time Value For MoneyQianyiiNo ratings yet

- Module 2Document60 pagesModule 2lizNo ratings yet

- Financial Management Ii: Chapter 5 (Fundamental of Corporate Finance) Introduction To Valuation: The Time Value of MoneyDocument33 pagesFinancial Management Ii: Chapter 5 (Fundamental of Corporate Finance) Introduction To Valuation: The Time Value of MoneyEldi JanuariNo ratings yet

- Lecture 7 9Document106 pagesLecture 7 9Nguyễn Thúy KiềuNo ratings yet

- CH4 - FM - For StudentsDocument45 pagesCH4 - FM - For Studentsjajo200110No ratings yet

- Time Value of MoneyDocument17 pagesTime Value of Moneyyolanda monikaNo ratings yet

- Chapter 3 Interest RateDocument15 pagesChapter 3 Interest RateEhab HosnyNo ratings yet

- Chap 5 TCDNDocument49 pagesChap 5 TCDNNhư Quỳnh TrầnNo ratings yet

- Future Value, Present Value and Interest Rates: Mcgraw-Hill/IrwinDocument44 pagesFuture Value, Present Value and Interest Rates: Mcgraw-Hill/IrwinYasser AlmishalNo ratings yet

- Present Values and Future ValuesDocument50 pagesPresent Values and Future Valueskaylakshmi8314100% (1)

- Unit 3 (a) : Time Value Of Money 1: Analyzing Single Cash Flows 货币时间价值1:分析单一现金流 - Chapter 4Document72 pagesUnit 3 (a) : Time Value Of Money 1: Analyzing Single Cash Flows 货币时间价值1:分析单一现金流 - Chapter 4KaMan CHAUNo ratings yet

- 2023 EBAD401 - Chapter 5 PPT LecturerDocument36 pages2023 EBAD401 - Chapter 5 PPT Lecturermaresa bruinersNo ratings yet

- KJ 169517158287616Document32 pagesKJ 169517158287616Нндн Н'No ratings yet

- Persuasive SpeechDocument7 pagesPersuasive SpeechНндн Н'No ratings yet

- Tsinghua Micro Ch02Document39 pagesTsinghua Micro Ch02Нндн Н'No ratings yet

- Tsinghua Micro Ch03Document40 pagesTsinghua Micro Ch03Нндн Н'No ratings yet

- CF - 04Document54 pagesCF - 04Нндн Н'No ratings yet

- Marketing Department of BritanniaDocument6 pagesMarketing Department of BritanniaradhikaNo ratings yet

- Computing Through Innovation: Group 6Document43 pagesComputing Through Innovation: Group 6Chin-Chin CeraNo ratings yet

- Od 121981902014335000Document4 pagesOd 121981902014335000AKSHAY GOYALNo ratings yet

- 005 - 1965 - Law Relating To TaxationDocument15 pages005 - 1965 - Law Relating To TaxationSubhayan BoralNo ratings yet

- Webslides Q221 FinalDocument19 pagesWebslides Q221 FinalxtrangeNo ratings yet

- Influential Factors in Rising Needs of Mobile BankingDocument5 pagesInfluential Factors in Rising Needs of Mobile BankingInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Value Equivalence LineDocument5 pagesValue Equivalence LineExoYelzy yueNo ratings yet

- IEC 60865-1 1993 - Short-Circuit Currents-Calculation of Effects-Part 1definitions and Calculation Methods.Document121 pagesIEC 60865-1 1993 - Short-Circuit Currents-Calculation of Effects-Part 1definitions and Calculation Methods.AgpKNo ratings yet

- Dissertation On T&P of M&M Ltd.Document49 pagesDissertation On T&P of M&M Ltd.sampada_naradNo ratings yet

- Autobox Press ReleaseDocument4 pagesAutobox Press ReleaseRobins GuptaNo ratings yet

- ReviewerDocument7 pagesReviewerDindi R. SapicoNo ratings yet

- Florida Sport Fishing November-December 2017Document164 pagesFlorida Sport Fishing November-December 2017rwplothowNo ratings yet

- IGCSE Business Studies DefinitionsDocument8 pagesIGCSE Business Studies Definitionsjohnsmacks7No ratings yet

- Marketing Strategy of Hyundai MotorsDocument142 pagesMarketing Strategy of Hyundai MotorsSourabh SoniNo ratings yet

- Apple Conflict Minerals ReportDocument29 pagesApple Conflict Minerals ReportRey MuhammadNo ratings yet

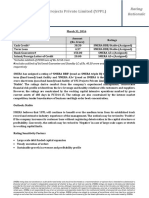

- YFC Projects Private Limited (YPPL) : Rating RationaleDocument2 pagesYFC Projects Private Limited (YPPL) : Rating Rationalelalit rawatNo ratings yet

- A Level Entrepreneurship Revision Questions Based On Syllabus Phase 2Document18 pagesA Level Entrepreneurship Revision Questions Based On Syllabus Phase 2humpho45No ratings yet

- Proposal For Youth Business HubDocument26 pagesProposal For Youth Business Hubfindurvoice100% (1)

- Popular - Telex & Other DocumentsDocument12 pagesPopular - Telex & Other DocumentsnajmithagoshiNo ratings yet

- Erd.1.f.008 Quality Finished Goods 1Document2 pagesErd.1.f.008 Quality Finished Goods 1Jonalyn BalerosNo ratings yet

- Cavalcanti PDFDocument18 pagesCavalcanti PDFThiago Leitao RibeiroNo ratings yet

- Action Plans and EU Acquis Progress Report 2023 WEBDocument212 pagesAction Plans and EU Acquis Progress Report 2023 WEBRaza KandicNo ratings yet

- Transcript Teleconference Financial Results Q1 2023Document16 pagesTranscript Teleconference Financial Results Q1 2023Cirlea CatalinNo ratings yet

- Define Negotiation. and Discuss Various Tactics Adopted in NegotiationDocument7 pagesDefine Negotiation. and Discuss Various Tactics Adopted in NegotiationRicha UpadhyayNo ratings yet