Download as pptx, pdf, or txt

You might also like

- REM 106 Real Estate Planning and Development Final Examination August 14, 2021Document10 pagesREM 106 Real Estate Planning and Development Final Examination August 14, 2021Nicole CantosNo ratings yet

- The Legal and Professional Requirement For An AuditorDocument11 pagesThe Legal and Professional Requirement For An AuditorSenelwa AnayaNo ratings yet

- Chapter 3 Statutory AuditDocument23 pagesChapter 3 Statutory Auditsameed iqbalNo ratings yet

- AA NotesDocument130 pagesAA NotessandramariyadavisNo ratings yet

- Audit and AuditorsDocument14 pagesAudit and AuditorsRehanbhikanNo ratings yet

- Auditing&Assurance LL (Lesson2)Document13 pagesAuditing&Assurance LL (Lesson2)BRIAN KORIRNo ratings yet

- Chapter 6 Legal Requirements (Revised Notes and Case Studies)Document11 pagesChapter 6 Legal Requirements (Revised Notes and Case Studies)M Azeem IqbalNo ratings yet

- Acca f8ch3Document4 pagesAcca f8ch3luckyjulie567No ratings yet

- Audit I CH 2 Part IDocument67 pagesAudit I CH 2 Part IKalkayeNo ratings yet

- Aa CH02 2023-24Document22 pagesAa CH02 2023-24Linh Bùi Ngọc ThùyNo ratings yet

- Auditors' Responsibilities and Legal Liabilities (Chapter 5 of Arens)Document102 pagesAuditors' Responsibilities and Legal Liabilities (Chapter 5 of Arens)Wen Xin GanNo ratings yet

- Lecture 2-Auditor Liabilities-Jan 2020 1Document102 pagesLecture 2-Auditor Liabilities-Jan 2020 1Ching XueNo ratings yet

- M3-Audit PlanningDocument15 pagesM3-Audit PlanningSanjay PradhanNo ratings yet

- Lecture 2-Auditor Liabilities-JUNE 2023 RevisedDocument103 pagesLecture 2-Auditor Liabilities-JUNE 2023 RevisedSheany LinNo ratings yet

- Aa CH02 2023-24Document22 pagesAa CH02 2023-2421073134No ratings yet

- Auditing Unit-3Document11 pagesAuditing Unit-3swethaswetty06No ratings yet

- AA - SessionDocument8 pagesAA - SessionPraddy BrookNo ratings yet

- Rights and Privileges of ShareholdersDocument40 pagesRights and Privileges of Shareholdersswatantra.s887245No ratings yet

- Companies Act Provisions Relating To AuditsDocument43 pagesCompanies Act Provisions Relating To Auditsshaleenpatni100% (1)

- Lecture OneDocument32 pagesLecture OneNeha LalNo ratings yet

- Auditors and Audit Committee 2022Document47 pagesAuditors and Audit Committee 2022Sherry LaiNo ratings yet

- Audit Tutorial 2Document10 pagesAudit Tutorial 2Chong Soon Kai100% (1)

- Rule S Regulations 2Document11 pagesRule S Regulations 2Taimur ShahidNo ratings yet

- The Regulatory EnvironmentDocument16 pagesThe Regulatory EnvironmentmavhikalucksonprofaccNo ratings yet

- F8 Notes Acca NotesDocument10 pagesF8 Notes Acca NotesSehaj Mago100% (1)

- Corporate AdministrationDocument7 pagesCorporate AdministrationaliyahnicoleeeeNo ratings yet

- Lesson 2Document11 pagesLesson 2wambualucas74No ratings yet

- Regulation of Audit and Assurance Services Learning ObjectivesDocument5 pagesRegulation of Audit and Assurance Services Learning ObjectivesdayoNo ratings yet

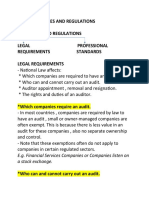

- E.G. Financial Services Companies or Companies Listen On A Stock ExchangeDocument6 pagesE.G. Financial Services Companies or Companies Listen On A Stock ExchangeFatemah MohamedaliNo ratings yet

- Appointment and Acceptance of AuditorsDocument27 pagesAppointment and Acceptance of AuditorsJonathan KyandoNo ratings yet

- Audit I - Chapter 2, Pt. I, The Auditing ProfessionDocument70 pagesAudit I - Chapter 2, Pt. I, The Auditing ProfessionAshenafiNo ratings yet

- Role of AuditorDocument5 pagesRole of AuditorHusnainShahid100% (1)

- Introduction To AuditingDocument7 pagesIntroduction To AuditingNishani WimalagunasekaraNo ratings yet

- Naresh Chandra Committee Report On Corporate Audit andDocument20 pagesNaresh Chandra Committee Report On Corporate Audit andHOD CommerceNo ratings yet

- Requirements For An AuditorDocument30 pagesRequirements For An AuditorNyaramba DavidNo ratings yet

- Auditors 28 Aug 12Document12 pagesAuditors 28 Aug 12Joseph SajiNo ratings yet

- UNEC TidualesDocument15 pagesUNEC TidualesTaKo TaKoNo ratings yet

- Chapter 6 Overview of Audit of Financial ReportDocument35 pagesChapter 6 Overview of Audit of Financial ReportLincoln KendeNo ratings yet

- Role of Auditor With-In A Company: AuditDocument6 pagesRole of Auditor With-In A Company: AuditUniq ManjuNo ratings yet

- The Institute of Chartered Accountants of Bangladesh Professional Stage: Knowledge Level Additional Sheet - Concept of and Need For AssuranceDocument4 pagesThe Institute of Chartered Accountants of Bangladesh Professional Stage: Knowledge Level Additional Sheet - Concept of and Need For AssuranceShahid MahmudNo ratings yet

- LAW485 Officers of The Company - AuditorDocument35 pagesLAW485 Officers of The Company - AuditorALIFP NAJMI SOFIANNo ratings yet

- Role of AuditorDocument6 pagesRole of AuditorSwastik GroverNo ratings yet

- Audit of Ultratech Cement LimitedDocument43 pagesAudit of Ultratech Cement Limitedpallavi21_1992No ratings yet

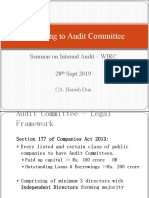

- Reporting To Audit Committee: Seminar On Internal Audit - WIRC 28 Sept 2019Document15 pagesReporting To Audit Committee: Seminar On Internal Audit - WIRC 28 Sept 2019Lakshmi Narayana Murthy KapavarapuNo ratings yet

- Naresh Chandra Commitee 2002 - Presentation To Be Taken For Class Seminar.Document26 pagesNaresh Chandra Commitee 2002 - Presentation To Be Taken For Class Seminar.sambhu_nNo ratings yet

- S2 - Rules and RegulationDocument5 pagesS2 - Rules and RegulationPham TungNo ratings yet

- F4 Chapter19Document31 pagesF4 Chapter19Husnain SattiNo ratings yet

- FIN301 - Week 09 - Auditors RoleDocument26 pagesFIN301 - Week 09 - Auditors RoleAhmed MunawarNo ratings yet

- Principles of Auditing - Chapter - 2Document33 pagesPrinciples of Auditing - Chapter - 2Wijdan Saleem EdwanNo ratings yet

- Discuss The Qualifications and Disqualifications of Auditor of The CompanyDocument9 pagesDiscuss The Qualifications and Disqualifications of Auditor of The CompanyDebabrata DasNo ratings yet

- Appointment of Auditors in PakistanDocument21 pagesAppointment of Auditors in PakistanSunaina ZakiNo ratings yet

- The CPA Profession: I Need Acpa !Document37 pagesThe CPA Profession: I Need Acpa !Nikhilesh ThakurNo ratings yet

- F8 Small NotesDocument22 pagesF8 Small NotesAnthimos Elia100% (1)

- F8 Notes - Chapter 2Document5 pagesF8 Notes - Chapter 2PEARL ANGELNo ratings yet

- I1.4 Auditing-AnswDocument16 pagesI1.4 Auditing-Answjbah saimon baptisteNo ratings yet

- Auditors and InvestigationDocument4 pagesAuditors and InvestigationSenelwa AnayaNo ratings yet

- PPA Notes Module 5Document42 pagesPPA Notes Module 5chethan jagadeeswaraNo ratings yet

- Audit Ethics and Regulations Prepared by Omnia HassanDocument22 pagesAudit Ethics and Regulations Prepared by Omnia HassanOmnia HassanNo ratings yet

- CH 1 (Audit)Document14 pagesCH 1 (Audit)UmerNo ratings yet

- Auditor of A CompanyDocument15 pagesAuditor of A CompanyPooja BoharaNo ratings yet

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- Pre-Advanced 1 - Final Written Test - Tipo BDocument5 pagesPre-Advanced 1 - Final Written Test - Tipo BJulia SantosNo ratings yet

- 78903567-Garga by GargacharyaDocument55 pages78903567-Garga by GargacharyaGirish BegoorNo ratings yet

- Hacking ICTDocument10 pagesHacking ICTHasalinda Noy IsmailNo ratings yet

- David v. Hall, 318 F.3d 343, 1st Cir. (2003)Document7 pagesDavid v. Hall, 318 F.3d 343, 1st Cir. (2003)Scribd Government DocsNo ratings yet

- Jeffrey DahmerDocument2 pagesJeffrey DahmerJef DunhamNo ratings yet

- Kunci Exercise More Reading PowerDocument2 pagesKunci Exercise More Reading PowerJefika LisusariraNo ratings yet

- A Multivariate Craniometric Study of TheDocument27 pagesA Multivariate Craniometric Study of TheNetupyr ImmfNo ratings yet

- Grant Thornton Tax Alert 2009 CIT FinalizationDocument2 pagesGrant Thornton Tax Alert 2009 CIT Finalizationngoba_cuongNo ratings yet

- Atwal Parole DocsDocument7 pagesAtwal Parole DocsCTV VancouverNo ratings yet

- Capital Asset Pricing Model: Objectives: After Reading This Chapter, You ShouldDocument17 pagesCapital Asset Pricing Model: Objectives: After Reading This Chapter, You ShouldGerrar10No ratings yet

- Mesthrie Origins of Fanagalo Part 1Document15 pagesMesthrie Origins of Fanagalo Part 1kayNo ratings yet

- Entrep Feasibility-AnalysisDocument8 pagesEntrep Feasibility-AnalysischllwithmeNo ratings yet

- Unit1. Economic EnvironmentDocument50 pagesUnit1. Economic EnvironmentAkshat YadavNo ratings yet

- Jumada Al-Awwal 1431 AH Prayer ScheduleDocument2 pagesJumada Al-Awwal 1431 AH Prayer SchedulemasjidibrahimNo ratings yet

- DH 2011 1008 Part A DCHB KishanganjDocument594 pagesDH 2011 1008 Part A DCHB Kishanganjaditi kaviwalaNo ratings yet

- Dekada '70 Reaction PaperDocument1 pageDekada '70 Reaction PaperSaxourie XiaoNo ratings yet

- Summary of Bank Niaga'S Case Study A. A Glance of Bank NiagaDocument4 pagesSummary of Bank Niaga'S Case Study A. A Glance of Bank Niagaaldiansyar mugiaNo ratings yet

- Seven Principles of PRDocument1 pageSeven Principles of PRAkshay ShettyNo ratings yet

- 2021 Association Implementation Report in GeorgiaDocument20 pages2021 Association Implementation Report in GeorgiaElmaddinNo ratings yet

- Allied Capital SDN BHD V Mohamed Latiff BinDocument10 pagesAllied Capital SDN BHD V Mohamed Latiff BinTee You WenNo ratings yet

- Debt and Equity FinancingDocument4 pagesDebt and Equity FinancingGrace MutheuNo ratings yet

- He Thong Phong Khong Viet NamDocument45 pagesHe Thong Phong Khong Viet NamminhcomputerNo ratings yet

- Vak Dec. '21 PDFDocument28 pagesVak Dec. '21 PDFMuralidharanNo ratings yet

- 2018 TheMathematicsOfThe - 5 Mies Van Der Rohe Caracteristics of The Free PlanDocument51 pages2018 TheMathematicsOfThe - 5 Mies Van Der Rohe Caracteristics of The Free Planvinicius carriãoNo ratings yet

- MA Reference CardsDocument12 pagesMA Reference CardsrpgnowsNo ratings yet

- Dr. Ram Manohar Lohia National Law University, Lucknow: Subject: Sociology Topic: Dr. Lohia and Socialism Final DraftDocument14 pagesDr. Ram Manohar Lohia National Law University, Lucknow: Subject: Sociology Topic: Dr. Lohia and Socialism Final Draftvikas rajNo ratings yet

- Bài Reading B Sung HP SauDocument23 pagesBài Reading B Sung HP SauTrangNo ratings yet

- Fostiima Business School Application ProcessDocument10 pagesFostiima Business School Application ProcessShashank KumarNo ratings yet

- Accounting Ratio For CHP 4Document5 pagesAccounting Ratio For CHP 4HtetThinzarNo ratings yet