Download as ppt, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Ohada Accounting PlanDocument72 pagesOhada Accounting PlanNchendeh Christian100% (3)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- SAft Purchase AgreementDocument22 pagesSAft Purchase AgreementSong BAONo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Relaxing Credit Standards Regency Rug Repair Company Is Trying To Decide Whether It Should Relax Its Credit StandardsDocument3 pagesRelaxing Credit Standards Regency Rug Repair Company Is Trying To Decide Whether It Should Relax Its Credit StandardsBlair Bass0% (1)

- Law and Practice of International FinanceDocument9 pagesLaw and Practice of International FinanceCarlos Belando PastorNo ratings yet

- Astral Polytechnik LTD - HBJ Capital's 10in3 Stock For April'11Document46 pagesAstral Polytechnik LTD - HBJ Capital's 10in3 Stock For April'11HBJ Capital Services Private LimitedNo ratings yet

- Market Outlook Report - The Market & Business Cycles - Sept 2011 IssueDocument43 pagesMarket Outlook Report - The Market & Business Cycles - Sept 2011 IssueMahe PaliNo ratings yet

- HBJ Capital's - The Millionaire Portfolio (TMP) Update - Latest SampleDocument19 pagesHBJ Capital's - The Millionaire Portfolio (TMP) Update - Latest SampleHBJ Capital Services Private Limited100% (1)

- Camson Bio Tech (Multibagger) - HBJ Cap's 10in3: Best Buy Between Rs 30-40 & BelowDocument88 pagesCamson Bio Tech (Multibagger) - HBJ Cap's 10in3: Best Buy Between Rs 30-40 & BelowHBJ Capital Services Private Limited100% (7)

- HBJ Capitals - Street Smart (Indian Stock Market) - Aug08 Issue - Education Sector CoverageDocument33 pagesHBJ Capitals - Street Smart (Indian Stock Market) - Aug08 Issue - Education Sector CoverageHBJ Capital Services Private Limited100% (6)

- CAF3 BusinessLaw ExamSupplementDocument21 pagesCAF3 BusinessLaw ExamSupplementQwerty19oNo ratings yet

- WACC Form (THAI SET STOCK)Document47 pagesWACC Form (THAI SET STOCK)Kan LertvimolkasemNo ratings yet

- Strategy, Balanced Scorecard, and Strategic Profitability Analysis 13-1 13-2Document40 pagesStrategy, Balanced Scorecard, and Strategic Profitability Analysis 13-1 13-2Agisti RevianiNo ratings yet

- Syllabus Real Options AnalysisDocument4 pagesSyllabus Real Options AnalysisShayne LimNo ratings yet

- MBA-Financial and Managerial Accounting Question BankDocument87 pagesMBA-Financial and Managerial Accounting Question BankElroy Barry100% (3)

- 2019 12 13 - StatementDocument8 pages2019 12 13 - StatementMarisac MihaiNo ratings yet

- DFPRDocument10 pagesDFPRVish indianNo ratings yet

- Analysis Down Take PipeDocument4 pagesAnalysis Down Take Piperohit kumarNo ratings yet

- JP Morgan BacheletDocument4 pagesJP Morgan BacheletDiario ElMostrador.clNo ratings yet

- Balance of Payments TableDocument3 pagesBalance of Payments TableteetickNo ratings yet

- JD - Manager Project Accounting Analysis (Major Projects)Document2 pagesJD - Manager Project Accounting Analysis (Major Projects)icq4joyNo ratings yet

- Histori TransaksiDocument3 pagesHistori TransaksiAde Wardhana ChicharitoNo ratings yet

- S&P Agreement - SA708DDocument5 pagesS&P Agreement - SA708DJojo Al-hami Zurairi Y.MNo ratings yet

- Understanding Extension Risk in Hybrid Debt 1652456136Document7 pagesUnderstanding Extension Risk in Hybrid Debt 1652456136jack norburyNo ratings yet

- ME Module 5Document54 pagesME Module 5Mohammed nadeerNo ratings yet

- Test Bank For Introduction To Management Accounting 16th Edition Charles T HorngrenDocument24 pagesTest Bank For Introduction To Management Accounting 16th Edition Charles T HorngrenRebeccaMillerbtmq100% (49)

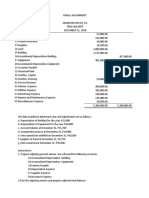

- Finals Assignment 1Document1 pageFinals Assignment 1Mary Kris CaparosoNo ratings yet

- Sale Under TpaDocument16 pagesSale Under Tpashubham100% (3)

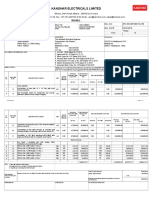

- Kanohar Electricals Limited: Ra BillDocument2 pagesKanohar Electricals Limited: Ra BillAnoop Dikshit100% (1)

- K.L.E.Society's College of Business Administration - BBA, HubliDocument21 pagesK.L.E.Society's College of Business Administration - BBA, HubliMahendr ChoudharyNo ratings yet

- Investors Guide To ImpactDocument21 pagesInvestors Guide To ImpactRobertNo ratings yet

- BFI Sample CommerceDocument24 pagesBFI Sample CommerceMAREESWARAN KNo ratings yet

- اسئلهIMA الهامهDocument31 pagesاسئلهIMA الهامهhmza_6No ratings yet

- Cost Accounting: Sixteenth Edition, Global EditionDocument32 pagesCost Accounting: Sixteenth Edition, Global EditionAhmed El KhateebNo ratings yet

- Long Examination in Mathematics in The Modern World (Finals) Name: SectionDocument3 pagesLong Examination in Mathematics in The Modern World (Finals) Name: SectionACE BRIANNo ratings yet

- Resume Weiting Hu 230606Document3 pagesResume Weiting Hu 230606api-634550315No ratings yet