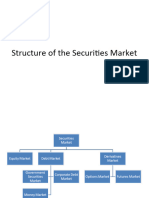

Secondary Market

Secondary Market

You might also like

- Actualbill DownloadDocument4 pagesActualbill DownloadYahya Almarzooqi100% (2)

- KornFerry and Peoplescout JobsDocument994 pagesKornFerry and Peoplescout JobsDeepak PasupuletiNo ratings yet

- Recent Dev in Stock MKT 1Document19 pagesRecent Dev in Stock MKT 1Manikandan N-17No ratings yet

- Origin of Share Markets in IndiaDocument18 pagesOrigin of Share Markets in IndiasrinivasjettyNo ratings yet

- FMO Module 3Document11 pagesFMO Module 3Sonia Dann KuruvillaNo ratings yet

- Capital Market Reforms and FfoDocument10 pagesCapital Market Reforms and FfoVishruti Shah JobanputraNo ratings yet

- Project Report On Stock Market "Working of Stock Exchange & Depositary Services"Document11 pagesProject Report On Stock Market "Working of Stock Exchange & Depositary Services"Kruti NemaNo ratings yet

- Stock Exchanges - A ProfileDocument24 pagesStock Exchanges - A Profilerohitluthra88No ratings yet

- Secondary Markets in IndiaDocument49 pagesSecondary Markets in Indiayashi225100% (1)

- Article Writing - Capital Market - Jyoti Mittal - FBD ChapterDocument5 pagesArticle Writing - Capital Market - Jyoti Mittal - FBD ChapterEsayas ArayaNo ratings yet

- Secondary Markets in IndiaDocument16 pagesSecondary Markets in IndiaAvanishNo ratings yet

- Management Revised SyllabusDocument19 pagesManagement Revised SyllabuskanikaNo ratings yet

- BSEDocument25 pagesBSEanon_35679790650% (2)

- What Is A Stock Exchange All About? The Institution Where Buying and Selling of Shares Essentially Takes Place Is The Stock ExchangeDocument24 pagesWhat Is A Stock Exchange All About? The Institution Where Buying and Selling of Shares Essentially Takes Place Is The Stock ExchangeJinson JohnNo ratings yet

- What Is Stock ExchangeDocument16 pagesWhat Is Stock ExchangeNeha_18No ratings yet

- SEBI ProjectDocument49 pagesSEBI ProjectS KingNo ratings yet

- Stock MarketsDocument37 pagesStock MarketsRahul SinghNo ratings yet

- Secondary Market/Stock Market Exchange (Se)Document36 pagesSecondary Market/Stock Market Exchange (Se)nagniranjanNo ratings yet

- Financial Market Short Notes & QuestionsDocument12 pagesFinancial Market Short Notes & QuestionssyedmerajaliNo ratings yet

- 098 Fmbo-2-Ketaki NikamDocument10 pages098 Fmbo-2-Ketaki NikamKetakiNo ratings yet

- Module 3.1 Secondary MarketDocument54 pagesModule 3.1 Secondary MarketsateeshjorliNo ratings yet

- Overview of The Indian Securities MarketDocument7 pagesOverview of The Indian Securities MarketNiftyDirectNo ratings yet

- Security MarketDocument30 pagesSecurity Marketashish_k_srivastavaNo ratings yet

- Chapter - 1Document12 pagesChapter - 1SsNo ratings yet

- Sebi Capital Market InvestorsDocument34 pagesSebi Capital Market Investors9887287779No ratings yet

- Distributed Generation An OverviewDocument9 pagesDistributed Generation An OverviewAbhishek SaxenaNo ratings yet

- Investing in The Stock Market - Benefits - ProspectsDocument5 pagesInvesting in The Stock Market - Benefits - ProspectsAba Emmanuel OcheNo ratings yet

- T.John Business SchoolDocument77 pagesT.John Business SchoolAkash SiddhuNo ratings yet

- Stock MarketDocument19 pagesStock MarketNishi SharmaNo ratings yet

- Secondary MarketDocument55 pagesSecondary MarketKavita GarkotiNo ratings yet

- CAPITAL-MARKET-BBA-3RD-SEM - FinalDocument84 pagesCAPITAL-MARKET-BBA-3RD-SEM - FinalSunny MittalNo ratings yet

- BSM Project (Stock Exchange)Document15 pagesBSM Project (Stock Exchange)PowerPoint GoNo ratings yet

- 1698302906984_CM Chapter 02Document17 pages1698302906984_CM Chapter 02akshaykr963963No ratings yet

- Stock Exchanges: MeaningDocument8 pagesStock Exchanges: MeaningAshish BhadulaNo ratings yet

- Meaning:: UNIT-3 Stock Exchange Meaning and Definition of Stock ExchangeDocument12 pagesMeaning:: UNIT-3 Stock Exchange Meaning and Definition of Stock ExchangeSudha RaoNo ratings yet

- Unit 2 SecuritiesDocument12 pagesUnit 2 Securitiespranati maruNo ratings yet

- Fin Mkts Unit III Lec NotesDocument6 pagesFin Mkts Unit III Lec Notesprakash.pNo ratings yet

- Internal Backlog Company Law Role of Sebi in Stock ExchangeDocument9 pagesInternal Backlog Company Law Role of Sebi in Stock ExchangeApoorv SrivastavaNo ratings yet

- Stock ExchangeDocument30 pagesStock ExchangeJust ListenNo ratings yet

- Unit IIIDocument17 pagesUnit IIIVidhyaBalaNo ratings yet

- Malaysian Investment Market and TransactionDocument62 pagesMalaysian Investment Market and TransactionRenese LeeNo ratings yet

- FIBA - Capital MarketDocument21 pagesFIBA - Capital MarketDivisha AgarwalNo ratings yet

- Unit 9 Capital Market I1 Secondary Market: 9.0 ObjectivesDocument16 pagesUnit 9 Capital Market I1 Secondary Market: 9.0 ObjectivesSmijin.P.SNo ratings yet

- 3 Market & SebiDocument7 pages3 Market & SebiSaloni AgrawalNo ratings yet

- Indian Money Market and Capital MarketDocument41 pagesIndian Money Market and Capital Marketsamrulezzz100% (4)

- Lecture 2.1.3 Secondary MarketDocument61 pagesLecture 2.1.3 Secondary MarketDeepansh SharmaNo ratings yet

- OTCEI: Concept and Advantages - India - Financial ManagementDocument9 pagesOTCEI: Concept and Advantages - India - Financial Managementjobin josephNo ratings yet

- EEB 2.2. Capital MarketDocument37 pagesEEB 2.2. Capital Marketkaranj321No ratings yet

- Law Final GauriDocument10 pagesLaw Final GauriPoonam KhondNo ratings yet

- Introduction:-: Providing Liability To SecuritiesDocument10 pagesIntroduction:-: Providing Liability To SecuritiespappunaagraajNo ratings yet

- Tunis Stock ExchangeDocument54 pagesTunis Stock ExchangeAnonymous AoDxR5Rp4JNo ratings yet

- Stock MarketDocument29 pagesStock MarketSarabjeet Kaur Sohi0% (1)

- SEBI (Securities and Exchange Board of India) Was Establishes As A Non Statutory Body inDocument2 pagesSEBI (Securities and Exchange Board of India) Was Establishes As A Non Statutory Body inRahul PandeyNo ratings yet

- Equity and Debt Pending NotesDocument18 pagesEquity and Debt Pending NotesAbbas BengaliwalaNo ratings yet

- Secondary MarketsDocument32 pagesSecondary MarketsRheneir MoraNo ratings yet

- Lecture 2.1.2 Primary MarketDocument27 pagesLecture 2.1.2 Primary MarketDeepansh SharmaNo ratings yet

- Stock Exchanges in IndiaDocument30 pagesStock Exchanges in Indiavinit_shah90No ratings yet

- TechnologyDocument16 pagesTechnologysuppishikhaNo ratings yet

- Definition of Stock ExchangeDocument21 pagesDefinition of Stock ExchangeSrinu UdumulaNo ratings yet

- Mastering the Market: A Comprehensive Guide to Successful Stock InvestingFrom EverandMastering the Market: A Comprehensive Guide to Successful Stock InvestingNo ratings yet

- 850Document21 pages850Harsh ThakurNo ratings yet

- Bba IV Bis Unit 4 NotesDocument12 pagesBba IV Bis Unit 4 NotesHarsh ThakurNo ratings yet

- Chapter 1Document16 pagesChapter 1Harsh ThakurNo ratings yet

- Players in The MarketDocument17 pagesPlayers in The MarketHarsh ThakurNo ratings yet

- Money Market Its InstrumentsDocument13 pagesMoney Market Its InstrumentsHarsh ThakurNo ratings yet

- Chapter 4Document34 pagesChapter 4Harsh ThakurNo ratings yet

- School of Managment Sciences, Varanasi (An Autonomous College)Document2 pagesSchool of Managment Sciences, Varanasi (An Autonomous College)Harsh ThakurNo ratings yet

- Fso Unit-3Document7 pagesFso Unit-3Harsh ThakurNo ratings yet

- Chapter 3Document32 pagesChapter 3Harsh ThakurNo ratings yet

- Capital Primary MarketDocument45 pagesCapital Primary MarketHarsh ThakurNo ratings yet

- Significance of Diagrams and GraphsDocument2 pagesSignificance of Diagrams and GraphsHarsh ThakurNo ratings yet

- Mutual Funds 1Document42 pagesMutual Funds 1Harsh ThakurNo ratings yet

- Bba IV Bis Unit 3 NotesDocument18 pagesBba IV Bis Unit 3 NotesHarsh ThakurNo ratings yet

- JMjCB90x1Y3PfBax - oUaQFH - oKoWHXFnp-Unique Value Proposition Competitive Analysis Matrix AccessibleDocument2 pagesJMjCB90x1Y3PfBax - oUaQFH - oKoWHXFnp-Unique Value Proposition Competitive Analysis Matrix AccessibleHarsh ThakurNo ratings yet

- Boyke Yurista - JalinDocument14 pagesBoyke Yurista - JalinARN100% (1)

- Competitor AnalysisDocument4 pagesCompetitor Analysisalhad86No ratings yet

- Concept Note For A Seed Value Chain SolutionDocument3 pagesConcept Note For A Seed Value Chain Solutionotaala8171100% (1)

- Food ProcessingDocument8 pagesFood ProcessingKhushbooNo ratings yet

- Annamalai University MBA Assignment Solution 2019Document98 pagesAnnamalai University MBA Assignment Solution 2019palaniappannNo ratings yet

- Green BuildingDocument79 pagesGreen BuildingSURJIT DUTTANo ratings yet

- Pay Slip For SalaryDocument6 pagesPay Slip For SalarysanilNo ratings yet

- Problems On Ratio AnalysisDocument7 pagesProblems On Ratio AnalysisVinay H V MBA100% (1)

- Topic 1. Introduction To Production and Operations ManagementDocument30 pagesTopic 1. Introduction To Production and Operations ManagementVikrant BaghelNo ratings yet

- Chapter 1-What Is MarketingDocument15 pagesChapter 1-What Is MarketingMohd AnwarshahNo ratings yet

- Recycling Saves The EcosystemDocument3 pagesRecycling Saves The EcosystemAbdulrahman AlhammadiNo ratings yet

- Discussion Paper On Attitudes Toward RiskDocument2 pagesDiscussion Paper On Attitudes Toward RiskXeena LeonesNo ratings yet

- Private: Anarchy and InventionDocument4 pagesPrivate: Anarchy and InventionMischa ByruckNo ratings yet

- The Role of Corporate Boards IN THE 1990s: February 29, 1992 Beaver Creek, ColoradoDocument21 pagesThe Role of Corporate Boards IN THE 1990s: February 29, 1992 Beaver Creek, ColoradoMuhammad RandyNo ratings yet

- Trading The Gartley 222Document14 pagesTrading The Gartley 222Joao PereiraNo ratings yet

- Public Borrowing and Debt Management by Mario RanceDocument47 pagesPublic Borrowing and Debt Management by Mario RanceWo Rance100% (2)

- Sri Lanka Demography and Income DistributionDocument176 pagesSri Lanka Demography and Income DistributionThilina DilshanNo ratings yet

- Module - 5: Direct MarketingDocument46 pagesModule - 5: Direct Marketingwintoday01No ratings yet

- Soc. Sci. Understanding Culture ActivityDocument4 pagesSoc. Sci. Understanding Culture Activityaomine daikiNo ratings yet

- Human Resources DevelopmentDocument16 pagesHuman Resources DevelopmentZahwa DhiyanaNo ratings yet

- Pages From LIST OF DOCUMENTS FOR Infra & EIA SUBMISSIONSDocument2 pagesPages From LIST OF DOCUMENTS FOR Infra & EIA SUBMISSIONSNgoc Ba NguyenNo ratings yet

- An Introduction To Portfolio OptimizationDocument55 pagesAn Introduction To Portfolio OptimizationMarlee123100% (1)

- Workbook 1 Introduction To IPSAS Accruals AccountingDocument40 pagesWorkbook 1 Introduction To IPSAS Accruals AccountingBig-Brain MuzunguNo ratings yet

- LN02-Introduction To Engineering EconomicsDocument17 pagesLN02-Introduction To Engineering Economicsmehedi hasanNo ratings yet

- SME Banking MasterclassDocument8 pagesSME Banking MasterclassJoan MilokNo ratings yet

- Final Examination Ge3 The Contemporary WorldDocument4 pagesFinal Examination Ge3 The Contemporary WorldRamon III ObligadoNo ratings yet

- Hiring PolicyDocument3 pagesHiring PolicyEhtesham ShoukatNo ratings yet

- FS 1Document19 pagesFS 1Christian Jay SelehenciaNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Actualbill DownloadDocument4 pagesActualbill DownloadYahya Almarzooqi100% (2)

- KornFerry and Peoplescout JobsDocument994 pagesKornFerry and Peoplescout JobsDeepak PasupuletiNo ratings yet

- Recent Dev in Stock MKT 1Document19 pagesRecent Dev in Stock MKT 1Manikandan N-17No ratings yet

- Origin of Share Markets in IndiaDocument18 pagesOrigin of Share Markets in IndiasrinivasjettyNo ratings yet

- FMO Module 3Document11 pagesFMO Module 3Sonia Dann KuruvillaNo ratings yet

- Capital Market Reforms and FfoDocument10 pagesCapital Market Reforms and FfoVishruti Shah JobanputraNo ratings yet

- Project Report On Stock Market "Working of Stock Exchange & Depositary Services"Document11 pagesProject Report On Stock Market "Working of Stock Exchange & Depositary Services"Kruti NemaNo ratings yet

- Stock Exchanges - A ProfileDocument24 pagesStock Exchanges - A Profilerohitluthra88No ratings yet

- Secondary Markets in IndiaDocument49 pagesSecondary Markets in Indiayashi225100% (1)

- Article Writing - Capital Market - Jyoti Mittal - FBD ChapterDocument5 pagesArticle Writing - Capital Market - Jyoti Mittal - FBD ChapterEsayas ArayaNo ratings yet

- Secondary Markets in IndiaDocument16 pagesSecondary Markets in IndiaAvanishNo ratings yet

- Management Revised SyllabusDocument19 pagesManagement Revised SyllabuskanikaNo ratings yet

- BSEDocument25 pagesBSEanon_35679790650% (2)

- What Is A Stock Exchange All About? The Institution Where Buying and Selling of Shares Essentially Takes Place Is The Stock ExchangeDocument24 pagesWhat Is A Stock Exchange All About? The Institution Where Buying and Selling of Shares Essentially Takes Place Is The Stock ExchangeJinson JohnNo ratings yet

- What Is Stock ExchangeDocument16 pagesWhat Is Stock ExchangeNeha_18No ratings yet

- SEBI ProjectDocument49 pagesSEBI ProjectS KingNo ratings yet

- Stock MarketsDocument37 pagesStock MarketsRahul SinghNo ratings yet

- Secondary Market/Stock Market Exchange (Se)Document36 pagesSecondary Market/Stock Market Exchange (Se)nagniranjanNo ratings yet

- Financial Market Short Notes & QuestionsDocument12 pagesFinancial Market Short Notes & QuestionssyedmerajaliNo ratings yet

- 098 Fmbo-2-Ketaki NikamDocument10 pages098 Fmbo-2-Ketaki NikamKetakiNo ratings yet

- Module 3.1 Secondary MarketDocument54 pagesModule 3.1 Secondary MarketsateeshjorliNo ratings yet

- Overview of The Indian Securities MarketDocument7 pagesOverview of The Indian Securities MarketNiftyDirectNo ratings yet

- Security MarketDocument30 pagesSecurity Marketashish_k_srivastavaNo ratings yet

- Chapter - 1Document12 pagesChapter - 1SsNo ratings yet

- Sebi Capital Market InvestorsDocument34 pagesSebi Capital Market Investors9887287779No ratings yet

- Distributed Generation An OverviewDocument9 pagesDistributed Generation An OverviewAbhishek SaxenaNo ratings yet

- Investing in The Stock Market - Benefits - ProspectsDocument5 pagesInvesting in The Stock Market - Benefits - ProspectsAba Emmanuel OcheNo ratings yet

- T.John Business SchoolDocument77 pagesT.John Business SchoolAkash SiddhuNo ratings yet

- Stock MarketDocument19 pagesStock MarketNishi SharmaNo ratings yet

- Secondary MarketDocument55 pagesSecondary MarketKavita GarkotiNo ratings yet

- CAPITAL-MARKET-BBA-3RD-SEM - FinalDocument84 pagesCAPITAL-MARKET-BBA-3RD-SEM - FinalSunny MittalNo ratings yet

- BSM Project (Stock Exchange)Document15 pagesBSM Project (Stock Exchange)PowerPoint GoNo ratings yet

- 1698302906984_CM Chapter 02Document17 pages1698302906984_CM Chapter 02akshaykr963963No ratings yet

- Stock Exchanges: MeaningDocument8 pagesStock Exchanges: MeaningAshish BhadulaNo ratings yet

- Meaning:: UNIT-3 Stock Exchange Meaning and Definition of Stock ExchangeDocument12 pagesMeaning:: UNIT-3 Stock Exchange Meaning and Definition of Stock ExchangeSudha RaoNo ratings yet

- Unit 2 SecuritiesDocument12 pagesUnit 2 Securitiespranati maruNo ratings yet

- Fin Mkts Unit III Lec NotesDocument6 pagesFin Mkts Unit III Lec Notesprakash.pNo ratings yet

- Internal Backlog Company Law Role of Sebi in Stock ExchangeDocument9 pagesInternal Backlog Company Law Role of Sebi in Stock ExchangeApoorv SrivastavaNo ratings yet

- Stock ExchangeDocument30 pagesStock ExchangeJust ListenNo ratings yet

- Unit IIIDocument17 pagesUnit IIIVidhyaBalaNo ratings yet

- Malaysian Investment Market and TransactionDocument62 pagesMalaysian Investment Market and TransactionRenese LeeNo ratings yet

- FIBA - Capital MarketDocument21 pagesFIBA - Capital MarketDivisha AgarwalNo ratings yet

- Unit 9 Capital Market I1 Secondary Market: 9.0 ObjectivesDocument16 pagesUnit 9 Capital Market I1 Secondary Market: 9.0 ObjectivesSmijin.P.SNo ratings yet

- 3 Market & SebiDocument7 pages3 Market & SebiSaloni AgrawalNo ratings yet

- Indian Money Market and Capital MarketDocument41 pagesIndian Money Market and Capital Marketsamrulezzz100% (4)

- Lecture 2.1.3 Secondary MarketDocument61 pagesLecture 2.1.3 Secondary MarketDeepansh SharmaNo ratings yet

- OTCEI: Concept and Advantages - India - Financial ManagementDocument9 pagesOTCEI: Concept and Advantages - India - Financial Managementjobin josephNo ratings yet

- EEB 2.2. Capital MarketDocument37 pagesEEB 2.2. Capital Marketkaranj321No ratings yet

- Law Final GauriDocument10 pagesLaw Final GauriPoonam KhondNo ratings yet

- Introduction:-: Providing Liability To SecuritiesDocument10 pagesIntroduction:-: Providing Liability To SecuritiespappunaagraajNo ratings yet

- Tunis Stock ExchangeDocument54 pagesTunis Stock ExchangeAnonymous AoDxR5Rp4JNo ratings yet

- Stock MarketDocument29 pagesStock MarketSarabjeet Kaur Sohi0% (1)

- SEBI (Securities and Exchange Board of India) Was Establishes As A Non Statutory Body inDocument2 pagesSEBI (Securities and Exchange Board of India) Was Establishes As A Non Statutory Body inRahul PandeyNo ratings yet

- Equity and Debt Pending NotesDocument18 pagesEquity and Debt Pending NotesAbbas BengaliwalaNo ratings yet

- Secondary MarketsDocument32 pagesSecondary MarketsRheneir MoraNo ratings yet

- Lecture 2.1.2 Primary MarketDocument27 pagesLecture 2.1.2 Primary MarketDeepansh SharmaNo ratings yet

- Stock Exchanges in IndiaDocument30 pagesStock Exchanges in Indiavinit_shah90No ratings yet

- TechnologyDocument16 pagesTechnologysuppishikhaNo ratings yet

- Definition of Stock ExchangeDocument21 pagesDefinition of Stock ExchangeSrinu UdumulaNo ratings yet

- Mastering the Market: A Comprehensive Guide to Successful Stock InvestingFrom EverandMastering the Market: A Comprehensive Guide to Successful Stock InvestingNo ratings yet

- 850Document21 pages850Harsh ThakurNo ratings yet

- Bba IV Bis Unit 4 NotesDocument12 pagesBba IV Bis Unit 4 NotesHarsh ThakurNo ratings yet

- Chapter 1Document16 pagesChapter 1Harsh ThakurNo ratings yet

- Players in The MarketDocument17 pagesPlayers in The MarketHarsh ThakurNo ratings yet

- Money Market Its InstrumentsDocument13 pagesMoney Market Its InstrumentsHarsh ThakurNo ratings yet

- Chapter 4Document34 pagesChapter 4Harsh ThakurNo ratings yet

- School of Managment Sciences, Varanasi (An Autonomous College)Document2 pagesSchool of Managment Sciences, Varanasi (An Autonomous College)Harsh ThakurNo ratings yet

- Fso Unit-3Document7 pagesFso Unit-3Harsh ThakurNo ratings yet

- Chapter 3Document32 pagesChapter 3Harsh ThakurNo ratings yet

- Capital Primary MarketDocument45 pagesCapital Primary MarketHarsh ThakurNo ratings yet

- Significance of Diagrams and GraphsDocument2 pagesSignificance of Diagrams and GraphsHarsh ThakurNo ratings yet

- Mutual Funds 1Document42 pagesMutual Funds 1Harsh ThakurNo ratings yet

- Bba IV Bis Unit 3 NotesDocument18 pagesBba IV Bis Unit 3 NotesHarsh ThakurNo ratings yet

- JMjCB90x1Y3PfBax - oUaQFH - oKoWHXFnp-Unique Value Proposition Competitive Analysis Matrix AccessibleDocument2 pagesJMjCB90x1Y3PfBax - oUaQFH - oKoWHXFnp-Unique Value Proposition Competitive Analysis Matrix AccessibleHarsh ThakurNo ratings yet

- Boyke Yurista - JalinDocument14 pagesBoyke Yurista - JalinARN100% (1)

- Competitor AnalysisDocument4 pagesCompetitor Analysisalhad86No ratings yet

- Concept Note For A Seed Value Chain SolutionDocument3 pagesConcept Note For A Seed Value Chain Solutionotaala8171100% (1)

- Food ProcessingDocument8 pagesFood ProcessingKhushbooNo ratings yet

- Annamalai University MBA Assignment Solution 2019Document98 pagesAnnamalai University MBA Assignment Solution 2019palaniappannNo ratings yet

- Green BuildingDocument79 pagesGreen BuildingSURJIT DUTTANo ratings yet

- Pay Slip For SalaryDocument6 pagesPay Slip For SalarysanilNo ratings yet

- Problems On Ratio AnalysisDocument7 pagesProblems On Ratio AnalysisVinay H V MBA100% (1)

- Topic 1. Introduction To Production and Operations ManagementDocument30 pagesTopic 1. Introduction To Production and Operations ManagementVikrant BaghelNo ratings yet

- Chapter 1-What Is MarketingDocument15 pagesChapter 1-What Is MarketingMohd AnwarshahNo ratings yet

- Recycling Saves The EcosystemDocument3 pagesRecycling Saves The EcosystemAbdulrahman AlhammadiNo ratings yet

- Discussion Paper On Attitudes Toward RiskDocument2 pagesDiscussion Paper On Attitudes Toward RiskXeena LeonesNo ratings yet

- Private: Anarchy and InventionDocument4 pagesPrivate: Anarchy and InventionMischa ByruckNo ratings yet

- The Role of Corporate Boards IN THE 1990s: February 29, 1992 Beaver Creek, ColoradoDocument21 pagesThe Role of Corporate Boards IN THE 1990s: February 29, 1992 Beaver Creek, ColoradoMuhammad RandyNo ratings yet

- Trading The Gartley 222Document14 pagesTrading The Gartley 222Joao PereiraNo ratings yet

- Public Borrowing and Debt Management by Mario RanceDocument47 pagesPublic Borrowing and Debt Management by Mario RanceWo Rance100% (2)

- Sri Lanka Demography and Income DistributionDocument176 pagesSri Lanka Demography and Income DistributionThilina DilshanNo ratings yet

- Module - 5: Direct MarketingDocument46 pagesModule - 5: Direct Marketingwintoday01No ratings yet

- Soc. Sci. Understanding Culture ActivityDocument4 pagesSoc. Sci. Understanding Culture Activityaomine daikiNo ratings yet

- Human Resources DevelopmentDocument16 pagesHuman Resources DevelopmentZahwa DhiyanaNo ratings yet

- Pages From LIST OF DOCUMENTS FOR Infra & EIA SUBMISSIONSDocument2 pagesPages From LIST OF DOCUMENTS FOR Infra & EIA SUBMISSIONSNgoc Ba NguyenNo ratings yet

- An Introduction To Portfolio OptimizationDocument55 pagesAn Introduction To Portfolio OptimizationMarlee123100% (1)

- Workbook 1 Introduction To IPSAS Accruals AccountingDocument40 pagesWorkbook 1 Introduction To IPSAS Accruals AccountingBig-Brain MuzunguNo ratings yet

- LN02-Introduction To Engineering EconomicsDocument17 pagesLN02-Introduction To Engineering Economicsmehedi hasanNo ratings yet

- SME Banking MasterclassDocument8 pagesSME Banking MasterclassJoan MilokNo ratings yet

- Final Examination Ge3 The Contemporary WorldDocument4 pagesFinal Examination Ge3 The Contemporary WorldRamon III ObligadoNo ratings yet

- Hiring PolicyDocument3 pagesHiring PolicyEhtesham ShoukatNo ratings yet

- FS 1Document19 pagesFS 1Christian Jay SelehenciaNo ratings yet