Download as pptx, pdf, or txt

You might also like

- The Maid Sisekelo S3Document165 pagesThe Maid Sisekelo S3nhloniphointelligence82% (28)

- Golden Rule of InterpretationDocument8 pagesGolden Rule of InterpretationAparthiba DebrayNo ratings yet

- Over 4,000 Years Ago - HammurabiDocument102 pagesOver 4,000 Years Ago - HammurabigurudarshanNo ratings yet

- Jurisprudence On Liberality of RulesDocument2 pagesJurisprudence On Liberality of RulesLaurice PocaisNo ratings yet

- 3 Principles of InsuranceDocument15 pages3 Principles of InsuranceZerin Hossain100% (1)

- InsuranceDocument25 pagesInsuranceDeepansh GoyalNo ratings yet

- 9 Law of InsuranceDocument22 pages9 Law of InsuranceMaria U DavidNo ratings yet

- Chapter 19 Contract of InsuranceDocument12 pagesChapter 19 Contract of InsuranceKgotso JacobNo ratings yet

- Principles of InsuranceDocument33 pagesPrinciples of Insurancearrakib.semNo ratings yet

- Risk Management and Insurance STUDENTDocument50 pagesRisk Management and Insurance STUDENTHạnh Nhân VănNo ratings yet

- Module 3Document104 pagesModule 3VK GamerNo ratings yet

- Basics of InsuranceDocument26 pagesBasics of Insurancedranita@yahoo.comNo ratings yet

- Introduction To InsuranceDocument28 pagesIntroduction To Insurancearun jacobNo ratings yet

- Chapter 02 InsuranceDocument47 pagesChapter 02 InsuranceMd Rabbi KhanNo ratings yet

- Pbi Module 4Document25 pagesPbi Module 4SUBHECHHA MOHAPATRANo ratings yet

- Insurance IDocument30 pagesInsurance IpushkarNo ratings yet

- Principles of Insurance: IndemnityDocument27 pagesPrinciples of Insurance: IndemnitytaijulshadinNo ratings yet

- InsuranceDocument108 pagesInsurancesnehachandan91No ratings yet

- Basic Principles of Insurance Law New 1Document20 pagesBasic Principles of Insurance Law New 1Billiee ButccherNo ratings yet

- Chapter 1: Basics of Insurance: Let's BeginDocument27 pagesChapter 1: Basics of Insurance: Let's BeginAviNo ratings yet

- Chapter 1: Basics of Insurance: Let's BeginDocument27 pagesChapter 1: Basics of Insurance: Let's BeginDipesh ShuklaNo ratings yet

- Chapter 1: Basics of Insurance: Let's BeginDocument27 pagesChapter 1: Basics of Insurance: Let's BeginAviNo ratings yet

- Module:-1 Introduction To Life InsuranceDocument67 pagesModule:-1 Introduction To Life InsuranceMandy RandiNo ratings yet

- Insurance & Risk ManagementDocument43 pagesInsurance & Risk Managementsibananda patra100% (1)

- Insurance PlanningDocument18 pagesInsurance PlanningNeha SharmaNo ratings yet

- Chapter 2: Fundamentals of InsuranceDocument16 pagesChapter 2: Fundamentals of InsuranceFaye Nandini SalinsNo ratings yet

- Chapter 5 - Insurance LawDocument36 pagesChapter 5 - Insurance LawAnis AmirahNo ratings yet

- Unit III BoirmDocument58 pagesUnit III BoirmsatyavathiNo ratings yet

- Law of Insurance AnswersheetDocument55 pagesLaw of Insurance Answersheetkhatriparas71No ratings yet

- UNIT 3 InsuranceDocument10 pagesUNIT 3 InsuranceAroop PalNo ratings yet

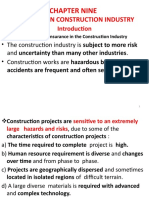

- Chapter Nine: Insurance in Construction IndustryDocument75 pagesChapter Nine: Insurance in Construction IndustryhNo ratings yet

- Nec 7 InsuranceDocument44 pagesNec 7 Insurancenishant khadkaNo ratings yet

- 1.property and PecuniaryDocument112 pages1.property and PecuniaryGashawNo ratings yet

- PPLI Mod 1 For StudentsDocument83 pagesPPLI Mod 1 For StudentsVISHAL BANSALNo ratings yet

- Aspects of Insurance LawDocument28 pagesAspects of Insurance Lawfelix robertNo ratings yet

- Essentials of An Insurance ContractDocument7 pagesEssentials of An Insurance ContractSameer JoshiNo ratings yet

- Bus Law Insu. PartDocument23 pagesBus Law Insu. PartBona IbrahimNo ratings yet

- History and Sources of Law of InsuranceDocument4 pagesHistory and Sources of Law of InsuranceMary-Lou Anne MohrNo ratings yet

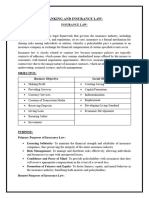

- Banking and InsuranceDocument15 pagesBanking and InsurancerichahcpatnaNo ratings yet

- Decision Theory 2Document31 pagesDecision Theory 2tage008No ratings yet

- Insurance and Assurance 5Document34 pagesInsurance and Assurance 5nrv2hcm25cNo ratings yet

- Insurance Act FinalDocument21 pagesInsurance Act FinalShrikant YadavNo ratings yet

- Chapter 3 - Principles of InsuranceDocument22 pagesChapter 3 - Principles of InsuranceAdam Sa'alpataNo ratings yet

- Insurance and Risk Management Unit IDocument9 pagesInsurance and Risk Management Unit Ipooranim1976No ratings yet

- Law of InsuranceDocument37 pagesLaw of InsuranceRaghavan CrsNo ratings yet

- Lesson Law of InsuranceDocument6 pagesLesson Law of Insurancegaurav94163No ratings yet

- Insurance Law in IndiaDocument44 pagesInsurance Law in IndiaVaibhav AhujaNo ratings yet

- Module V-2Document12 pagesModule V-2kashifidaplNo ratings yet

- CH 7 Insurance Law and Regulation 1Document35 pagesCH 7 Insurance Law and Regulation 1PUTTU GURU PRASAD SENGUNTHA MUDALIAR100% (1)

- HC 4.3: Financial Services: InsuranceDocument9 pagesHC 4.3: Financial Services: InsuranceAishwaryaNo ratings yet

- Insurance Code of The Philippines PD No. 1460, As Amended: July 26, 2012Document48 pagesInsurance Code of The Philippines PD No. 1460, As Amended: July 26, 2012Melissa M. Abansi-BautistaNo ratings yet

- Audit of Insurance CompaniesDocument5 pagesAudit of Insurance Companiesdavidkecelyn06No ratings yet

- Class Notes Part 3Document5 pagesClass Notes Part 3greatsali70No ratings yet

- Session 3-4Document16 pagesSession 3-4SARA KOSHY RCBSNo ratings yet

- Chapter Seven: Law of InsuranceDocument37 pagesChapter Seven: Law of InsuranceSirbela KedirNo ratings yet

- Unit 1 Introduction & Development of Insurance LawDocument174 pagesUnit 1 Introduction & Development of Insurance LawAnchalNo ratings yet

- Business Services - Part 3: ObjectivesDocument14 pagesBusiness Services - Part 3: ObjectivesSanta GlenmarkNo ratings yet

- InsuranceDocument7 pagesInsuranceraghunaikaNo ratings yet

- Insurance - Lecture 23Document13 pagesInsurance - Lecture 23MunyNo ratings yet

- Module 2 - General Principles of Insurance LawDocument60 pagesModule 2 - General Principles of Insurance Lawkumar kartikeyaNo ratings yet

- Summer Training Report: in Partial Fulfillment of The Requirements For The Award of The Degree ofDocument74 pagesSummer Training Report: in Partial Fulfillment of The Requirements For The Award of The Degree ofrahul19myNo ratings yet

- Detailed Notes On Insurance Law MIDSEM CHAP1-CHAP4Document6 pagesDetailed Notes On Insurance Law MIDSEM CHAP1-CHAP4deb.wns.graceNo ratings yet

- 2024 03 14 17 53 21Document6 pages2024 03 14 17 53 21nhloniphointelligenceNo ratings yet

- Statement of AccountDocument1 pageStatement of AccountnhloniphointelligenceNo ratings yet

- Memo SG 9.7 2023Document1 pageMemo SG 9.7 2023nhloniphointelligenceNo ratings yet

- Manchester City Financial Report 2022 23Document54 pagesManchester City Financial Report 2022 23nhloniphointelligenceNo ratings yet

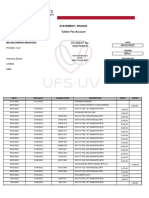

- Statement / Invoice Tuition Fee Account: Student No. 2023783075 28/02/2023Document3 pagesStatement / Invoice Tuition Fee Account: Student No. 2023783075 28/02/2023nhloniphointelligenceNo ratings yet

- Study Guide 6.6Document1 pageStudy Guide 6.6nhloniphointelligenceNo ratings yet

- MyDoc 1692012943798Document6 pagesMyDoc 1692012943798nhloniphointelligenceNo ratings yet

- PricelistDocument2 pagesPricelistnhloniphointelligenceNo ratings yet

- Forbidden Love Lwazi& LumiDocument801 pagesForbidden Love Lwazi& Luminhloniphointelligence0% (1)

- Money Can Bring Happiness or MiseryDocument1 pageMoney Can Bring Happiness or MiserynhloniphointelligenceNo ratings yet

- 2013 1 General Institutional Rules First Qualifications 1110 EngDocument87 pages2013 1 General Institutional Rules First Qualifications 1110 EngnhloniphointelligenceNo ratings yet

- Application For Leave/Commutation of Earned Leave: Asis A. NiñaDocument2 pagesApplication For Leave/Commutation of Earned Leave: Asis A. NiñaMario N. MariNo ratings yet

- 20.) Teehankee Vs MadayagDocument2 pages20.) Teehankee Vs MadayagEta CarineNo ratings yet

- School Timetable TemplateDocument1 pageSchool Timetable Templateraju bhowalNo ratings yet

- Liaison Office Guidelines PDFDocument3 pagesLiaison Office Guidelines PDFawellNo ratings yet

- Confirmation of Degree Form PDFDocument2 pagesConfirmation of Degree Form PDFlouis0% (2)

- Persistent Losses Prompt Ctas To Improvise: June 18, 2014Document12 pagesPersistent Losses Prompt Ctas To Improvise: June 18, 2014Allen FuchsNo ratings yet

- AccountingDocument4 pagesAccountingNicolas LuchmunNo ratings yet

- Free ConsentDocument5 pagesFree ConsentChetan NarasannavarNo ratings yet

- Kohl RauschDocument7 pagesKohl RauschFarhan Aamir BaigNo ratings yet

- Essay On Freedom Fighter: (Maulana Abul Kalam Azad)Document6 pagesEssay On Freedom Fighter: (Maulana Abul Kalam Azad)drmadankumarbnysNo ratings yet

- Procurement Guidelines 2018Document117 pagesProcurement Guidelines 2018janithbogahawattaNo ratings yet

- Diona v. BalangueDocument6 pagesDiona v. BalangueCharisma AclanNo ratings yet

- Dixon.2022 11 10 PDFDocument1 pageDixon.2022 11 10 PDFsherrieNo ratings yet

- gr34674 - Cruz V YoungbergDocument3 pagesgr34674 - Cruz V YoungbergmansikiaboNo ratings yet

- Etymology of CriminologyDocument11 pagesEtymology of CriminologyLoke DelacruzNo ratings yet

- Rajasthan Gramin Bank: Advertisement No. RGB 1/2010Document14 pagesRajasthan Gramin Bank: Advertisement No. RGB 1/2010addyjbsNo ratings yet

- CC 105 ModDocument10 pagesCC 105 ModPrecious Andoy-MegabonNo ratings yet

- (Finals) LTD 2021 Syllabus - LeyretanaDocument11 pages(Finals) LTD 2021 Syllabus - LeyretanaSabrina YuNo ratings yet

- Kelas XII News ItemDocument6 pagesKelas XII News ItemRahmatullah MuhammadNo ratings yet

- Travel ContactsDocument6 pagesTravel Contactsmeghnabhaduri100% (1)

- Integration SheetDocument68 pagesIntegration SheetMayank Shahabadee100% (1)

- Structural Dynamics - ESA 322 Lecture 2Document36 pagesStructural Dynamics - ESA 322 Lecture 2Purawin Subramaniam0% (1)

- Final Exam Answer Sheet International Investment (Dtue310) : Foreign Trade University HCMC CampusDocument6 pagesFinal Exam Answer Sheet International Investment (Dtue310) : Foreign Trade University HCMC CampusMai Lê Thị XuânNo ratings yet

- Torts CDocument55 pagesTorts CDickson Tk Chuma Jr.No ratings yet

- NLU Jodhpur GuidelinesDocument1 pageNLU Jodhpur GuidelinesShivaniNo ratings yet

- XXXX - Assessment Form (Comb)Document3 pagesXXXX - Assessment Form (Comb)muhammad fayzanNo ratings yet

- THE STATE v. KWAKU NKYIDocument4 pagesTHE STATE v. KWAKU NKYISolomon BoatengNo ratings yet

- AP Comparative Government: A Tale of Two SystemsDocument2 pagesAP Comparative Government: A Tale of Two SystemsNathaniel PiNo ratings yet