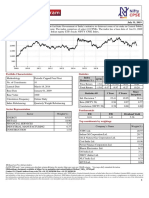

Fidelity Investment Managers: All-Terrain Investing: November 2010

Fidelity Investment Managers: All-Terrain Investing: November 2010

You might also like

- The Intelligent REIT Investor: How to Build Wealth with Real Estate Investment TrustsFrom EverandThe Intelligent REIT Investor: How to Build Wealth with Real Estate Investment TrustsRating: 4.5 out of 5 stars4.5/5 (4)

- Submitted By: Cabling, Alvin Hachiles, Jomari Honera, Shawn Michael Miranda, Christopher Odonzo, Aldwin Salvador, ChristianDocument32 pagesSubmitted By: Cabling, Alvin Hachiles, Jomari Honera, Shawn Michael Miranda, Christopher Odonzo, Aldwin Salvador, ChristianKimberly Claire AtienzaNo ratings yet

- Sample StatementDocument1 pageSample StatementShahzad YounasNo ratings yet

- Fid MoneybuilderDocument2 pagesFid Moneybuildersnake1977No ratings yet

- The Investment ClockDocument4 pagesThe Investment ClockJean Carlos TorresNo ratings yet

- August 2011Document7 pagesAugust 2011stephen_wood_36No ratings yet

- January 2012Document8 pagesJanuary 2012stephen_wood_36No ratings yet

- Weekly Market Commentary: Run For The RosesDocument3 pagesWeekly Market Commentary: Run For The Rosespathanfor786No ratings yet

- Q2 2013 Market UpdateDocument57 pagesQ2 2013 Market Updaterwmortell3580No ratings yet

- 2011-2012 Review and Outlook: Metwest Total Return Bond Fund Is There Life After Debt?Document55 pages2011-2012 Review and Outlook: Metwest Total Return Bond Fund Is There Life After Debt?Brad SamplesNo ratings yet

- Pitchbook StrategyDocument25 pagesPitchbook Strategydfk1111No ratings yet

- Sgreits 020911Document18 pagesSgreits 020911Royston Tan Keng SanNo ratings yet

- Selector September 2004 Quarterly NewsletterDocument5 pagesSelector September 2004 Quarterly Newsletterapi-237451731No ratings yet

- February 2011Document3 pagesFebruary 2011gradnvNo ratings yet

- May 2012Document8 pagesMay 2012stephen_wood_36No ratings yet

- 10 Key Trends Changing Inv MGMTDocument50 pages10 Key Trends Changing Inv MGMTcaitlynharveyNo ratings yet

- JPM Weekly MKT Recap 8-13-12Document2 pagesJPM Weekly MKT Recap 8-13-12Flat Fee PortfoliosNo ratings yet

- JPM Weekly MKT Recap 9-10-12Document2 pagesJPM Weekly MKT Recap 9-10-12Flat Fee PortfoliosNo ratings yet

- November 2011Document8 pagesNovember 2011stephen_wood_36No ratings yet

- 2012 Outlook: Australian Equity StrategyDocument36 pages2012 Outlook: Australian Equity StrategyLuke Campbell-Smith100% (1)

- File 1Document10 pagesFile 1Alberto VillalpandoNo ratings yet

- Fixed Income Is NecessaryDocument11 pagesFixed Income Is NecessaryAkshat TulsyanNo ratings yet

- Investment Process: Portfolio ConstructionDocument22 pagesInvestment Process: Portfolio ConstructionÃarthï ArülrãjNo ratings yet

- Weekly Market Commentary 3-512-2012Document4 pagesWeekly Market Commentary 3-512-2012monarchadvisorygroupNo ratings yet

- Group 24Document23 pagesGroup 24dineomokoena327No ratings yet

- 2009: A Tale of Two Halves: A Roadmap For The Global RecessionDocument12 pages2009: A Tale of Two Halves: A Roadmap For The Global RecessionsdNo ratings yet

- Weekly Market Commentary 03092015Document5 pagesWeekly Market Commentary 03092015dpbasicNo ratings yet

- CIMB-Principal Australian Equity Fund (Ex)Document2 pagesCIMB-Principal Australian Equity Fund (Ex)Pei ChinNo ratings yet

- IDFC Emergin Businesses NFODocument5 pagesIDFC Emergin Businesses NFOfinancialbondingNo ratings yet

- 2011-07-31 Brait Multi StrategyDocument2 pages2011-07-31 Brait Multi StrategykcousinsNo ratings yet

- Maverick Capital Q1 2011Document13 pagesMaverick Capital Q1 2011Yingluq100% (1)

- Goldman Sachs - MarketPulse - Special Edition - Ten For 2013Document3 pagesGoldman Sachs - MarketPulse - Special Edition - Ten For 2013cdietzrNo ratings yet

- Bond Market Perspectives 06092015Document4 pagesBond Market Perspectives 06092015dpbasicNo ratings yet

- Artemis Fund Managers Limited IncomeDocument14 pagesArtemis Fund Managers Limited IncomeAlviNo ratings yet

- Weekly Market Commentary 10-10-11Document3 pagesWeekly Market Commentary 10-10-11monarchadvisorygroupNo ratings yet

- Osku Ob Kid Save June 2013 FactsheetDocument3 pagesOsku Ob Kid Save June 2013 FactsheetRaymond Chan Chun LimNo ratings yet

- Quarterly Fund GuideDocument72 pagesQuarterly Fund GuideJohn SmithNo ratings yet

- Direct Factsheet July 12Document8 pagesDirect Factsheet July 12stephen_wood_36No ratings yet

- C Mmodity O: OutlookDocument36 pagesC Mmodity O: Outlookgaurav_agrawal_4No ratings yet

- JPM Weekly MKT Recap 3-05-12Document2 pagesJPM Weekly MKT Recap 3-05-12Flat Fee PortfoliosNo ratings yet

- JPM Weekly MKT Recap 10-15-12Document2 pagesJPM Weekly MKT Recap 10-15-12Flat Fee PortfoliosNo ratings yet

- JF Asia New Frontiers: Fund ObjectiveDocument1 pageJF Asia New Frontiers: Fund ObjectiveMd Saiful Islam KhanNo ratings yet

- JPM Weekly MKT Recap 2-27-12Document2 pagesJPM Weekly MKT Recap 2-27-12Flat Fee PortfoliosNo ratings yet

- Mfi 0516Document48 pagesMfi 0516StephNo ratings yet

- Sarasin EM Bond OutlookDocument20 pagesSarasin EM Bond OutlookabbdealsNo ratings yet

- Equity Strategy: The 5 Top Picks For FebruaryDocument26 pagesEquity Strategy: The 5 Top Picks For Februarymwrolim_01No ratings yet

- 209652CIMB Islamic DALI Equity Growth FundDocument2 pages209652CIMB Islamic DALI Equity Growth FundazmimdaliNo ratings yet

- The Case For Yield Investing: SchrodersDocument6 pagesThe Case For Yield Investing: SchrodersnigeltaylorNo ratings yet

- Security Bank - UITF Investment ReportDocument2 pagesSecurity Bank - UITF Investment ReportgwapongkabayoNo ratings yet

- AMANX FactSheetDocument2 pagesAMANX FactSheetMayukh RoyNo ratings yet

- JPMorgan Global Investment Banks 2010-09-08Document176 pagesJPMorgan Global Investment Banks 2010-09-08francoib991905No ratings yet

- CCT Ar-2015Document184 pagesCCT Ar-2015Sassy TanNo ratings yet

- JPM Weekly Market Recap October 10, 2011Document2 pagesJPM Weekly Market Recap October 10, 2011everest8848No ratings yet

- MR RIC EmergingMarketsEquityFund A enDocument2 pagesMR RIC EmergingMarketsEquityFund A enabandegenialNo ratings yet

- CORPFIN 7040: Fixed Income Securities (M) Embedded Research ProjectDocument12 pagesCORPFIN 7040: Fixed Income Securities (M) Embedded Research Project邓媛No ratings yet

- JPM Weekly MKT Recap 10-08-12Document2 pagesJPM Weekly MKT Recap 10-08-12Flat Fee PortfoliosNo ratings yet

- June 2012Document8 pagesJune 2012stephen_wood_36No ratings yet

- JPM Weekly MKT Recap 4-23-12Document2 pagesJPM Weekly MKT Recap 4-23-12Flat Fee PortfoliosNo ratings yet

- Jpmorgan Trust IIDocument180 pagesJpmorgan Trust IIgunjanbihaniNo ratings yet

- Raghuram Rajan - Fin Devt and RiskDocument20 pagesRaghuram Rajan - Fin Devt and Riska65b66incNo ratings yet

- Allan Gray Equity Fund: BenchmarkDocument2 pagesAllan Gray Equity Fund: Benchmarkapi-217792169No ratings yet

- Platform Factsheet Nov 2012Document7 pagesPlatform Factsheet Nov 2012stephen_wood_36No ratings yet

- 2022 Grade 10 Controlled Test 3 QP EngDocument5 pages2022 Grade 10 Controlled Test 3 QP EngkellzylesediNo ratings yet

- Offering Document: Management Company Alfalah GHP Investment Management LimitedDocument63 pagesOffering Document: Management Company Alfalah GHP Investment Management Limitedaslam_gheewalaNo ratings yet

- Company Secretary N.K.SinhaDocument4 pagesCompany Secretary N.K.SinhaMohit KeswaniNo ratings yet

- 2 Financial Marek T and ServicesDocument2 pages2 Financial Marek T and Servicesbhaskarganesh0% (1)

- SMB Foundation: Mon Tue Wed Thu FriDocument3 pagesSMB Foundation: Mon Tue Wed Thu FriSidharth GummallaNo ratings yet

- CFM Graph DataDocument11 pagesCFM Graph DataMohammed NazeerNo ratings yet

- Unit III MakroekonomiksDocument40 pagesUnit III MakroekonomiksLerton G. ClaudioNo ratings yet

- Notes - Investment Property BookDocument2 pagesNotes - Investment Property BookJake AustriaNo ratings yet

- Corp Fin Test PDFDocument6 pagesCorp Fin Test PDFRaghav JainNo ratings yet

- Module 12 - Investment PropertyDocument15 pagesModule 12 - Investment PropertyJehPoyNo ratings yet

- Taxsutra All Rights ReservedDocument8 pagesTaxsutra All Rights ReservedAlpa Shah DesaiNo ratings yet

- FINC1302 - Exer&Asgnt - Revised 5 Feb 2020Document24 pagesFINC1302 - Exer&Asgnt - Revised 5 Feb 2020faqehaNo ratings yet

- Chapte - 25 - InternationalDiversification FinanceDocument43 pagesChapte - 25 - InternationalDiversification FinanceKlajdPanariti100% (1)

- TELUS Corporation: Dividend Policy: Canadian Telecommunication IndustryDocument7 pagesTELUS Corporation: Dividend Policy: Canadian Telecommunication Industrymalaika12No ratings yet

- The 4 Pillars of Investing: Quick Reference ChecklistDocument5 pagesThe 4 Pillars of Investing: Quick Reference ChecklistAlex BirfaNo ratings yet

- Business Finance q2 Las w1Document47 pagesBusiness Finance q2 Las w1ggonegvft86% (7)

- Stock Brocking Industry ProfileDocument10 pagesStock Brocking Industry ProfilesaiyuvatechNo ratings yet

- Basics of Islamic BankingDocument186 pagesBasics of Islamic BankingFaryal JamilNo ratings yet

- Role of Commodity Exchange in Agricultural GrowthDocument63 pagesRole of Commodity Exchange in Agricultural GrowthSoumyalin Santy50% (2)

- Economics 2 (Money Banking and International Trade 1)Document22 pagesEconomics 2 (Money Banking and International Trade 1)Ankit AnandNo ratings yet

- Wyckoff Method and Cheat SheetDocument25 pagesWyckoff Method and Cheat SheetAhmad Azwar AmaladiNo ratings yet

- Wealth Insight - April 2024Document64 pagesWealth Insight - April 2024barundasaNo ratings yet

- Review of Session 2002-2003Document262 pagesReview of Session 2002-2003The Royal Society of EdinburghNo ratings yet

- DHL ExpressDocument32 pagesDHL ExpressGregory FrancoNo ratings yet

- Dividend Policy, Chapter 17Document22 pagesDividend Policy, Chapter 17202110782No ratings yet

- A Comparative Study of ELSSDocument4 pagesA Comparative Study of ELSSSilparajaNo ratings yet

- Ind Nifty CPSEDocument1 pageInd Nifty CPSEPrabhakar DalviNo ratings yet

- NISM Series X B-Investment Adviser Level 2 - New VersionDocument274 pagesNISM Series X B-Investment Adviser Level 2 - New VersionAlamgir HaqueNo ratings yet

Download as ppt, pdf, or txt

You might also like

- The Intelligent REIT Investor: How to Build Wealth with Real Estate Investment TrustsFrom EverandThe Intelligent REIT Investor: How to Build Wealth with Real Estate Investment TrustsRating: 4.5 out of 5 stars4.5/5 (4)

- Submitted By: Cabling, Alvin Hachiles, Jomari Honera, Shawn Michael Miranda, Christopher Odonzo, Aldwin Salvador, ChristianDocument32 pagesSubmitted By: Cabling, Alvin Hachiles, Jomari Honera, Shawn Michael Miranda, Christopher Odonzo, Aldwin Salvador, ChristianKimberly Claire AtienzaNo ratings yet

- Sample StatementDocument1 pageSample StatementShahzad YounasNo ratings yet

- Fid MoneybuilderDocument2 pagesFid Moneybuildersnake1977No ratings yet

- The Investment ClockDocument4 pagesThe Investment ClockJean Carlos TorresNo ratings yet

- August 2011Document7 pagesAugust 2011stephen_wood_36No ratings yet

- January 2012Document8 pagesJanuary 2012stephen_wood_36No ratings yet

- Weekly Market Commentary: Run For The RosesDocument3 pagesWeekly Market Commentary: Run For The Rosespathanfor786No ratings yet

- Q2 2013 Market UpdateDocument57 pagesQ2 2013 Market Updaterwmortell3580No ratings yet

- 2011-2012 Review and Outlook: Metwest Total Return Bond Fund Is There Life After Debt?Document55 pages2011-2012 Review and Outlook: Metwest Total Return Bond Fund Is There Life After Debt?Brad SamplesNo ratings yet

- Pitchbook StrategyDocument25 pagesPitchbook Strategydfk1111No ratings yet

- Sgreits 020911Document18 pagesSgreits 020911Royston Tan Keng SanNo ratings yet

- Selector September 2004 Quarterly NewsletterDocument5 pagesSelector September 2004 Quarterly Newsletterapi-237451731No ratings yet

- February 2011Document3 pagesFebruary 2011gradnvNo ratings yet

- May 2012Document8 pagesMay 2012stephen_wood_36No ratings yet

- 10 Key Trends Changing Inv MGMTDocument50 pages10 Key Trends Changing Inv MGMTcaitlynharveyNo ratings yet

- JPM Weekly MKT Recap 8-13-12Document2 pagesJPM Weekly MKT Recap 8-13-12Flat Fee PortfoliosNo ratings yet

- JPM Weekly MKT Recap 9-10-12Document2 pagesJPM Weekly MKT Recap 9-10-12Flat Fee PortfoliosNo ratings yet

- November 2011Document8 pagesNovember 2011stephen_wood_36No ratings yet

- 2012 Outlook: Australian Equity StrategyDocument36 pages2012 Outlook: Australian Equity StrategyLuke Campbell-Smith100% (1)

- File 1Document10 pagesFile 1Alberto VillalpandoNo ratings yet

- Fixed Income Is NecessaryDocument11 pagesFixed Income Is NecessaryAkshat TulsyanNo ratings yet

- Investment Process: Portfolio ConstructionDocument22 pagesInvestment Process: Portfolio ConstructionÃarthï ArülrãjNo ratings yet

- Weekly Market Commentary 3-512-2012Document4 pagesWeekly Market Commentary 3-512-2012monarchadvisorygroupNo ratings yet

- Group 24Document23 pagesGroup 24dineomokoena327No ratings yet

- 2009: A Tale of Two Halves: A Roadmap For The Global RecessionDocument12 pages2009: A Tale of Two Halves: A Roadmap For The Global RecessionsdNo ratings yet

- Weekly Market Commentary 03092015Document5 pagesWeekly Market Commentary 03092015dpbasicNo ratings yet

- CIMB-Principal Australian Equity Fund (Ex)Document2 pagesCIMB-Principal Australian Equity Fund (Ex)Pei ChinNo ratings yet

- IDFC Emergin Businesses NFODocument5 pagesIDFC Emergin Businesses NFOfinancialbondingNo ratings yet

- 2011-07-31 Brait Multi StrategyDocument2 pages2011-07-31 Brait Multi StrategykcousinsNo ratings yet

- Maverick Capital Q1 2011Document13 pagesMaverick Capital Q1 2011Yingluq100% (1)

- Goldman Sachs - MarketPulse - Special Edition - Ten For 2013Document3 pagesGoldman Sachs - MarketPulse - Special Edition - Ten For 2013cdietzrNo ratings yet

- Bond Market Perspectives 06092015Document4 pagesBond Market Perspectives 06092015dpbasicNo ratings yet

- Artemis Fund Managers Limited IncomeDocument14 pagesArtemis Fund Managers Limited IncomeAlviNo ratings yet

- Weekly Market Commentary 10-10-11Document3 pagesWeekly Market Commentary 10-10-11monarchadvisorygroupNo ratings yet

- Osku Ob Kid Save June 2013 FactsheetDocument3 pagesOsku Ob Kid Save June 2013 FactsheetRaymond Chan Chun LimNo ratings yet

- Quarterly Fund GuideDocument72 pagesQuarterly Fund GuideJohn SmithNo ratings yet

- Direct Factsheet July 12Document8 pagesDirect Factsheet July 12stephen_wood_36No ratings yet

- C Mmodity O: OutlookDocument36 pagesC Mmodity O: Outlookgaurav_agrawal_4No ratings yet

- JPM Weekly MKT Recap 3-05-12Document2 pagesJPM Weekly MKT Recap 3-05-12Flat Fee PortfoliosNo ratings yet

- JPM Weekly MKT Recap 10-15-12Document2 pagesJPM Weekly MKT Recap 10-15-12Flat Fee PortfoliosNo ratings yet

- JF Asia New Frontiers: Fund ObjectiveDocument1 pageJF Asia New Frontiers: Fund ObjectiveMd Saiful Islam KhanNo ratings yet

- JPM Weekly MKT Recap 2-27-12Document2 pagesJPM Weekly MKT Recap 2-27-12Flat Fee PortfoliosNo ratings yet

- Mfi 0516Document48 pagesMfi 0516StephNo ratings yet

- Sarasin EM Bond OutlookDocument20 pagesSarasin EM Bond OutlookabbdealsNo ratings yet

- Equity Strategy: The 5 Top Picks For FebruaryDocument26 pagesEquity Strategy: The 5 Top Picks For Februarymwrolim_01No ratings yet

- 209652CIMB Islamic DALI Equity Growth FundDocument2 pages209652CIMB Islamic DALI Equity Growth FundazmimdaliNo ratings yet

- The Case For Yield Investing: SchrodersDocument6 pagesThe Case For Yield Investing: SchrodersnigeltaylorNo ratings yet

- Security Bank - UITF Investment ReportDocument2 pagesSecurity Bank - UITF Investment ReportgwapongkabayoNo ratings yet

- AMANX FactSheetDocument2 pagesAMANX FactSheetMayukh RoyNo ratings yet

- JPMorgan Global Investment Banks 2010-09-08Document176 pagesJPMorgan Global Investment Banks 2010-09-08francoib991905No ratings yet

- CCT Ar-2015Document184 pagesCCT Ar-2015Sassy TanNo ratings yet

- JPM Weekly Market Recap October 10, 2011Document2 pagesJPM Weekly Market Recap October 10, 2011everest8848No ratings yet

- MR RIC EmergingMarketsEquityFund A enDocument2 pagesMR RIC EmergingMarketsEquityFund A enabandegenialNo ratings yet

- CORPFIN 7040: Fixed Income Securities (M) Embedded Research ProjectDocument12 pagesCORPFIN 7040: Fixed Income Securities (M) Embedded Research Project邓媛No ratings yet

- JPM Weekly MKT Recap 10-08-12Document2 pagesJPM Weekly MKT Recap 10-08-12Flat Fee PortfoliosNo ratings yet

- June 2012Document8 pagesJune 2012stephen_wood_36No ratings yet

- JPM Weekly MKT Recap 4-23-12Document2 pagesJPM Weekly MKT Recap 4-23-12Flat Fee PortfoliosNo ratings yet

- Jpmorgan Trust IIDocument180 pagesJpmorgan Trust IIgunjanbihaniNo ratings yet

- Raghuram Rajan - Fin Devt and RiskDocument20 pagesRaghuram Rajan - Fin Devt and Riska65b66incNo ratings yet

- Allan Gray Equity Fund: BenchmarkDocument2 pagesAllan Gray Equity Fund: Benchmarkapi-217792169No ratings yet

- Platform Factsheet Nov 2012Document7 pagesPlatform Factsheet Nov 2012stephen_wood_36No ratings yet

- 2022 Grade 10 Controlled Test 3 QP EngDocument5 pages2022 Grade 10 Controlled Test 3 QP EngkellzylesediNo ratings yet

- Offering Document: Management Company Alfalah GHP Investment Management LimitedDocument63 pagesOffering Document: Management Company Alfalah GHP Investment Management Limitedaslam_gheewalaNo ratings yet

- Company Secretary N.K.SinhaDocument4 pagesCompany Secretary N.K.SinhaMohit KeswaniNo ratings yet

- 2 Financial Marek T and ServicesDocument2 pages2 Financial Marek T and Servicesbhaskarganesh0% (1)

- SMB Foundation: Mon Tue Wed Thu FriDocument3 pagesSMB Foundation: Mon Tue Wed Thu FriSidharth GummallaNo ratings yet

- CFM Graph DataDocument11 pagesCFM Graph DataMohammed NazeerNo ratings yet

- Unit III MakroekonomiksDocument40 pagesUnit III MakroekonomiksLerton G. ClaudioNo ratings yet

- Notes - Investment Property BookDocument2 pagesNotes - Investment Property BookJake AustriaNo ratings yet

- Corp Fin Test PDFDocument6 pagesCorp Fin Test PDFRaghav JainNo ratings yet

- Module 12 - Investment PropertyDocument15 pagesModule 12 - Investment PropertyJehPoyNo ratings yet

- Taxsutra All Rights ReservedDocument8 pagesTaxsutra All Rights ReservedAlpa Shah DesaiNo ratings yet

- FINC1302 - Exer&Asgnt - Revised 5 Feb 2020Document24 pagesFINC1302 - Exer&Asgnt - Revised 5 Feb 2020faqehaNo ratings yet

- Chapte - 25 - InternationalDiversification FinanceDocument43 pagesChapte - 25 - InternationalDiversification FinanceKlajdPanariti100% (1)

- TELUS Corporation: Dividend Policy: Canadian Telecommunication IndustryDocument7 pagesTELUS Corporation: Dividend Policy: Canadian Telecommunication Industrymalaika12No ratings yet

- The 4 Pillars of Investing: Quick Reference ChecklistDocument5 pagesThe 4 Pillars of Investing: Quick Reference ChecklistAlex BirfaNo ratings yet

- Business Finance q2 Las w1Document47 pagesBusiness Finance q2 Las w1ggonegvft86% (7)

- Stock Brocking Industry ProfileDocument10 pagesStock Brocking Industry ProfilesaiyuvatechNo ratings yet

- Basics of Islamic BankingDocument186 pagesBasics of Islamic BankingFaryal JamilNo ratings yet

- Role of Commodity Exchange in Agricultural GrowthDocument63 pagesRole of Commodity Exchange in Agricultural GrowthSoumyalin Santy50% (2)

- Economics 2 (Money Banking and International Trade 1)Document22 pagesEconomics 2 (Money Banking and International Trade 1)Ankit AnandNo ratings yet

- Wyckoff Method and Cheat SheetDocument25 pagesWyckoff Method and Cheat SheetAhmad Azwar AmaladiNo ratings yet

- Wealth Insight - April 2024Document64 pagesWealth Insight - April 2024barundasaNo ratings yet

- Review of Session 2002-2003Document262 pagesReview of Session 2002-2003The Royal Society of EdinburghNo ratings yet

- DHL ExpressDocument32 pagesDHL ExpressGregory FrancoNo ratings yet

- Dividend Policy, Chapter 17Document22 pagesDividend Policy, Chapter 17202110782No ratings yet

- A Comparative Study of ELSSDocument4 pagesA Comparative Study of ELSSSilparajaNo ratings yet

- Ind Nifty CPSEDocument1 pageInd Nifty CPSEPrabhakar DalviNo ratings yet

- NISM Series X B-Investment Adviser Level 2 - New VersionDocument274 pagesNISM Series X B-Investment Adviser Level 2 - New VersionAlamgir HaqueNo ratings yet