Download as pptx, pdf, or txt

You might also like

- Sbi Fix Deposit SlipDocument1 pageSbi Fix Deposit SlipRahul Kumar83% (12)

- Capter 2Document5 pagesCapter 2DiwakarNo ratings yet

- Consulting Math DrillsDocument15 pagesConsulting Math DrillsHashaam Javed50% (2)

- Report Monika 29 Okt SD 13 Nov 2018Document1,219 pagesReport Monika 29 Okt SD 13 Nov 2018Aindra BudiarNo ratings yet

- Summary Economics of Money Banking and Financial Markets Frederic S Mishkin PDFDocument143 pagesSummary Economics of Money Banking and Financial Markets Frederic S Mishkin PDFJohn StephensNo ratings yet

- Introduction To Stock Markets: ZerodhaDocument104 pagesIntroduction To Stock Markets: ZerodhakosurugNo ratings yet

- Personal InvestmentDocument93 pagesPersonal InvestmentPratham Poovaiah MalavandaNo ratings yet

- US$ Millions, Except Number of Shares Which Are Reflected in Thousands and Per Share Amounts Consolidated Statement of OperationsDocument31 pagesUS$ Millions, Except Number of Shares Which Are Reflected in Thousands and Per Share Amounts Consolidated Statement of OperationsT CNo ratings yet

- Arogya Sanjeevani Policy - Premium ChartDocument5 pagesArogya Sanjeevani Policy - Premium ChartBalaNo ratings yet

- EMIDetailDocument6 pagesEMIDetailpramodkgowda3No ratings yet

- Target SPM PTM 2019 BanjarbaruDocument5 pagesTarget SPM PTM 2019 BanjarbaruSyarifah auliaNo ratings yet

- Rate Tabel Angsuran KSMDocument1 pageRate Tabel Angsuran KSMagengNo ratings yet

- Mitraguna Bsi - Bumn Promo Maret 2022Document1 pageMitraguna Bsi - Bumn Promo Maret 2022SukroNo ratings yet

- Mortgage Loan Schedule: Amount of Loan: Annual Percentage Rate: Monthly Payment TermsDocument24 pagesMortgage Loan Schedule: Amount of Loan: Annual Percentage Rate: Monthly Payment TermsNishant GoelNo ratings yet

- KTA Payroll 0.9%Document2 pagesKTA Payroll 0.9%akbars.thasimaNo ratings yet

- FIRE CalculatorDocument6 pagesFIRE CalculatorAbhijit BhowmickNo ratings yet

- Mymaxicare Rates 2021Document2 pagesMymaxicare Rates 2021Ariane ComboyNo ratings yet

- Rate KPR Danamon V 7.0 SingleDocument1 pageRate KPR Danamon V 7.0 SingleEka Wahyudi NggoheleNo ratings yet

- Smart Wealth InsuredDocument2 pagesSmart Wealth InsuredAshish RanjanNo ratings yet

- NPMP Rate Chart With GSTDocument2 pagesNPMP Rate Chart With GSTHIMANSHU SADANNo ratings yet

- RUSDocument1 pageRUSRoric ThomasNo ratings yet

- Loan Amort CalculatorDocument11 pagesLoan Amort CalculatorGeromil HernandezNo ratings yet

- Brosur Promo Mei 2023Document1 pageBrosur Promo Mei 2023Adiez AhmadiNo ratings yet

- Maths Investigation SpreadsheetDocument8 pagesMaths Investigation Spreadsheetmaddie.george020406No ratings yet

- Jeevan SaralDocument1 pageJeevan SaralHarish ChandNo ratings yet

- Jeevan SaralDocument1 pageJeevan SaralHarish ChandNo ratings yet

- Mymaxicare Rates 2022Document2 pagesMymaxicare Rates 2022Jako DeleonNo ratings yet

- Arogya Sanjeevani - Premium Chart Excl. GSTDocument5 pagesArogya Sanjeevani - Premium Chart Excl. GSTsonNo ratings yet

- Click Here 1Document1 pageClick Here 1ahemed122No ratings yet

- Emi CalculatorDocument10 pagesEmi CalculatormuraryNo ratings yet

- Tabelas LeisDocument5 pagesTabelas Leisp22sspamNo ratings yet

- Trading PlanDocument8 pagesTrading PlanAziz PradanaNo ratings yet

- Super Surplus PremiumDocument6 pagesSuper Surplus PremiumshreyashahNo ratings yet

- Executive Order No. 201 Salary Standardization LawDocument9 pagesExecutive Order No. 201 Salary Standardization LawDiosdado Cabo-Contiga AdolfoNo ratings yet

- Amount Borrowed Years Annual Rate Payment Months Beginning PMT Interest PrincipalDocument16 pagesAmount Borrowed Years Annual Rate Payment Months Beginning PMT Interest PrincipaldutchNo ratings yet

- ANGSURAN LENGKAP MitragunaDocument1 pageANGSURAN LENGKAP MitragunaOktiya SariNo ratings yet

- Trading Plan 100 Hari: Hari Modal Profit 10% Modal Akhir Rupiah Kurs 15,000Document3 pagesTrading Plan 100 Hari: Hari Modal Profit 10% Modal Akhir Rupiah Kurs 15,000Dani SetiawanNo ratings yet

- Time Is Our Friend: The Power of Compounding Tabel Ialpha-10% Invested End of Year AGE Amount BalanceDocument8 pagesTime Is Our Friend: The Power of Compounding Tabel Ialpha-10% Invested End of Year AGE Amount Balancebp3tki PontianakNo ratings yet

- Wa0035Document1 pageWa0035Nisaul karimahNo ratings yet

- Finance 2Document208 pagesFinance 2B SNo ratings yet

- TABEL Bank BJBS SyariahDocument1 pageTABEL Bank BJBS SyariahTommi YudhiantoNo ratings yet

- 2013 Assets Current AssetsDocument18 pages2013 Assets Current AssetsrosieNo ratings yet

- Tangsuran Mitraguna 2023Document1 pageTangsuran Mitraguna 2023M SalimNo ratings yet

- Consulta Amigable: Municipalidad PIA PIMDocument3 pagesConsulta Amigable: Municipalidad PIA PIMMiguel Carcausto VargasNo ratings yet

- Target PPSMDocument94 pagesTarget PPSMLucan MusicNo ratings yet

- Clim DayDocument6 pagesClim Daygiacomofrancesco2016No ratings yet

- Enter Your Monthly Saving AmountDocument17 pagesEnter Your Monthly Saving AmountHarish ChandNo ratings yet

- ASB SimulationDocument8 pagesASB SimulationZharfan MazliNo ratings yet

- Universal Sompo General Insurance Co LTD: Complete Healthcare Insurance UIN: UNIHLIP21409V022021Document10 pagesUniversal Sompo General Insurance Co LTD: Complete Healthcare Insurance UIN: UNIHLIP21409V022021Naveenraj SNo ratings yet

- Group 5Document14 pagesGroup 5Basmala IbrahimNo ratings yet

- AMHI - Easy HealthDocument16 pagesAMHI - Easy HealthRobin VermaNo ratings yet

- OT Assignment Subham 2Document19 pagesOT Assignment Subham 2S SubhamNo ratings yet

- Cement Grade Wise Report-2021-2022Document28 pagesCement Grade Wise Report-2021-2022fjohnmajorNo ratings yet

- ST BK of IndiaDocument10 pagesST BK of IndiangbopNo ratings yet

- EMIDetail 3Document14 pagesEMIDetail 3inland trustNo ratings yet

- PremiumChart CompleteHealthcareInsurance PDFDocument10 pagesPremiumChart CompleteHealthcareInsurance PDFgrr.homeNo ratings yet

- Universal Sompo General Insurance Co LTD: Complete Healthcare Insurance UIN: UNIHLIP14003V011314Document10 pagesUniversal Sompo General Insurance Co LTD: Complete Healthcare Insurance UIN: UNIHLIP14003V011314HarshaNo ratings yet

- Griya BSIDocument1 pageGriya BSIcvksielmumtazgroupNo ratings yet

- Lala Historical Results v5 UploadDocument20 pagesLala Historical Results v5 UploadRayados PittNo ratings yet

- IndusInd BankDocument10 pagesIndusInd Bankmovies bookNo ratings yet

- Food Cost DecemberDocument6 pagesFood Cost Decemberrezaakum13No ratings yet

- Currency ETFDocument1 pageCurrency ETFstrongasNo ratings yet

- Drinking Water and Sweeper and Home Guard ChargesDocument6 pagesDrinking Water and Sweeper and Home Guard ChargeschinkugargNo ratings yet

- Quiz - CashDocument1 pageQuiz - CashAna Mae HernandezNo ratings yet

- Xii Acc WS 3Document4 pagesXii Acc WS 3Gaytri ThaparNo ratings yet

- Advantages and Disadvantages of Equity SharesDocument2 pagesAdvantages and Disadvantages of Equity Sharespiyush chauhanNo ratings yet

- Hindu Marriage FormsDocument4 pagesHindu Marriage Formsgnsr_1984No ratings yet

- Banking PDFDocument37 pagesBanking PDFShahrukh MunirNo ratings yet

- Money - English Currency IIDocument55 pagesMoney - English Currency IIThe 18th Century Material Culture Resource Center100% (1)

- Statement of Cash FlowsDocument12 pagesStatement of Cash FlowsDaniel PeterNo ratings yet

- Quizesfm 2Document2 pagesQuizesfm 2Prince MalabaNo ratings yet

- 2021 RFP SlipDocument566 pages2021 RFP SlipRachel BongabongNo ratings yet

- Bond Value - YieldDocument40 pagesBond Value - YieldSheeza AshrafNo ratings yet

- The Analysis and Valuation of Bonds: Innovative Financial InstrumentsDocument42 pagesThe Analysis and Valuation of Bonds: Innovative Financial InstrumentsNathalie LeeNo ratings yet

- Section A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Document24 pagesSection A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Kenny HoNo ratings yet

- Capital StructureDocument44 pagesCapital StructureHardeep KaurNo ratings yet

- MIFA Chap 10Document17 pagesMIFA Chap 10aalomukherjeeNo ratings yet

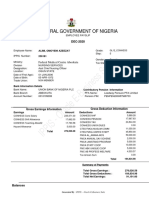

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument1 pageIPPIS - Oracle E-Business Suite: Federal Government of NigeriaAlimi kehinde100% (1)

- Fin C 000002Document14 pagesFin C 000002Nageshwar SinghNo ratings yet

- Simple Annuity: Learner's Module in General MathematicsDocument24 pagesSimple Annuity: Learner's Module in General MathematicsZack William100% (2)

- Downturn Upturn Expectations Consumption: Vocabulary 1: THE BUSINESS CYCLEDocument9 pagesDownturn Upturn Expectations Consumption: Vocabulary 1: THE BUSINESS CYCLEANH LƯƠNG NGUYỄN VÂNNo ratings yet

- LC PC ConfigurationDocument2 pagesLC PC ConfigurationmoorthykemNo ratings yet

- Fundamentals of Corporate Finance 9th Edition Brealey Test Bank 1Document36 pagesFundamentals of Corporate Finance 9th Edition Brealey Test Bank 1jillhernandezqortfpmndz100% (28)

- Estmt - 2023 10 19Document6 pagesEstmt - 2023 10 19lansingj48No ratings yet

- Problem Set 5 AnswersDocument2 pagesProblem Set 5 Answerssandrae brown100% (1)

- Accounting For Business Combination - CompressDocument17 pagesAccounting For Business Combination - CompressRonan Ian DinagtuanNo ratings yet

- Assignment #1 Tri Pack Film Limited: Analysis of Solvency RatiosDocument4 pagesAssignment #1 Tri Pack Film Limited: Analysis of Solvency RatiossooperusmanNo ratings yet

- Reviewer: Accounting For Partnership Part 2Document14 pagesReviewer: Accounting For Partnership Part 2gab mNo ratings yet

- Posada Corporation S Balance Sheet at December 31 2009 Is PresDocument1 pagePosada Corporation S Balance Sheet at December 31 2009 Is PresM Bilal SaleemNo ratings yet